Accounting Fundamentals: Journal Entries, Statements, and Analysis

VerifiedAdded on 2023/01/06

|16

|3528

|40

Essay

AI Summary

This essay provides a comprehensive overview of accounting fundamentals, starting with an introduction to key concepts and principles. The main body of the essay is divided into four tasks. Task 1 focuses on completing journal entries, preparing an updated trial balance, and constructing a statement of profit and loss account, along with a statement of financial position. Task 2 critically assesses the relevance of financial literacy to business managers, highlighting its importance in decision-making and understanding financial impacts. Task 3 involves journal entries, trial balance updates, and the creation of financial statements with additional adjustments. Task 4 compares the results of two businesses, identifying the better performer. The essay concludes with a summary of the key findings and references supporting the analysis.

Essay on accounting

fundamentals

fundamentals

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................2

MAIN BODY..................................................................................................................................2

TASK 1............................................................................................................................................2

1. Complete the Journal entries required to use additional information......................................2

2. Updated trial balance...............................................................................................................3

3. Statement of profit and loss account........................................................................................4

TASK 2............................................................................................................................................5

Critically assess the relevance of financial literacy to business managers..................................5

TASK 3............................................................................................................................................8

1. Journal entries by using additional adjustment........................................................................8

2. Updated Trial balance..............................................................................................................9

3. Statement of Profit or Loss and Statement of Financial position............................................9

TASK 4..........................................................................................................................................11

Compare results and identify the better of the two businesses..................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

1

MAIN BODY..................................................................................................................................2

TASK 1............................................................................................................................................2

1. Complete the Journal entries required to use additional information......................................2

2. Updated trial balance...............................................................................................................3

3. Statement of profit and loss account........................................................................................4

TASK 2............................................................................................................................................5

Critically assess the relevance of financial literacy to business managers..................................5

TASK 3............................................................................................................................................8

1. Journal entries by using additional adjustment........................................................................8

2. Updated Trial balance..............................................................................................................9

3. Statement of Profit or Loss and Statement of Financial position............................................9

TASK 4..........................................................................................................................................11

Compare results and identify the better of the two businesses..................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

1

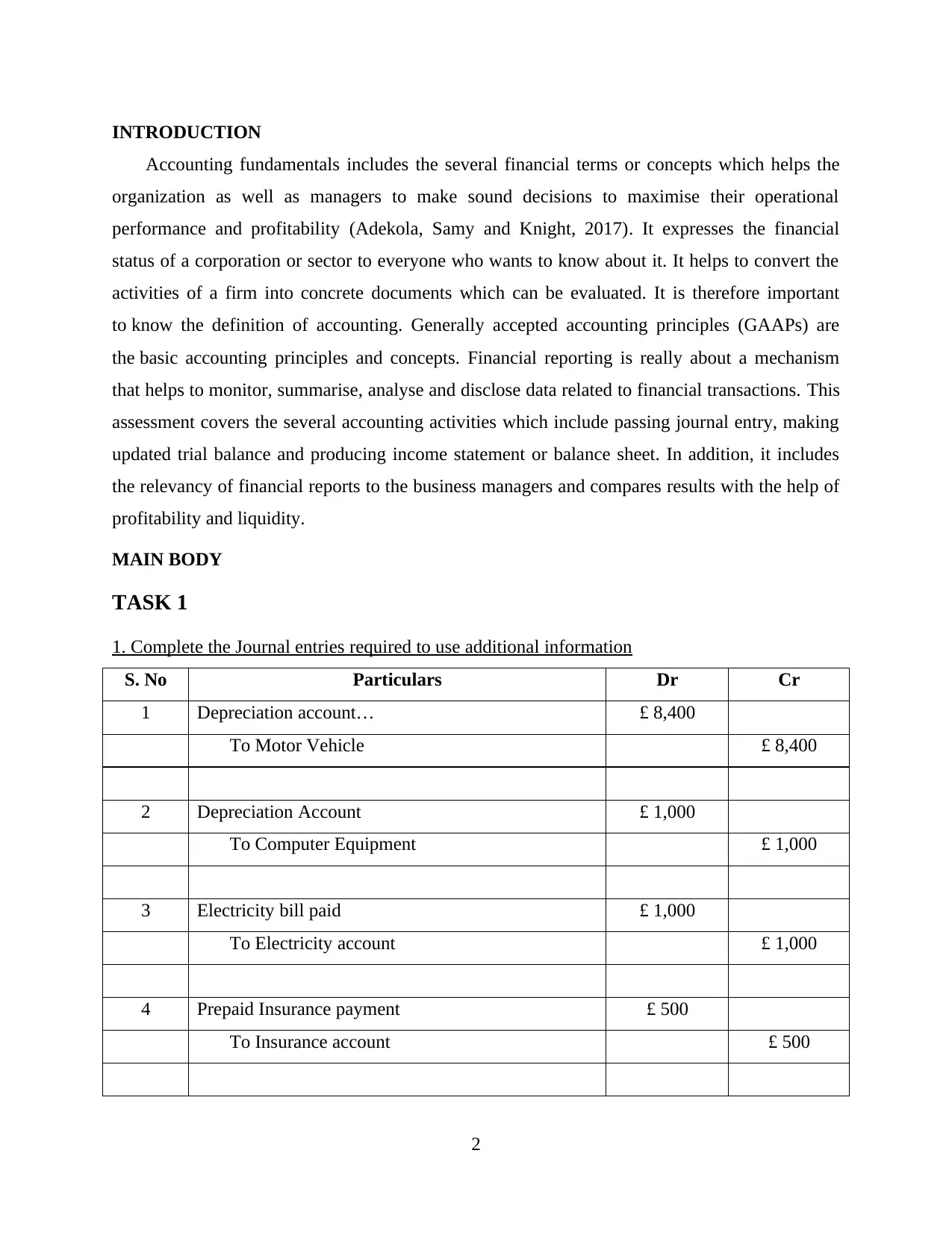

INTRODUCTION

Accounting fundamentals includes the several financial terms or concepts which helps the

organization as well as managers to make sound decisions to maximise their operational

performance and profitability (Adekola, Samy and Knight, 2017). It expresses the financial

status of a corporation or sector to everyone who wants to know about it. It helps to convert the

activities of a firm into concrete documents which can be evaluated. It is therefore important

to know the definition of accounting. Generally accepted accounting principles (GAAPs) are

the basic accounting principles and concepts. Financial reporting is really about a mechanism

that helps to monitor, summarise, analyse and disclose data related to financial transactions. This

assessment covers the several accounting activities which include passing journal entry, making

updated trial balance and producing income statement or balance sheet. In addition, it includes

the relevancy of financial reports to the business managers and compares results with the help of

profitability and liquidity.

