Accounting Fundamentals: Analysis of Financial Statements Report

VerifiedAdded on 2022/11/13

|10

|1957

|459

Report

AI Summary

This report delves into the core principles of financial accounting, emphasizing its practical application in a business context. It outlines the accounting cycle, from transaction recording and classification to the preparation of financial statements. The report includes an illustrative example, presenting an income statement, balance sheet, and statement of changes in equity. It analyzes the business's financial performance, highlighting key metrics such as gross profit, operating expenses, and net loss, while also assessing its financial position concerning liquidity and solvency. Furthermore, it explores depreciation methods, inventory control systems, and internal control mechanisms. The report concludes with recommendations for optimizing financial practices, aiming to improve profitability and operational efficiency, and references various academic sources to support the analysis.

Running head: ACCOUNTING FUNDAMENTALS

Accounting Fundamentals

Name of the Student:

Name of the University:

Author’s Note:

Accounting Fundamentals

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FUNDAMENTALS

Executive Summary:

This report aimed at analyzing and understanding the fundamentals of financial accounting and

its application in business. Financial accounting is the process of recording, classifying,

summarizing and preparing financial reports for the use of financial information users. In this

report, the whole cycle of accounting has been illustrated with the help of a practical example.

Lastly, the report concludes with the analysis of such a financial statement to understand the

financial performance and position of the business.

Executive Summary:

This report aimed at analyzing and understanding the fundamentals of financial accounting and

its application in business. Financial accounting is the process of recording, classifying,

summarizing and preparing financial reports for the use of financial information users. In this

report, the whole cycle of accounting has been illustrated with the help of a practical example.

Lastly, the report concludes with the analysis of such a financial statement to understand the

financial performance and position of the business.

ACCOUNTING FUNDAMENTALS

Table of Contents

Introduction:....................................................................................................................................4

Financial Statement:........................................................................................................................4

Financial Performance and Financial Position:...............................................................................6

Investment in assets and depreciation method:...............................................................................7

Inventory Control System:...............................................................................................................8

Internal Control Mechanism:...........................................................................................................8

Conclusion:......................................................................................................................................9

References and bibliography:........................................................................................................10

Table of Contents

Introduction:....................................................................................................................................4

Financial Statement:........................................................................................................................4

Financial Performance and Financial Position:...............................................................................6

Investment in assets and depreciation method:...............................................................................7

Inventory Control System:...............................................................................................................8

Internal Control Mechanism:...........................................................................................................8

Conclusion:......................................................................................................................................9

References and bibliography:........................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FUNDAMENTALS

