Accounting Principles: Functions, Regulations & Cash Budgeting

VerifiedAdded on 2023/06/10

|10

|2631

|257

Report

AI Summary

This report delves into accounting principles, exploring the purpose and functions of accounting within an organization, considering regulatory and ethical constraints. It assesses accounting functions like payroll, legal compliance, accounts receivable & payable, budgeting, inventory management, record-keeping, and performance review. The report further discusses the benefits and limitations of budgeting and budgetary control, including the preparation of a cash budget for a business. It highlights how budgeting aids in financial management, objective setting, and ensuring future financial availability, while also acknowledging its limitations, such as reliance on past data and potential inflexibility. The concept of budgetary control as a continuous process of planning, coordination, and deviation rectification is also explained.

Accounting Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

Purpose of the Accounting Functions Within an Organisation :-...............................................4

Assessment of the Accounting Functions in Context of Regulatory and Ethical Constraints :-.4

Cash Budget................................................................................................................................6

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

Purpose of the Accounting Functions Within an Organisation :-...............................................4

Assessment of the Accounting Functions in Context of Regulatory and Ethical Constraints :-.4

Cash Budget................................................................................................................................6

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

This report is mainly discuss the concepts of accounting. Accounting is basically related

to activities like identifying the events or transactions which affect the business entity in any way

,sorting, storing, consolidating, reporting those to the owners of the business entity in such

manner that is understandable as well as assist them in qualitative decision making (Almagtome,

2021). Accounting principles are rules and principles which are followed by the organisations

while presenting financial data to stakeholders. This report contains two part. In first part of this

report, various purposes and functions of accounting are considered in details in the context of

the regulatory and ethical constraints. Further in this report, benefits and limitations of the budget

and budgetary planning, and control for an organisation are discussed along-with preparation of a

cash budget. In the second part of report, financial statements for a sole proprietary business, a

partnership and a non-for-profit organisation and interpret them as well. Afterwards, important

financial ratios are calculated and a comparison of the organisation's performance over the time

using financial ratios are done.

MAIN BODY

Accounting is a process of identifying, recording, analysing and reporting the financial

information to the owners and other users of it. It is a wider term. Accounting function plays a

vital role in an organisation. Accounting functions helps the organisation to track their financial

data which will help it in keeping financial records. Through which it will be easy for the

organisation to analyse their financial data in such manner that assist the management of the

organisation to decision-making (Dănescu and Prozan, 2018). There are several functions of the

accounting which are as follows:-

Payroll

Legal compliance

Account receivables & payables

Budgeting

Inventory management

Record-keeping

Performance review.

This report is mainly discuss the concepts of accounting. Accounting is basically related

to activities like identifying the events or transactions which affect the business entity in any way

,sorting, storing, consolidating, reporting those to the owners of the business entity in such

manner that is understandable as well as assist them in qualitative decision making (Almagtome,

2021). Accounting principles are rules and principles which are followed by the organisations

while presenting financial data to stakeholders. This report contains two part. In first part of this

report, various purposes and functions of accounting are considered in details in the context of

the regulatory and ethical constraints. Further in this report, benefits and limitations of the budget

and budgetary planning, and control for an organisation are discussed along-with preparation of a

cash budget. In the second part of report, financial statements for a sole proprietary business, a

partnership and a non-for-profit organisation and interpret them as well. Afterwards, important

financial ratios are calculated and a comparison of the organisation's performance over the time

using financial ratios are done.

MAIN BODY

Accounting is a process of identifying, recording, analysing and reporting the financial

information to the owners and other users of it. It is a wider term. Accounting function plays a

vital role in an organisation. Accounting functions helps the organisation to track their financial

data which will help it in keeping financial records. Through which it will be easy for the

organisation to analyse their financial data in such manner that assist the management of the

organisation to decision-making (Dănescu and Prozan, 2018). There are several functions of the

accounting which are as follows:-

Payroll

Legal compliance

Account receivables & payables

Budgeting

Inventory management

Record-keeping

Performance review.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Purpose of the Accounting Functions Within an Organisation :-

The main purpose of the accounting is to provide assistance to the owners and managers

so that they will be able to take decisions in the best interest of the business entity. The primary

purpose of the accounting is to provide aid to the governing body of the organisation in

identifying the areas which require special consideration and efforts so that it will be beneficial

for the organisation as a whole (Eebo, 2020). Similarly the main purpose of the accounting

functions is to provide feasibility to the business which will help it ultimately in preparing

necessary and useful qualitative reports to the governing body of the business. Reports are

generated in the form of financial statements of the organisation to the internal and external users

of the financial information.