MAIN BODY

TASK 1

1. Complete the Journal entries required to use additional information

S. No Particulars Dr Cr

1 Depreciation account… £ 8,400

To Motor Vehicle £ 8,400

2 Depreciation Account £ 1,000

To Computer Equipment £ 1,000

3 Electricity bill paid £ 1,000

To Electricity account £ 1,000

4 Prepaid Insurance payment £ 500

To Insurance account £ 500

2

Accounting fundamentals includes the several financial terms or concepts which helps the

organization as well as managers to make sound decisions to maximise their operational

performance and profitability (Adekola, Samy and Knight, 2017). It expresses the financial

status of a corporation or sector to everyone who wants to know about it. It helps to convert the

activities of a firm into concrete documents which can be evaluated. It is therefore important

to know the definition of accounting. Generally accepted accounting principles (GAAPs) are

the basic accounting principles and concepts. Financial reporting is really about a mechanism

that helps to monitor, summarise, analyse and disclose data related to financial transactions. This

assessment covers the several accounting activities which include passing journal entry, making

updated trial balance and producing income statement or balance sheet. In addition, it includes

the relevancy of financial reports to the business managers and compares results with the help of

profitability and liquidity.

MAIN BODY

TASK 1

1. Complete the Journal entries required to use additional information

S. No Particulars Dr Cr

1 Depreciation account… £ 8,400

To Motor Vehicle £ 8,400

2 Depreciation Account £ 1,000

To Computer Equipment £ 1,000

3 Electricity bill paid £ 1,000

To Electricity account £ 1,000

4 Prepaid Insurance payment £ 500

To Insurance account £ 500

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5 Tax Expenses £ 1,920

To Outstanding Tax Expenses £ 1,920

2. Updated trial balance

Particulars Debit Credit

Accounts Payable £ 16,120

Accounts Receivables. £ 16,480

Carriage Inwards £ 2,440

Computer Equipment at cost £ 10,000

Carriage Outwards £ 4,000

Drawings £ 6,500

Electricity £ 7,000

Loan Interest £ 480

Provision for Doubtful Debts £ 1,000

Insurance £ 1,000

Motor Vehicle at Cost £ 51,200

Capital £ 84,760

Opening Inventory £ 3,600

Accumulated Depreciation -Motor Vehicle £ 17,600

Depreciation on Motor Vehicle £ 8400

Depreciation on Computer Equipment £ 1,000

Petty Cash £ 40

Bank Overdraft £ 59,120

Purchases £ 26,400

Rent £ 5,600

Sales £ 60,600

Telephones £ 4,320

Tax Expenses £ 1,920

3

To Outstanding Tax Expenses £ 1,920

2. Updated trial balance

Particulars Debit Credit

Accounts Payable £ 16,120

Accounts Receivables. £ 16,480

Carriage Inwards £ 2,440

Computer Equipment at cost £ 10,000

Carriage Outwards £ 4,000

Drawings £ 6,500

Electricity £ 7,000

Loan Interest £ 480

Provision for Doubtful Debts £ 1,000

Insurance £ 1,000

Motor Vehicle at Cost £ 51,200

Capital £ 84,760

Opening Inventory £ 3,600

Accumulated Depreciation -Motor Vehicle £ 17,600

