Accounting Fundamentals Assignment: Income Statement and Ratios

VerifiedAdded on 2023/01/09

|11

|3192

|58

Homework Assignment

AI Summary

This assignment analyzes accounting fundamentals through the lens of Wales Plc's financial data. It begins with the formulation of an income statement and statement of financial position, including necessary adjustments to the trial balance. The assignment then delves into ratio calculations, comparing 2018 and 2019 data to assess the company's performance, including return on capital employed, return on equity, and other key metrics. Further, the assignment explores the different user groups of company accounts, detailing their interests in financial information, and discusses the advantages and disadvantages of a highly regulated financial reporting regime. Finally, it addresses the limitations of financial statements, providing a comprehensive overview of accounting principles and their practical application.

Accounting

fundamentals

fundamentals

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

Formulation of income statement and statement of financial position for the Wales Plc by

making all the adjustments..........................................................................................................1

QUESTION 2..................................................................................................................................4

a. Calculation of various ratios....................................................................................................4

b. Analysis of the position of company on the basis of ratio’s calculation.................................4

QUESTION 3..................................................................................................................................5

a. Various user groups of company accounts and why they are interested in the information

which is provided by the financial statements.............................................................................5

b. All the advantages and disadvantages of a financial reporting regime which is highly

regulated......................................................................................................................................6

c. Different limitations for financial statements..........................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

Formulation of income statement and statement of financial position for the Wales Plc by

making all the adjustments..........................................................................................................1

QUESTION 2..................................................................................................................................4

a. Calculation of various ratios....................................................................................................4

b. Analysis of the position of company on the basis of ratio’s calculation.................................4

QUESTION 3..................................................................................................................................5

a. Various user groups of company accounts and why they are interested in the information

which is provided by the financial statements.............................................................................5

b. All the advantages and disadvantages of a financial reporting regime which is highly

regulated......................................................................................................................................6

c. Different limitations for financial statements..........................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION

Accounting fundamentals are the basic terms of accounting that are used for the purpose

of generating all the final accounts. With the help of them, all the accounting professionals can

get aware of the key aspects that should be focused by them while generating the financial

statements. If they get failed in creation of final accounts properly then it will leave negative

impact upon functionality of business (Aldeia, 2019). Some of the key accounting fundamentals

are revenues, expenses, liabilities, incomes, assets and all the financial statements like profit and

loss account, balance sheet and cash flow statement. This assignment is focused with various

aspects of finance. It covers various topics such as formulating of income statements with

adjustments, calculation of ratios and assessment of the actual situation of the entity on the basis

of calculations. Apart from this, different user groups of company accounts, their interest in the

information, advantage and disadvantage of highly regulated financial reporting regime and

limitations of financial statements are also covered in present report.

QUESTION 1

Formulation of income statement and statement of financial position for the Wales Plc by

making all the adjustments

Income statement: It is also known as profit and loss account of the company in which

information of all the incomes an expense is recorded. With the help of it, the management teams

could determine that the organisation is able to generate profits or not. While planning to reach

the long-term business goals it is very important for all the entities to make sure that they are

higher profits are generated in the accounting year. Apart from this, if the company is not able to

generate good profits then it may leave negative impact upon mind set of investors to make

investment within the business. If they will not be able to analyse that the company will provide

them higher returns or not then they will ignore to make investment in the entity (An, Chiu and

Zhang, 2020).

Balance sheet: It is also known as statement of financial position of the company. By

using it, all the internal as well as external stakeholders will be aware of actual performance and

position of business which can help them to formulate decision for future. Detailed information

of assets, labilities and equities is recorded in this statement so that financial performance of the

1

Accounting fundamentals are the basic terms of accounting that are used for the purpose

of generating all the final accounts. With the help of them, all the accounting professionals can

get aware of the key aspects that should be focused by them while generating the financial

statements. If they get failed in creation of final accounts properly then it will leave negative

impact upon functionality of business (Aldeia, 2019). Some of the key accounting fundamentals

are revenues, expenses, liabilities, incomes, assets and all the financial statements like profit and

loss account, balance sheet and cash flow statement. This assignment is focused with various

aspects of finance. It covers various topics such as formulating of income statements with

adjustments, calculation of ratios and assessment of the actual situation of the entity on the basis

of calculations. Apart from this, different user groups of company accounts, their interest in the

information, advantage and disadvantage of highly regulated financial reporting regime and

limitations of financial statements are also covered in present report.

QUESTION 1

Formulation of income statement and statement of financial position for the Wales Plc by

making all the adjustments

Income statement: It is also known as profit and loss account of the company in which

information of all the incomes an expense is recorded. With the help of it, the management teams

could determine that the organisation is able to generate profits or not. While planning to reach

the long-term business goals it is very important for all the entities to make sure that they are

higher profits are generated in the accounting year. Apart from this, if the company is not able to

generate good profits then it may leave negative impact upon mind set of investors to make

investment within the business. If they will not be able to analyse that the company will provide

them higher returns or not then they will ignore to make investment in the entity (An, Chiu and

Zhang, 2020).