Financial statements include Balance sheet, income statement, cash flow statement ,

statements of changes in equity and notes to accounts (Kovtun, Kopytina and Pavlyuchenko,

2018). By consider the above stated financial statements, internal and external users will able to

make decisions about what is the financial position of the business, whether the business is

profitable or not, whether the business is able to pay back its debts, what is the liquidity position

of the business, what are the financial needs of the business, whether the business is able to

generate returns to the stakeholders, where the business stands in comparison with its

competitors, the type of the industry in which it is operating, the risks and benefits associated

with that industry which are affecting the business, the other factors that influences the business

in its survival to the long run, whether it is beneficial for the investors to invest in the business

etc.

Assessment of the Accounting Functions in Context of Regulatory and Ethical Constraints :-

There are various accounting functions of an organisation which are required to make

accounting process more authentic and systematic with the supreme goal of an organisation.

Accounting functions are required to perform to accomplish the ultimate purposes of the

accounting process of the organisation. Various accounting functions are identified above let us

take a detailed analysis of each function, which are as follows :-

Payroll :- Payroll function assist managers to proper management of the human

resources of the organisation, to identify payroll related expenditure that are required to

done by the business entity. It is related to the activities like calculating wages and

salaries of the workers, to make payment of those. This function of the accounting helps

The main purpose of the accounting is to provide assistance to the owners and managers

so that they will be able to take decisions in the best interest of the business entity. The primary

purpose of the accounting is to provide aid to the governing body of the organisation in

identifying the areas which require special consideration and efforts so that it will be beneficial

for the organisation as a whole (Eebo, 2020). Similarly the main purpose of the accounting

functions is to provide feasibility to the business which will help it ultimately in preparing

necessary and useful qualitative reports to the governing body of the business. Reports are

generated in the form of financial statements of the organisation to the internal and external users

of the financial information.

Financial statements include Balance sheet, income statement, cash flow statement ,

statements of changes in equity and notes to accounts (Kovtun, Kopytina and Pavlyuchenko,

2018). By consider the above stated financial statements, internal and external users will able to

make decisions about what is the financial position of the business, whether the business is

profitable or not, whether the business is able to pay back its debts, what is the liquidity position

of the business, what are the financial needs of the business, whether the business is able to

generate returns to the stakeholders, where the business stands in comparison with its

competitors, the type of the industry in which it is operating, the risks and benefits associated

with that industry which are affecting the business, the other factors that influences the business

in its survival to the long run, whether it is beneficial for the investors to invest in the business

etc.

Assessment of the Accounting Functions in Context of Regulatory and Ethical Constraints :-

There are various accounting functions of an organisation which are required to make

accounting process more authentic and systematic with the supreme goal of an organisation.

Accounting functions are required to perform to accomplish the ultimate purposes of the

accounting process of the organisation. Various accounting functions are identified above let us

take a detailed analysis of each function, which are as follows :-

Payroll :- Payroll function assist managers to proper management of the human

resources of the organisation, to identify payroll related expenditure that are required to

done by the business entity. It is related to the activities like calculating wages and

salaries of the workers, to make payment of those. This function of the accounting helps

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to make decision making relating whether the business entity is making payment

regularly to its employees or workers, to identify and report to the senior governing body

about the expenditure of the business entity over a period of time (Mulawarman and

Kamayanti, 2018).

Legal compliance :- There are no. of rules and regulations which are required to comply

by a business organisation in order to prevent misleading reporting, tax evasion or fraud

instances. This function helps the organisation to identify what are the various rules and

regulations that required to be complied with in the industry specific, whether the

business entity is regular in compliance with the related legal requirements, what are the

effects of the non-compliance of such legal requirements.

Account receivables & payable :- This function of the accounting helps the governing

body to manage funds in the form of accounts receivables and payables. Whether the

organisation is able to receive funds from its debtors in a particular time period and make

payments to creditors of the business entity. Through the analysis of this, managers will

be able to determine how efficient is the business entity to make payments to its creditors

within a short span of time as well as how effective is the management's strategy in

obtaining the funds from the debtors.