Depreciation on Motor Vehicle £ 8400

Depreciation on Computer Equipment £ 1,000

Petty Cash £ 40

Bank Overdraft £ 59,120

Purchases £ 26,400

Rent £ 5,600

Sales £ 60,600

Telephones £ 4,320

Tax Expenses £ 1,920

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

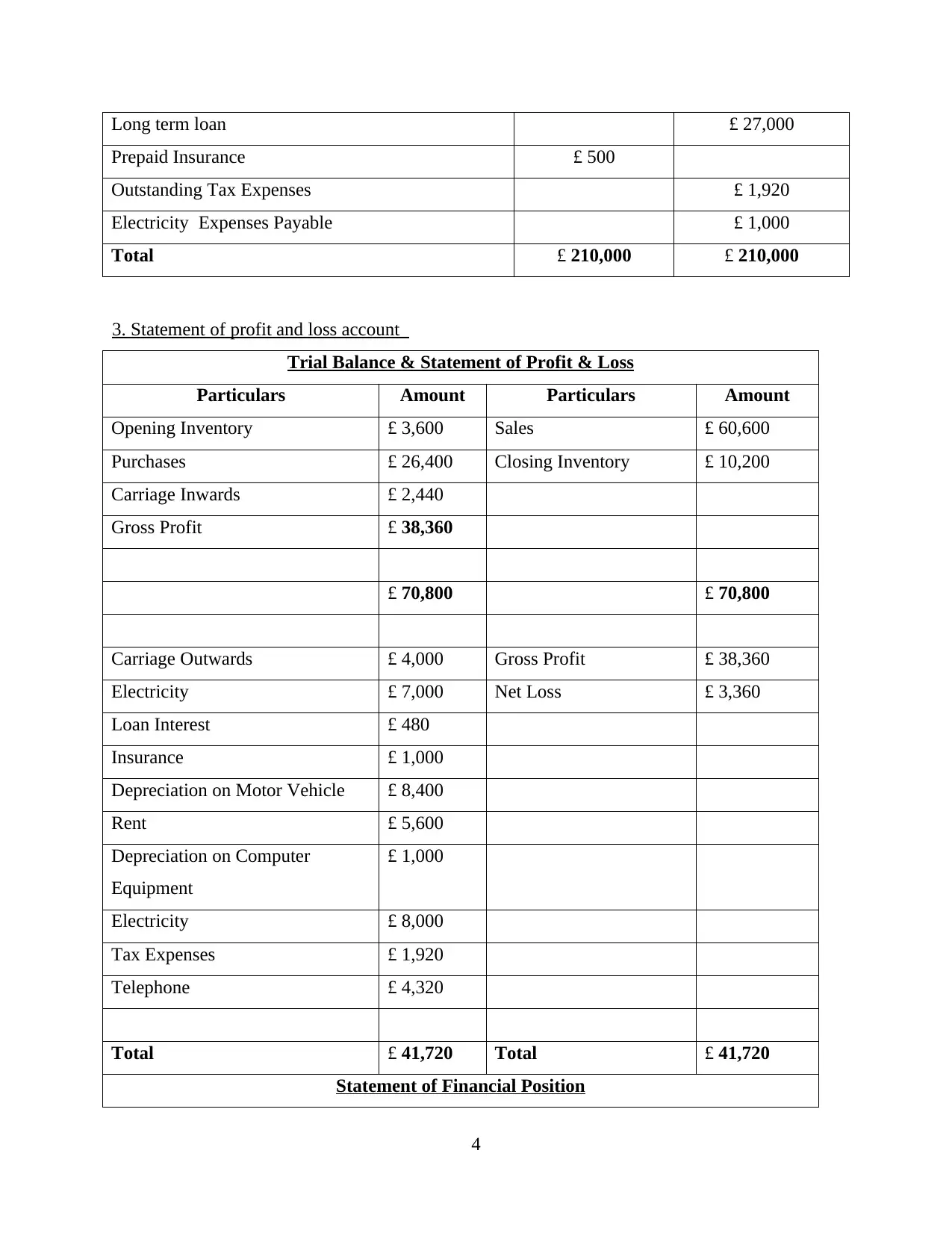

Long term loan £ 27,000

Prepaid Insurance £ 500

Outstanding Tax Expenses £ 1,920

Electricity Expenses Payable £ 1,000

Total £ 210,000 £ 210,000

3. Statement of profit and loss account

Trial Balance & Statement of Profit & Loss

Particulars Amount Particulars Amount

Opening Inventory £ 3,600 Sales £ 60,600

Purchases £ 26,400 Closing Inventory £ 10,200

Carriage Inwards £ 2,440

Gross Profit £ 38,360

£ 70,800 £ 70,800

Carriage Outwards £ 4,000 Gross Profit £ 38,360

Electricity £ 7,000 Net Loss £ 3,360

Loan Interest £ 480

Insurance £ 1,000

Depreciation on Motor Vehicle £ 8,400

Rent £ 5,600

Depreciation on Computer

Equipment

£ 1,000

Electricity £ 8,000

Tax Expenses £ 1,920

Telephone £ 4,320

Total £ 41,720 Total £ 41,720

Statement of Financial Position

4

Prepaid Insurance £ 500

Outstanding Tax Expenses £ 1,920

Electricity Expenses Payable £ 1,000

Total £ 210,000 £ 210,000

3. Statement of profit and loss account

Trial Balance & Statement of Profit & Loss

Particulars Amount Particulars Amount

Opening Inventory £ 3,600 Sales £ 60,600

Purchases £ 26,400 Closing Inventory £ 10,200

Carriage Inwards £ 2,440

Gross Profit £ 38,360

£ 70,800 £ 70,800

Carriage Outwards £ 4,000 Gross Profit £ 38,360

Electricity £ 7,000 Net Loss £ 3,360

Loan Interest £ 480

Insurance £ 1,000

Depreciation on Motor Vehicle £ 8,400

Rent £ 5,600

Depreciation on Computer

Equipment

£ 1,000

Electricity £ 8,000

Tax Expenses £ 1,920

Telephone £ 4,320

Total £ 41,720 Total £ 41,720

Statement of Financial Position

4

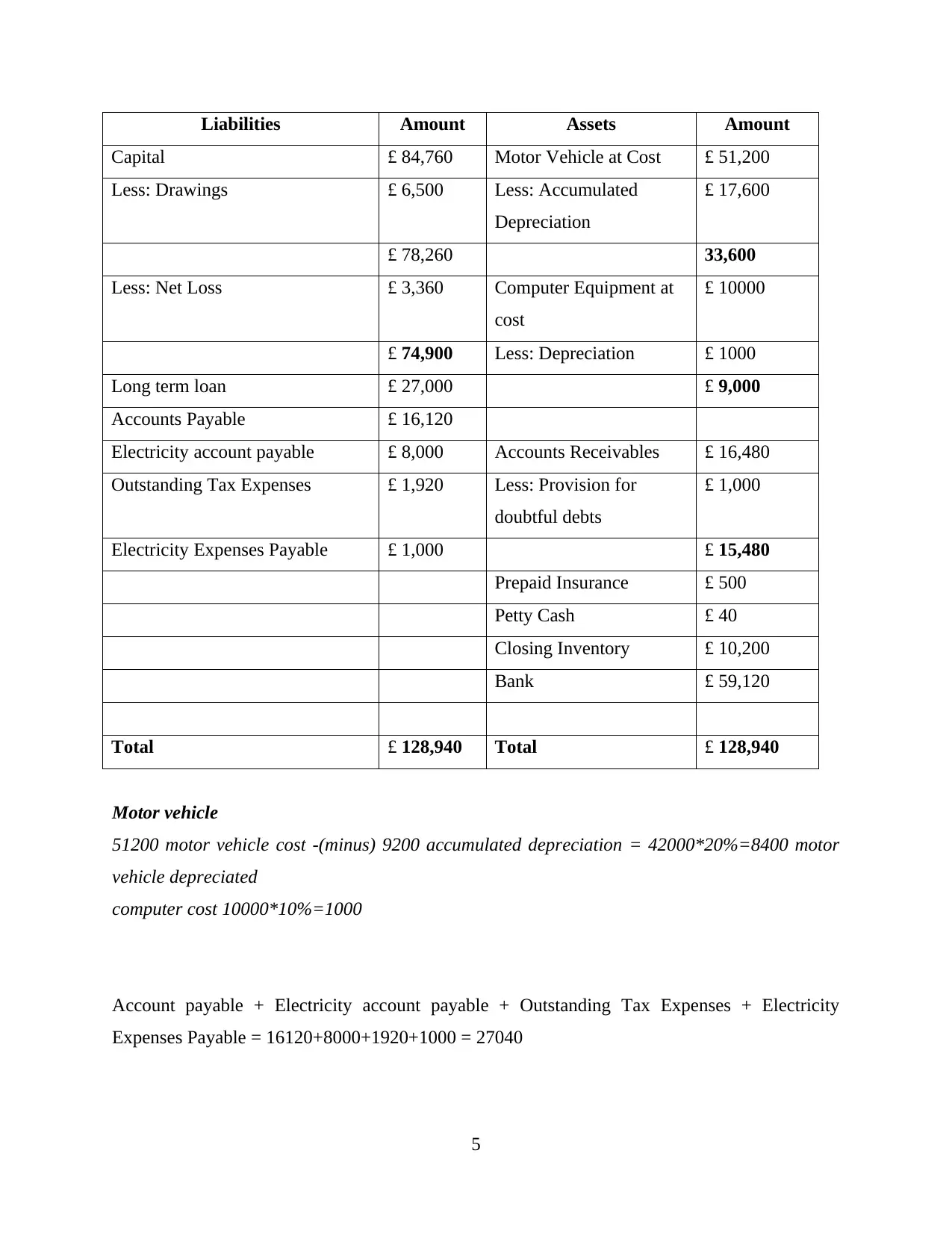

Liabilities Amount Assets Amount

Capital £ 84,760 Motor Vehicle at Cost £ 51,200

Less: Drawings £ 6,500 Less: Accumulated

Depreciation

£ 17,600

£ 78,260 33,600

Less: Net Loss £ 3,360 Computer Equipment at

cost

£ 10000

£ 74,900 Less: Depreciation £ 1000

Long term loan £ 27,000 £ 9,000

Accounts Payable £ 16,120

Electricity account payable £ 8,000 Accounts Receivables £ 16,480

Outstanding Tax Expenses £ 1,920 Less: Provision for

doubtful debts

£ 1,000

Electricity Expenses Payable £ 1,000 £ 15,480

Prepaid Insurance £ 500

Petty Cash £ 40

Closing Inventory £ 10,200

Bank £ 59,120

Total £ 128,940 Total £ 128,940

Motor vehicle

51200 motor vehicle cost -(minus) 9200 accumulated depreciation = 42000*20%=8400 motor

vehicle depreciated

computer cost 10000*10%=1000

Account payable + Electricity account payable + Outstanding Tax Expenses + Electricity

Expenses Payable = 16120+8000+1920+1000 = 27040

5

Capital £ 84,760 Motor Vehicle at Cost £ 51,200

Less: Drawings £ 6,500 Less: Accumulated

Depreciation

£ 17,600

£ 78,260 33,600

Less: Net Loss £ 3,360 Computer Equipment at

cost

£ 10000

£ 74,900 Less: Depreciation £ 1000