Balance sheet: It is also known as statement of financial position of the company. By

using it, all the internal as well as external stakeholders will be aware of actual performance and

position of business which can help them to formulate decision for future. Detailed information

of assets, labilities and equities is recorded in this statement so that financial performance of the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business could be determined. It helps to analyse that the company will be able to meet all its

obligations with the help of the assets that are available for business.

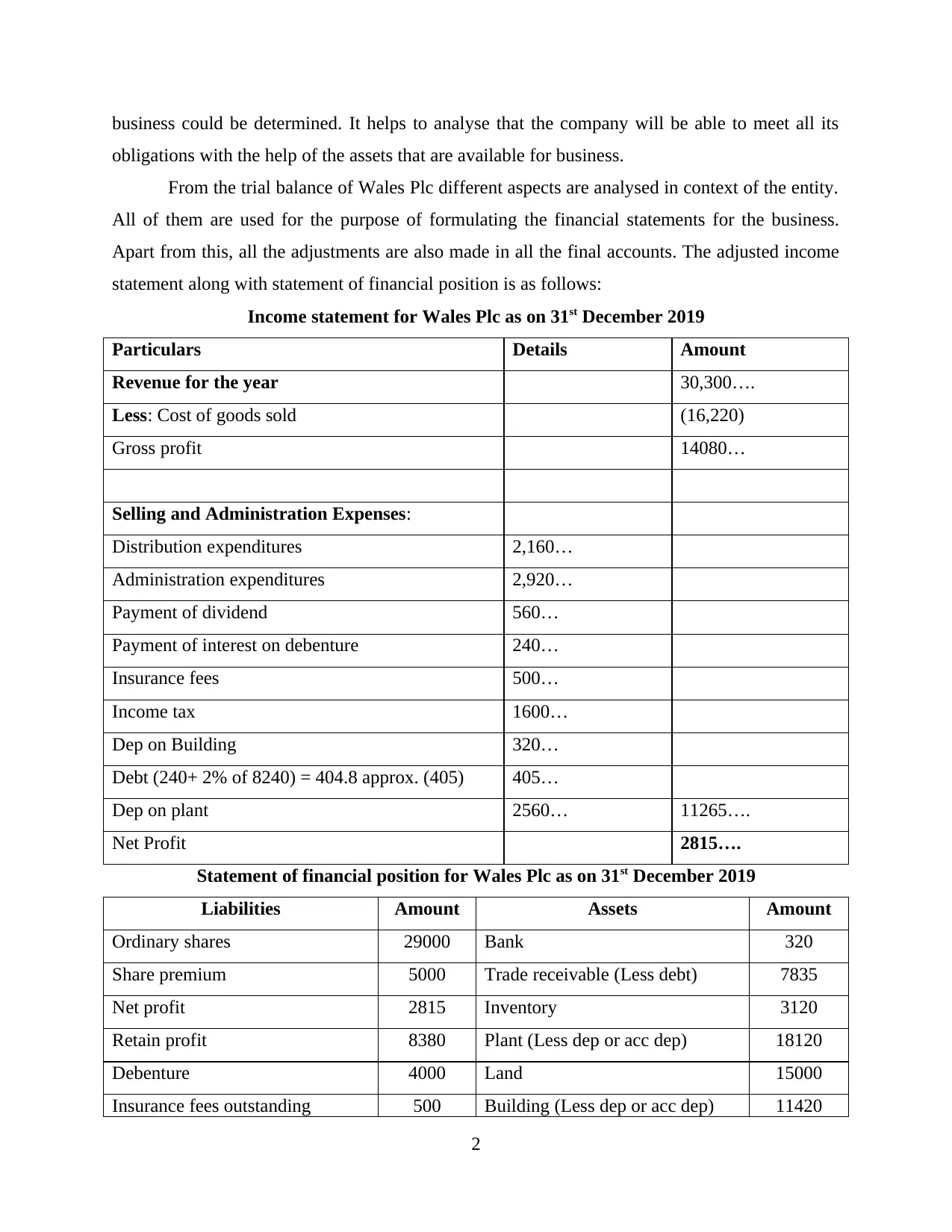

From the trial balance of Wales Plc different aspects are analysed in context of the entity.

All of them are used for the purpose of formulating the financial statements for the business.

Apart from this, all the adjustments are also made in all the final accounts. The adjusted income

statement along with statement of financial position is as follows:

Income statement for Wales Plc as on 31st December 2019

Particulars Details Amount

Revenue for the year 30,300….

Less: Cost of goods sold (16,220)

Gross profit 14080…

Selling and Administration Expenses:

Distribution expenditures 2,160…

Administration expenditures 2,920…

Payment of dividend 560…

Payment of interest on debenture 240…

Insurance fees 500…

Income tax 1600…

Dep on Building 320…

Debt (240+ 2% of 8240) = 404.8 approx. (405) 405…

Dep on plant 2560… 11265….

Net Profit 2815….

