Accounting Fundamentals Exam: Cost Analysis and Management Accounting

VerifiedAdded on 2022/12/29

|7

|1404

|78

Homework Assignment

AI Summary

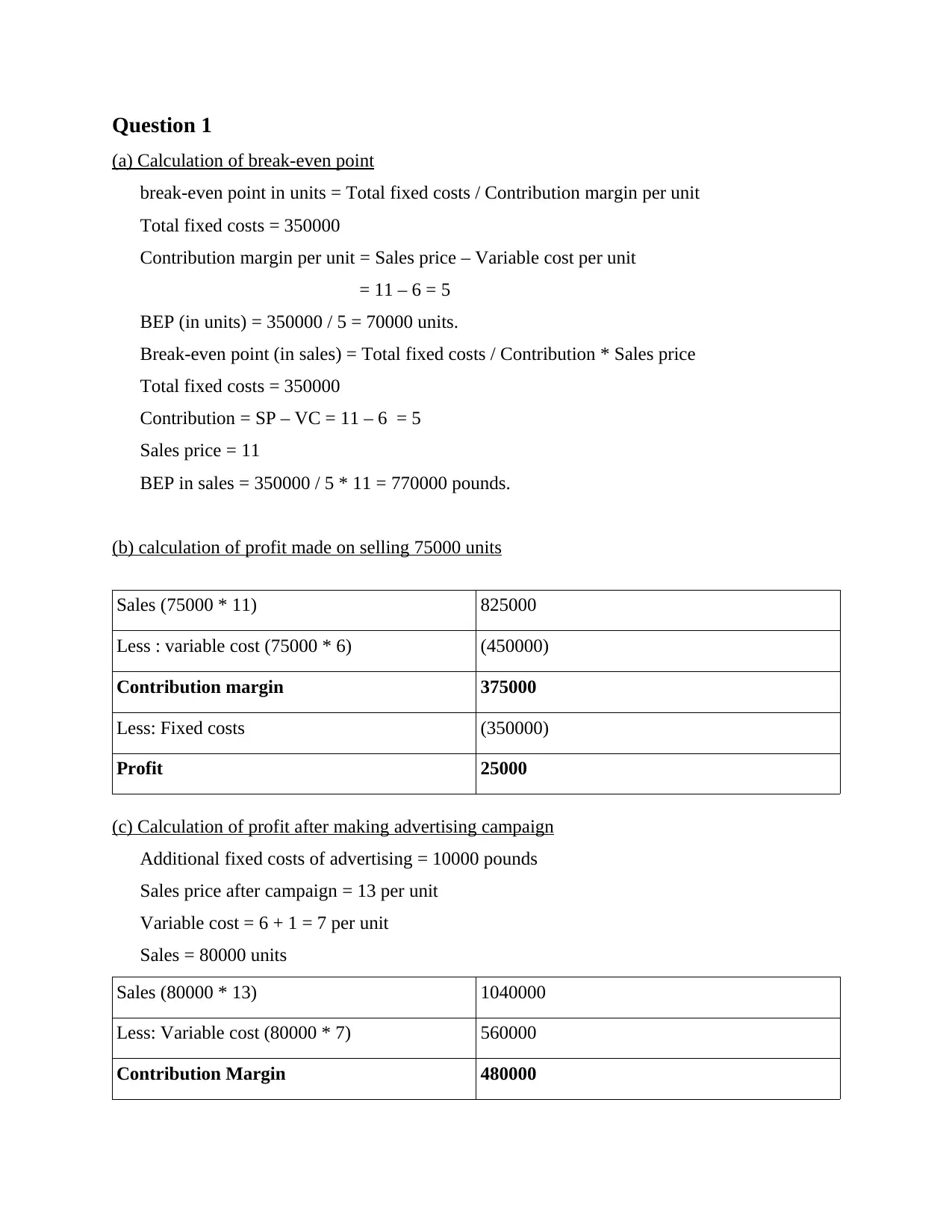

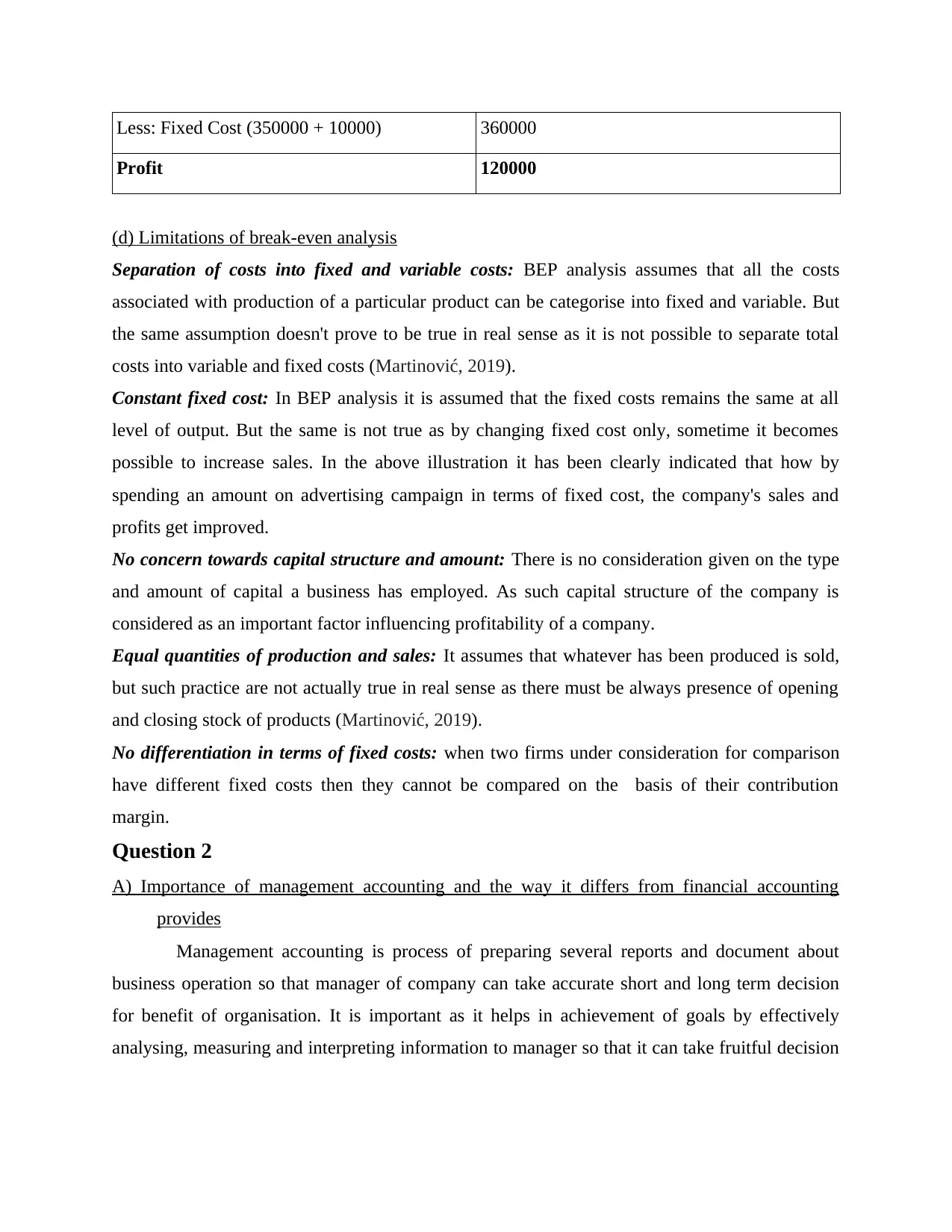

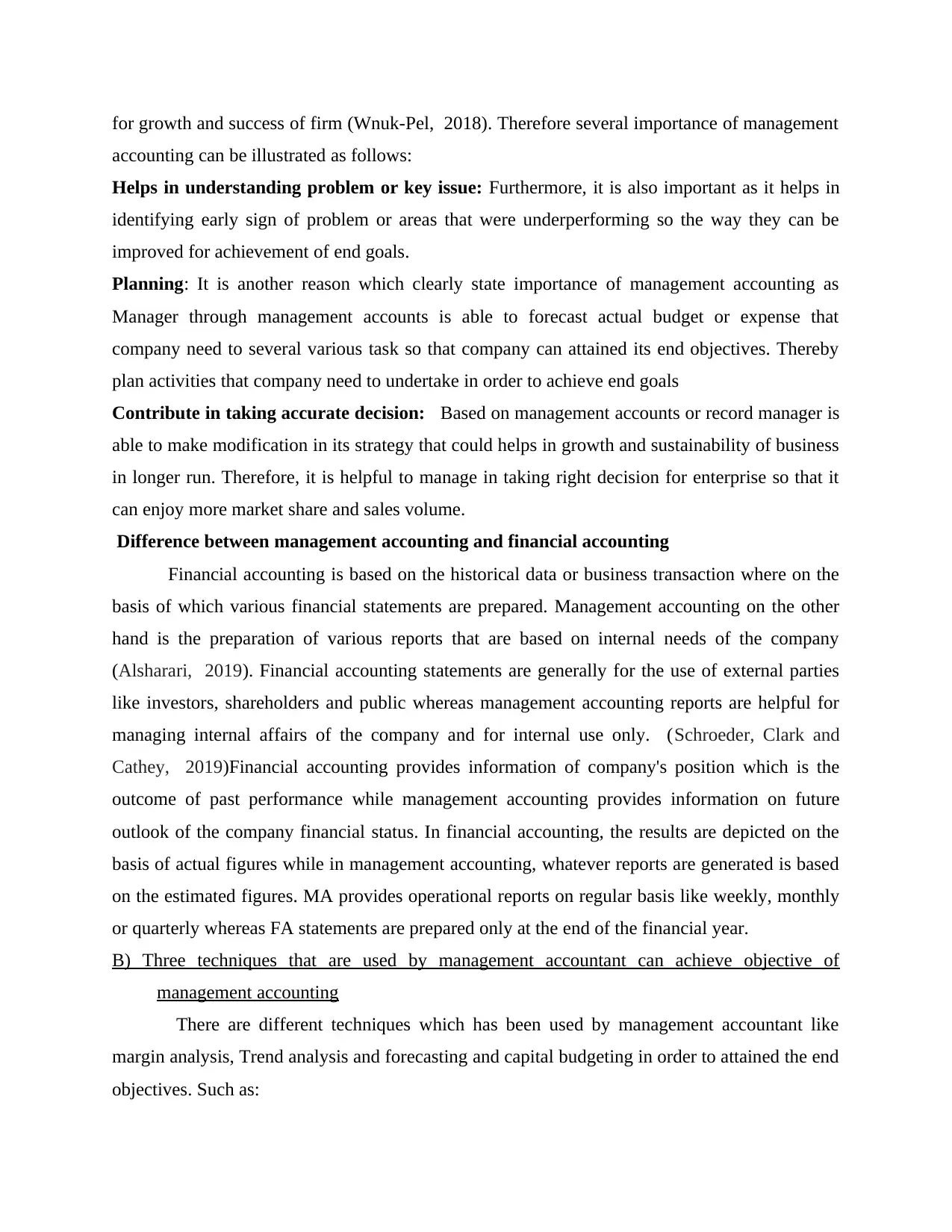

This assignment provides a detailed solution to an accounting fundamentals exam, covering key concepts such as break-even analysis, profit calculations, and the limitations of break-even analysis. The solution includes calculations for break-even points in units and sales, profit determination under different scenarios, and an analysis of the impact of an advertising campaign. Furthermore, the assignment explores the importance of management accounting, differentiating it from financial accounting and highlighting its role in aiding managerial decision-making. It also identifies and explains three key techniques used by management accountants, including margin analysis, capital budgeting, and trend analysis, demonstrating how these techniques contribute to achieving management accounting objectives. The solution references various academic sources to support its analysis and conclusions.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.