Company Accounting Report on Goodwill and Accounting Treatment

VerifiedAdded on 2023/03/23

|7

|655

|27

Report

AI Summary

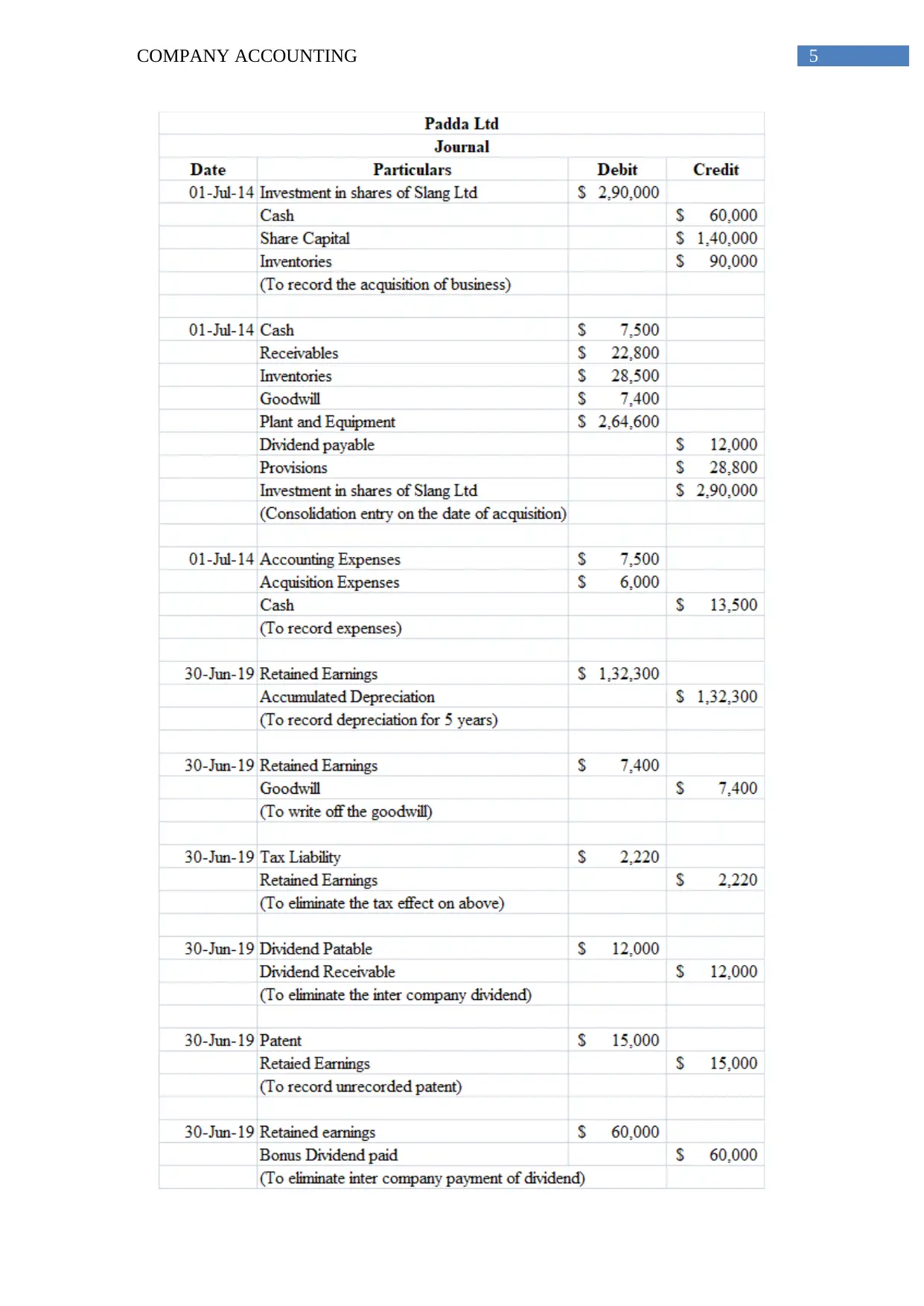

This report, prepared for ACCT20073, delves into the intricacies of company accounting, with a specific focus on goodwill. It begins with a memorandum discussing the nature of goodwill, differentiating between inherent and purchased goodwill, and outlining their respective accounting treatments. The report emphasizes that inherent goodwill, developed internally, is not recorded in the books, whereas purchased goodwill, arising from acquisitions, is recognized as an asset and subject to impairment testing. The report also includes a bibliography of relevant academic sources. The report provides a comprehensive understanding of goodwill accounting, offering clarity on its classification and financial reporting implications.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.