Statement of financial position for Wales Plc as on 31st December 2019

Liabilities Amount Assets Amount

Ordinary shares 29000 Bank 320

Share premium 5000 Trade receivable (Less debt) 7835

Net profit 2815 Inventory 3120

Retain profit 8380 Plant (Less dep or acc dep) 18120

Debenture 4000 Land 15000

Insurance fees outstanding 500 Building (Less dep or acc dep) 11420

2

obligations with the help of the assets that are available for business.

From the trial balance of Wales Plc different aspects are analysed in context of the entity.

All of them are used for the purpose of formulating the financial statements for the business.

Apart from this, all the adjustments are also made in all the final accounts. The adjusted income

statement along with statement of financial position is as follows:

Income statement for Wales Plc as on 31st December 2019

Particulars Details Amount

Revenue for the year 30,300….

Less: Cost of goods sold (16,220)

Gross profit 14080…

Selling and Administration Expenses:

Distribution expenditures 2,160…

Administration expenditures 2,920…

Payment of dividend 560…

Payment of interest on debenture 240…

Insurance fees 500…

Income tax 1600…

Dep on Building 320…

Debt (240+ 2% of 8240) = 404.8 approx. (405) 405…

Dep on plant 2560… 11265….

Net Profit 2815….

Statement of financial position for Wales Plc as on 31st December 2019

Liabilities Amount Assets Amount

Ordinary shares 29000 Bank 320

Share premium 5000 Trade receivable (Less debt) 7835

Net profit 2815 Inventory 3120

Retain profit 8380 Plant (Less dep or acc dep) 18120

Debenture 4000 Land 15000

Insurance fees outstanding 500 Building (Less dep or acc dep) 11420

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trade payable 4480

55815 55815

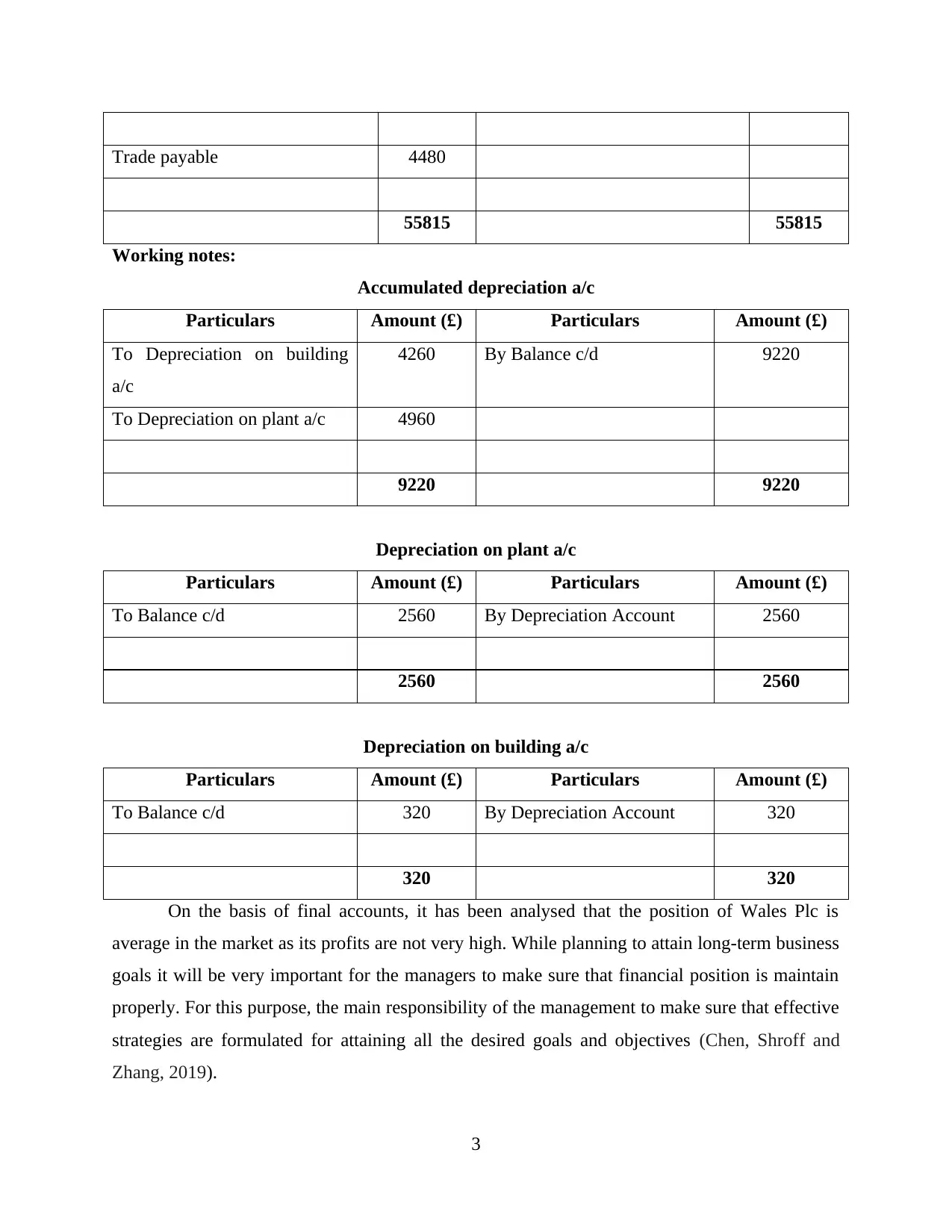

Working notes:

Accumulated depreciation a/c

Particulars Amount (£) Particulars Amount (£)

To Depreciation on building

a/c

4260 By Balance c/d 9220

To Depreciation on plant a/c 4960

9220 9220

Depreciation on plant a/c

Particulars Amount (£) Particulars Amount (£)

To Balance c/d 2560 By Depreciation Account 2560

2560 2560

Depreciation on building a/c

Particulars Amount (£) Particulars Amount (£)

To Balance c/d 320 By Depreciation Account 320

320 320

On the basis of final accounts, it has been analysed that the position of Wales Plc is

average in the market as its profits are not very high. While planning to attain long-term business

goals it will be very important for the managers to make sure that financial position is maintain

properly. For this purpose, the main responsibility of the management to make sure that effective

strategies are formulated for attaining all the desired goals and objectives (Chen, Shroff and

Zhang, 2019).

3

55815 55815

Working notes:

Accumulated depreciation a/c

Particulars Amount (£) Particulars Amount (£)

To Depreciation on building

a/c

4260 By Balance c/d 9220

To Depreciation on plant a/c 4960

9220 9220

Depreciation on plant a/c

Particulars Amount (£) Particulars Amount (£)

To Balance c/d 2560 By Depreciation Account 2560

2560 2560

Depreciation on building a/c

Particulars Amount (£) Particulars Amount (£)

To Balance c/d 320 By Depreciation Account 320

320 320

On the basis of final accounts, it has been analysed that the position of Wales Plc is

average in the market as its profits are not very high. While planning to attain long-term business

goals it will be very important for the managers to make sure that financial position is maintain

properly. For this purpose, the main responsibility of the management to make sure that effective

strategies are formulated for attaining all the desired goals and objectives (Chen, Shroff and

Zhang, 2019).

