Financial Analysis Report: Vacuum Cleaning Specialists - ACC106

VerifiedAdded on 2022/11/10

|9

|1593

|328

Report

AI Summary

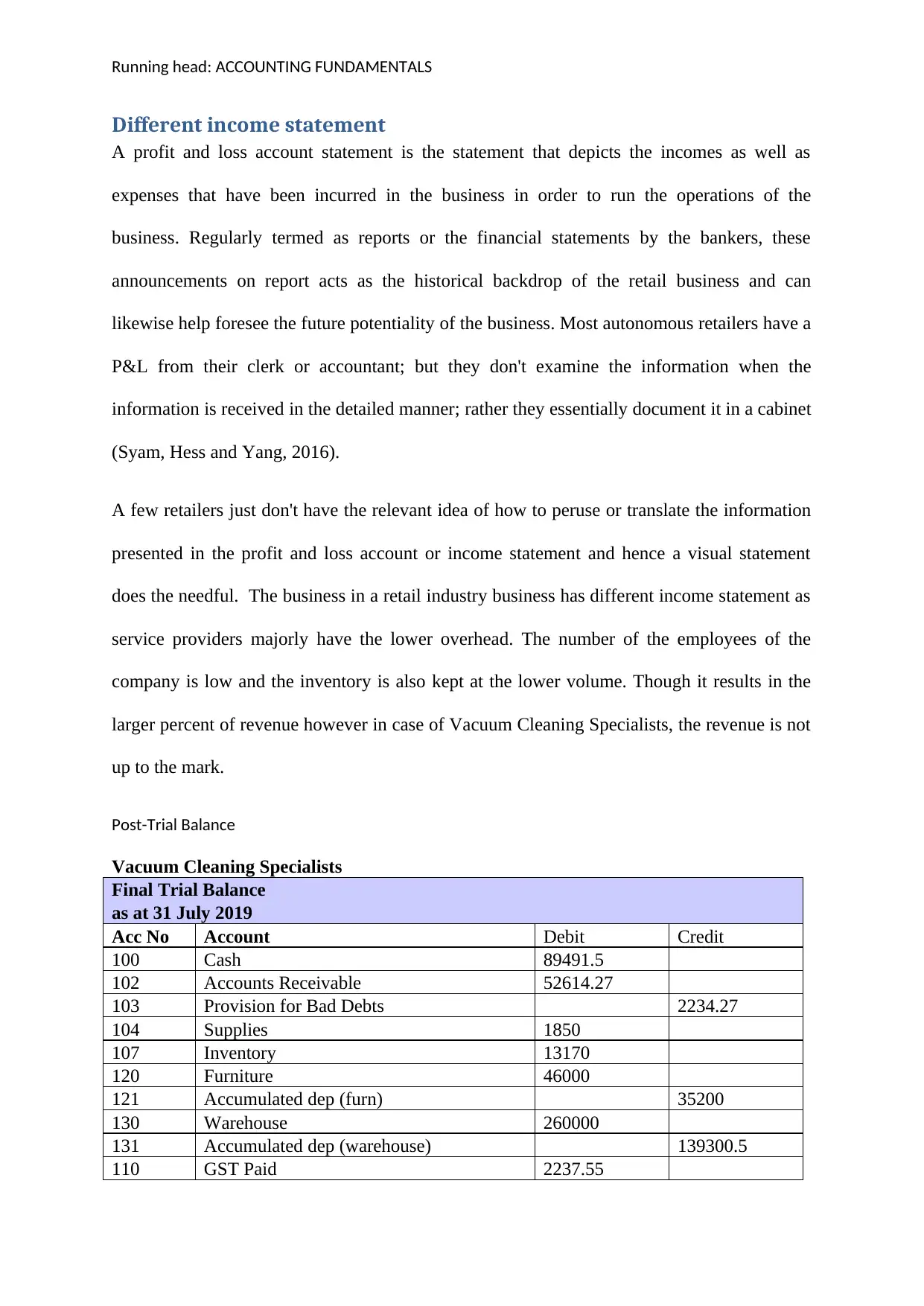

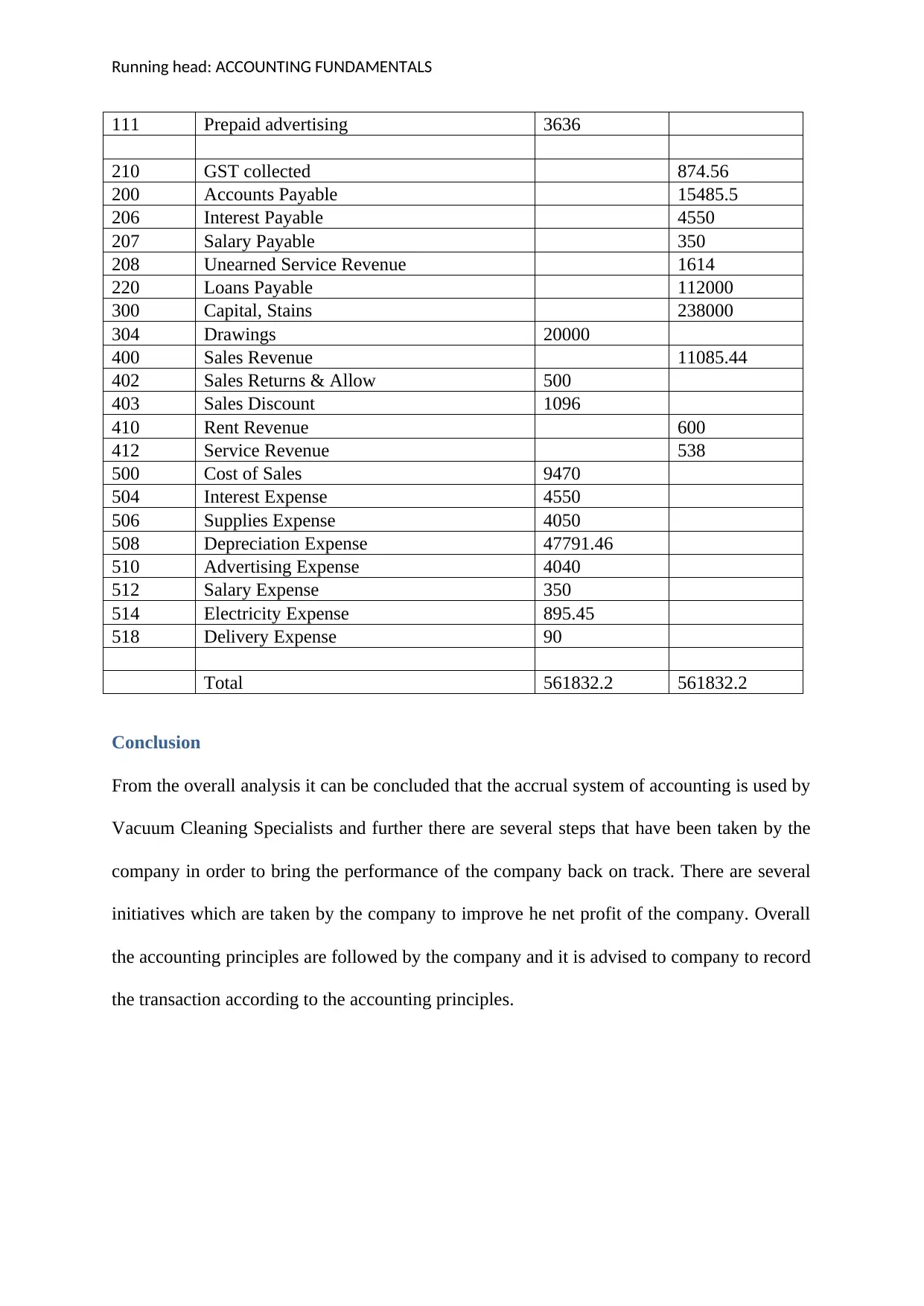

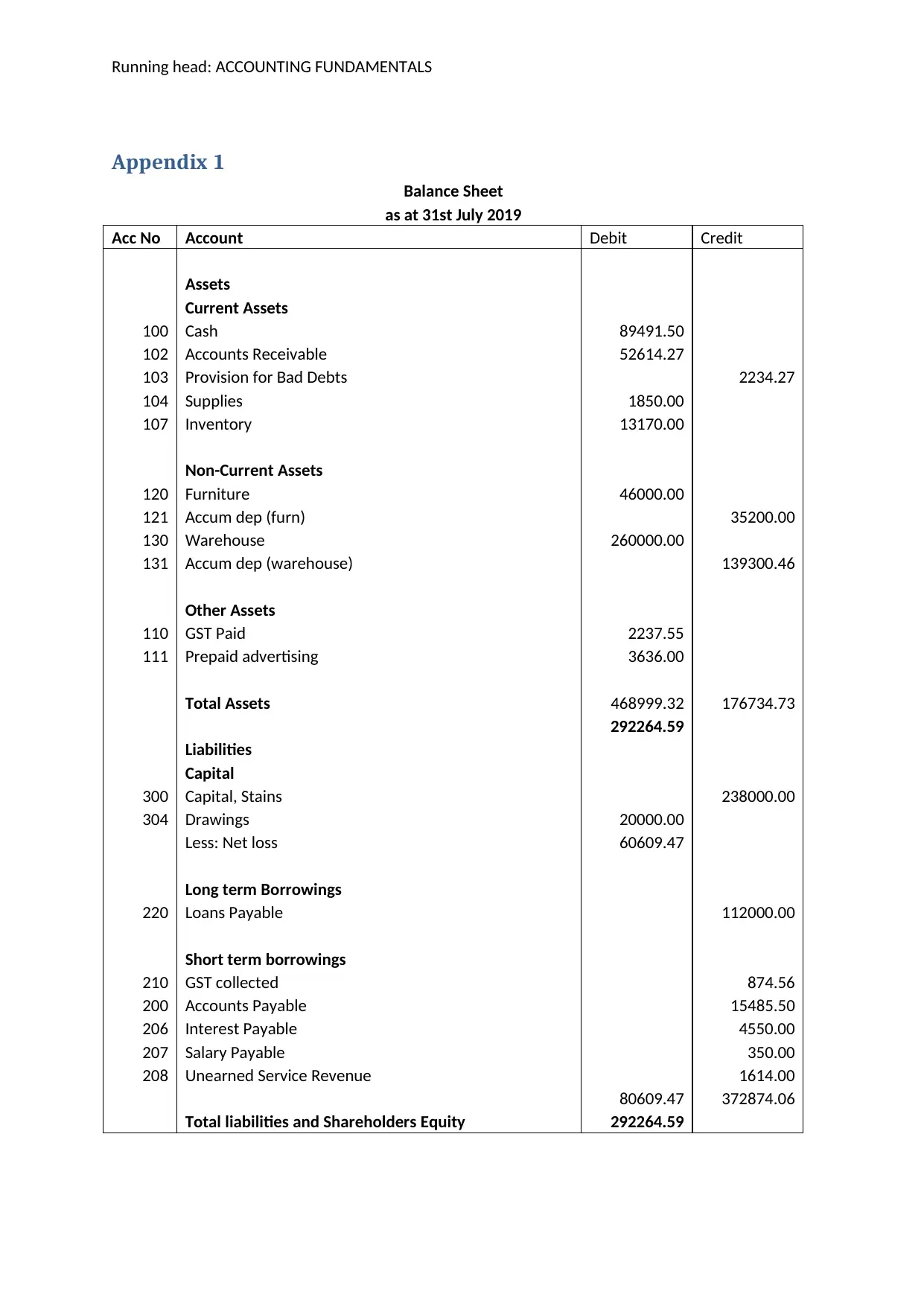

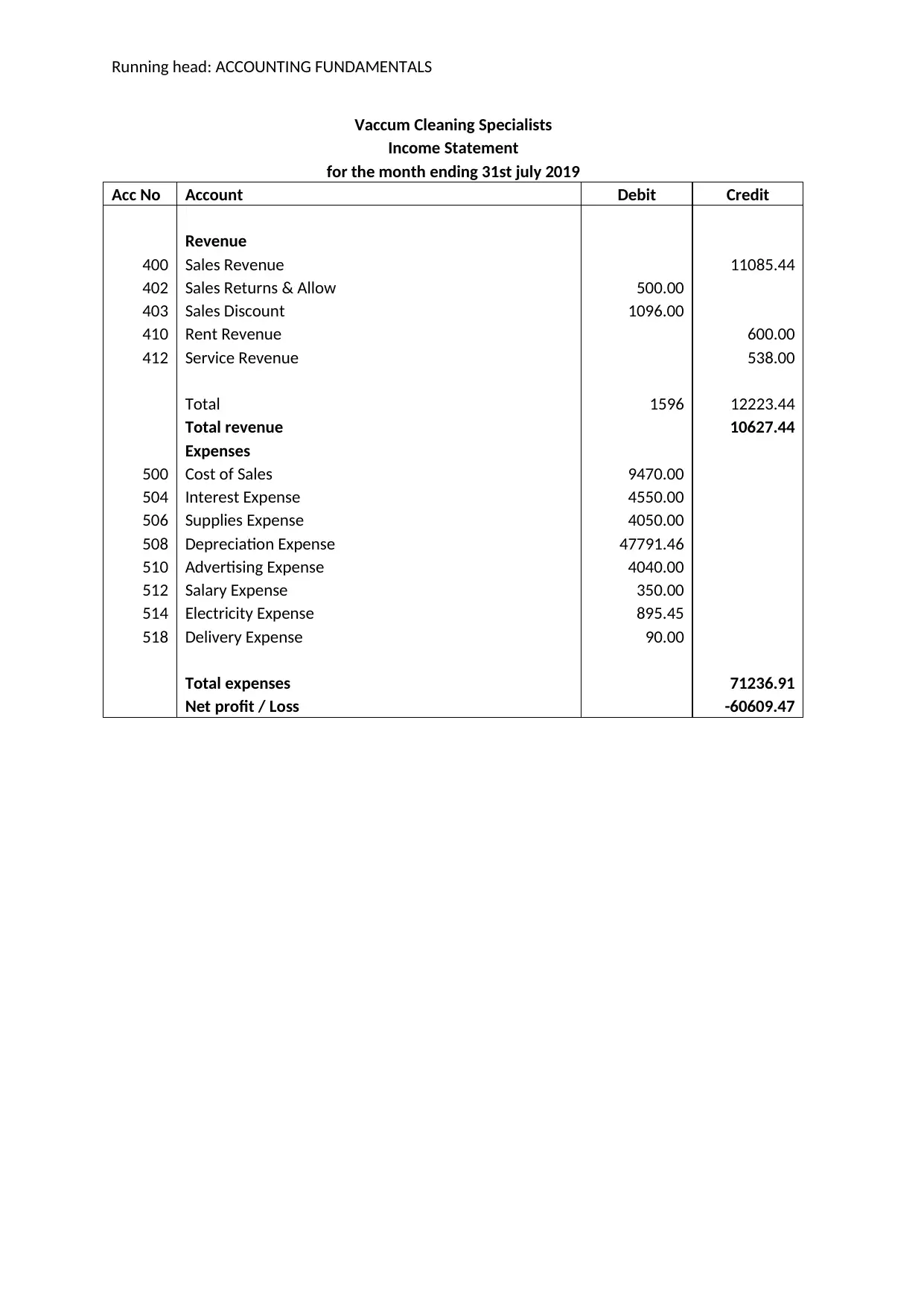

This report provides a comprehensive financial analysis of Vacuum Cleaning Specialists, examining its financial performance based on the provided trial balance and financial statements. The analysis includes an assessment of the company's profitability, highlighting a net loss and discussing strategies for improvement, such as cost reduction and pricing adjustments. The report delves into the accounting methods used, contrasting accrual and cash accounting, and explaining the treatment of prepaid expenses and bad debts. Furthermore, it presents and interprets the income statement and balance sheet, offering insights into the company's assets, liabilities, and equity. The conclusion summarizes key findings and recommends adherence to accounting principles for improved financial management. The report also includes a balance sheet and income statement for the period.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.