ACCT20074: Contemporary Accounting - Financial Reporting Report

VerifiedAdded on 2023/04/04

|21

|4097

|486

Report

AI Summary

This report provides a comprehensive analysis of the Conceptual Framework (CF) for Financial Reporting, essential for enhancing financial statement assessments. Part A evaluates the CF and its application by the A2 milk company, examining how they use the system in making decisions of the fiscal reports. Part B compares the global integrated reporting framework with sustainability reporting conventions, assessing the limitations and strengths of traditional accounting in relation to the CF. The paper also includes a detailed examination of the CF's development, Australian accounting profession concerns, and academic viewpoints on its quality. Furthermore, the report analyzes the application of the CF by the A2 Milk Company, detailing its major components, measurement bases, recognition principles, and qualitative characteristics. Finally, the report will fundamentally analyse and assess the revealing operations of Shoprite Holding Ltd, on a record, opposed to the organization's integrated telecom.

Running head: CONTEMPORARY ACCOUNTING 1

Contemporary Accounting

Student’s Name

Professor’s Name

Institution Affiliation

Date

Contemporary Accounting

Student’s Name

Professor’s Name

Institution Affiliation

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING 2

1. Executive Summary

The Conceptual Framework (CF) is one of the basic bookkeeping parts which

basically upgrades assessments of budget reports. Conceptual Framework is somehow

relevant to analysts in distinguishing the objectives for organizations in a coordinated money

related report. In such manner, this examination, section A, gives a rating for Conceptual

Framework and A2 milk organization, in the purchaser essential segment, in how whey use

the system in making choices of the fiscal reports, conditions, and occasions, that are dared to

be accounted for or condensed. Part B of this paper looks at the worldwide incorporated

revealing framework against the supportability detailing convention, including the

investigation of the pertinent constraints and qualities of traditional bookkeeping in reference

to the calculated structure. To viably grasp the justification of this report, hypotheses will be

connected to delineate and characterize the supportability rules and incorporated announcing.

In conclusion, the paper will fundamentally analyse and assess the revealing operations of

Shoprite Holding Ltd, on a record, opposed to the organization's incorporated telecom.

1. Executive Summary

The Conceptual Framework (CF) is one of the basic bookkeeping parts which

basically upgrades assessments of budget reports. Conceptual Framework is somehow

relevant to analysts in distinguishing the objectives for organizations in a coordinated money

related report. In such manner, this examination, section A, gives a rating for Conceptual

Framework and A2 milk organization, in the purchaser essential segment, in how whey use

the system in making choices of the fiscal reports, conditions, and occasions, that are dared to

be accounted for or condensed. Part B of this paper looks at the worldwide incorporated

revealing framework against the supportability detailing convention, including the

investigation of the pertinent constraints and qualities of traditional bookkeeping in reference

to the calculated structure. To viably grasp the justification of this report, hypotheses will be

connected to delineate and characterize the supportability rules and incorporated announcing.

In conclusion, the paper will fundamentally analyse and assess the revealing operations of

Shoprite Holding Ltd, on a record, opposed to the organization's incorporated telecom.

CONTEMPORARY ACCOUNTING 3

2. Introduction

This structure's certification is commanded to display central ideas, which lie and

administer the introduction with the readiness of an organization's budget reports. These

records are used by outer clients, for example, the organization's partners, to plan a CF major

for money related assessment. In this manner, it is important to understand the documentation

serves a basic point of helping the IASB to define modified budgetary norms, which is

pertinent for fiscal summaries material by organizations when applying for money related

conventions or taking care of issues clear in the consistency exercises to explicit bookkeeping

principles. In such manner, this paper examines the calculated system purposed for budgetary

detailing with its importance and uses in some Australian Company, for example, The A2

milk organization. Secondly, the paper will assess supportability and incorporated revealing

structures material in one of South African’s companies such as Shoprite Holding Ltd.