3

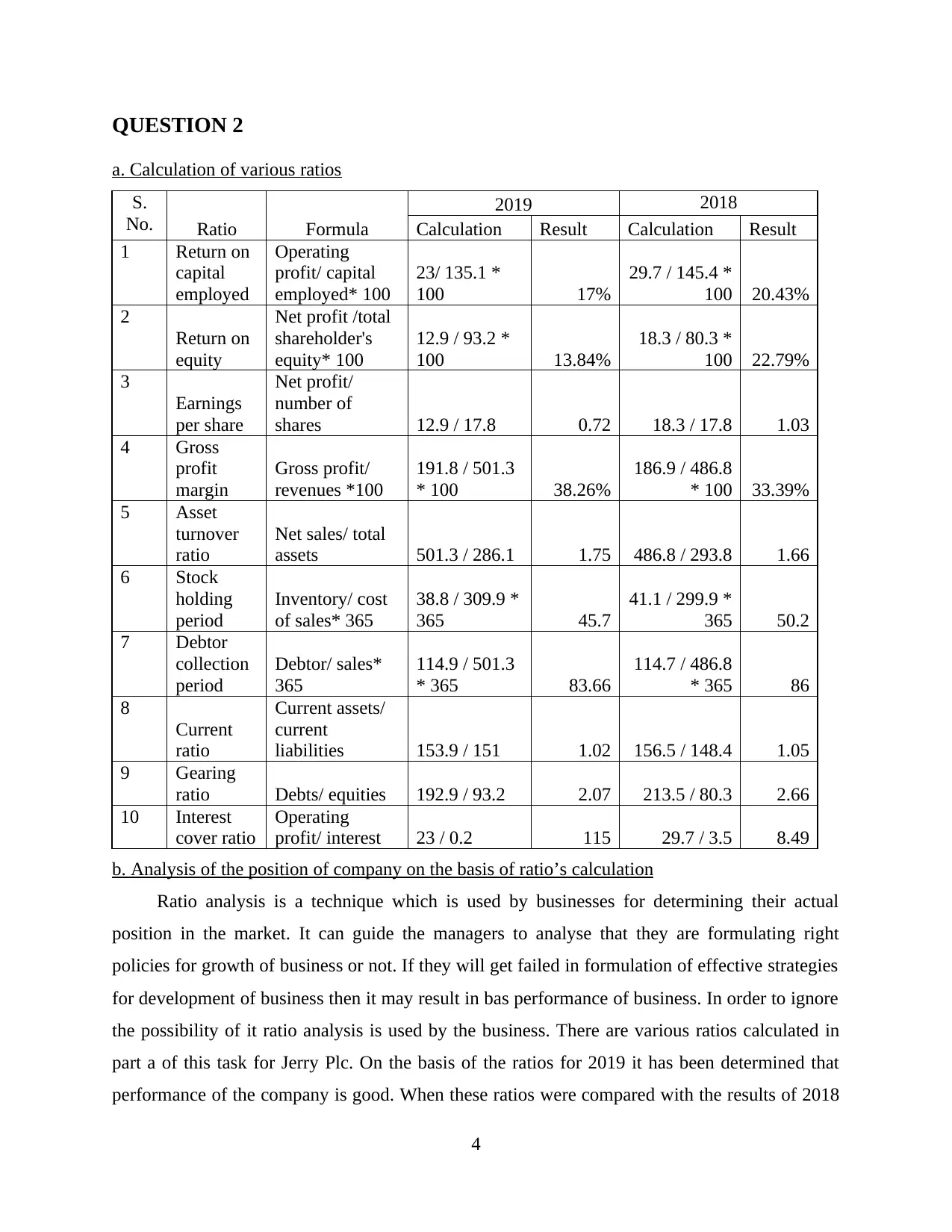

QUESTION 2

a. Calculation of various ratios

S.

No. Ratio Formula

2019 2018

Calculation Result Calculation Result

1 Return on

capital

employed

Operating

profit/ capital

employed* 100

23/ 135.1 *

100 17%

29.7 / 145.4 *

100 20.43%

2

Return on

equity

Net profit /total

shareholder's

equity* 100

12.9 / 93.2 *

100 13.84%

18.3 / 80.3 *

100 22.79%

3

Earnings

per share

Net profit/

number of

shares 12.9 / 17.8 0.72 18.3 / 17.8 1.03

4 Gross

profit

margin

Gross profit/

revenues *100

191.8 / 501.3

* 100 38.26%

186.9 / 486.8

* 100 33.39%

5 Asset

turnover

ratio

Net sales/ total

assets 501.3 / 286.1 1.75 486.8 / 293.8 1.66

6 Stock

holding

period

Inventory/ cost

of sales* 365

38.8 / 309.9 *

365 45.7

41.1 / 299.9 *

365 50.2

7 Debtor

collection

period

Debtor/ sales*

365

114.9 / 501.3

* 365 83.66

114.7 / 486.8

* 365 86

8

Current

ratio

Current assets/

current

liabilities 153.9 / 151 1.02 156.5 / 148.4 1.05

9 Gearing

ratio Debts/ equities 192.9 / 93.2 2.07 213.5 / 80.3 2.66

10 Interest

cover ratio

Operating

profit/ interest 23 / 0.2 115 29.7 / 3.5 8.49

b. Analysis of the position of company on the basis of ratio’s calculation

Ratio analysis is a technique which is used by businesses for determining their actual

position in the market. It can guide the managers to analyse that they are formulating right

policies for growth of business or not. If they will get failed in formulation of effective strategies

for development of business then it may result in bas performance of business. In order to ignore

the possibility of it ratio analysis is used by the business. There are various ratios calculated in

part a of this task for Jerry Plc. On the basis of the ratios for 2019 it has been determined that

performance of the company is good. When these ratios were compared with the results of 2018

4

a. Calculation of various ratios

S.

No. Ratio Formula

2019 2018

Calculation Result Calculation Result

1 Return on

capital

employed

Operating

profit/ capital

employed* 100

23/ 135.1 *

100 17%

29.7 / 145.4 *

100 20.43%

2

Return on

equity

Net profit /total

shareholder's

equity* 100

12.9 / 93.2 *

100 13.84%

18.3 / 80.3 *

100 22.79%

3

Earnings

per share

Net profit/

number of

shares 12.9 / 17.8 0.72 18.3 / 17.8 1.03

4 Gross

profit

margin

Gross profit/

revenues *100

191.8 / 501.3

* 100 38.26%

186.9 / 486.8

* 100 33.39%

5 Asset

turnover

ratio

Net sales/ total

assets 501.3 / 286.1 1.75 486.8 / 293.8 1.66

6 Stock

holding

period

Inventory/ cost

of sales* 365

38.8 / 309.9 *

365 45.7

41.1 / 299.9 *

365 50.2

7 Debtor

collection

period

Debtor/ sales*

365

114.9 / 501.3

* 365 83.66

114.7 / 486.8

* 365 86

8

Current

ratio

Current assets/

current

liabilities 153.9 / 151 1.02 156.5 / 148.4 1.05

9 Gearing

ratio Debts/ equities 192.9 / 93.2 2.07 213.5 / 80.3 2.66

10 Interest

cover ratio

Operating

profit/ interest 23 / 0.2 115 29.7 / 3.5 8.49

b. Analysis of the position of company on the basis of ratio’s calculation

Ratio analysis is a technique which is used by businesses for determining their actual

position in the market. It can guide the managers to analyse that they are formulating right

policies for growth of business or not. If they will get failed in formulation of effective strategies

for development of business then it may result in bas performance of business. In order to ignore

the possibility of it ratio analysis is used by the business. There are various ratios calculated in

part a of this task for Jerry Plc. On the basis of the ratios for 2019 it has been determined that

performance of the company is good. When these ratios were compared with the results of 2018

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

then it was assessed that the company’s position is not good in comparison of previous year

(Christodoulou, Clubb and Mcleay, 2016).