Long term loan £ 27,000 £ 9,000

Accounts Payable £ 16,120

Electricity account payable £ 8,000 Accounts Receivables £ 16,480

Outstanding Tax Expenses £ 1,920 Less: Provision for

doubtful debts

£ 1,000

Electricity Expenses Payable £ 1,000 £ 15,480

Prepaid Insurance £ 500

Petty Cash £ 40

Closing Inventory £ 10,200

Bank £ 59,120

Total £ 128,940 Total £ 128,940

Motor vehicle

51200 motor vehicle cost -(minus) 9200 accumulated depreciation = 42000*20%=8400 motor

vehicle depreciated

computer cost 10000*10%=1000

Account payable + Electricity account payable + Outstanding Tax Expenses + Electricity

Expenses Payable = 16120+8000+1920+1000 = 27040

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

Critically assess the relevance of financial literacy to business managers

It is true that, primary objective of financial statement or related information is to informed

their users about the business performance throw-out the period (Burger and Curtis, 2017). In

addition, business managers are the primary users of financial reports because they has to made

several decisions in relation to the organization or it will helps in maximising business

performance and outcomes.

Financial literacy is a comprehension of financial terms, claims and definitions, and

awareness about how this knowledge can be used to make a financial impression while making

any business decision by managers. There are five ways which shows that how financial literacy

relevant for business managers and these are discussed below:

Understand the impact of their actions: Once business manager understand company's

financial statements, so they can track particular items which have an effect

on their organisation's bottom line. If applicable to the day to day tasks, knowledge into the

company's financial reporting can be a motivational factor for managers and their team. Knowing

the effect of decisions have on financial wellbeing of the larger company will help manager to

keep a big picture in mind.

Make informed decisions: In relation to manager of organization, financial literacy will

help them to grips with issues with a fresh toolkit. When confronted with a tough strategic move,

manager can comfortably understand the financial consequences before evaluating their choices

and making right choice for their team and company (Dewi, Azam and Yusoff, 2019). Financial

literacy will encourage manager to become an excellently-rounded leader who recognizes several

aspects of any problems that arise.

Support Team’s Budget: When team members are in need of funds for any project or

product, business managers understanding related to finance requirement could even help them

to build a strong argument. For instance, if the team is demanding fund for project management

tool, managers could measure the expected financial return predicated on how much more

effectively the software can enable their workers to focus. Demonstrating the impact on

company's bottom line will make manager's case more interesting.