3. Part A

a) Review of the history and development of the Conceptual Framework for

Financial Reporting

Advancement of Conceptual Framework began around 1976 in the UK, US and

internationally whereby it was presented in the United States by the FASB. The structure was

detailed as essential for using the important money-related guidelines and relieving the

present bookkeeping revealing issues. From 1978 to 2010, the administering element has

issued 8 bookkeeping proclamations with respect to the important budgetary detailing

connected by different organizations, which involves SFAC No. 4, that details applying to

non-enterprise endeavours. Be that as it may, No. 1, 2 and 3 SFACs have just been

supplanted, this leaves 5 as the substantial SFAC No. The announcement is that SFAC No. 4,

speaks to the late systems advised by the International Accounting Standards Committee

2. Introduction

This structure's certification is commanded to display central ideas, which lie and

administer the introduction with the readiness of an organization's budget reports. These

records are used by outer clients, for example, the organization's partners, to plan a CF major

for money related assessment. In this manner, it is important to understand the documentation

serves a basic point of helping the IASB to define modified budgetary norms, which is

pertinent for fiscal summaries material by organizations when applying for money related

conventions or taking care of issues clear in the consistency exercises to explicit bookkeeping

principles. In such manner, this paper examines the calculated system purposed for budgetary

detailing with its importance and uses in some Australian Company, for example, The A2

milk organization. Secondly, the paper will assess supportability and incorporated revealing

structures material in one of South African’s companies such as Shoprite Holding Ltd.

3. Part A

a) Review of the history and development of the Conceptual Framework for

Financial Reporting

Advancement of Conceptual Framework began around 1976 in the UK, US and

internationally whereby it was presented in the United States by the FASB. The structure was

detailed as essential for using the important money-related guidelines and relieving the

present bookkeeping revealing issues. From 1978 to 2010, the administering element has

issued 8 bookkeeping proclamations with respect to the important budgetary detailing

connected by different organizations, which involves SFAC No. 4, that details applying to

non-enterprise endeavours. Be that as it may, No. 1, 2 and 3 SFACs have just been

supplanted, this leaves 5 as the substantial SFAC No. The announcement is that SFAC No. 4,

speaks to the late systems advised by the International Accounting Standards Committee

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING 4

(IASC), which was created in the year 1973. it spoke to an antecedent element of the

bookkeeping models body all inclusive. By 2010, the bookkeeping substance (IASB)

accepted this job of IASC obliging itself in setting out the worldwide bookkeeping structures,

regardless of the present models being an acknowledgment to International Financial

Reporting Standards (IFRS) (Timbate and Park, 2018). This substance displayed its

underlying announcing of IAS in the year 1975, and spoke to the bookkeeping strategy

revelation (Crombie, 2012). By April 1989, IASC gave its 28th IAS, that spoke to budget

reports for interest in significant acquaintances.

All things considered, the reasonable structure produced for this introduction with the

arrangement of bookkeeping systems which was endorsed in April 1989 by the IASC. The

detailing was distributed in 1989 along this line and connected by IASB in the yeay 2001,

regardless of its importance in industrializing and defining IAS system. With the end goal of

deferred issuing of the standard, the key reason for the Conceptual Framework is to help the

budgetary element to figure International Accounting Standards later on; and permit surveys

for present Standards passages (IASB, B1713 and 2010b) meaning this structure.

This bookkeeping structure submitted itself to an understanding with the US’s FASB,

that alluded as second Norwalk Agreement in the year 2002, and ordering the two

bookkeeping elements could chiefly regard expelling the present contrasts with converge

basing on the applied structure of quality(Ehoff, 2010). as for the joint meeting that took

place in 2004, the bookkeeping bodies ( IASB and FASB) consented to incorporate individual

main segments and worries being an interlinked task to figure a solitary Conceptual

Framework. The activity is represented and built up dependent on the first FASB's reasonable

system and the IASB's structure. These two sheets used created system being an

establishment of their bookkeeping models of budgetary announcing.

(IASC), which was created in the year 1973. it spoke to an antecedent element of the

bookkeeping models body all inclusive. By 2010, the bookkeeping substance (IASB)

accepted this job of IASC obliging itself in setting out the worldwide bookkeeping structures,

regardless of the present models being an acknowledgment to International Financial

Reporting Standards (IFRS) (Timbate and Park, 2018). This substance displayed its

underlying announcing of IAS in the year 1975, and spoke to the bookkeeping strategy

revelation (Crombie, 2012). By April 1989, IASC gave its 28th IAS, that spoke to budget

reports for interest in significant acquaintances.