Budgeting :- Budgeting helps the management to concentrate upon the financial goals of

the organisation. It helps in identifying what are the financial goals of the business entity

and how can a entity accomplish them within a specific time period. It provide assistance

to the management to control over the liquidity position for the entity, to identify and

save several costs incurred which are non-value added, to keep an eye over the net

spendings of the entity.

Inventory management :- This is an important accounting function which involves

descriptive analysis of the inventories of the business entity. It assists managers to make

qualitative decision making about the requirements of the working capital for the entity.

Record Keeping :- This functions involves maintaining records for every important

transaction and essential reports. It is mandatory requirement for the business

organisations to maintain proper, accurate and updating records from time to time of

business reports and statements of business entity but records should maintained

confidential (Srivastava and Shabi, 2019).

regularly to its employees or workers, to identify and report to the senior governing body

about the expenditure of the business entity over a period of time (Mulawarman and

Kamayanti, 2018).

Legal compliance :- There are no. of rules and regulations which are required to comply

by a business organisation in order to prevent misleading reporting, tax evasion or fraud

instances. This function helps the organisation to identify what are the various rules and

regulations that required to be complied with in the industry specific, whether the

business entity is regular in compliance with the related legal requirements, what are the

effects of the non-compliance of such legal requirements.

Account receivables & payable :- This function of the accounting helps the governing

body to manage funds in the form of accounts receivables and payables. Whether the

organisation is able to receive funds from its debtors in a particular time period and make

payments to creditors of the business entity. Through the analysis of this, managers will

be able to determine how efficient is the business entity to make payments to its creditors

within a short span of time as well as how effective is the management's strategy in

obtaining the funds from the debtors.

Budgeting :- Budgeting helps the management to concentrate upon the financial goals of

the organisation. It helps in identifying what are the financial goals of the business entity

and how can a entity accomplish them within a specific time period. It provide assistance

to the management to control over the liquidity position for the entity, to identify and

save several costs incurred which are non-value added, to keep an eye over the net

spendings of the entity.

Inventory management :- This is an important accounting function which involves

descriptive analysis of the inventories of the business entity. It assists managers to make

qualitative decision making about the requirements of the working capital for the entity.

Record Keeping :- This functions involves maintaining records for every important

transaction and essential reports. It is mandatory requirement for the business

organisations to maintain proper, accurate and updating records from time to time of

business reports and statements of business entity but records should maintained

confidential (Srivastava and Shabi, 2019).

Performance review :- The accounting reports prepared helps the business entity to keep

and check the performance of the business over a fixed time period and also assists

whether the business is able to achieve its goals.