Return on capital employed and equity were high in last year that shows that company’s

position in 2019 is little bit bad when it will be compared with last year’s results. Current and

gearing ratios of previous year were also very good and for 2019 these were decreased. Apart

from all these aspects. The interest cover and debtor collection period ratios are showing results

in favour of 2019 because the period of collecting payments from debtor is decreased and

interest cover for 2019 is increased. By determining all the key aspects of business, it has been

evaluated that position of Jerry Plc is good in the market as the ratios are showing position

condition of company.

QUESTION 3

a. Various user groups of company accounts and why they are interested in the information

which is provided by the financial statements

Financial statements are the reports that are used by organisations to analyse that they are

able to meet the financial goals or not. Apart from this, while planning to formulate effective

strategies for future it will be very important for businesses to analyse that the final accounts are

formed properly or not. If the information recorded in the financial statements is not accurate and

transparent then it may bias the decisions of management teams. There are various stakeholders

of the entities who use the information of the final accounts in order to analyse the actual

position of business (Chu, Mathieu and Mbagwu, 2018). All of them could be segregated in three

different groups which are discussed below along with the interest of each one of them in the

information shared by the final accounts:

Board members: All the senior authorities or the main members of the company are

considered as the part of board members. Shareholders, CEO etc. are some of the board members

who use financial statements for analysing actual position of business. With the help of final

accounts, they assess that the plans that were formed by the in past have resulted positively for

business or not. They are interested in the information of financial statement because they are

focused with development of business and with the help of the final accounts, they can analyse

the position of business form new strategies for betterment of it.

5

(Christodoulou, Clubb and Mcleay, 2016).

Return on capital employed and equity were high in last year that shows that company’s

position in 2019 is little bit bad when it will be compared with last year’s results. Current and

gearing ratios of previous year were also very good and for 2019 these were decreased. Apart

from all these aspects. The interest cover and debtor collection period ratios are showing results

in favour of 2019 because the period of collecting payments from debtor is decreased and

interest cover for 2019 is increased. By determining all the key aspects of business, it has been

evaluated that position of Jerry Plc is good in the market as the ratios are showing position

condition of company.

QUESTION 3

a. Various user groups of company accounts and why they are interested in the information

which is provided by the financial statements

Financial statements are the reports that are used by organisations to analyse that they are

able to meet the financial goals or not. Apart from this, while planning to formulate effective

strategies for future it will be very important for businesses to analyse that the final accounts are

formed properly or not. If the information recorded in the financial statements is not accurate and

transparent then it may bias the decisions of management teams. There are various stakeholders

of the entities who use the information of the final accounts in order to analyse the actual

position of business (Chu, Mathieu and Mbagwu, 2018). All of them could be segregated in three

different groups which are discussed below along with the interest of each one of them in the

information shared by the final accounts:

Board members: All the senior authorities or the main members of the company are

considered as the part of board members. Shareholders, CEO etc. are some of the board members

who use financial statements for analysing actual position of business. With the help of final

accounts, they assess that the plans that were formed by the in past have resulted positively for

business or not. They are interested in the information of financial statement because they are

focused with development of business and with the help of the final accounts, they can analyse

the position of business form new strategies for betterment of it.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Internal users: All the parties that are internally connected with the organisation are the

internal stakeholders who use the financial statements for determining the position of business.

Main aim of them is to be a part of such company which financially strong and having good

competitive advantage in the industry. Some of the internal users of financial statements are staff

members, management teams etc. Employees analyse the final accounts for the purpose of

making sure that the entity will be able to provide them appropriate compensate for their work or

not. Managers use the financial statement’s information as they are interested in the analysis of

that the policies which were formed by them in previous year are able to meet their expectations

or not (Goldschmidt, 2020).

External users: The individuals which are not internally connected with the entity but

having interest in the position of business are the external users of business. Some of the external

users of financial statements of companies are investors, creditors, government, customers etc.

All of them have different interests in the information which is shared through final accounts.

Investors are interested in the details of financial statement for determining the rate of return

which could be offered by the company if they make investment within the business. Creditors

are the external parties who allow credit to the entity and they use information of final accounts

to analyse that the entity will be able to repay the owed amount on time or not. Customers use

the information of financial statements to analyse that they are buying products from a company

which is strong in financial terms or not. Government uses the financial statements for the

purpose of analysing that the company is able to perform all the operations under legal terms and

conditions or not. If any type of error is determined by the legal authorities in final accounts then

strict action against the company could be taken (Hesarzadeh, Bazrafshan and Rajabalizadeh,

2019).

b. All the advantages and disadvantages of a financial reporting regime which is highly regulated

Financial reporting could be defined as the process of recording finance related

information in the appropriate accounts and books. With the help of all the final accounts the

business entities will be able to determine that they are able to sustain in the market or not. If the

businesses will not be able to analyse that they are progressing or not then it will leave negative

impacts upon functionality of business. For this purpose, it is very important for all the entities to

make sure that they are focused with highly regulated financial reporting regime. With the help

of it, possibility of making mistakes in the books of accounting will be reduced and the accounts

6

internal stakeholders who use the financial statements for determining the position of business.