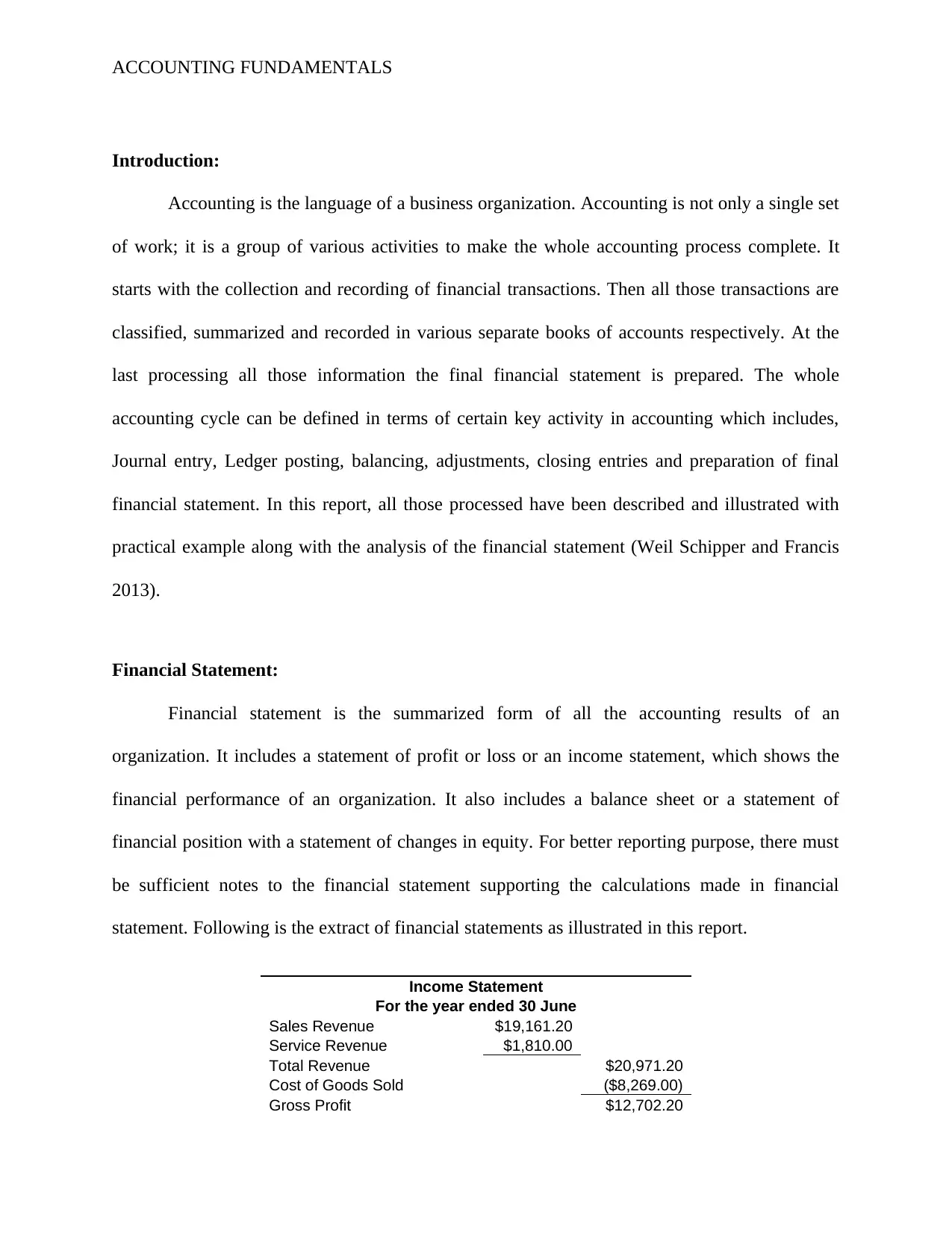

Introduction:

Accounting is the language of a business organization. Accounting is not only a single set

of work; it is a group of various activities to make the whole accounting process complete. It

starts with the collection and recording of financial transactions. Then all those transactions are

classified, summarized and recorded in various separate books of accounts respectively. At the

last processing all those information the final financial statement is prepared. The whole

accounting cycle can be defined in terms of certain key activity in accounting which includes,

Journal entry, Ledger posting, balancing, adjustments, closing entries and preparation of final

financial statement. In this report, all those processed have been described and illustrated with

practical example along with the analysis of the financial statement (Weil Schipper and Francis

2013).

Financial Statement:

Financial statement is the summarized form of all the accounting results of an

organization. It includes a statement of profit or loss or an income statement, which shows the

financial performance of an organization. It also includes a balance sheet or a statement of

financial position with a statement of changes in equity. For better reporting purpose, there must

be sufficient notes to the financial statement supporting the calculations made in financial

statement. Following is the extract of financial statements as illustrated in this report.

Income Statement

For the year ended 30 June

Sales Revenue $19,161.20

Service Revenue $1,810.00

Total Revenue $20,971.20

Cost of Goods Sold ($8,269.00)

Gross Profit $12,702.20

Introduction:

Accounting is the language of a business organization. Accounting is not only a single set

of work; it is a group of various activities to make the whole accounting process complete. It

starts with the collection and recording of financial transactions. Then all those transactions are

classified, summarized and recorded in various separate books of accounts respectively. At the

last processing all those information the final financial statement is prepared. The whole

accounting cycle can be defined in terms of certain key activity in accounting which includes,

Journal entry, Ledger posting, balancing, adjustments, closing entries and preparation of final

financial statement. In this report, all those processed have been described and illustrated with

practical example along with the analysis of the financial statement (Weil Schipper and Francis

2013).

Financial Statement:

Financial statement is the summarized form of all the accounting results of an

organization. It includes a statement of profit or loss or an income statement, which shows the

financial performance of an organization. It also includes a balance sheet or a statement of

financial position with a statement of changes in equity. For better reporting purpose, there must

be sufficient notes to the financial statement supporting the calculations made in financial

statement. Following is the extract of financial statements as illustrated in this report.

