Accounting Fundamentals Report: Financial Position and Strategy

VerifiedAdded on 2023/03/17

|11

|1631

|46

Report

AI Summary

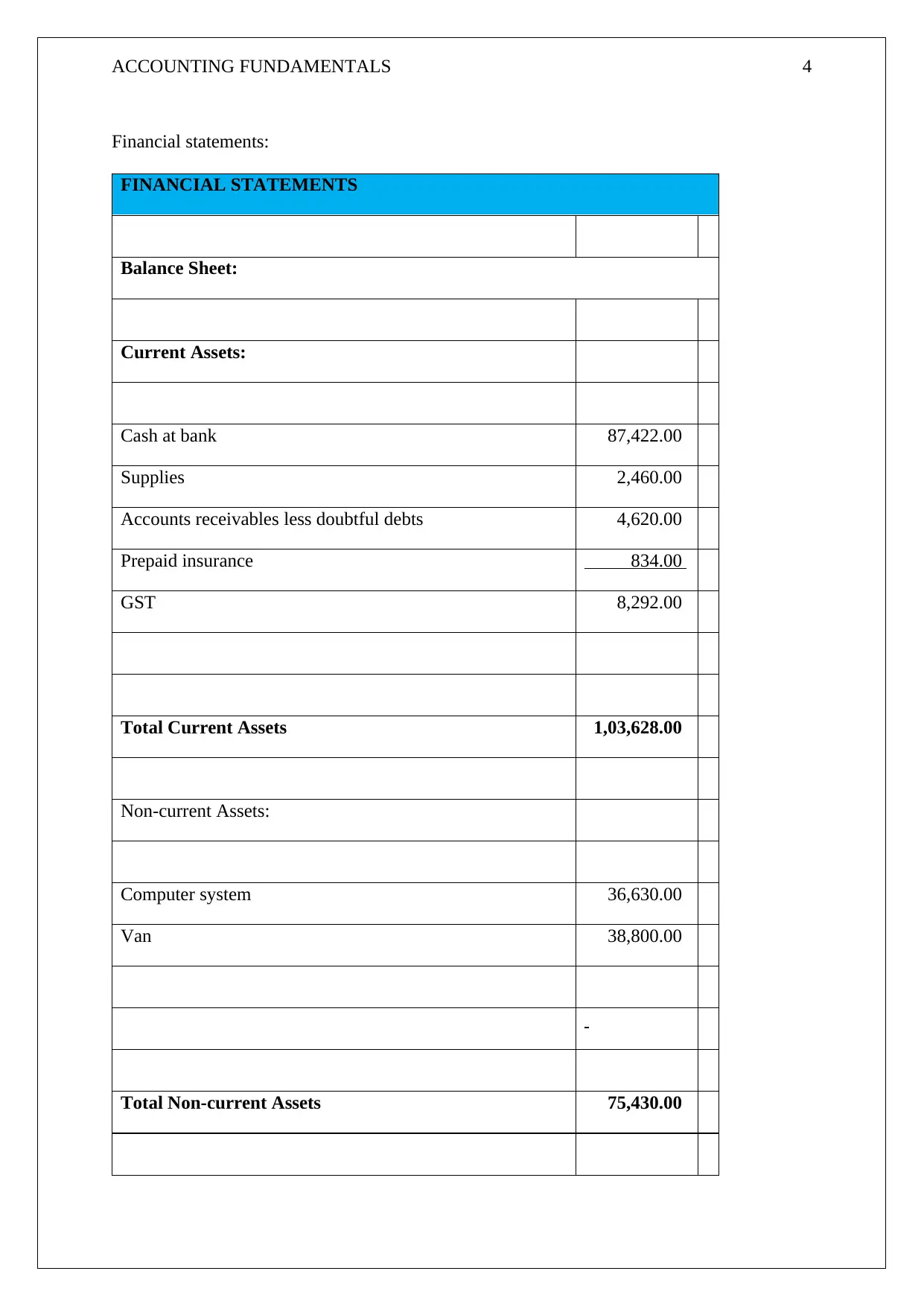

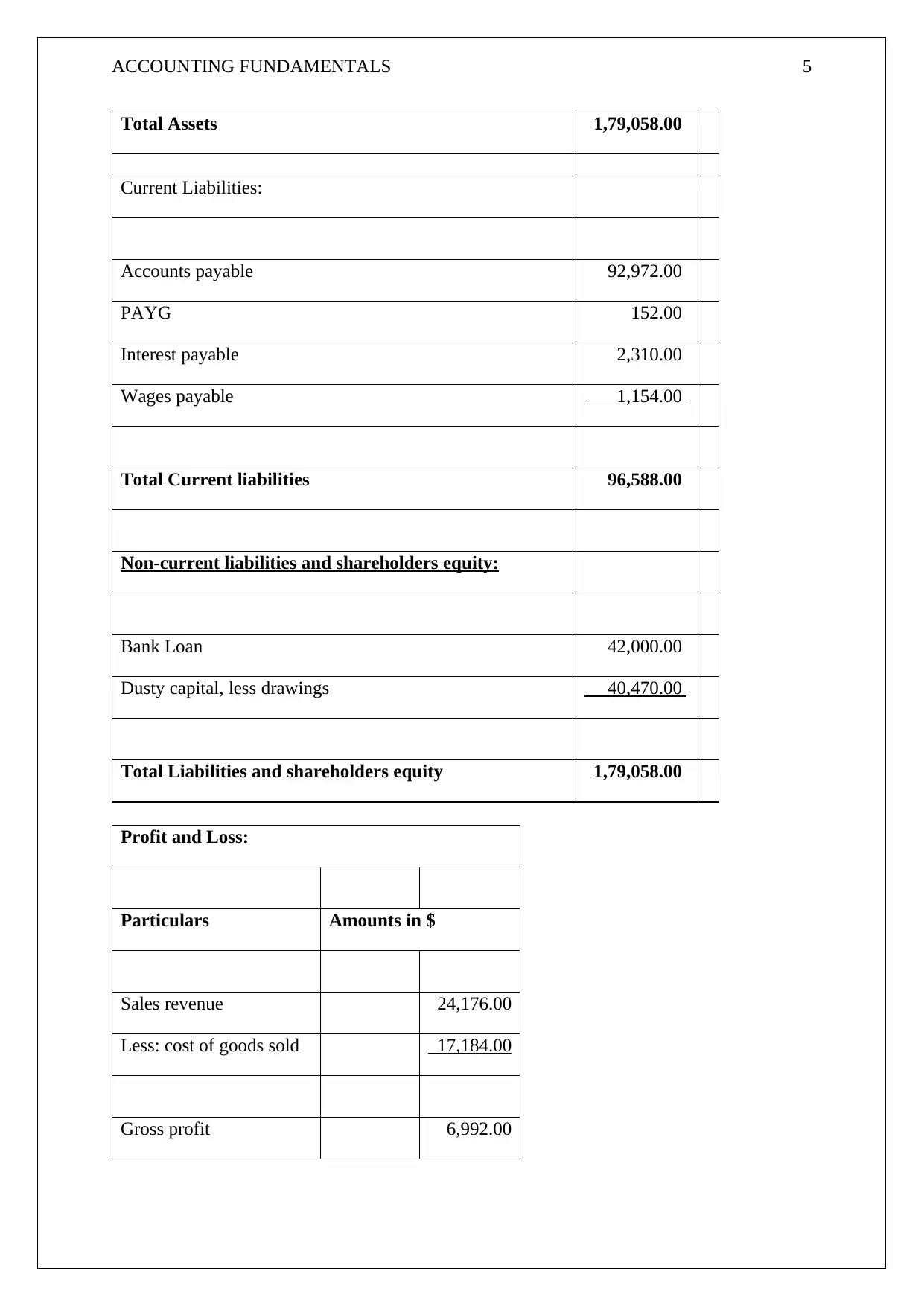