Main aim of them is to be a part of such company which financially strong and having good

competitive advantage in the industry. Some of the internal users of financial statements are staff

members, management teams etc. Employees analyse the final accounts for the purpose of

making sure that the entity will be able to provide them appropriate compensate for their work or

not. Managers use the financial statement’s information as they are interested in the analysis of

that the policies which were formed by them in previous year are able to meet their expectations

or not (Goldschmidt, 2020).

External users: The individuals which are not internally connected with the entity but

having interest in the position of business are the external users of business. Some of the external

users of financial statements of companies are investors, creditors, government, customers etc.

All of them have different interests in the information which is shared through final accounts.

Investors are interested in the details of financial statement for determining the rate of return

which could be offered by the company if they make investment within the business. Creditors

are the external parties who allow credit to the entity and they use information of final accounts

to analyse that the entity will be able to repay the owed amount on time or not. Customers use

the information of financial statements to analyse that they are buying products from a company

which is strong in financial terms or not. Government uses the financial statements for the

purpose of analysing that the company is able to perform all the operations under legal terms and

conditions or not. If any type of error is determined by the legal authorities in final accounts then

strict action against the company could be taken (Hesarzadeh, Bazrafshan and Rajabalizadeh,

2019).

b. All the advantages and disadvantages of a financial reporting regime which is highly regulated

Financial reporting could be defined as the process of recording finance related

information in the appropriate accounts and books. With the help of all the final accounts the

business entities will be able to determine that they are able to sustain in the market or not. If the

businesses will not be able to analyse that they are progressing or not then it will leave negative

impacts upon functionality of business. For this purpose, it is very important for all the entities to

make sure that they are focused with highly regulated financial reporting regime. With the help

of it, possibility of making mistakes in the books of accounting will be reduced and the accounts

6

will be more transparent. There are various advantages and disadvantages of it for users as well

as prepares which are as follows:

Advantages of highly regulated financial reporting regime:

Highly regulated regime of financial reporting will be beneficial for users as with the help

of it they will be able to get accurate information of the company and use it according to

their interest.

When highly regulated financial reporting regime will be followed by the preparers then

it will provide them various benefits as it will result in high level of accuracy and

transparency in the final accounts. With the help of it, the entities can attract large

number of investors (Sohn, 2016).

Disadvantages of highly regulated financial reporting regime:

Due to high level of regulation in the financial reporting the difficulty for users in

understanding all the aspects of final accounts will be increased which may lead them

towards formulation of wrong decision (Velichko, Tshovrebov and Niyazgulov, 2020).

The restriction in highly regulated financial reporting regime are very high due to which

the preparers may have to be extra focused with compilation of all the rules and

regulations. If they will ignore a single one then it may result in action against them.

c. Different limitations for financial statements

While formulating the financial statements it is very important for all the companies to be

aware of all the limitations of it. Some of them are listed below:

Financial statements ignore the implications of non-monetary factors which results in

inappropriate information about actual position of business (Taiwo, 2016).

In the formulation of final accounts only historical costs are considered due to which the

market prices of assets are ignored and the stakeholders are not able to analyse the actual

value of the business.

CONCLUSION

From the above project report it has been concluded that accounting fundamentals are the

main elements that are required to be focused by all the entities while performing reporting

related activities. In order to attain all the goals, it will be very important for businesses to make

sure that they are able to formulate effective strategies for future. While formulating the financial

7

as prepares which are as follows:

Advantages of highly regulated financial reporting regime:

Highly regulated regime of financial reporting will be beneficial for users as with the help

of it they will be able to get accurate information of the company and use it according to

their interest.

When highly regulated financial reporting regime will be followed by the preparers then

it will provide them various benefits as it will result in high level of accuracy and

transparency in the final accounts. With the help of it, the entities can attract large

number of investors (Sohn, 2016).

Disadvantages of highly regulated financial reporting regime:

Due to high level of regulation in the financial reporting the difficulty for users in

understanding all the aspects of final accounts will be increased which may lead them

towards formulation of wrong decision (Velichko, Tshovrebov and Niyazgulov, 2020).

The restriction in highly regulated financial reporting regime are very high due to which

the preparers may have to be extra focused with compilation of all the rules and

regulations. If they will ignore a single one then it may result in action against them.

c. Different limitations for financial statements

While formulating the financial statements it is very important for all the companies to be

aware of all the limitations of it. Some of them are listed below:

Financial statements ignore the implications of non-monetary factors which results in

inappropriate information about actual position of business (Taiwo, 2016).

In the formulation of final accounts only historical costs are considered due to which the

market prices of assets are ignored and the stakeholders are not able to analyse the actual

value of the business.