Income Statement

For the year ended 30 June

Sales Revenue $19,161.20

Service Revenue $1,810.00

Total Revenue $20,971.20

Cost of Goods Sold ($8,269.00)

Gross Profit $12,702.20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FUNDAMENTALS

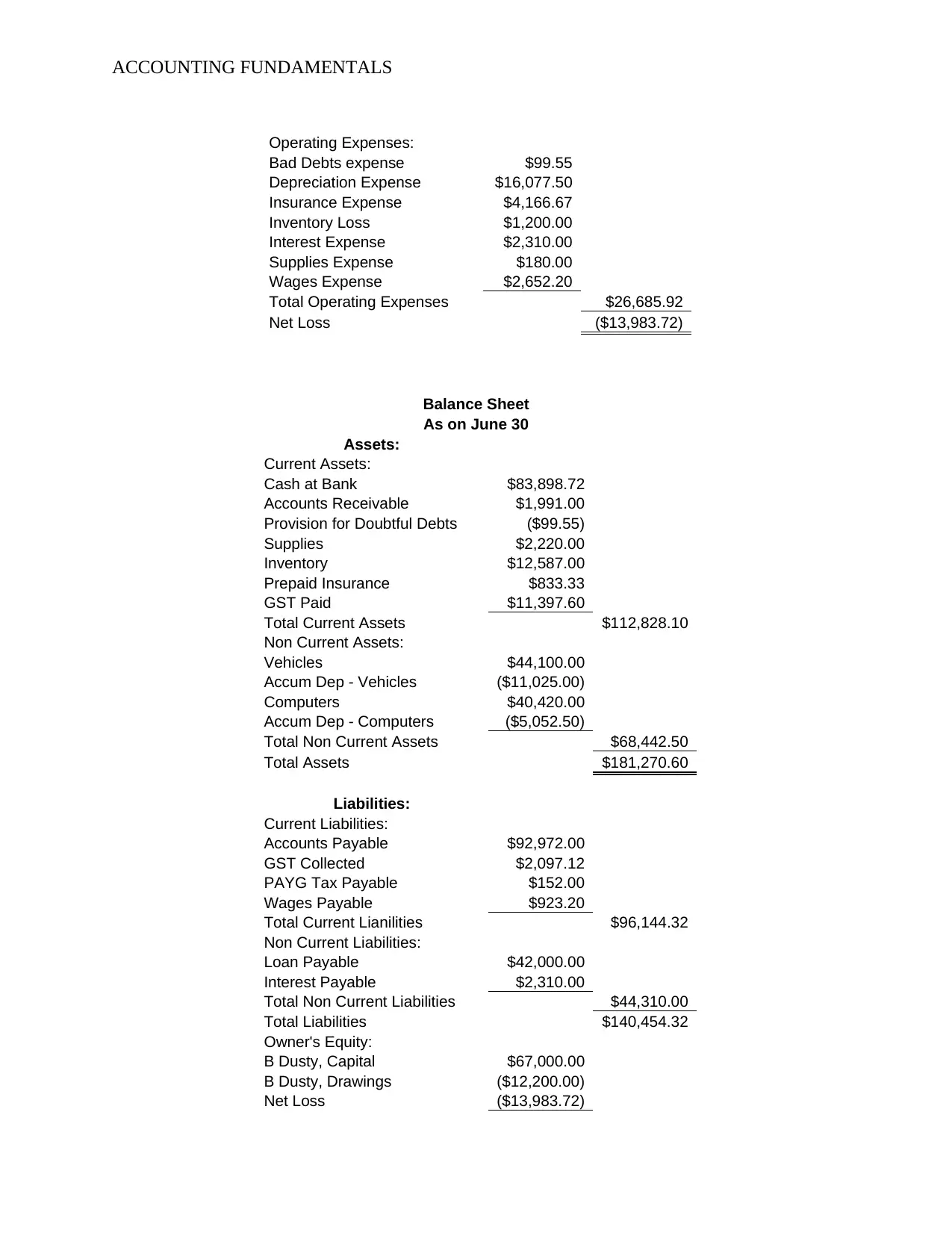

Operating Expenses:

Bad Debts expense $99.55

Depreciation Expense $16,077.50

Insurance Expense $4,166.67

Inventory Loss $1,200.00

Interest Expense $2,310.00

Supplies Expense $180.00

Wages Expense $2,652.20

Total Operating Expenses $26,685.92

Net Loss ($13,983.72)

