LCBB4001 Accounting Fundamentals: Kedison & Chocco Plc Report

VerifiedAdded on 2023/06/18

|8

|1384

|410

Homework Assignment

AI Summary

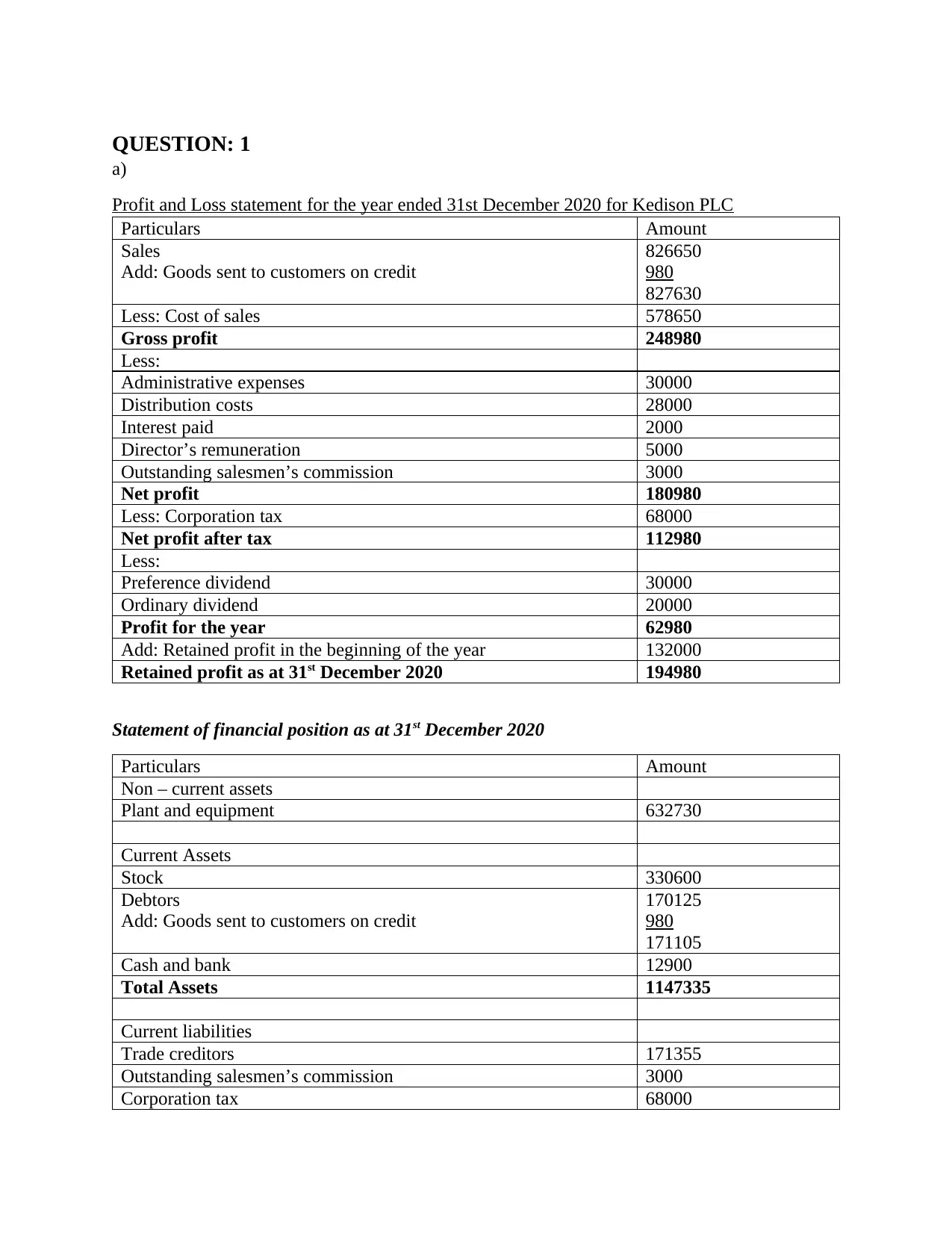

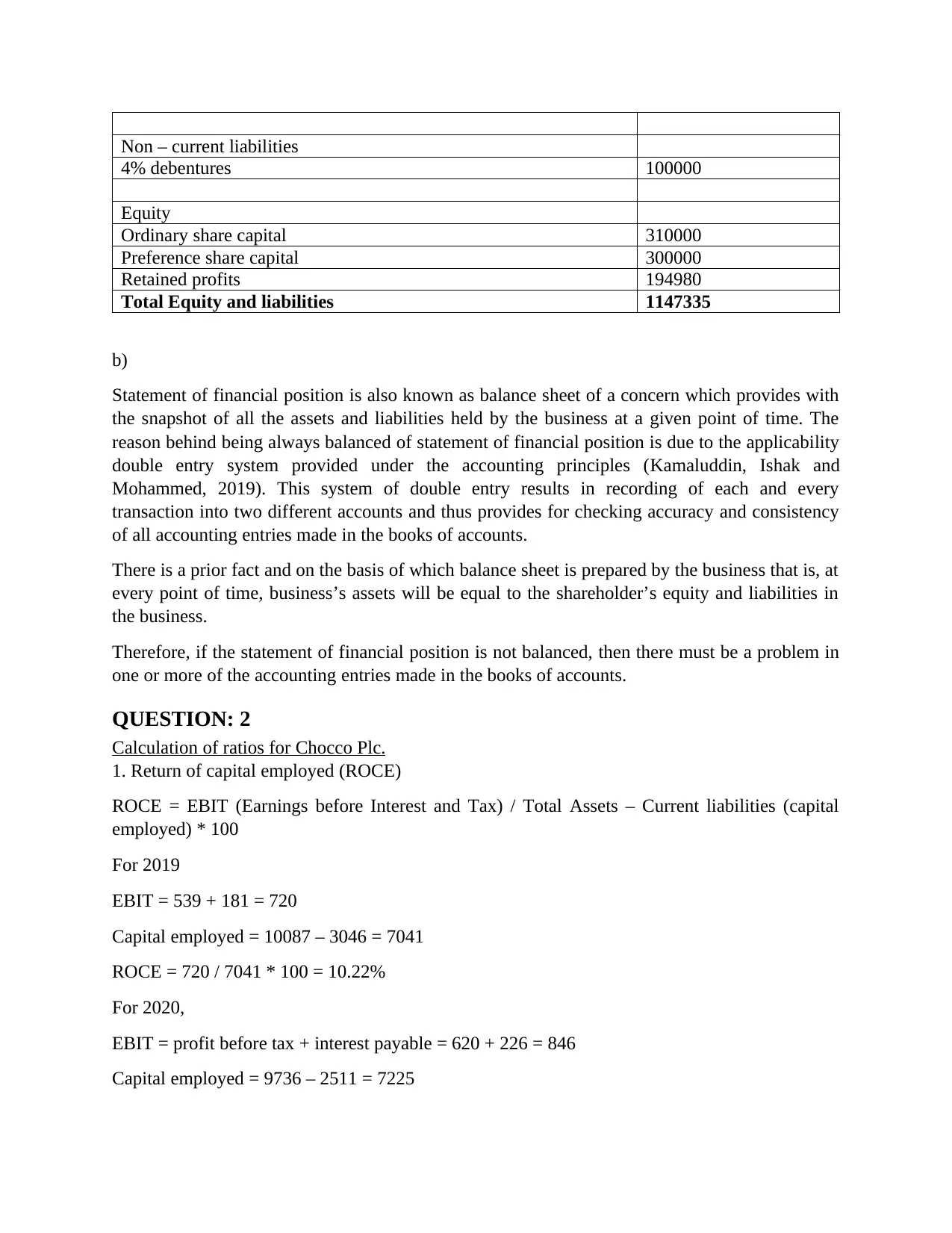

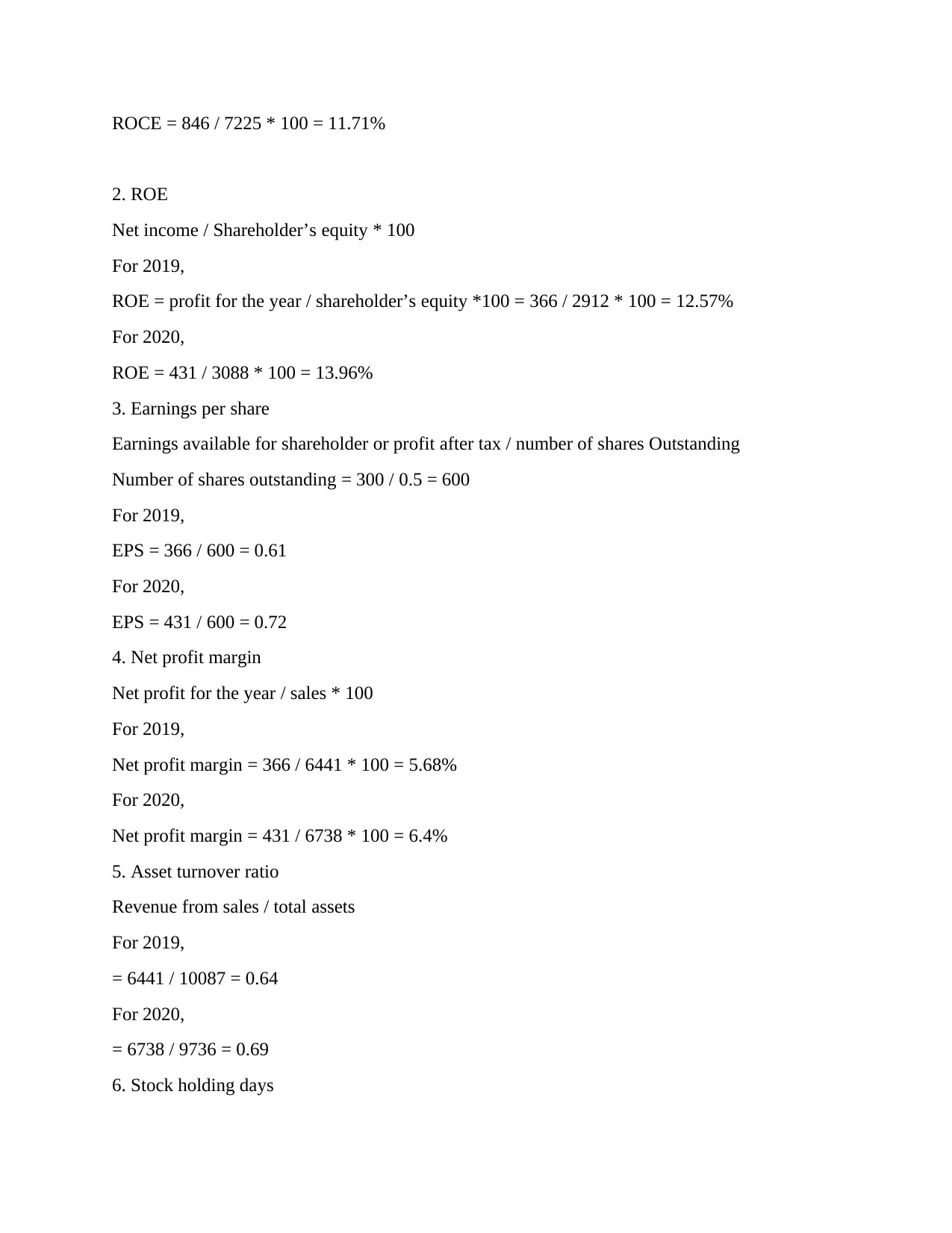

This assignment focuses on the financial analysis of two companies, Kedison PLC and Chocco Plc, using accounting fundamentals. For Kedison PLC, a profit and loss statement for the year ended December 31, 2020, is prepared, along with a statement of financial position. The assignment explains the importance of a balanced statement of financial position due to the double-entry system. For Chocco Plc, various financial ratios are calculated for 2019 and 2020, including Return on Capital Employed (ROCE), Return on Equity (ROE), Earnings Per Share (EPS), Net Profit Margin, Asset Turnover Ratio, Stock Holding Days, Debtor's Collection Period, Current Ratio, Gearing Ratio, and Inventory Turnover Ratio. The analysis interprets these ratios to assess Chocco Plc's profitability, efficiency, liquidity, and solvency, highlighting changes and trends between the two years. The document emphasizes the importance of these ratios in understanding a company's financial health and performance. Desklib provides access to similar solved assignments and past papers for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.