All things considered, the reasonable structure produced for this introduction with the

arrangement of bookkeeping systems which was endorsed in April 1989 by the IASC. The

detailing was distributed in 1989 along this line and connected by IASB in the yeay 2001,

regardless of its importance in industrializing and defining IAS system. With the end goal of

deferred issuing of the standard, the key reason for the Conceptual Framework is to help the

budgetary element to figure International Accounting Standards later on; and permit surveys

for present Standards passages (IASB, B1713 and 2010b) meaning this structure.

This bookkeeping structure submitted itself to an understanding with the US’s FASB,

that alluded as second Norwalk Agreement in the year 2002, and ordering the two

bookkeeping elements could chiefly regard expelling the present contrasts with converge

basing on the applied structure of quality(Ehoff, 2010). as for the joint meeting that took

place in 2004, the bookkeeping bodies ( IASB and FASB) consented to incorporate individual

main segments and worries being an interlinked task to figure a solitary Conceptual

Framework. The activity is represented and built up dependent on the first FASB's reasonable

system and the IASB's structure. These two sheets used created system being an

establishment of their bookkeeping models of budgetary announcing.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING 5

b) Explanation of Australian accounting profession’s concerns regarding

Conceptual Framework

Australian bookkeeping calling keeps alternating interest in regards to Conceptual

Framework. In Australia, Quasi-enactment signifies that the need for the Constitution-

focused Conceptual Framework makes it difficult to guarantee that the archived bookkeeping

systems have been planned sensibly and are steady. Regardless of the way that apparently it is

helpful to assess the basics of bookkeeping in the term 'targets' of the applicable bookkeeping

articulations, the callings guarantees that this detachment of the principles has introduced

progressively potential bookkeeping matters. All things considered, the so called Australian

Accounting Profession is somehow increasingly troubled with sorting of CF capacities rather

than its destinations in the assessment of an element's budget summaries. This further

suggests the callings at present refuse the remark and thinking ideas of CF based on

bookkeeping 'targets' in the assessment of budget reports. The principle explanation behind

this is the presence of encouraged to build up the supporting bookkeeping structures wavers

transient bookkeeping destinations.

c) Discussion of academic’s concerns about the quality (potential benefits and

limitations) of the Conceptual Framework

CF has possible merits and confinements looking upon as scholarly interests. All things

considered, these are the advantages obvious after presentation of the system in this

bookkeeping business.

● Scholarly is worried about bookkeeping rationale and consistency, which infers that

bookkeeping measures built up following the utilization of CF ought to be intelligent

and predictable.

b) Explanation of Australian accounting profession’s concerns regarding

Conceptual Framework

Australian bookkeeping calling keeps alternating interest in regards to Conceptual

Framework. In Australia, Quasi-enactment signifies that the need for the Constitution-

focused Conceptual Framework makes it difficult to guarantee that the archived bookkeeping

systems have been planned sensibly and are steady. Regardless of the way that apparently it is

helpful to assess the basics of bookkeeping in the term 'targets' of the applicable bookkeeping

articulations, the callings guarantees that this detachment of the principles has introduced

progressively potential bookkeeping matters. All things considered, the so called Australian

Accounting Profession is somehow increasingly troubled with sorting of CF capacities rather

than its destinations in the assessment of an element's budget summaries. This further

suggests the callings at present refuse the remark and thinking ideas of CF based on

bookkeeping 'targets' in the assessment of budget reports. The principle explanation behind

this is the presence of encouraged to build up the supporting bookkeeping structures wavers

transient bookkeeping destinations.

c) Discussion of academic’s concerns about the quality (potential benefits and

limitations) of the Conceptual Framework

CF has possible merits and confinements looking upon as scholarly interests. All things

considered, these are the advantages obvious after presentation of the system in this

bookkeeping business.

● Scholarly is worried about bookkeeping rationale and consistency, which infers that

bookkeeping measures built up following the utilization of CF ought to be intelligent

and predictable.

