Accounting Report: Analyzing Business Structures and Governance

VerifiedAdded on 2020/06/03

|10

|2661

|240

Report

AI Summary

This accounting report delves into various business structures, commencing with an introduction to accounting's role in achieving sustainable advantages. It examines the suitability of sole proprietorship for new ventures, detailing its advantages like profit retention and low registration costs, alongside disadvantages such as limited funds and liability. The report then explores stakeholders, classifying them into internal and external groups like customers, government, investors, and creditors, emphasizing the importance of transparency and corporate responsibility. A memorandum addresses key issues arising from strikes and environmental concerns, proposing solutions involving management accounting tools and compliance with environmental laws. Part B analyzes partnership factors, joint liability, and partner liabilities, differentiating between public and proprietary companies, and discussing the concept of a separate legal entity. The report offers a comprehensive overview of accounting concepts, business structures, and corporate governance.

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Question 1...................................................................................................................................3

Question 2...................................................................................................................................4

Question 3...................................................................................................................................1

PART B............................................................................................................................................3

SET 1...........................................................................................................................................3

SET 2...........................................................................................................................................4

SET 3...........................................................................................................................................4

PART C............................................................................................................................................5

Covered in PPT...........................................................................................................................5

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Question 1...................................................................................................................................3

Question 2...................................................................................................................................4

Question 3...................................................................................................................................1

PART B............................................................................................................................................3

SET 1...........................................................................................................................................3

SET 2...........................................................................................................................................4

SET 3...........................................................................................................................................4

PART C............................................................................................................................................5

Covered in PPT...........................................................................................................................5

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION

Accounting is the main thing which is used in the business for getting sustainable

advantages over the firms. Now, each company is trying to achieve its sustainable development

with the help of effective application of accounting standard within the business objectives

(Bushman, Piotroski and Smith, 2004). Under the given case, parent client wants to includes its

family members in any structure. With the help of this, they would able to form an entity so that

the intended entity could attain optimum benefits, and this can only be achieved after having vast

investigations of each structure advantages and disadvantages. Under this, the company is able to

make their business objectives viable.

PART A

Question 1

1.

In order to start a new business the best option is of the sole trading. It is one of the most

suitable technique as it incorporation of this is easy easy and can be started with less of

formalities. There is a single person who owns the business and is liable for all the decision

taking. There are different advantages and disadvantages of this concept which needs to be

considered while selecting it as a choice of business:

Advantages

Keeps all the profit – the best positive factor about this concept is that the total earning

remains with the sole proprietor which increases the chances of higher growth to the

entrepreneur. All the benefits are enjoyed alone by the sole trader which motivates an

individual to perform well (Ittner and Larcker, 2001).

Low registration cost – As less formalities are required for incorporation the cost of

registration is very low which makes it a preferred option for staring a new business type.

Low regulation – When a business is run as a sole proprietorship very few regulations

need to be follow. This is because it generally operates on a comparatively lower scale

which makes it less risky.

Much money can be saved – Under the system of sole proprietorship less formalities

need to be done like low filing work and much maintenance of records is also not

required which reduces the total cost of mainatince for the company.

Accounting is the main thing which is used in the business for getting sustainable

advantages over the firms. Now, each company is trying to achieve its sustainable development

with the help of effective application of accounting standard within the business objectives

(Bushman, Piotroski and Smith, 2004). Under the given case, parent client wants to includes its

family members in any structure. With the help of this, they would able to form an entity so that

the intended entity could attain optimum benefits, and this can only be achieved after having vast

investigations of each structure advantages and disadvantages. Under this, the company is able to

make their business objectives viable.

PART A

Question 1

1.

In order to start a new business the best option is of the sole trading. It is one of the most

suitable technique as it incorporation of this is easy easy and can be started with less of

formalities. There is a single person who owns the business and is liable for all the decision

taking. There are different advantages and disadvantages of this concept which needs to be

considered while selecting it as a choice of business:

Advantages

Keeps all the profit – the best positive factor about this concept is that the total earning

remains with the sole proprietor which increases the chances of higher growth to the

entrepreneur. All the benefits are enjoyed alone by the sole trader which motivates an

individual to perform well (Ittner and Larcker, 2001).

Low registration cost – As less formalities are required for incorporation the cost of

registration is very low which makes it a preferred option for staring a new business type.