Improve their Negotiation Skills: Financial knowledge can help business managers thrive

at the bargaining table. Whether people are negotiating wage, perks, or the scale of the project,

6

Critically assess the relevance of financial literacy to business managers

It is true that, primary objective of financial statement or related information is to informed

their users about the business performance throw-out the period (Burger and Curtis, 2017). In

addition, business managers are the primary users of financial reports because they has to made

several decisions in relation to the organization or it will helps in maximising business

performance and outcomes.

Financial literacy is a comprehension of financial terms, claims and definitions, and

awareness about how this knowledge can be used to make a financial impression while making

any business decision by managers. There are five ways which shows that how financial literacy

relevant for business managers and these are discussed below:

Understand the impact of their actions: Once business manager understand company's

financial statements, so they can track particular items which have an effect

on their organisation's bottom line. If applicable to the day to day tasks, knowledge into the

company's financial reporting can be a motivational factor for managers and their team. Knowing

the effect of decisions have on financial wellbeing of the larger company will help manager to

keep a big picture in mind.

Make informed decisions: In relation to manager of organization, financial literacy will

help them to grips with issues with a fresh toolkit. When confronted with a tough strategic move,

manager can comfortably understand the financial consequences before evaluating their choices

and making right choice for their team and company (Dewi, Azam and Yusoff, 2019). Financial

literacy will encourage manager to become an excellently-rounded leader who recognizes several

aspects of any problems that arise.

Support Team’s Budget: When team members are in need of funds for any project or

product, business managers understanding related to finance requirement could even help them

to build a strong argument. For instance, if the team is demanding fund for project management

tool, managers could measure the expected financial return predicated on how much more

effectively the software can enable their workers to focus. Demonstrating the impact on

company's bottom line will make manager's case more interesting.

Improve their Negotiation Skills: Financial knowledge can help business managers thrive

at the bargaining table. Whether people are negotiating wage, perks, or the scale of the project,

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

having a clear understanding of larger financial image can represent users well. If the issue of

negotiating process will affect the monetary well-being of the organisation, acknowledging how

to actually speak about the financial consequences of their desired outcome can influence the

discussion in their favour.

Become financially efficient: Financial literacy helps the business managers to understand

how each of their team’s expenses needs to play into obligations on the organisation's balance

sheet which can allow managers to assess to be more efficient and profitable. Sometimes there's

a team who previously subscribed and no longer allows, or perhaps they can find a free variant of

a tool their team already has to pay for (Baksaas and Stenheim, 2019).

When business manager aware of how each expenditure factors into balance sheet, this can be

better to spot strategies to become more cost-effective (Hermuningsih, Kirana and Erawati,

2019).

There are some other different types of users who interested in the financial report of the

organizations and these are discussed below:

Management: They are interested in the financial reports of company. Even if they are

people who are beginning to prepare the financial reports of board & members as a

whole, they must relate to them when taking into account the growth/ performance of the

company. The Board of Directors evaluates financial statement from perspective of

equity, efficiency, cash sales, income and expenditures, capital assets, budget

requirements, loans to be paid, finance or economics and several other daily basis

operations. Organisation must be able to make sound decisions on financial reports.

Investors: They really like to know and stay up-to - date with financial status of the

company. They would also like make investment decision on the basis of their

profitability and financial performance. Because of this, investors are interested in the

financial reports.

Customers: These users also have to view financial position of the business where they

purchase products and services. Large consumers will want to maintain a long-term

agreement or contract with the company, and they'd like to engage with a company that is

financially stable. In addition, profitable company might provide its customers with

services at a discount rate relative to the industry.

7

negotiating process will affect the monetary well-being of the organisation, acknowledging how

to actually speak about the financial consequences of their desired outcome can influence the

discussion in their favour.

Become financially efficient: Financial literacy helps the business managers to understand

how each of their team’s expenses needs to play into obligations on the organisation's balance

sheet which can allow managers to assess to be more efficient and profitable. Sometimes there's

a team who previously subscribed and no longer allows, or perhaps they can find a free variant of

a tool their team already has to pay for (Baksaas and Stenheim, 2019).

When business manager aware of how each expenditure factors into balance sheet, this can be

better to spot strategies to become more cost-effective (Hermuningsih, Kirana and Erawati,

2019).

There are some other different types of users who interested in the financial report of the

organizations and these are discussed below:

Management: They are interested in the financial reports of company. Even if they are

people who are beginning to prepare the financial reports of board & members as a

whole, they must relate to them when taking into account the growth/ performance of the

company. The Board of Directors evaluates financial statement from perspective of

equity, efficiency, cash sales, income and expenditures, capital assets, budget

requirements, loans to be paid, finance or economics and several other daily basis

operations. Organisation must be able to make sound decisions on financial reports.

Investors: They really like to know and stay up-to - date with financial status of the

company. They would also like make investment decision on the basis of their

profitability and financial performance. Because of this, investors are interested in the

financial reports.

Customers: These users also have to view financial position of the business where they

purchase products and services. Large consumers will want to maintain a long-term

agreement or contract with the company, and they'd like to engage with a company that is

financially stable. In addition, profitable company might provide its customers with

services at a discount rate relative to the industry.

7

Competitors: These are another kind of users which also have to examine financial

position of entity & business. Customers who are stick with brand for longer time interval

mainly wants to know about how strong is position of a brand on basis of which they are

able to take interest in company.

Government: Some agencies like tax department, corporate tax etc. really have to go

through company's balance sheet to verify if the firm pays correct taxes or not. They

would like to charge tax estimates on the basis of the performance of the company and

the rules lay down.

Employees: These are the internal stakeholders who are interested in the company's

financial statement across various perspectives. They would just want to know how the

business does the award and sums are highly dependent on the earnings of the firm

(Hutton, 2017). They will also be looking for an in-depth summary of the market

situation and the current situation of the business sector that will be the consumers of the

financial statements. It would also want employees to understand entirely the finances.

Organisation can involve employees in decision-making process.