Balance Sheet

As on June 30

Assets:

Current Assets:

Cash at Bank $83,898.72

Accounts Receivable $1,991.00

Provision for Doubtful Debts ($99.55)

Supplies $2,220.00

Inventory $12,587.00

Prepaid Insurance $833.33

GST Paid $11,397.60

Total Current Assets $112,828.10

Non Current Assets:

Vehicles $44,100.00

Accum Dep - Vehicles ($11,025.00)

Computers $40,420.00

Accum Dep - Computers ($5,052.50)

Total Non Current Assets $68,442.50

Total Assets $181,270.60

Liabilities:

Current Liabilities:

Accounts Payable $92,972.00

GST Collected $2,097.12

PAYG Tax Payable $152.00

Wages Payable $923.20

Total Current Lianilities $96,144.32

Non Current Liabilities:

Loan Payable $42,000.00

Interest Payable $2,310.00

Total Non Current Liabilities $44,310.00

Total Liabilities $140,454.32

Owner's Equity:

B Dusty, Capital $67,000.00

B Dusty, Drawings ($12,200.00)

Net Loss ($13,983.72)

Operating Expenses:

Bad Debts expense $99.55

Depreciation Expense $16,077.50

Insurance Expense $4,166.67

Inventory Loss $1,200.00

Interest Expense $2,310.00

Supplies Expense $180.00

Wages Expense $2,652.20

Total Operating Expenses $26,685.92

Net Loss ($13,983.72)

Balance Sheet

As on June 30

Assets:

Current Assets:

Cash at Bank $83,898.72

Accounts Receivable $1,991.00

Provision for Doubtful Debts ($99.55)

Supplies $2,220.00

Inventory $12,587.00

Prepaid Insurance $833.33

GST Paid $11,397.60

Total Current Assets $112,828.10

Non Current Assets:

Vehicles $44,100.00

Accum Dep - Vehicles ($11,025.00)

Computers $40,420.00

Accum Dep - Computers ($5,052.50)

Total Non Current Assets $68,442.50

Total Assets $181,270.60

Liabilities:

Current Liabilities:

Accounts Payable $92,972.00

GST Collected $2,097.12

PAYG Tax Payable $152.00

Wages Payable $923.20

Total Current Lianilities $96,144.32

Non Current Liabilities:

Loan Payable $42,000.00

Interest Payable $2,310.00

Total Non Current Liabilities $44,310.00

Total Liabilities $140,454.32

Owner's Equity:

B Dusty, Capital $67,000.00

B Dusty, Drawings ($12,200.00)

Net Loss ($13,983.72)