CONTEMPORARY ACCOUNTING 6

● Since numerous countries have set up CF, which is comparable comprehensively (or

might have on the other hand received the IASC structures), there is the requirement

for nations to grasp significant worldwide similarity based on different bookkeeping

gauges (Prosic, 2015). All things considered, scholarly worry on value highlights on

the standard's equivalence and inconsistency over the worldwide money related

revealing (whereby callings contends that it is pertinent for the assessment of remote

venture capitals and streams.

● CF gives the worldwide essentials of bookkeeping frameworks. All things considered,

the quality-setters are relied upon as being responsible for their monetary choices

(Romolini, Fissi and Gori, 2017). On the off chance that choices are found from main

distressed assessed in the CF, the bookkeeping callings anticipate that the benchmarks

should be clear in this manner requiring more clarification preceding the usage.

● The CF sets up a fitting approach to imparting the major ideas dependent on the

present money related reports. Along these lines, this system gives the best direction

to substances to provide details regarding specific bookkeeping measures and

assessment of any money related distress (Crombie, 2012).

● Accounting-setters will encounter negligible opinion weight at a time of the definition

of additionally bookkeeping measures because the significant distress such as the

targets of monetary records, the paradigm to acknowledgment have been viewed as

because of the foundation of CF.

Some of the confinements which have been identified with reasonable systems of accounting

are:

● Abstract structures are ridiculous in defining.

● Since numerous countries have set up CF, which is comparable comprehensively (or

might have on the other hand received the IASC structures), there is the requirement

for nations to grasp significant worldwide similarity based on different bookkeeping

gauges (Prosic, 2015). All things considered, scholarly worry on value highlights on

the standard's equivalence and inconsistency over the worldwide money related

revealing (whereby callings contends that it is pertinent for the assessment of remote

venture capitals and streams.

● CF gives the worldwide essentials of bookkeeping frameworks. All things considered,

the quality-setters are relied upon as being responsible for their monetary choices

(Romolini, Fissi and Gori, 2017). On the off chance that choices are found from main

distressed assessed in the CF, the bookkeeping callings anticipate that the benchmarks

should be clear in this manner requiring more clarification preceding the usage.

● The CF sets up a fitting approach to imparting the major ideas dependent on the

present money related reports. Along these lines, this system gives the best direction

to substances to provide details regarding specific bookkeeping measures and

assessment of any money related distress (Crombie, 2012).

● Accounting-setters will encounter negligible opinion weight at a time of the definition

of additionally bookkeeping measures because the significant distress such as the

targets of monetary records, the paradigm to acknowledgment have been viewed as

because of the foundation of CF.

Some of the confinements which have been identified with reasonable systems of accounting

are:

● Abstract structures are ridiculous in defining.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING 7

● Legislative activities have influenced the improvement of the CF. As a result of this, a

few bookkeepers have the worry that CF is increasingly disposed to opinion

methodology.

● As per the impediment delineated above, at whatever point the CF considers including

bookkeeping worries, dependably issues are there for money related approximation of

resources as contended by (Molyneux and Wilson, 2017).

● CFs distresses more on most issues related to money. All things considered, this

system will consider ignoring different execution fragments, for example, biological

and social uncovering parts. More so, CFs fundamentally travels the thought of

monetary examiners dependent on corporate execution according to the assessment of

monetary fund execution,.

d) Explanation of how the conceptual framework has been applied by the selected

Australian Company

(i) major components and the number of reports/statements that have been according to

the Conceptual Framework

● Legislative activities have influenced the improvement of the CF. As a result of this, a

few bookkeepers have the worry that CF is increasingly disposed to opinion

methodology.

● As per the impediment delineated above, at whatever point the CF considers including

bookkeeping worries, dependably issues are there for money related approximation of

resources as contended by (Molyneux and Wilson, 2017).

