Contemporary Issues in Accounting: AGL Energy Analysis

VerifiedAdded on 2023/06/09

|17

|2261

|331

Report

AI Summary

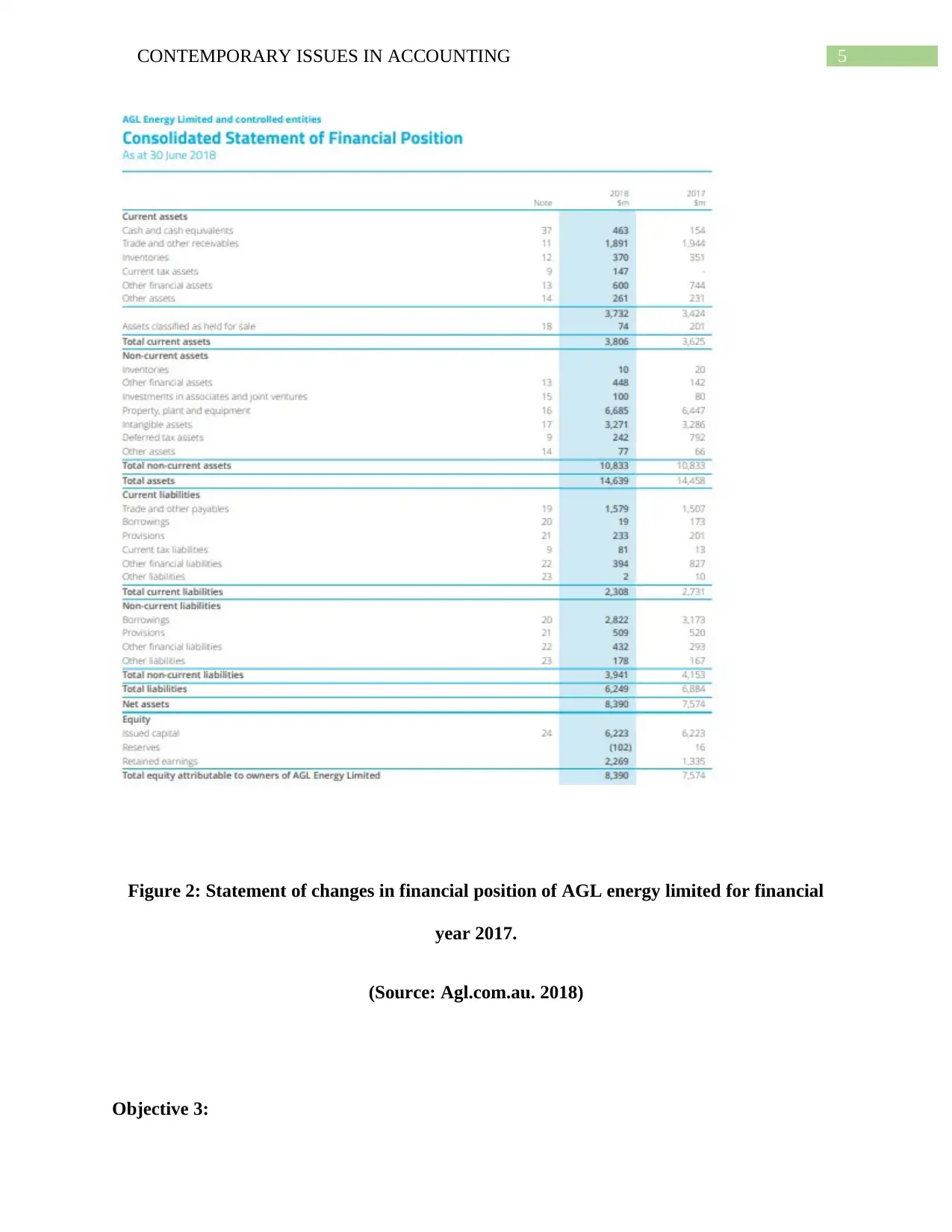

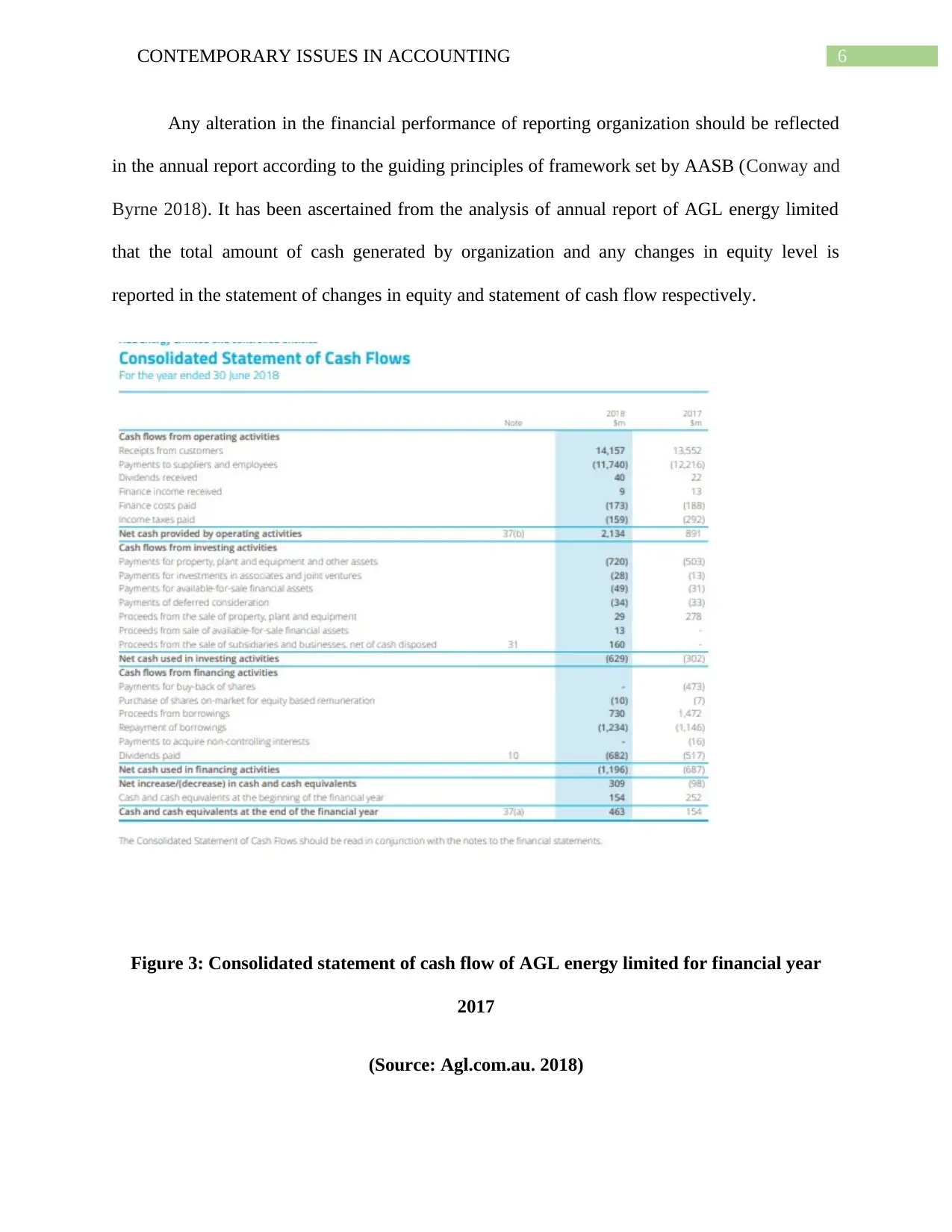