ACCOUNTING FUNDAMENTALS

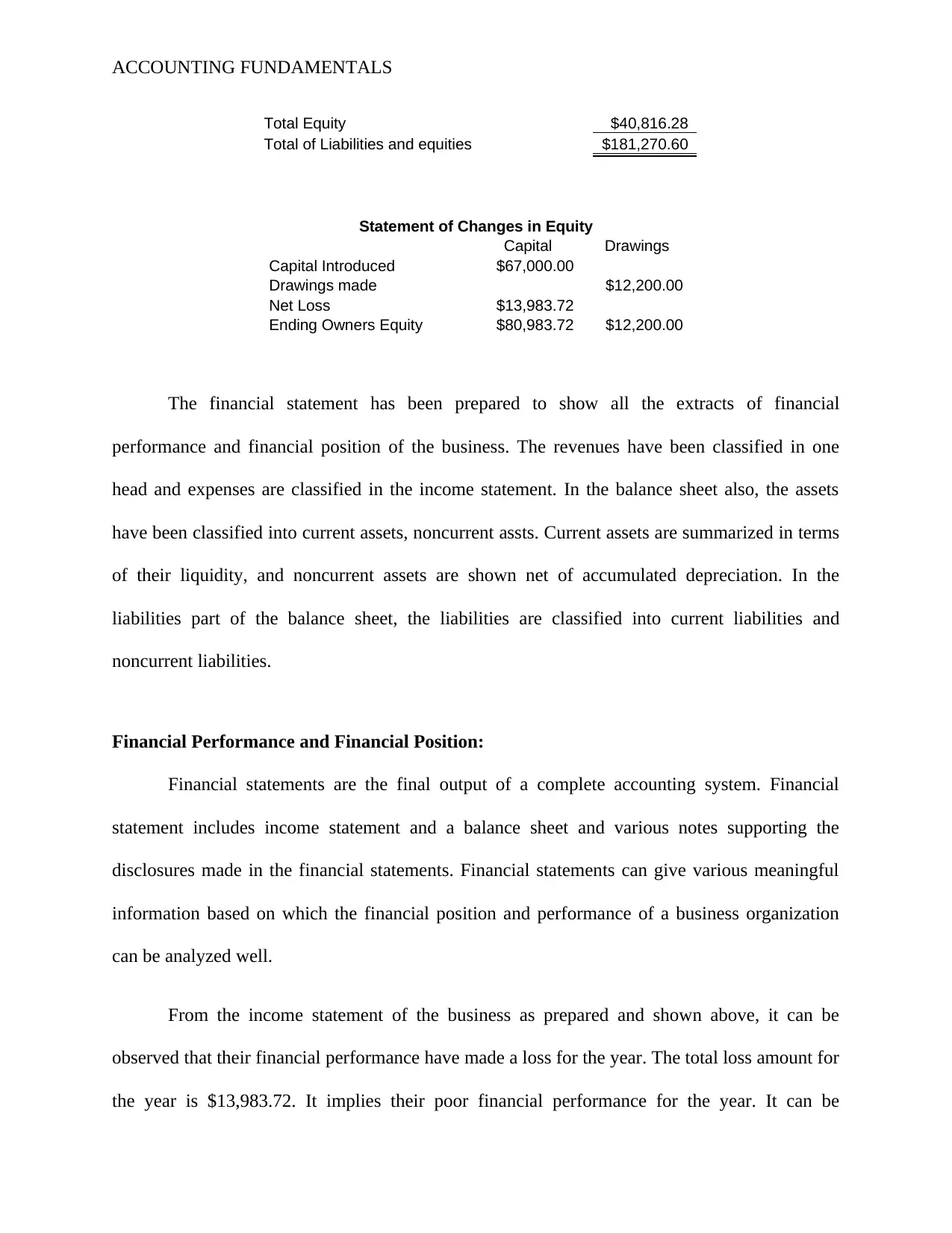

Total Equity $40,816.28

Total of Liabilities and equities $181,270.60

Statement of Changes in Equity

Capital Drawings

Capital Introduced $67,000.00

Drawings made $12,200.00

Net Loss $13,983.72

Ending Owners Equity $80,983.72 $12,200.00

The financial statement has been prepared to show all the extracts of financial

performance and financial position of the business. The revenues have been classified in one

head and expenses are classified in the income statement. In the balance sheet also, the assets

have been classified into current assets, noncurrent assts. Current assets are summarized in terms

of their liquidity, and noncurrent assets are shown net of accumulated depreciation. In the

liabilities part of the balance sheet, the liabilities are classified into current liabilities and

noncurrent liabilities.

Financial Performance and Financial Position:

Financial statements are the final output of a complete accounting system. Financial

statement includes income statement and a balance sheet and various notes supporting the

disclosures made in the financial statements. Financial statements can give various meaningful

information based on which the financial position and performance of a business organization

can be analyzed well.

From the income statement of the business as prepared and shown above, it can be

observed that their financial performance have made a loss for the year. The total loss amount for

the year is $13,983.72. It implies their poor financial performance for the year. It can be

Total Equity $40,816.28

Total of Liabilities and equities $181,270.60

Statement of Changes in Equity

Capital Drawings

Capital Introduced $67,000.00

Drawings made $12,200.00

Net Loss $13,983.72

Ending Owners Equity $80,983.72 $12,200.00

The financial statement has been prepared to show all the extracts of financial

performance and financial position of the business. The revenues have been classified in one

head and expenses are classified in the income statement. In the balance sheet also, the assets

have been classified into current assets, noncurrent assts. Current assets are summarized in terms

of their liquidity, and noncurrent assets are shown net of accumulated depreciation. In the

liabilities part of the balance sheet, the liabilities are classified into current liabilities and

noncurrent liabilities.