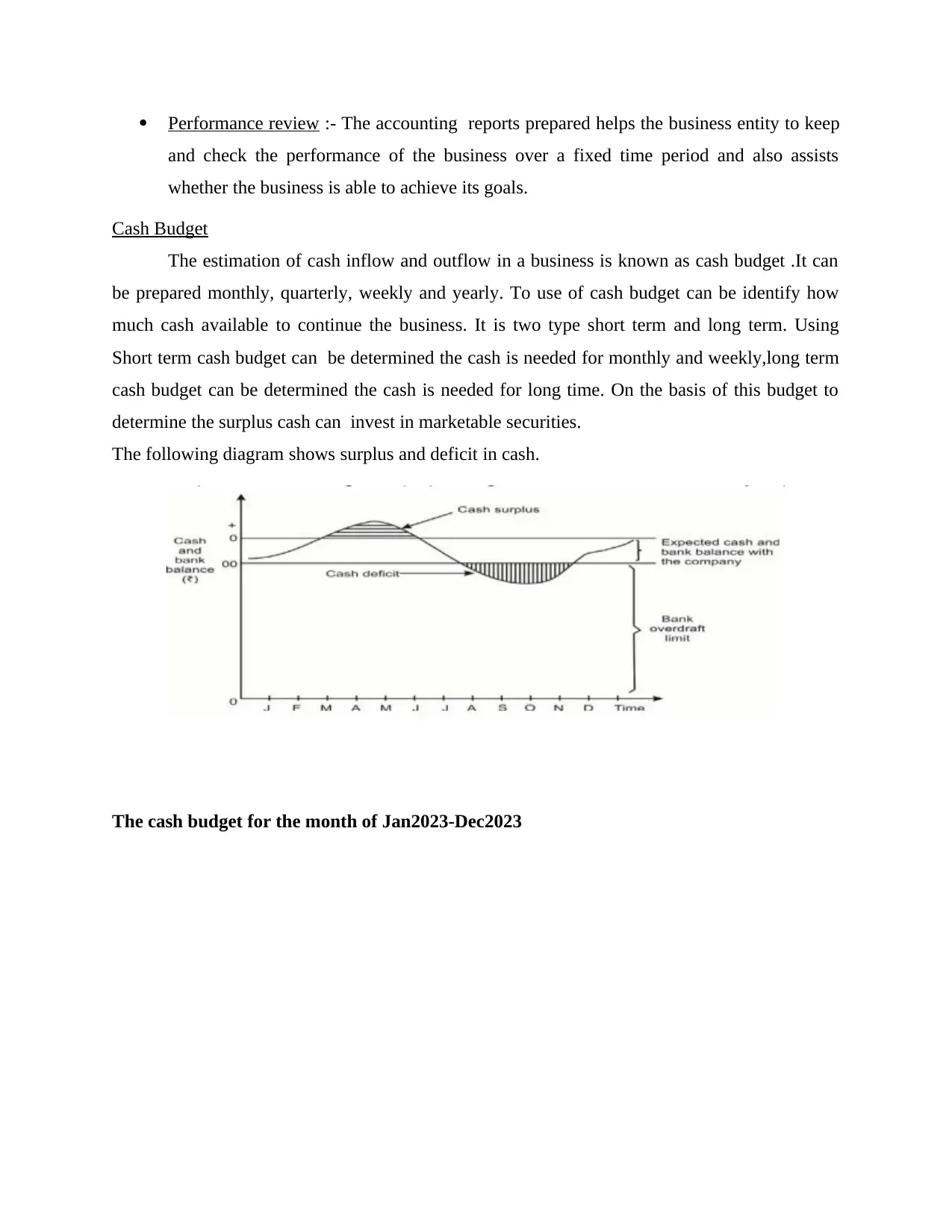

Cash Budget

The estimation of cash inflow and outflow in a business is known as cash budget .It can

be prepared monthly, quarterly, weekly and yearly. To use of cash budget can be identify how

much cash available to continue the business. It is two type short term and long term. Using

Short term cash budget can be determined the cash is needed for monthly and weekly,long term

cash budget can be determined the cash is needed for long time. On the basis of this budget to

determine the surplus cash can invest in marketable securities.

The following diagram shows surplus and deficit in cash.