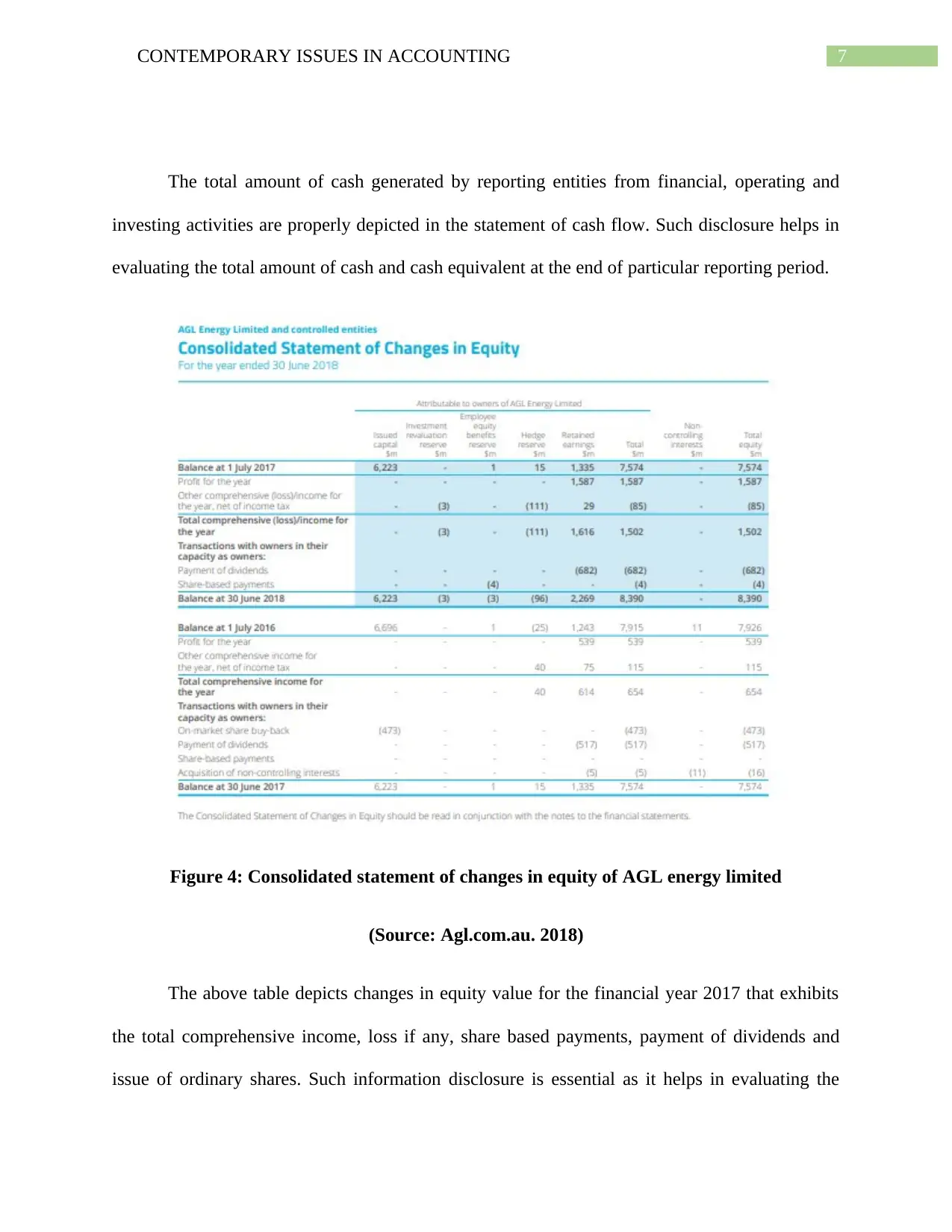

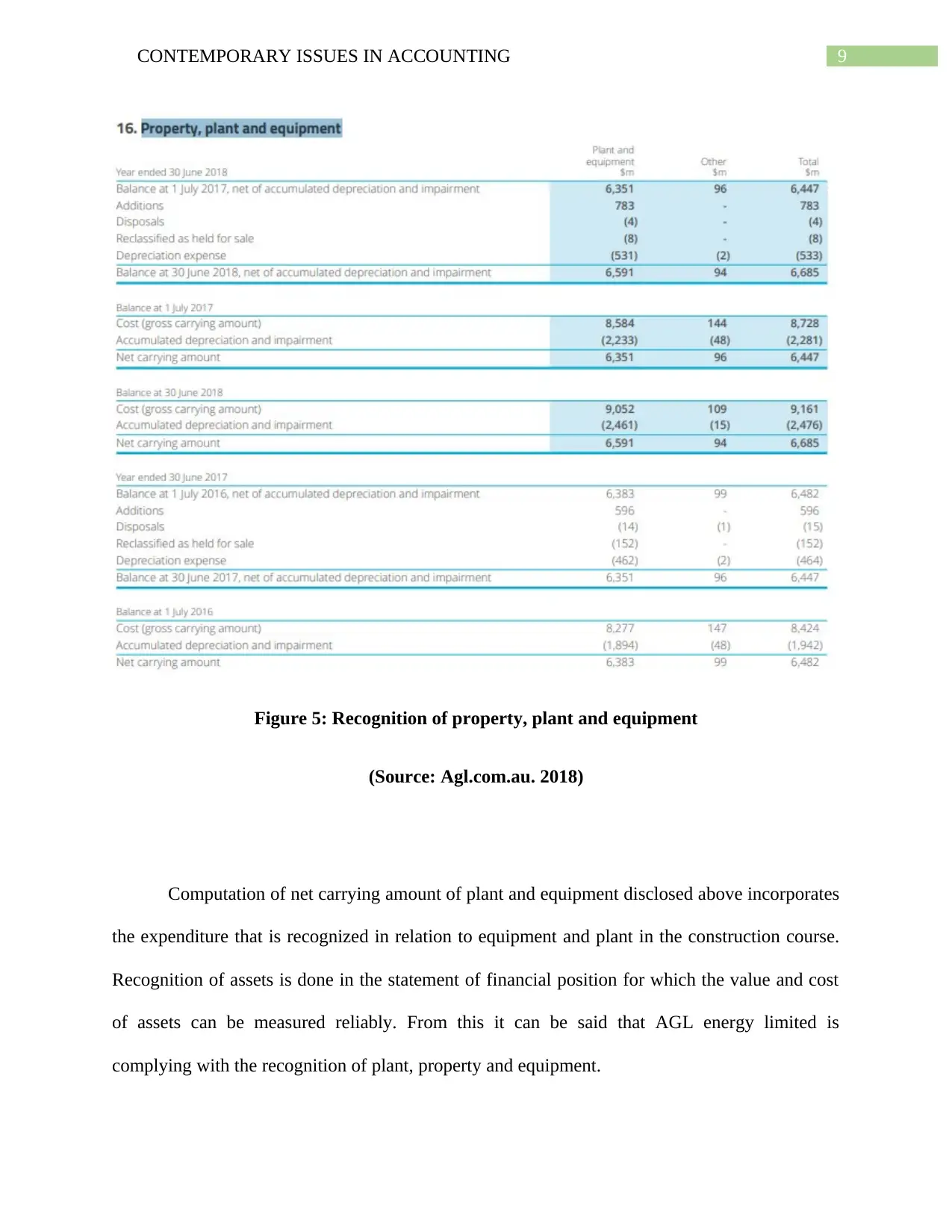

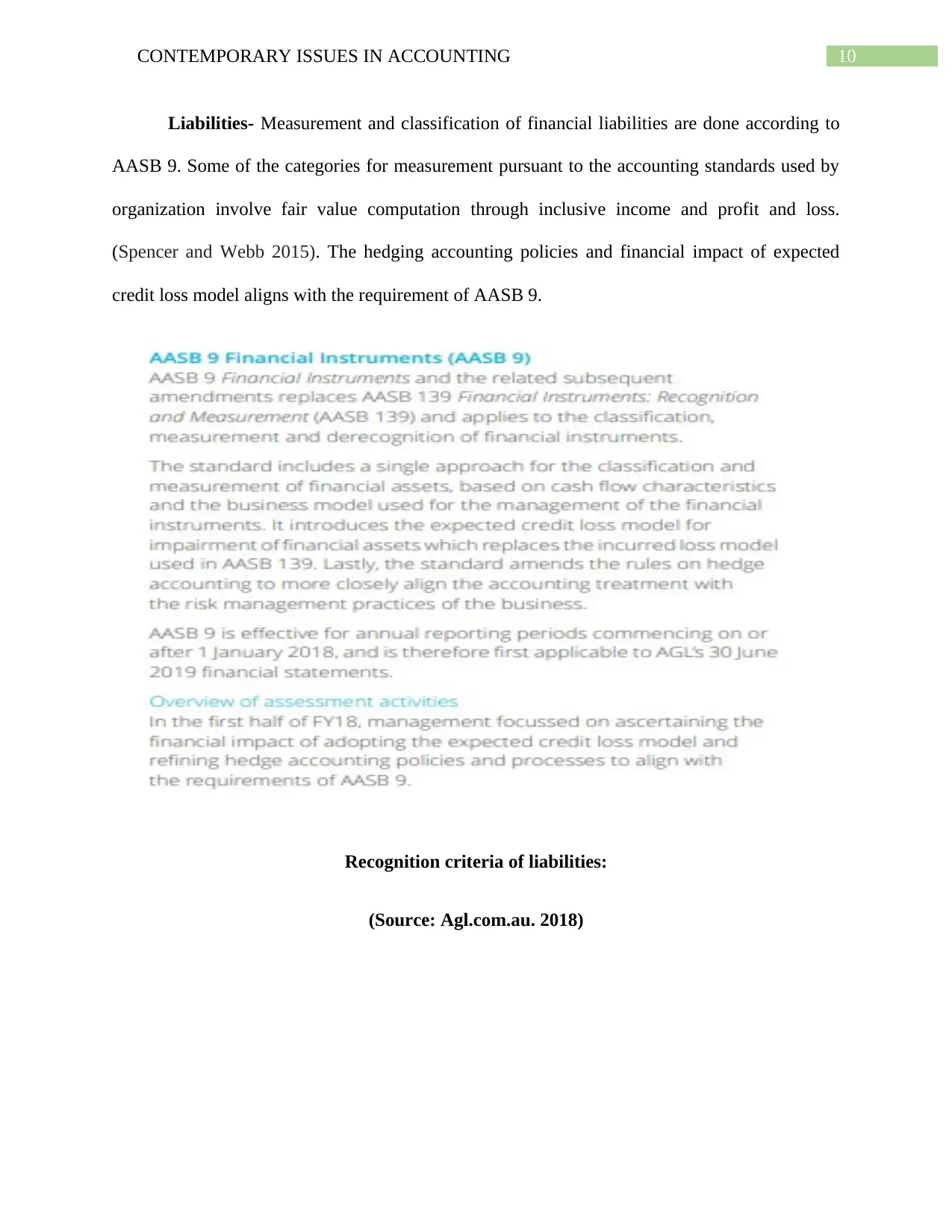

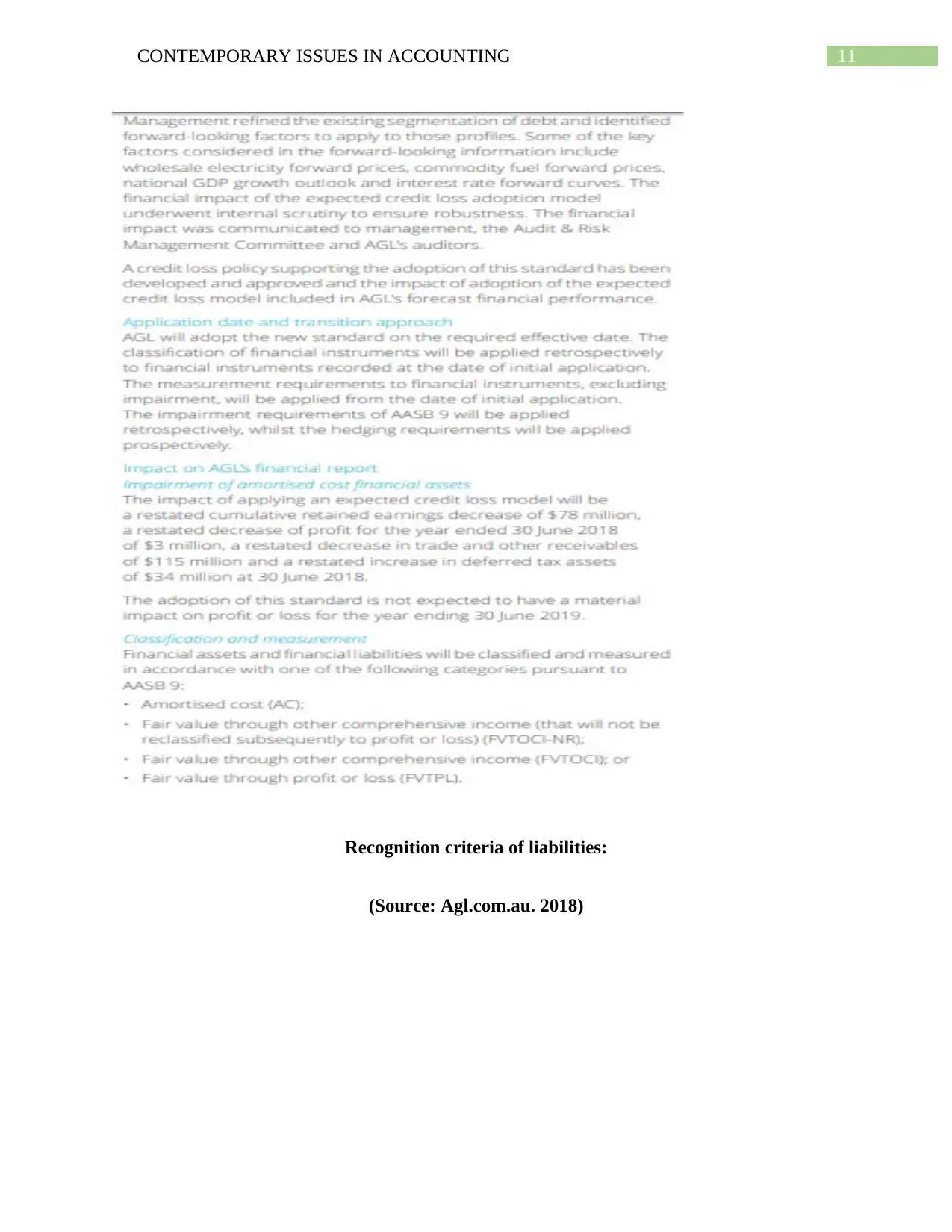

This report critically analyzes the financial reporting of AGL Energy Limited, evaluating its adherence to the conceptual framework of accounting. The report assesses whether AGL meets the objectives of general purpose financial reporting, providing relevant information for investors and resource contributors. It examines the recognition criteria for various financial statement elements, including assets, liabilities, expenses, and revenue, based on the AASB standards. Furthermore, the report explores both the fundamental and enhancing qualitative characteristics of financial reporting, such as relevance, faithfulness, timeliness, and understandability. The analysis utilizes AGL's annual report, providing evidence of compliance with accounting standards and offering recommendations for improved transparency and adherence to the conceptual framework.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.