Financial Performance and Financial Position:

Financial statements are the final output of a complete accounting system. Financial

statement includes income statement and a balance sheet and various notes supporting the

disclosures made in the financial statements. Financial statements can give various meaningful

information based on which the financial position and performance of a business organization

can be analyzed well.

From the income statement of the business as prepared and shown above, it can be

observed that their financial performance have made a loss for the year. The total loss amount for

the year is $13,983.72. It implies their poor financial performance for the year. It can be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FUNDAMENTALS

observed from their income statement that, the main reason behind their huge loss is their huge

amount of operating expenses. The major part of their operating expenses includes the

depreciation expenses. It means they are using huge amount of fixed assets, but they are unable

to utilize those assets properly. Hence, their return on assets performance is very poor. The gross

profit margin of the business is significantly well, but they are having a net loss in their financial

statement. From their statement of financial position, it can be observed that, they are having a

huge amount of cash in their balance sheet. It implies they are having a high short term liquidity.

In terms of solvency also, it can be said that, they are having a enough solvency but not above

the standard benchmark. The current assets should have been double of the current liabilities, but

they are not having the same. In terms of long term solvency the company is having a fair

situation. Half of their fixed assets are financed by the long-term debt. A proper mix of debt and

equity might be giving the company an advantage of maximizing the wealth of the business. It

can be recommended for the company to maximize their sales and utilize the assets properly to

maximize their revenue and resulting profit from their operating business activities (May 2013).

Investment in assets and depreciation method:

The company is having a total carrying value of $68,442.50 as the carrying amount of

their total noncurrent assets. Now the organization is planning to invest more in the fixed assets.

It can be observed from their income statement and balance sheet, despite having a huge amount

of fixed assets, they could not utilized it properly, which resulted in a huge depreciation expense

and a net loss for the period. It can also be observed from their current accounting and

accounting systems, that they are following two methods for two types of fixed assets, they are

following straight-line depreciation method as well as a diminishing balance method of

depreciation. Diminishing method of charging depreciation is more superior to the straight-line

observed from their income statement that, the main reason behind their huge loss is their huge

amount of operating expenses. The major part of their operating expenses includes the

depreciation expenses. It means they are using huge amount of fixed assets, but they are unable

to utilize those assets properly. Hence, their return on assets performance is very poor. The gross

profit margin of the business is significantly well, but they are having a net loss in their financial

statement. From their statement of financial position, it can be observed that, they are having a

huge amount of cash in their balance sheet. It implies they are having a high short term liquidity.

In terms of solvency also, it can be said that, they are having a enough solvency but not above

the standard benchmark. The current assets should have been double of the current liabilities, but

they are not having the same. In terms of long term solvency the company is having a fair

situation. Half of their fixed assets are financed by the long-term debt. A proper mix of debt and

equity might be giving the company an advantage of maximizing the wealth of the business. It

can be recommended for the company to maximize their sales and utilize the assets properly to

maximize their revenue and resulting profit from their operating business activities (May 2013).

Investment in assets and depreciation method:

The company is having a total carrying value of $68,442.50 as the carrying amount of

their total noncurrent assets. Now the organization is planning to invest more in the fixed assets.

It can be observed from their income statement and balance sheet, despite having a huge amount

of fixed assets, they could not utilized it properly, which resulted in a huge depreciation expense

and a net loss for the period. It can also be observed from their current accounting and

accounting systems, that they are following two methods for two types of fixed assets, they are

following straight-line depreciation method as well as a diminishing balance method of

depreciation. Diminishing method of charging depreciation is more superior to the straight-line

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FUNDAMENTALS

method of depreciation. Therefore, it can be recommended for the company to use the

diminishing balance of depreciation method for their further investment in fixed assets (Warren

Reeve and Duchac 2013).

Inventory Control System:

As can be observed from their current accounting systems and policies, they are

following the weighted average method for inventory valuation. In this system of inventory

valuation the cost of goods sold and closing inventory is valued based on the weighted average

price of last available quantity of materials and respective total amount of materials. There are

many other methods of inventory valuation, such as FIFO method, LIFO method, Simple

Average method and specific items method (Beatty and Liao 2014). The specific items method

is more superior and logical but, it is very much complex in practice. Where a huge amount of

stock and numerous numbers of inventories are there, it cannot be successfully implemented. On

the other hand, FIFO and LIFO is the traditional method of inventory valuation, which have their

own advantages and disadvantages. Periodic inventory system is also there but it is very much

traditional and unscientific. Hence, it can be recommended for the company to follow their

existing system of inventory control and valuation. It will result in different valuation for the cost

of goods sold and ending inventory, which will result in different amount of net income or net

loss (Warren Reeve and Duchac 2013).