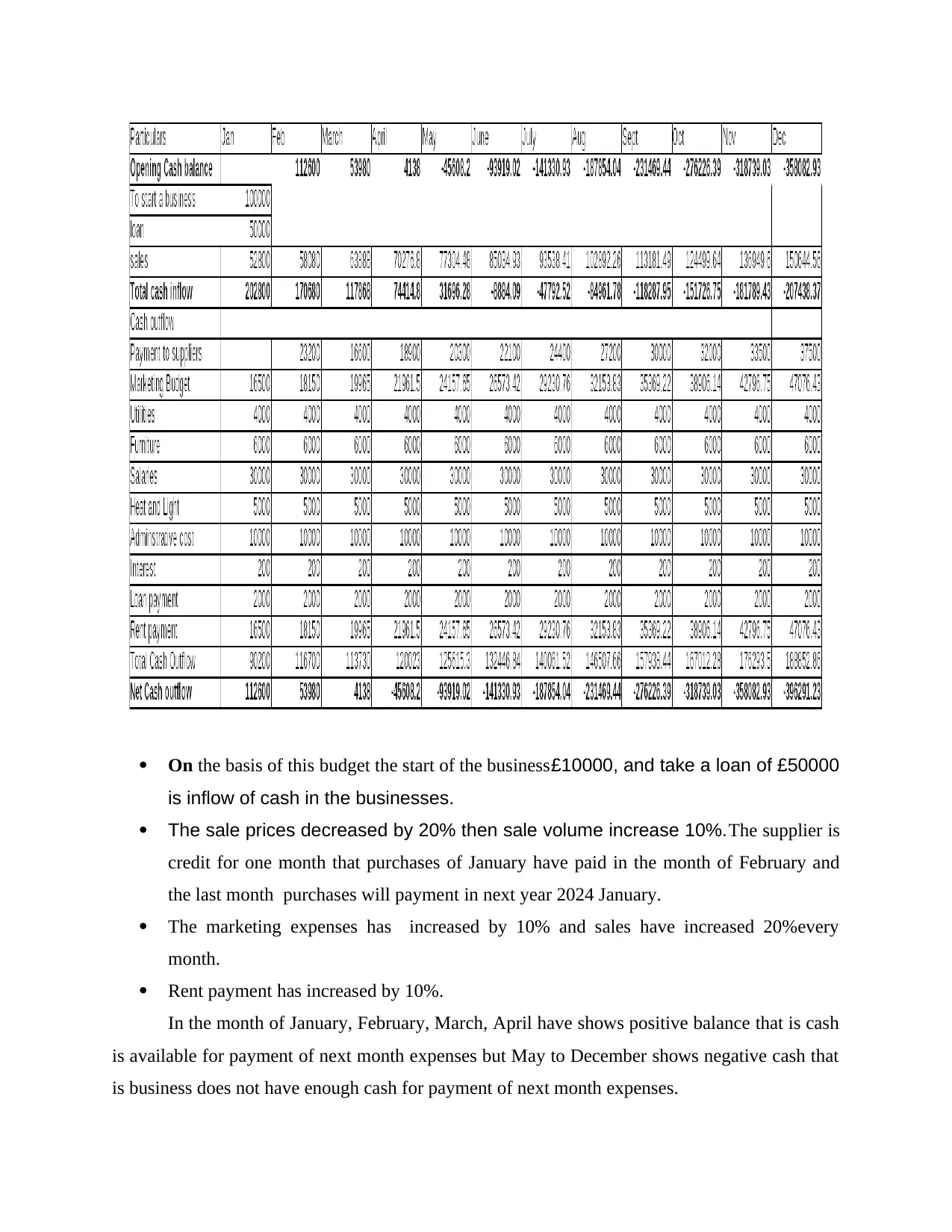

The cash budget for the month of Jan2023-Dec2023

and check the performance of the business over a fixed time period and also assists

whether the business is able to achieve its goals.

Cash Budget

The estimation of cash inflow and outflow in a business is known as cash budget .It can

be prepared monthly, quarterly, weekly and yearly. To use of cash budget can be identify how

much cash available to continue the business. It is two type short term and long term. Using

Short term cash budget can be determined the cash is needed for monthly and weekly,long term

cash budget can be determined the cash is needed for long time. On the basis of this budget to

determine the surplus cash can invest in marketable securities.

The following diagram shows surplus and deficit in cash.

The cash budget for the month of Jan2023-Dec2023

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On the basis of this budget the start of the business£10000, and take a loan of £50000

is inflow of cash in the businesses.

The sale prices decreased by 20% then sale volume increase 10%.The supplier is

credit for one month that purchases of January have paid in the month of February and

the last month purchases will payment in next year 2024 January.

The marketing expenses has increased by 10% and sales have increased 20%every

month.

Rent payment has increased by 10%.

In the month of January, February, March, April have shows positive balance that is cash

is available for payment of next month expenses but May to December shows negative cash that

is business does not have enough cash for payment of next month expenses.

is inflow of cash in the businesses.

The sale prices decreased by 20% then sale volume increase 10%.The supplier is

credit for one month that purchases of January have paid in the month of February and

the last month purchases will payment in next year 2024 January.

The marketing expenses has increased by 10% and sales have increased 20%every

month.

Rent payment has increased by 10%.

In the month of January, February, March, April have shows positive balance that is cash

is available for payment of next month expenses but May to December shows negative cash that

is business does not have enough cash for payment of next month expenses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget plays an effective role in an organization:

In a small business budget plays an important role. It shows the status of financial

position in a company at any point of time. Budget helps in controlling the money in future.

Budget can be prepare a group, individual and company to shows cash inflow and outflow in

future (Wong, George and Tanima, 2018). The surplus budget shows that expenses are less than

the incomes and deficit budgets shows the expenses are more than incomes. Budget can prepared

in different types like sales budget, cash budget,and purchase budget.

A budget plays a vital role

It manage all the finances in a business.

To meet objectives and taking financial decision.

To ensure the money is available for future projects.

To determine availability of current capital to meet an expenses.

Benefits of budget

Budget is help in controlling the income and expenditure in a business. It helps in identify

weakness,inefficiency in an organisation which can achieved goal .Using cash budget helps to

identify how much cash is needed to meet the expenses. To maintain adequate cash to determine

liquidity of the company,to determine the future cash needed in business. Budget is help in

controlling the capital expenditure. It helps in management to make proper planning. To use

budget identify the shortage of cash and abnormally cash requirement. It make arrangement to

deficit cash such as overdraft. The use of budgeting system helps in cost consciousness that is

optimise use of resources, and developing profit mindless environment. It provide systematic and

disciplined approach to the solution of problems in a organisation.