CONCLUSION

From the above project report it has been concluded that accounting fundamentals are the

main elements that are required to be focused by all the entities while performing reporting

related activities. In order to attain all the goals, it will be very important for businesses to make

sure that they are able to formulate effective strategies for future. While formulating the financial

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

statements such as profit and loss account and balance sheet it will be essential for the managers

to take all the adjustments in to consideration. It will help to analyse actual position of business

and facilitate the users to make decision for future. Ratio analysis is the process of analysing the

position of business as all of them guide to determine liquidity and profitability of business. If

the management teams of the companies will not be able to form strategies for future accounting

to the actual position then it may affect the execution of future activities. There are various users

of financial statements and they are interested for different purposes in the information provided

by the final accounts. These group of users are board members, internal and external users.

Highly regulated financial reporting regime is required to be focused by all the entities as it can

help to reach the predetermined goals and objectives. Apart from this, it is also very important

for business entities to analyse the limitations of the final accounts so that possibility of errors

could be ignored.

8

to take all the adjustments in to consideration. It will help to analyse actual position of business

and facilitate the users to make decision for future. Ratio analysis is the process of analysing the

position of business as all of them guide to determine liquidity and profitability of business. If

the management teams of the companies will not be able to form strategies for future accounting

to the actual position then it may affect the execution of future activities. There are various users

of financial statements and they are interested for different purposes in the information provided

by the final accounts. These group of users are board members, internal and external users.

Highly regulated financial reporting regime is required to be focused by all the entities as it can

help to reach the predetermined goals and objectives. Apart from this, it is also very important

for business entities to analyse the limitations of the final accounts so that possibility of errors

could be ignored.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Aldeia, S., 2019. Fundamentals of expenses’ non-deductibility in the companies' income tax law:

Portuguese’s case.

An, R., Chiu, P. C. and Zhang, Y., 2020. Back to Fundamentals: The Accrual–Cash Flow

Correlation, the Inverted-U Pattern, and Stock Returns. Available at SSRN 3603096.

Chen, W., Shroff, P. K. and Zhang, I., 2019. Fair value accounting: Consequences of booking

market-driven goodwill impairment. Available at SSRN 2420528.

Christodoulou, D., Clubb, C. and Mcleay, S., 2016. A structural accounting framework for

estimating the expected rate of return on equity. Abacus. 52(1). pp.176-210.

Chu, L., Mathieu, R. and Mbagwu, C., 2018. The association between firm fundamentals and

bank interest rates under different measures of risk. Advances in accounting. 41. pp.46-

58.

Goldschmidt, J., 2020. Fundamentals of Business-Introduction to Information Technology.

Hesarzadeh, R., Bazrafshan, A. and Rajabalizadeh, J., 2019. Financial reporting readability:

Managerial choices versus firm fundamentals. Spanish Journal of Finance and

Accounting/Revista Española de Financiación y Contabilidad. pp.1-31.

Sohn, B. C., 2016. The effect of accounting comparability on the accrual-based and real earnings

management. Journal of Accounting and Public Policy. 35(5). pp.513-539.

Taiwo, J. N., 2016. Effect of ICT on accounting information system and organisational

performance: The application of information and communication technology on

accounting information system. European Journal of Business and Social Sciences.

5(2). pp.1-15.

Velichko, E., Tshovrebov, E. and Niyazgulov, U., 2020. Organizational, technical and economic

fundamentals of waste management and monitoring. In E3S Web of Conferences (Vol.

164. p. 08031). EDP Sciences.

9

Books and Journals:

Aldeia, S., 2019. Fundamentals of expenses’ non-deductibility in the companies' income tax law:

Portuguese’s case.

An, R., Chiu, P. C. and Zhang, Y., 2020. Back to Fundamentals: The Accrual–Cash Flow

Correlation, the Inverted-U Pattern, and Stock Returns. Available at SSRN 3603096.

Chen, W., Shroff, P. K. and Zhang, I., 2019. Fair value accounting: Consequences of booking

market-driven goodwill impairment. Available at SSRN 2420528.

Christodoulou, D., Clubb, C. and Mcleay, S., 2016. A structural accounting framework for

estimating the expected rate of return on equity. Abacus. 52(1). pp.176-210.

Chu, L., Mathieu, R. and Mbagwu, C., 2018. The association between firm fundamentals and

bank interest rates under different measures of risk. Advances in accounting. 41. pp.46-

58.

Goldschmidt, J., 2020. Fundamentals of Business-Introduction to Information Technology.

Hesarzadeh, R., Bazrafshan, A. and Rajabalizadeh, J., 2019. Financial reporting readability:

Managerial choices versus firm fundamentals. Spanish Journal of Finance and

Accounting/Revista Española de Financiación y Contabilidad. pp.1-31.

Sohn, B. C., 2016. The effect of accounting comparability on the accrual-based and real earnings

management. Journal of Accounting and Public Policy. 35(5). pp.513-539.

Taiwo, J. N., 2016. Effect of ICT on accounting information system and organisational

performance: The application of information and communication technology on

accounting information system. European Journal of Business and Social Sciences.

5(2). pp.1-15.

Velichko, E., Tshovrebov, E. and Niyazgulov, U., 2020. Organizational, technical and economic

fundamentals of waste management and monitoring. In E3S Web of Conferences (Vol.

164. p. 08031). EDP Sciences.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.