● CFs distresses more on most issues related to money. All things considered, this

system will consider ignoring different execution fragments, for example, biological

and social uncovering parts. More so, CFs fundamentally travels the thought of

monetary examiners dependent on corporate execution according to the assessment of

monetary fund execution,.

d) Explanation of how the conceptual framework has been applied by the selected

Australian Company

(i) major components and the number of reports/statements that have been according to

the Conceptual Framework

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING 8

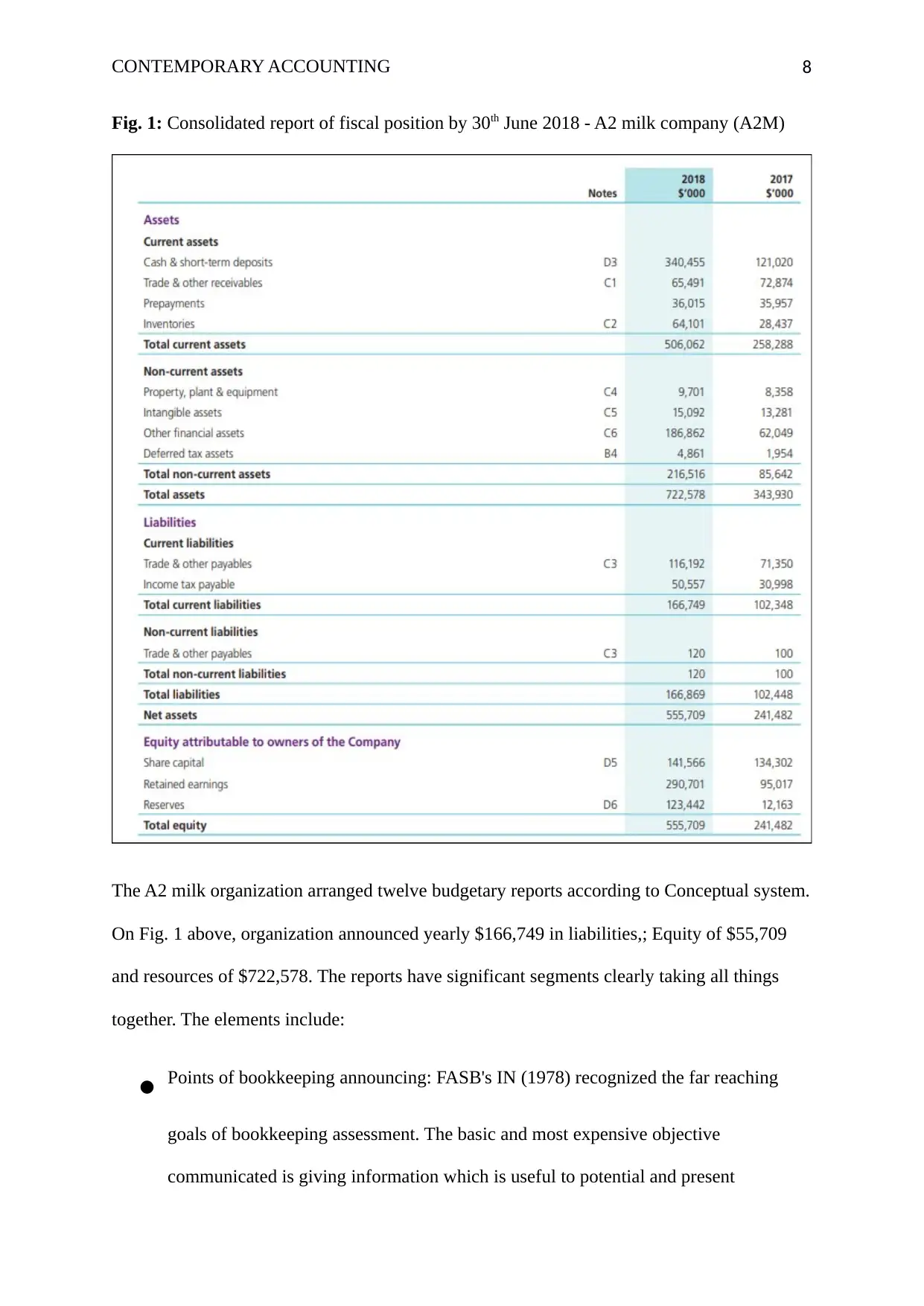

Fig. 1: Consolidated report of fiscal position by 30th June 2018 - A2 milk company (A2M)

The A2 milk organization arranged twelve budgetary reports according to Conceptual system.