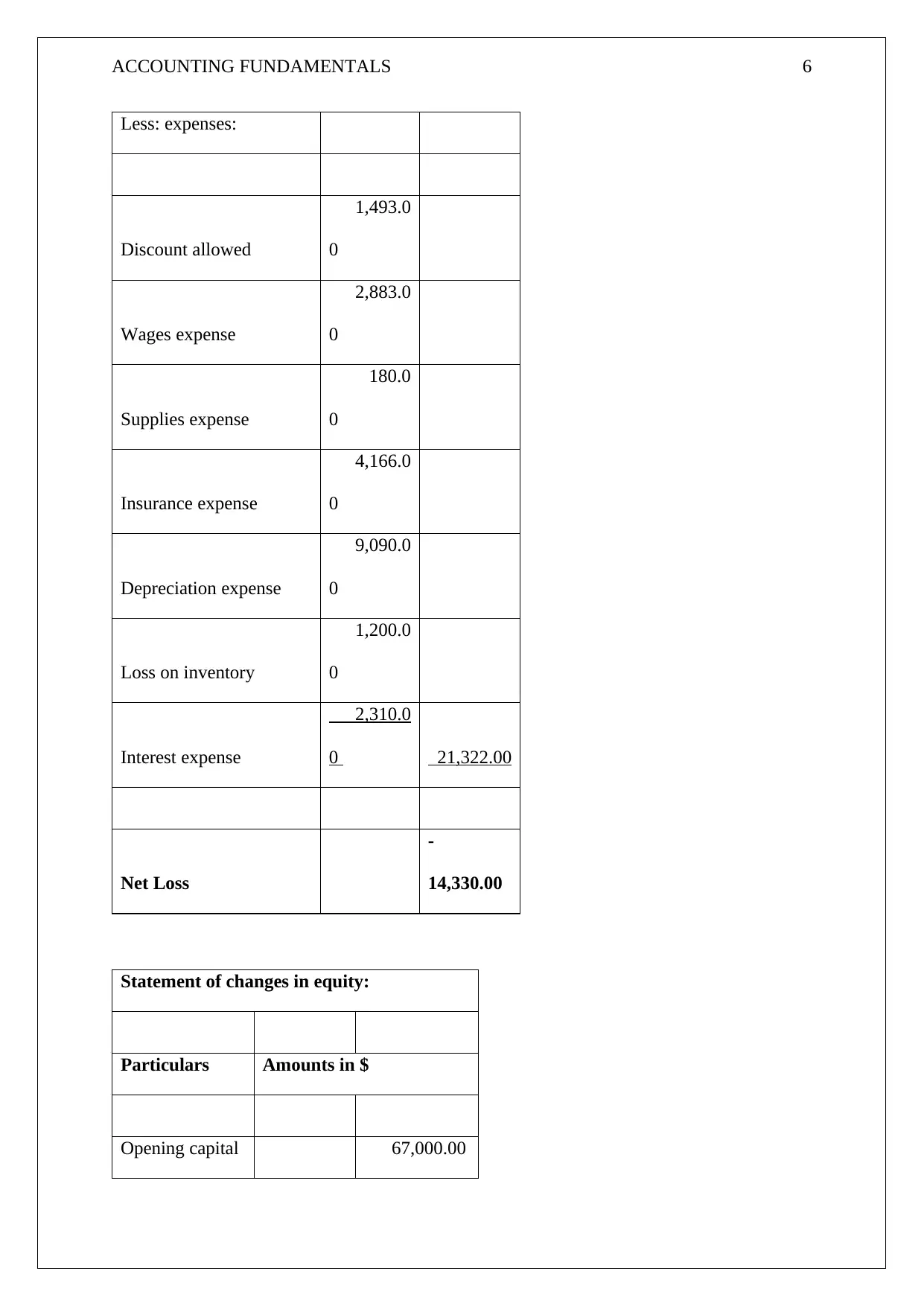

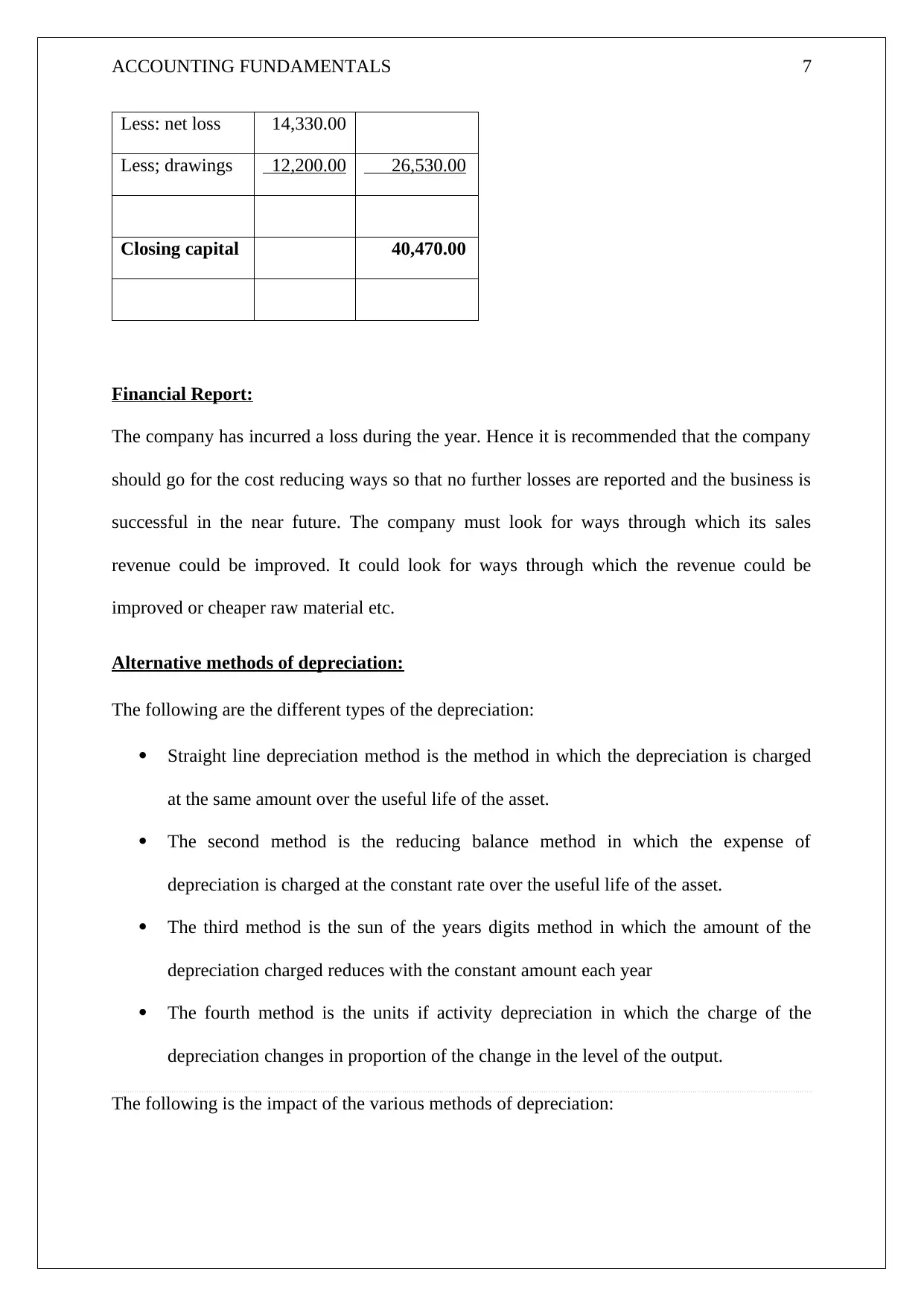

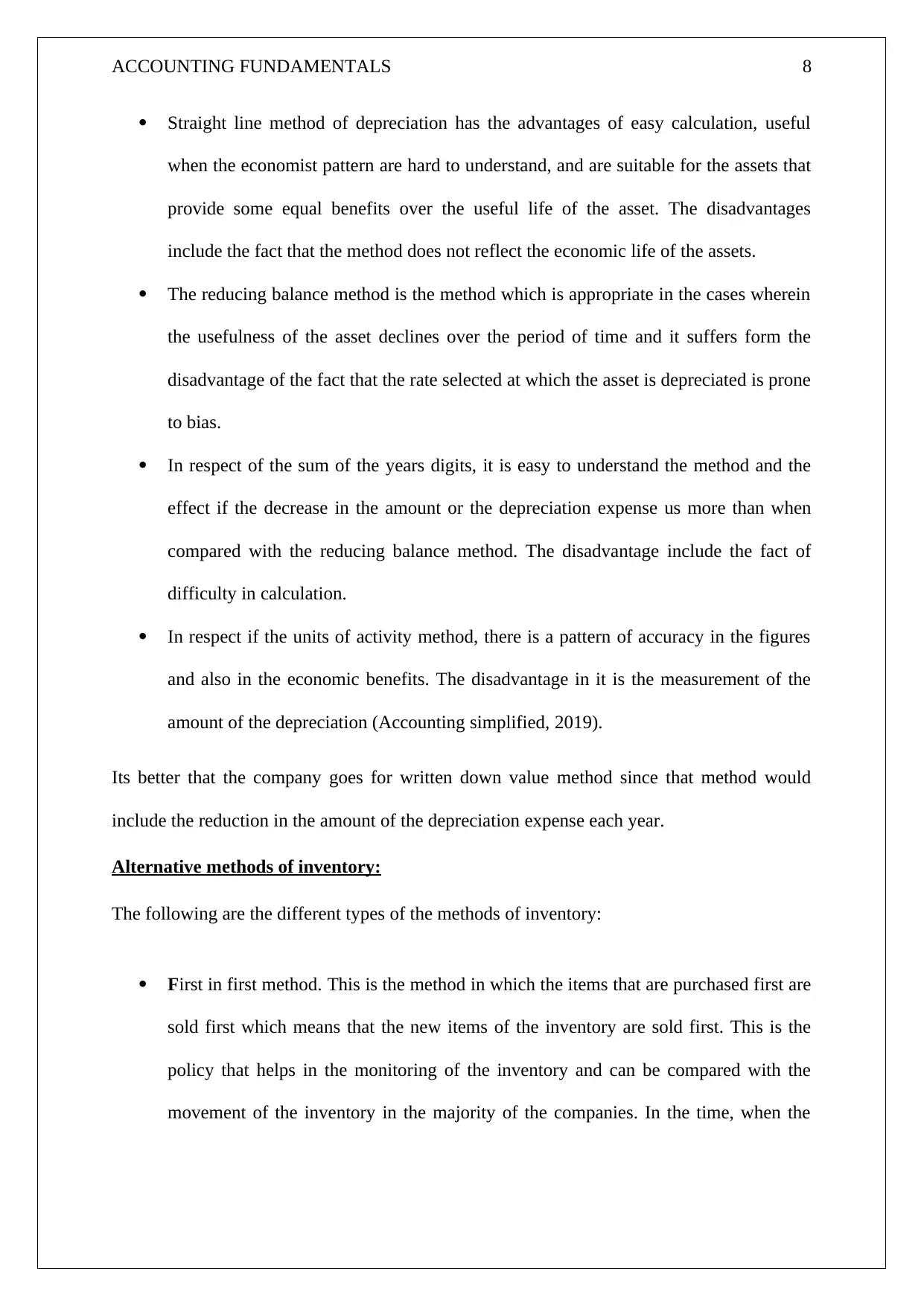

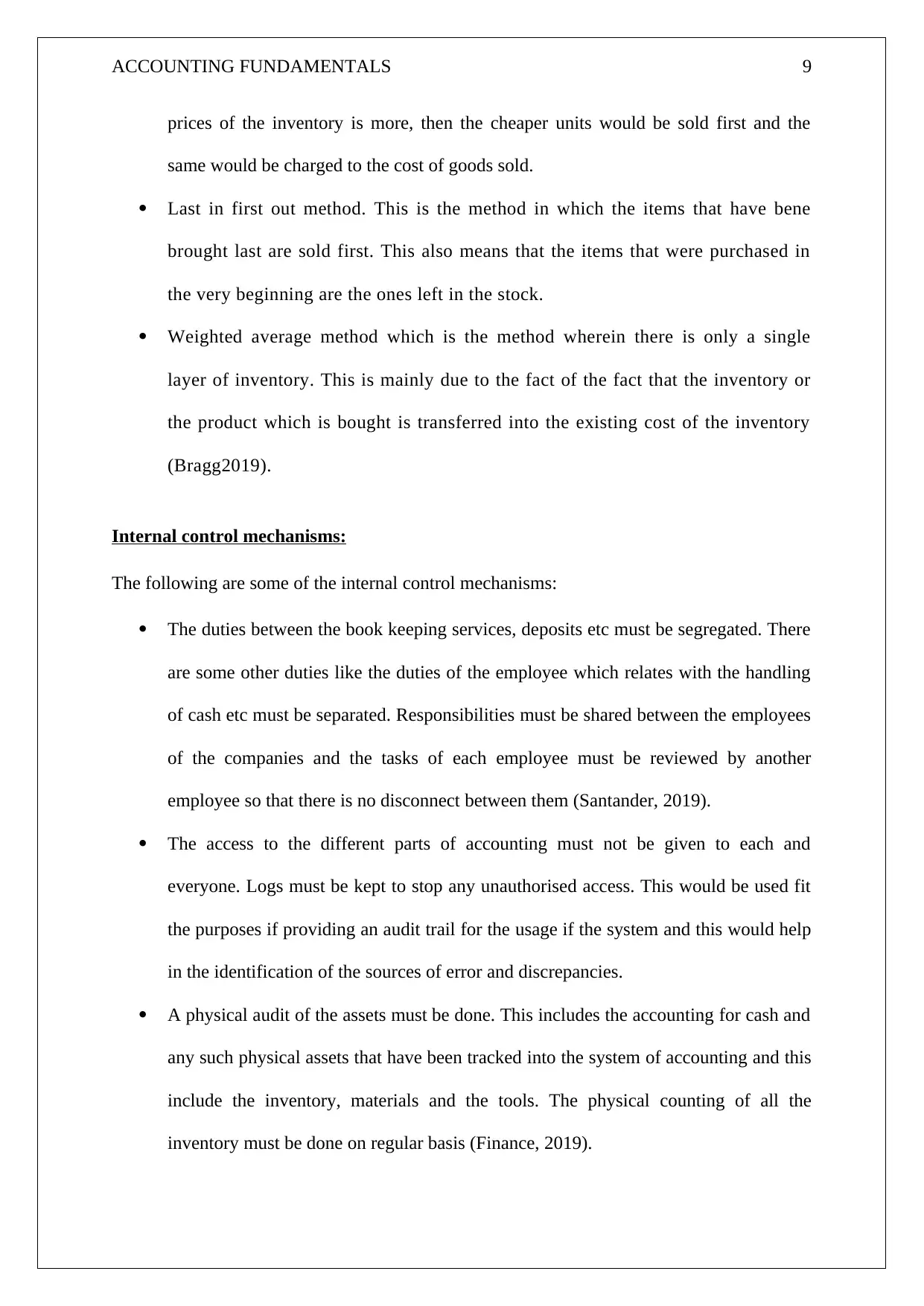

This report provides an overview of accounting fundamentals, including the creation and analysis of financial statements (balance sheet, profit and loss, and statement of changes in equity) for a company that has incurred a loss during the year. It explores various methods of depreciation (straight-line, reducing balance, sum of the years' digits, and units of activity) and inventory valuation (FIFO, LIFO, and weighted average), along with their respective advantages and disadvantages. The report also examines internal control mechanisms, such as segregation of duties, access controls, physical audits, documentation, trial balances, and account reconciliation. Finally, it concludes with recommendations for the company to improve its financial performance and future profitability, suggesting a focus on cost reduction, revenue enhancement, and the implementation of robust internal controls. The company is advised to use the written down value method of inventory.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.