Limitation of budget:

Budget based on the future periods so the small organization cannot prepare it and it is

very time consuming ,data is to prepared on the analysis of past periods. The expenses which

will pay in future but not identify it i then the cash disbursement will occur. Cash budget focus

on financial needs ,non financial factors are not consider. The success of Budget is depends on

all the members of an organisation but the budget is to prepared an individual, many time budget

has failed. It has prepared in certain policies and principal so that it cannot change in according

to market policies. The failure of budget has arises many problems that get effective the running

of the business. It is prepared the principal of profit oriented which is more quantitative whether

In a small business budget plays an important role. It shows the status of financial

position in a company at any point of time. Budget helps in controlling the money in future.

Budget can be prepare a group, individual and company to shows cash inflow and outflow in

future (Wong, George and Tanima, 2018). The surplus budget shows that expenses are less than

the incomes and deficit budgets shows the expenses are more than incomes. Budget can prepared

in different types like sales budget, cash budget,and purchase budget.

A budget plays a vital role

It manage all the finances in a business.

To meet objectives and taking financial decision.

To ensure the money is available for future projects.

To determine availability of current capital to meet an expenses.

Benefits of budget

Budget is help in controlling the income and expenditure in a business. It helps in identify

weakness,inefficiency in an organisation which can achieved goal .Using cash budget helps to

identify how much cash is needed to meet the expenses. To maintain adequate cash to determine

liquidity of the company,to determine the future cash needed in business. Budget is help in

controlling the capital expenditure. It helps in management to make proper planning. To use

budget identify the shortage of cash and abnormally cash requirement. It make arrangement to

deficit cash such as overdraft. The use of budgeting system helps in cost consciousness that is

optimise use of resources, and developing profit mindless environment. It provide systematic and

disciplined approach to the solution of problems in a organisation.

Limitation of budget:

Budget based on the future periods so the small organization cannot prepare it and it is

very time consuming ,data is to prepared on the analysis of past periods. The expenses which

will pay in future but not identify it i then the cash disbursement will occur. Cash budget focus

on financial needs ,non financial factors are not consider. The success of Budget is depends on

all the members of an organisation but the budget is to prepared an individual, many time budget

has failed. It has prepared in certain policies and principal so that it cannot change in according

to market policies. The failure of budget has arises many problems that get effective the running

of the business. It is prepared the principal of profit oriented which is more quantitative whether

the people are needed more qualitative that cannot fullfill the people requirement. It is not

supported the unrealistic environment,it has prepared in past data if any change in business plan

the budget will get reflected.

Budgetary Control:

It is a method to prepare budget using various technique and activities and compare the

results with actual and if any deviation comes , rectify the budget this whole method is known as

Budgetary Control. It is a continuous process to planning and coordinating.

Budgetary control responsibility centre

Revenue Centre: The original units are compared in monetary terms not compared in

input cost

Expense Centre: Units are compared in previous budget not compare in actual output.

Profit Centres: The differences have found in revenue and expense then inter department

is using in transfer price that is cost plus profit price.

Investment Centres: producing rate of interest when output compared with assets.

Budgetary Controls helps in decision making:

Budget is to prepared by the organisation members,to participate of employees help in

taking decision of the market so budget can prepare in accordance to future requirement. To

make proper budget helps in finance department identify budgetary deviation and take corrective

action in strategic manner (Wochner And et.al., 2018). This budget helps cost management to

reduce cost using of budgetary control techniques. The company does not have knowledge new

technique and internal control, budget owner communicate to the finance department and taking

decision based on future events. It helps in coordinating all business activities then taking

decision of future according to new technology and method. Budget function are interlinked with

each other, effective implementation budget depends on all departments. To analyse of market,

gathered relevant information which helps in preparation of future budget and taking decision

based on future events.

CONCLUSION

supported the unrealistic environment,it has prepared in past data if any change in business plan

the budget will get reflected.

Budgetary Control:

It is a method to prepare budget using various technique and activities and compare the

results with actual and if any deviation comes , rectify the budget this whole method is known as

Budgetary Control. It is a continuous process to planning and coordinating.