On Fig. 1 above, organization announced yearly $166,749 in liabilities,; Equity of $55,709

and resources of $722,578. The reports have significant segments clearly taking all things

together. The elements include:

● Points of bookkeeping announcing: FASB's IN (1978) recognized the far reaching

goals of bookkeeping assessment. The basic and most expensive objective

communicated is giving information which is useful to potential and present

Fig. 1: Consolidated report of fiscal position by 30th June 2018 - A2 milk company (A2M)

The A2 milk organization arranged twelve budgetary reports according to Conceptual system.

On Fig. 1 above, organization announced yearly $166,749 in liabilities,; Equity of $55,709

and resources of $722,578. The reports have significant segments clearly taking all things

together. The elements include:

● Points of bookkeeping announcing: FASB's IN (1978) recognized the far reaching

goals of bookkeeping assessment. The basic and most expensive objective

communicated is giving information which is useful to potential and present

CONTEMPORARY ACCOUNTING 9

examiners and various customers in coming up with the fair endeavor, approval, and

equivalent decisions. As for this beginning stage, the A2M conveyed more logically

express targets.

● importance of Expedient Financial Information: The following part in applied

structure are qualities or abstract characteristics that monetary fund information

should have if it is of importance in essential authority. In SFAC 2, the FASB stated

that data is important when is (I) significant, (ii) commensurate, and (iii) reliable

(Carnevale and Mazzuca, 2012). Information is appropriate if it has any sort of impact

in making decisions. The quality of information can be rated when it empowers

consumers to evaluate the past and envision the future and is found to impact their

decisions.

● Fundamentals for Financial Statement. The other critical progression in structuring up

an applied system is choosing the segments of spending records. It incorporates

portraying categories of A2M's data which should be contained in money related

records. FASB's trade of monetary synopsis segments fuses implications of

noteworthy segments, for instance, assets, liabilities, esteem, livelihoods, costs,

increments, and incidents (Crombie, 2012).

Monetary Recognition and Measurement: In the SFAC 5, Estimation and Affirmation in

Fiscal synopses of Enterprise Ventures', FASB sets up thoughts for picking (1) at a time when

things should be presented in spending outlines, and (2) how to dispense numbers to money

related things.

(ii) Measurement bases and recognition principles which have been applied for liabilities,

revenue, and assets.

examiners and various customers in coming up with the fair endeavor, approval, and

equivalent decisions. As for this beginning stage, the A2M conveyed more logically

express targets.

● importance of Expedient Financial Information: The following part in applied

structure are qualities or abstract characteristics that monetary fund information

should have if it is of importance in essential authority. In SFAC 2, the FASB stated

that data is important when is (I) significant, (ii) commensurate, and (iii) reliable

(Carnevale and Mazzuca, 2012). Information is appropriate if it has any sort of impact

in making decisions. The quality of information can be rated when it empowers

consumers to evaluate the past and envision the future and is found to impact their

decisions.

● Fundamentals for Financial Statement. The other critical progression in structuring up

an applied system is choosing the segments of spending records. It incorporates

portraying categories of A2M's data which should be contained in money related

records. FASB's trade of monetary synopsis segments fuses implications of

noteworthy segments, for instance, assets, liabilities, esteem, livelihoods, costs,

increments, and incidents (Crombie, 2012).

Monetary Recognition and Measurement: In the SFAC 5, Estimation and Affirmation in

Fiscal synopses of Enterprise Ventures', FASB sets up thoughts for picking (1) at a time when

things should be presented in spending outlines, and (2) how to dispense numbers to money

related things.

(ii) Measurement bases and recognition principles which have been applied for liabilities,

revenue, and assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ACCOUNTING 10

Normally, FASB has most times stated that things should be seen in a monetary synopses if

they meet the criteria: Definitions: if these things meet the importance of a segment of

spending records; Measurability: if they have significant qualities that are quantifiable with

sufficient constancy; Importance: if the information about them is prepared in having any

impact on customer decisions; and lastly Reliability: if the A2M's information is explanatory,

undaunted, verifiable, and fair.

