Analysis of Accounting Conceptual Framework in Corporate Reporting

VerifiedAdded on 2020/03/04

|10

|1414

|188

Report

AI Summary

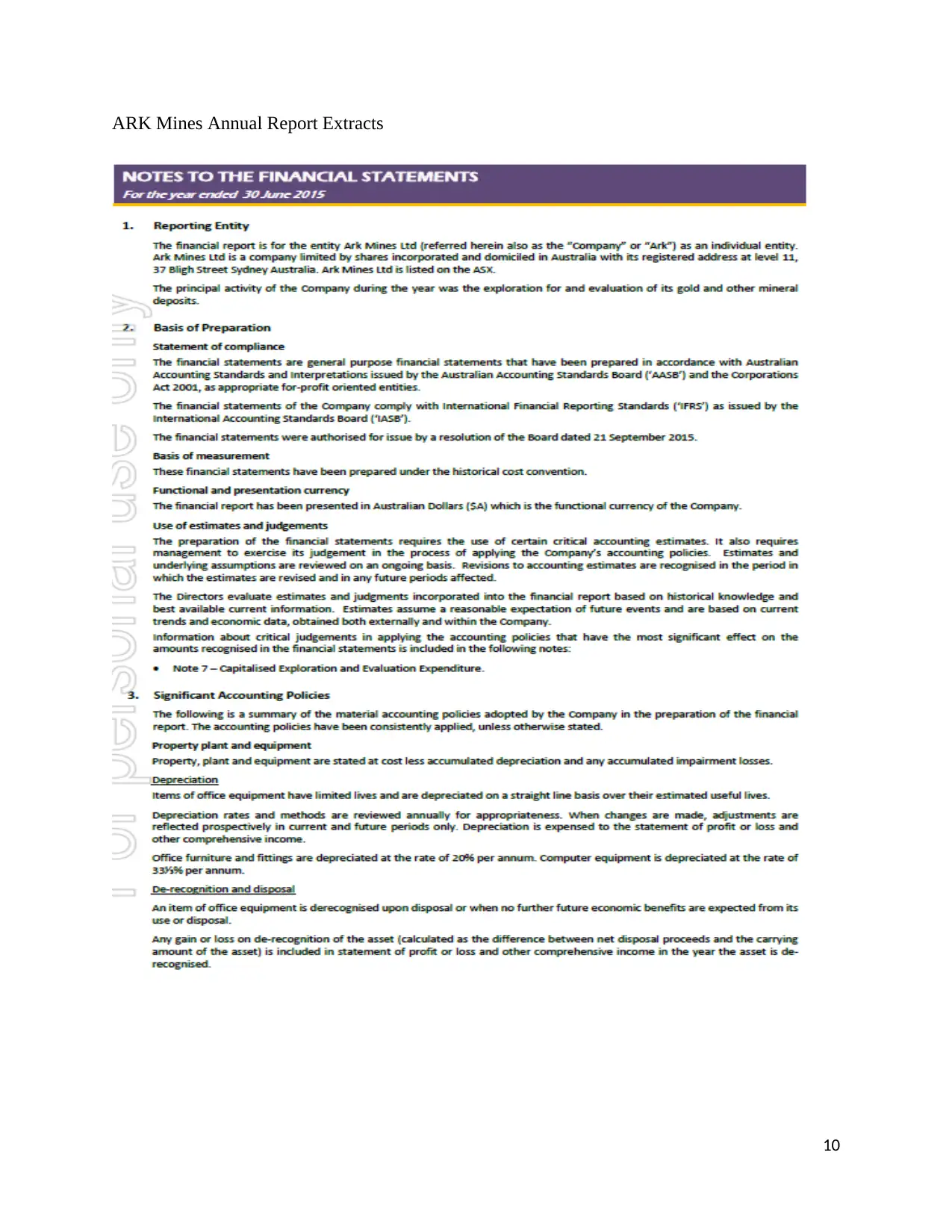

This report provides an executive summary and detailed analysis of the effectiveness of the current accounting conceptual framework in meeting the needs of financial report users. It evaluates the compliance of annual reports from Huon Aquaculture Group and ARK Mines, both listed on the ASX, with AASB standards and the conceptual framework. The report highlights the varying degrees of compliance between the two companies, attributing non-compliance to factors such as company size and stage of development. Furthermore, it discusses the reintroduction of prudence into the accounting conceptual framework to address disparities in corporate reporting and protect stakeholder interests. The analysis includes recommendations for improved compliance and transparency, emphasizing the importance of prudence in financial statement preparation. The report concludes with a comparison of financial reporting practices and the necessity of including prudence in the conceptual framework to prevent fraudulent activities.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.