Above discuss parties are the users who are interested in the financial statement of company

but primary user is business managers who have to manage everything in the business

operations. They are updated with the every changes and business transection to make effective

decisions which helps in maximising productivity as well as profitability. It further helps in

increasing business objectives and goals.

TASK 3

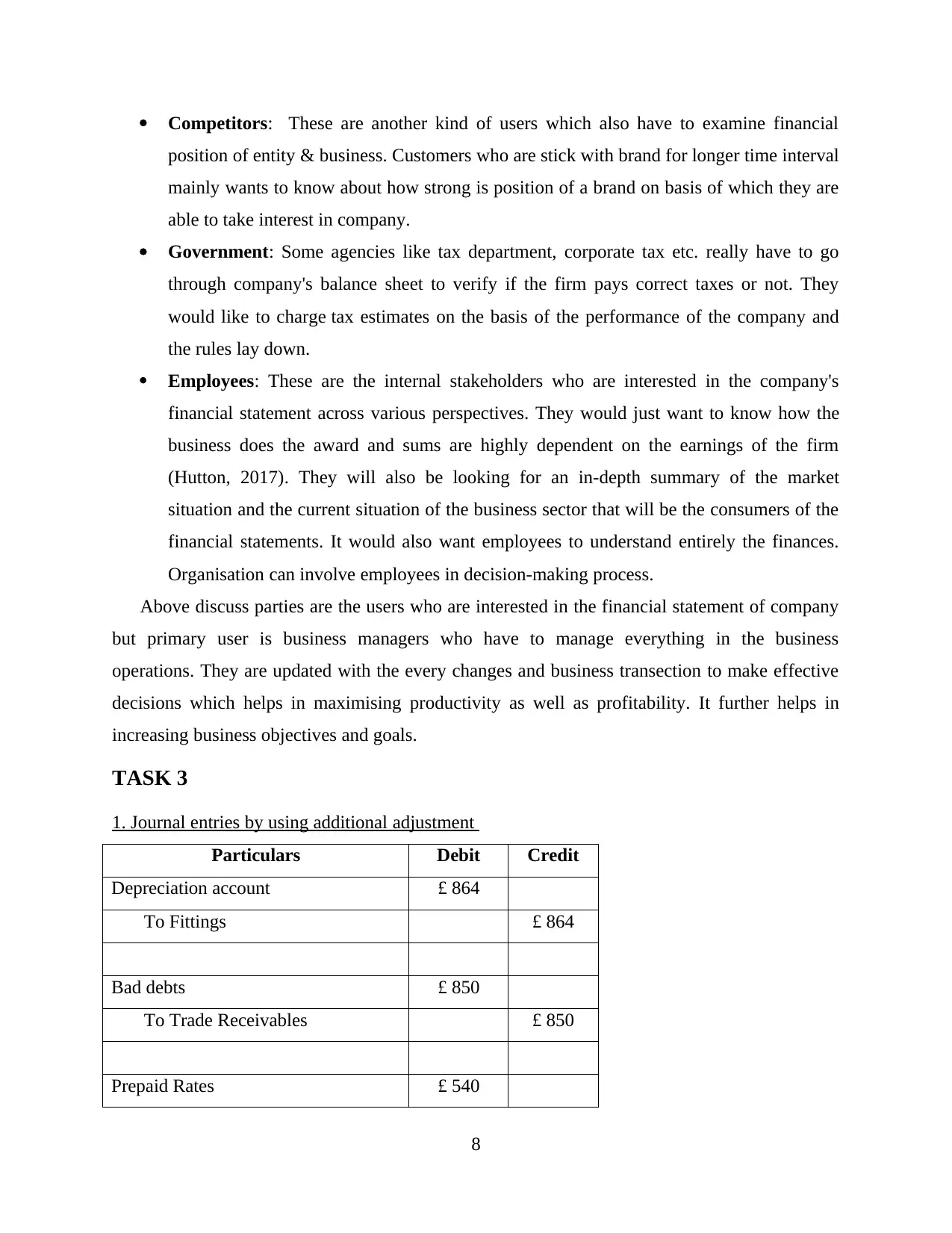

1. Journal entries by using additional adjustment

Particulars Debit Credit

Depreciation account £ 864

To Fittings £ 864

Bad debts £ 850

To Trade Receivables £ 850

Prepaid Rates £ 540

8

position of entity & business. Customers who are stick with brand for longer time interval

mainly wants to know about how strong is position of a brand on basis of which they are

able to take interest in company.

Government: Some agencies like tax department, corporate tax etc. really have to go

through company's balance sheet to verify if the firm pays correct taxes or not. They

would like to charge tax estimates on the basis of the performance of the company and

the rules lay down.

Employees: These are the internal stakeholders who are interested in the company's

financial statement across various perspectives. They would just want to know how the

business does the award and sums are highly dependent on the earnings of the firm

(Hutton, 2017). They will also be looking for an in-depth summary of the market

situation and the current situation of the business sector that will be the consumers of the

financial statements. It would also want employees to understand entirely the finances.

Organisation can involve employees in decision-making process.

Above discuss parties are the users who are interested in the financial statement of company

but primary user is business managers who have to manage everything in the business

operations. They are updated with the every changes and business transection to make effective

decisions which helps in maximising productivity as well as profitability. It further helps in

increasing business objectives and goals.