In the SFAC 5, the FASB has elastrated that a whole course of action of spending rundowns

ought to show up: Money related grounds around the completion of the time, Exhaustive pay

for times and Profit for period. The thought which is new and broader compared to benefit

and consolidates all changes in owners' esteem and not those that came about as a result of

trades to the owners (Hodge, Rajgopal and Shevlin, 2009). Some changes in asset regards are

consolidated by this thought anyway are expelled from A2M pay.

(iii) Qualitative distinctive of data that display in different financial reports of a company

Operating of the abstract properties: To manufacture an approximation contraption, there is

utilization of prior composition that describes cash affiliated enumerating quality to the extent

the vital and updating emotional traits crucial decision comfort as portrayed in the ED. The

essential emotional characteristics (for instance criticalness and faithful depiction) which are

noteworthy and choose the matter of cash affiliated enumerating information (Alfiero, Cane,

Doronzo and Esposito, 2018). The rising abstract traits (for instance equality, get capacity,

common sense, and verifiable status) can improve decision esteem when the critical

emotional qualities are set up. In any case, they can't choose bookkeeping enumerating

quality isolated.

Importance: 'Centrality' highlight of the organization alludes to its ability to fathom different

distress raised by customers since they provide capital in the organization. Thinking about the

Normally, FASB has most times stated that things should be seen in a monetary synopses if

they meet the criteria: Definitions: if these things meet the importance of a segment of

spending records; Measurability: if they have significant qualities that are quantifiable with

sufficient constancy; Importance: if the information about them is prepared in having any

impact on customer decisions; and lastly Reliability: if the A2M's information is explanatory,

undaunted, verifiable, and fair.

In the SFAC 5, the FASB has elastrated that a whole course of action of spending rundowns

ought to show up: Money related grounds around the completion of the time, Exhaustive pay

for times and Profit for period. The thought which is new and broader compared to benefit

and consolidates all changes in owners' esteem and not those that came about as a result of

trades to the owners (Hodge, Rajgopal and Shevlin, 2009). Some changes in asset regards are

consolidated by this thought anyway are expelled from A2M pay.

(iii) Qualitative distinctive of data that display in different financial reports of a company

Operating of the abstract properties: To manufacture an approximation contraption, there is

utilization of prior composition that describes cash affiliated enumerating quality to the extent

the vital and updating emotional traits crucial decision comfort as portrayed in the ED. The

essential emotional characteristics (for instance criticalness and faithful depiction) which are

noteworthy and choose the matter of cash affiliated enumerating information (Alfiero, Cane,

Doronzo and Esposito, 2018). The rising abstract traits (for instance equality, get capacity,

common sense, and verifiable status) can improve decision esteem when the critical

emotional qualities are set up. In any case, they can't choose bookkeeping enumerating

quality isolated.

Importance: 'Centrality' highlight of the organization alludes to its ability to fathom different

distress raised by customers since they provide capital in the organization. Thinking about the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING 11

past writing, the importance of applying different bookkeeping components signifies

demonstrative and judicious structure. As examined before in this paper, bookkeepers will

fundamentally assess the nature of money related income as opposed to its quality and

bookkeeping announcing. This angle is limited because of the way that it overlooks non-

monetary data and future money related associated information that is accessible by investors

(Mostyn, 2012). So as to improve the quality, expands broad and perceptive examination of

A2M's; budget report is needed.

4. Part B

a) Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

Both international integrated and sustainability reportage systems are appropriate in

today's enterprise world(Pérez-López, Moreno-Romero, and Barkemeyer, 2013). Today, the

job of organizations in public arena is step by step expanding, as thought about its underlying

commitment for evaluating its gainfulness or encoding its funds. Sustainability Reporting

Guideline shows important principles pertinent to assistance organizations to upgrade upper

hand (Ceulemans, Lozano and Alonso-Almeida, 2015). Besides, part of ecological justifiable

in rule is basically prescribed for businesses to utilize present reality. Be that as it may, this

type of reporting focuses on a chosen portion of the element's status yet unfit to demonstrate

the particular and important climatic advances and natural variables (Crombie, 2012). Aside

from that, justifiable reports do not adequately show monetary data significant for assessing

the chances and dangers of a substance.