Internal Control Mechanism:

Internal control mechanism, includes various checkpoints and control system which

prevents from employee frauds and cash mismanagement. It also prevents from mistakes and

misstatement of financial information in the financial records and financial statement of an

method of depreciation. Therefore, it can be recommended for the company to use the

diminishing balance of depreciation method for their further investment in fixed assets (Warren

Reeve and Duchac 2013).

Inventory Control System:

As can be observed from their current accounting systems and policies, they are

following the weighted average method for inventory valuation. In this system of inventory

valuation the cost of goods sold and closing inventory is valued based on the weighted average

price of last available quantity of materials and respective total amount of materials. There are

many other methods of inventory valuation, such as FIFO method, LIFO method, Simple

Average method and specific items method (Beatty and Liao 2014). The specific items method

is more superior and logical but, it is very much complex in practice. Where a huge amount of

stock and numerous numbers of inventories are there, it cannot be successfully implemented. On

the other hand, FIFO and LIFO is the traditional method of inventory valuation, which have their

own advantages and disadvantages. Periodic inventory system is also there but it is very much

traditional and unscientific. Hence, it can be recommended for the company to follow their

existing system of inventory control and valuation. It will result in different valuation for the cost

of goods sold and ending inventory, which will result in different amount of net income or net

loss (Warren Reeve and Duchac 2013).

Internal Control Mechanism:

Internal control mechanism, includes various checkpoints and control system which

prevents from employee frauds and cash mismanagement. It also prevents from mistakes and

misstatement of financial information in the financial records and financial statement of an

ACCOUNTING FUNDAMENTALS

organization. Some of such internal control mechanisms are Bank Reconciliations periodically

and Cash Control mechanism. There must be the authority of the employees so distributed that

they can perform their duties within their authority. The recording, authorizing and processing of

various transaction including cash transactions must be done by more than one person, so that

their works are checked by others. Internal audit system also can help in controlling the financial

performance and position of the business (Beatty and Liao 2014).

Conclusion:

From the above discussion and analysis, it can be concluded that, the financial accounting

is a crucial and integrated part of the business organization. All the financial transactions and

data must be recorded in the books of accounts properly in accordance with the respective

accounting standards and guidelines. Lastly, it can be recommended for an organization to adopt

such accounting policies and principles, which best suits with their structure of business and their

operating activities.

organization. Some of such internal control mechanisms are Bank Reconciliations periodically

and Cash Control mechanism. There must be the authority of the employees so distributed that

they can perform their duties within their authority. The recording, authorizing and processing of

various transaction including cash transactions must be done by more than one person, so that

their works are checked by others. Internal audit system also can help in controlling the financial

performance and position of the business (Beatty and Liao 2014).

Conclusion:

From the above discussion and analysis, it can be concluded that, the financial accounting

is a crucial and integrated part of the business organization. All the financial transactions and

data must be recorded in the books of accounts properly in accordance with the respective

accounting standards and guidelines. Lastly, it can be recommended for an organization to adopt

such accounting policies and principles, which best suits with their structure of business and their

operating activities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FUNDAMENTALS

References and bibliography:

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Carraher, S. and Van Auken, H., 2013. The use of financial statements for decision making by

small firms. Journal of Small Business & Entrepreneurship, 26(3), pp.323-336.

Edwards, J.R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

May, G.O., 2013. Financial accounting. Read Books Ltd.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Financial and managerial accounting.

Nelson Education.

Warren, C., Reeve, J.M. and Duchac, J., 2013. Financial & managerial accounting. Cengage

Learning.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

References and bibliography:

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Carraher, S. and Van Auken, H., 2013. The use of financial statements for decision making by

small firms. Journal of Small Business & Entrepreneurship, 26(3), pp.323-336.

Edwards, J.R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

May, G.O., 2013. Financial accounting. Read Books Ltd.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Financial and managerial accounting.

Nelson Education.

Warren, C., Reeve, J.M. and Duchac, J., 2013. Financial & managerial accounting. Cengage

Learning.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.