TASK 3

1. Journal entries by using additional adjustment

Particulars Debit Credit

Depreciation account £ 864

To Fittings £ 864

Bad debts £ 850

To Trade Receivables £ 850

Prepaid Rates £ 540

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To Rates £ 540

Drawings £ 450

To Bank £ 450

Trade Receivables £ 690

To Allowance for Doubtful debts £ 690

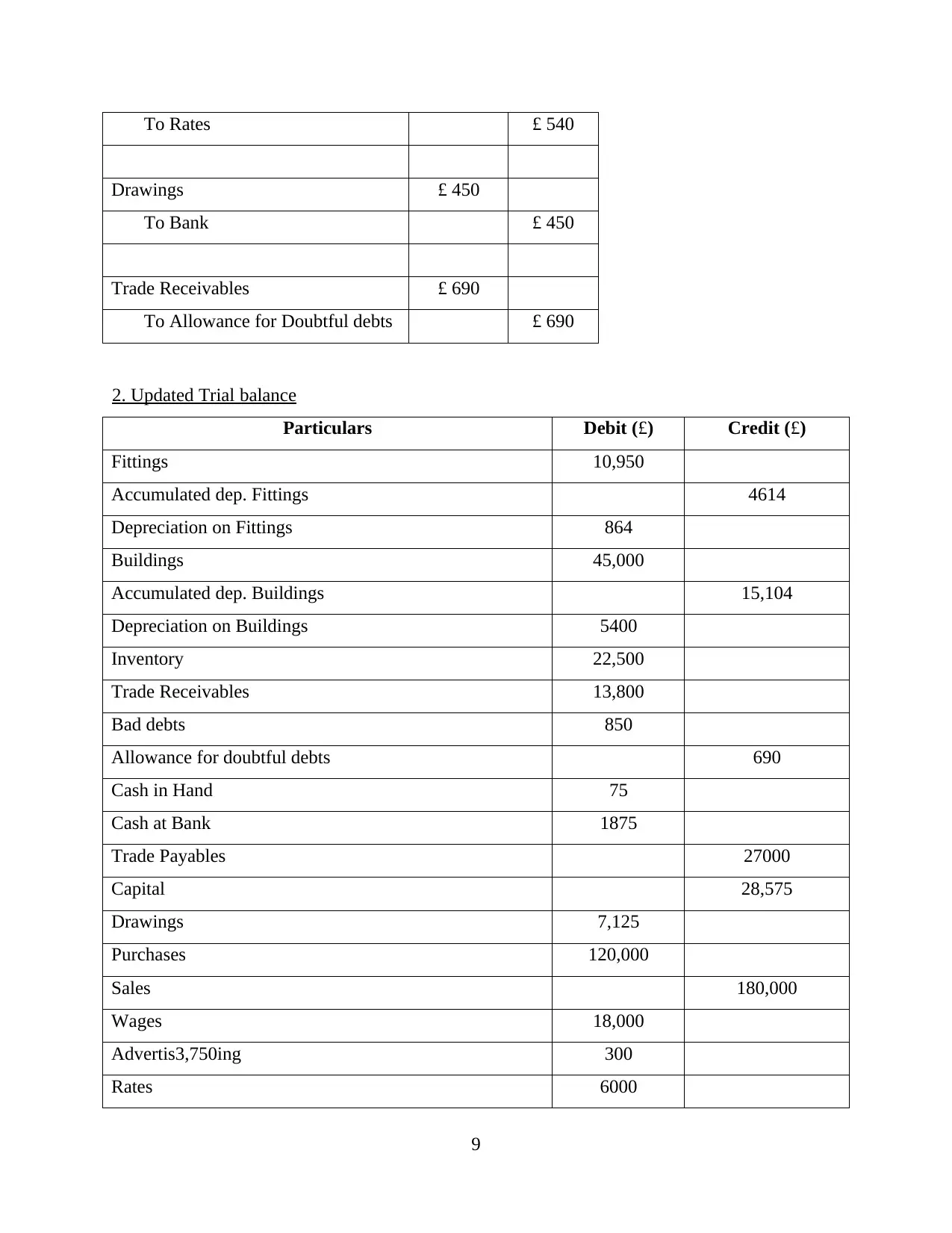

2. Updated Trial balance

Particulars Debit (£) Credit (£)

Fittings 10,950

Accumulated dep. Fittings 4614

Depreciation on Fittings 864

Buildings 45,000

Accumulated dep. Buildings 15,104

Depreciation on Buildings 5400

Inventory 22,500

Trade Receivables 13,800

Bad debts 850

Allowance for doubtful debts 690

Cash in Hand 75

Cash at Bank 1875

Trade Payables 27000

Capital 28,575

Drawings 7,125

Purchases 120,000

Sales 180,000

Wages 18,000

Advertis3,750ing 300

Rates 6000

9

Drawings £ 450

To Bank £ 450

Trade Receivables £ 690

To Allowance for Doubtful debts £ 690

2. Updated Trial balance

Particulars Debit (£) Credit (£)