Budgetary control responsibility centre

Revenue Centre: The original units are compared in monetary terms not compared in

input cost

Expense Centre: Units are compared in previous budget not compare in actual output.

Profit Centres: The differences have found in revenue and expense then inter department

is using in transfer price that is cost plus profit price.

Investment Centres: producing rate of interest when output compared with assets.

Budgetary Controls helps in decision making:

Budget is to prepared by the organisation members,to participate of employees help in

taking decision of the market so budget can prepare in accordance to future requirement. To

make proper budget helps in finance department identify budgetary deviation and take corrective

action in strategic manner (Wochner And et.al., 2018). This budget helps cost management to

reduce cost using of budgetary control techniques. The company does not have knowledge new

technique and internal control, budget owner communicate to the finance department and taking

decision based on future events. It helps in coordinating all business activities then taking

decision of future according to new technology and method. Budget function are interlinked with

each other, effective implementation budget depends on all departments. To analyse of market,

gathered relevant information which helps in preparation of future budget and taking decision

based on future events.

CONCLUSION

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Almagtome, A.H., 2021. Artificial Intelligence Applications in Accounting and Financial

Reporting Systems: An International Perspective. In Handbook of Research on Applied

AI for International Business and Marketing Applications (pp. 540-558). IGI Global.

Dănescu, T. and Prozan, M., 2018. Valences of the Corporate Governance in the Process of

Accounting Reporting. In Throughput Accounting in a Hyperconnected World (pp. 145-

166). IGI Global.

Eebo, T.O., 2020. Effects of Cooperative, Project-Based and Inquiry-Based Teaching Methods

on Business Education Students’ Academic Performance in Principles of

Accounting (Doctoral dissertation, Kwara State University (Nigeria)).

Kovtun, A.I., Kopytina, M.L. and Pavlyuchenko, T.N., 2018. ACCOUNTING OF

BIOLOGICAL ASSETS. I n Актуальные проблемы аграрной науки, производства

и образования (pp. 102-105).

Mulawarman, A.D. and Kamayanti, A., 2018. Towards Islamic Accounting Anthropology: how

secular anthropology reshaped accounting in Indonesia. Journal of Islamic

Accounting and Business Research.

Srivastava, R.M. and Shabi, V., 2019. The accounting system in India. In Indian Business:

Understanding a Rapidly Emerging Economy (pp. 153-165). Routledge.

Wochner, I. And et.al., 2018. upplementary Material: Optimality principles in human point-to-

manifold reaching accounting for muscle dynamics.

Wong, A., George, S. and Tanima, F.A., 2018. Operationalising dialogic accounting education

through praxis and social and environmental accounting: exploring student

perspectives. Accounting Education. 30(5). pp.525-550.

Books and Journals

Almagtome, A.H., 2021. Artificial Intelligence Applications in Accounting and Financial

Reporting Systems: An International Perspective. In Handbook of Research on Applied

AI for International Business and Marketing Applications (pp. 540-558). IGI Global.

Dănescu, T. and Prozan, M., 2018. Valences of the Corporate Governance in the Process of

Accounting Reporting. In Throughput Accounting in a Hyperconnected World (pp. 145-

166). IGI Global.

Eebo, T.O., 2020. Effects of Cooperative, Project-Based and Inquiry-Based Teaching Methods

on Business Education Students’ Academic Performance in Principles of

Accounting (Doctoral dissertation, Kwara State University (Nigeria)).

Kovtun, A.I., Kopytina, M.L. and Pavlyuchenko, T.N., 2018. ACCOUNTING OF

BIOLOGICAL ASSETS. I n Актуальные проблемы аграрной науки, производства

и образования (pp. 102-105).

Mulawarman, A.D. and Kamayanti, A., 2018. Towards Islamic Accounting Anthropology: how

secular anthropology reshaped accounting in Indonesia. Journal of Islamic

Accounting and Business Research.

Srivastava, R.M. and Shabi, V., 2019. The accounting system in India. In Indian Business:

Understanding a Rapidly Emerging Economy (pp. 153-165). Routledge.

Wochner, I. And et.al., 2018. upplementary Material: Optimality principles in human point-to-

manifold reaching accounting for muscle dynamics.

Wong, A., George, S. and Tanima, F.A., 2018. Operationalising dialogic accounting education

through praxis and social and environmental accounting: exploring student

perspectives. Accounting Education. 30(5). pp.525-550.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.