Then again, the International Integrated Reporting Framework improves the

partnership's notoriety; in this way, the gainfulness that the firm has can be determined

dependent on worldwide standards and rules (Messner, 2010). The coverage requires

past writing, the importance of applying different bookkeeping components signifies

demonstrative and judicious structure. As examined before in this paper, bookkeepers will

fundamentally assess the nature of money related income as opposed to its quality and

bookkeeping announcing. This angle is limited because of the way that it overlooks non-

monetary data and future money related associated information that is accessible by investors

(Mostyn, 2012). So as to improve the quality, expands broad and perceptive examination of

A2M's; budget report is needed.

4. Part B

a) Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

Both international integrated and sustainability reportage systems are appropriate in

today's enterprise world(Pérez-López, Moreno-Romero, and Barkemeyer, 2013). Today, the

job of organizations in public arena is step by step expanding, as thought about its underlying

commitment for evaluating its gainfulness or encoding its funds. Sustainability Reporting

Guideline shows important principles pertinent to assistance organizations to upgrade upper

hand (Ceulemans, Lozano and Alonso-Almeida, 2015). Besides, part of ecological justifiable

in rule is basically prescribed for businesses to utilize present reality. Be that as it may, this

type of reporting focuses on a chosen portion of the element's status yet unfit to demonstrate

the particular and important climatic advances and natural variables (Crombie, 2012). Aside

from that, justifiable reports do not adequately show monetary data significant for assessing

the chances and dangers of a substance.

Then again, the International Integrated Reporting Framework improves the

partnership's notoriety; in this way, the gainfulness that the firm has can be determined

dependent on worldwide standards and rules (Messner, 2010). The coverage requires

CONTEMPORARY ACCOUNTING 12

financial specialists to fabricate the association with bookkeeping and non-bookkeeping data

examiners to have the option to viably determine potential dangers. Most associations have

vivaciously are getting promptly integrated feed backs in various designs and each feedback

has been moulded according to the prerequisites of enterprise properties. Additionally,

incorporated declaring benchmarks and guidelines have been conveyed by Worldwide

Integrated Detailing Board, to provide guidance to study escalator (Soyka, 2013). With

extending hugeness and dispersed of integrated enumerating, chats about the favourable

circumstances and matters experienced in status extended. As per this examination, the

followings are explained: the price of financial declaring, dependency investigation, and

bookkeeping itemizing; the improvement of these conditions; favourable circumstances of

incorporated uncovering and issues that may be knowledgeable while status; and the

association between integrated specifying and budgetary reporting.

b) Rigour (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated

reports

Strengths

The accepted bookkeeping fixated on CF gives an organization establishment to defining

upcoming budget report benchmarks, that improve the dependency status of explicit

organizations. The quality obvious in this structure is to allow the presentation of

bookkeeping benchmarks and international incorporated reports that explain the main issues

in fiscal summaries. Accepted bookkeeping likewise assesses main components concerns, for

example, both affirmative and unsupportive, in budget reports.

Limitations

financial specialists to fabricate the association with bookkeeping and non-bookkeeping data

examiners to have the option to viably determine potential dangers. Most associations have

vivaciously are getting promptly integrated feed backs in various designs and each feedback

has been moulded according to the prerequisites of enterprise properties. Additionally,

incorporated declaring benchmarks and guidelines have been conveyed by Worldwide

Integrated Detailing Board, to provide guidance to study escalator (Soyka, 2013). With

extending hugeness and dispersed of integrated enumerating, chats about the favourable

circumstances and matters experienced in status extended. As per this examination, the

followings are explained: the price of financial declaring, dependency investigation, and

bookkeeping itemizing; the improvement of these conditions; favourable circumstances of

incorporated uncovering and issues that may be knowledgeable while status; and the

association between integrated specifying and budgetary reporting.

b) Rigour (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated

reports

Strengths

The accepted bookkeeping fixated on CF gives an organization establishment to defining

upcoming budget report benchmarks, that improve the dependency status of explicit

organizations. The quality obvious in this structure is to allow the presentation of

bookkeeping benchmarks and international incorporated reports that explain the main issues

in fiscal summaries. Accepted bookkeeping likewise assesses main components concerns, for

example, both affirmative and unsupportive, in budget reports.

Limitations

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.