Fittings 10,950

Accumulated dep. Fittings 4614

Depreciation on Fittings 864

Buildings 45,000

Accumulated dep. Buildings 15,104

Depreciation on Buildings 5400

Inventory 22,500

Trade Receivables 13,800

Bad debts 850

Allowance for doubtful debts 690

Cash in Hand 75

Cash at Bank 1875

Trade Payables 27000

Capital 28,575

Drawings 7,125

Purchases 120,000

Sales 180,000

Wages 18,000

Advertis3,750ing 300

Rates 6000

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bank Charges 2,700

Prepaid Rates 540

Total 255974 255974

Value of depreciation =

Fitting = 10950* 12/100 = 1314

Depreciation = 864

Initial balance = 3750

Deprecation = 3750*12/100 = 450

1314-450 = 864

Building = 45000

Accumulated depreciation opening balance value = 9000

Depreciation on building = 5400

Accumulated depreciation 15104

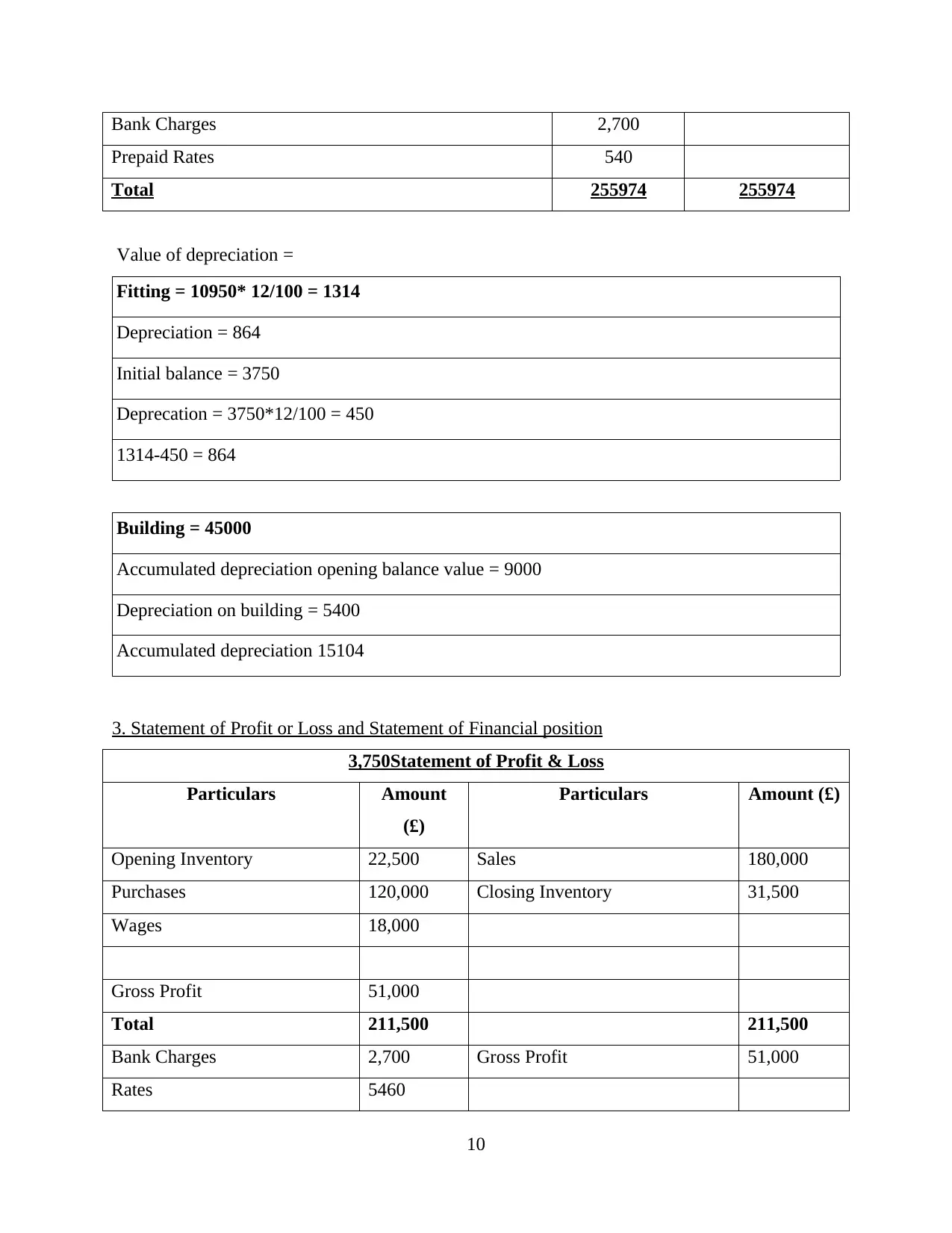

3. Statement of Profit or Loss and Statement of Financial position

3,750Statement of Profit & Loss

Particulars Amount

(£)

Particulars Amount (£)

Opening Inventory 22,500 Sales 180,000

Purchases 120,000 Closing Inventory 31,500

Wages 18,000

Gross Profit 51,000

Total 211,500 211,500

Bank Charges 2,700 Gross Profit 51,000

Rates 5460

10

Prepaid Rates 540

Total 255974 255974

Value of depreciation =

Fitting = 10950* 12/100 = 1314

Depreciation = 864

Initial balance = 3750

Deprecation = 3750*12/100 = 450

1314-450 = 864

Building = 45000

Accumulated depreciation opening balance value = 9000

Depreciation on building = 5400

Accumulated depreciation 15104

3. Statement of Profit or Loss and Statement of Financial position

3,750Statement of Profit & Loss

Particulars Amount

(£)

Particulars Amount (£)

Opening Inventory 22,500 Sales 180,000

Purchases 120,000 Closing Inventory 31,500

Wages 18,000

Gross Profit 51,000

Total 211,500 211,500

Bank Charges 2,700 Gross Profit 51,000

Rates 5460

10

Advertising 300

Depreciation on Fittings 864

Depreciation on Buildings 5400

Allowance for Doubtful debts 690

Bad debts 850

Net Profit 16,264

Total 34000 Total 51,000

Statement of Financial Position

Liabilities Amount Assets Amount

Capital 28,575 Fittings 10,950

Less: Drawings 7,125 Accumulated dCash at Bankep.

Fittings

2886

21,450 8064

Add: Net Profit 16,264 Buildings 45000

37,714 Accumulated dep. Buildings 20,504

24,496

Trade Payable 27,000

Suspense account 14976 Trade Receivables 15,000

Less: Provision for doubtful debts 1890

13,110

Inventory 31,500

Prepaid Rates 540

Cash in HandCash at Bank 75

Cash at Bank 1875

Total 79,660 Total 79,660

TASK 4

Compare results and identify the better of the two businesses

Profitability ratio:Cash at Bank

11

Depreciation on Fittings 864

Depreciation on Buildings 5400

Allowance for Doubtful debts 690

Bad debts 850

Net Profit 16,264

Total 34000 Total 51,000

Statement of Financial Position

Liabilities Amount Assets Amount

Capital 28,575 Fittings 10,950

Less: Drawings 7,125 Accumulated dCash at Bankep.

Fittings

2886

21,450 8064

Add: Net Profit 16,264 Buildings 45000

37,714 Accumulated dep. Buildings 20,504

24,496

Trade Payable 27,000

Suspense account 14976 Trade Receivables 15,000

Less: Provision for doubtful debts 1890

13,110

Inventory 31,500

Prepaid Rates 540

Cash in HandCash at Bank 75

Cash at Bank 1875

Total 79,660 Total 79,660

TASK 4

Compare results and identify the better of the two businesses

Profitability ratio:Cash at Bank

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.