Low regulation – When a business is run as a sole proprietorship very few regulations

need to be follow. This is because it generally operates on a comparatively lower scale

which makes it less risky.

Much money can be saved – Under the system of sole proprietorship less formalities

need to be done like low filing work and much maintenance of records is also not

required which reduces the total cost of mainatince for the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Easy to commence and wind up – As less formalities are required at the time of

commencing the business entity hence makes it an easy option comparatively. Apart from

this even at the time of winding up no complexity is faced as business can be shut down

at point of time whenever the sole trader wish to. This is due to the reason that business

does not have any liability against anyone except the trader (Solomon, 2007).

Disadvantages

Less availability of funds – as the money is invested by a single person the total amount

available is very less due to which the investor face the difficulty of adequate funds.

Unlimited liability – In case of sole proprietorship all the risk is shared alone by an

individual. In case of insolvency all the amount is paid by a single person and no pressure

is shared by other person.

Lower scope of development – Due to non availability of adequate resources the speed

of development is less. On the other hand business entities which are running has joint

venture has greater growth opportunities due to having excessive availability of resources

(Bhattacharya, Daouk and Welker, 2003).

Question 2

1. Stakeholders are those which has direct or indirect interest in a particular organisation.

They invest in an enterprise and hence it becomes necessary to keep them updated with whatever

things that are taking place. It is the corporate responsibility of any organisation to keep all its

stakeholder well informed so that accordingly they can take their future decisions. In case if any

quantity information is hidden by an enterprise for personal benefit than the a legal action can be

taken against the same by the different interested parties (Larcker, Richardson and Tuna, 2007).

They on the basis of their availability and role can be divided into internal and external. Some of

the major stakeholders are:

▪ Customers – These are one of the most important stakeholder for any company.

In order to take the buying decision it is necessary that they are well informed and

no quality information is kept secret which can influence the buying decision. If

found that the customer is not given the right data than he can take a legal action

against the enterprise.

▪ Government – It is one of the external stakeholder which does not have any

direct interest in the operations of the company but in order to maintain discipline

commencing the business entity hence makes it an easy option comparatively. Apart from

this even at the time of winding up no complexity is faced as business can be shut down

at point of time whenever the sole trader wish to. This is due to the reason that business

does not have any liability against anyone except the trader (Solomon, 2007).

Disadvantages

Less availability of funds – as the money is invested by a single person the total amount

available is very less due to which the investor face the difficulty of adequate funds.

Unlimited liability – In case of sole proprietorship all the risk is shared alone by an

individual. In case of insolvency all the amount is paid by a single person and no pressure

is shared by other person.

Lower scope of development – Due to non availability of adequate resources the speed

of development is less. On the other hand business entities which are running has joint

venture has greater growth opportunities due to having excessive availability of resources

(Bhattacharya, Daouk and Welker, 2003).

Question 2

1. Stakeholders are those which has direct or indirect interest in a particular organisation.

They invest in an enterprise and hence it becomes necessary to keep them updated with whatever

things that are taking place. It is the corporate responsibility of any organisation to keep all its

stakeholder well informed so that accordingly they can take their future decisions. In case if any

quantity information is hidden by an enterprise for personal benefit than the a legal action can be

taken against the same by the different interested parties (Larcker, Richardson and Tuna, 2007).

They on the basis of their availability and role can be divided into internal and external. Some of

the major stakeholders are:

▪ Customers – These are one of the most important stakeholder for any company.

In order to take the buying decision it is necessary that they are well informed and

no quality information is kept secret which can influence the buying decision. If

found that the customer is not given the right data than he can take a legal action

against the enterprise.

▪ Government – It is one of the external stakeholder which does not have any

direct interest in the operations of the company but in order to maintain discipline

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and proper working government keeps on checking that weather each unit is

operating effectively or not (Hope, 2003). It is necessary that every organisation

full fills all its social responsibility for which company needs to give the

knowledge of its work to the present legal authority in order to remain free from

any legal action.

▪ Investors – These are those parties which do investment in the company. Hence it

is very important that they are given complete knowledge so that accordingly they

can decide weather to continue investment or not. After going through the

financial data provided by the organisation an individual decides that weather he

will invest in that firm or not (Ajinkya, Bhojraj and Sengupta, 2005).

▪ Creditors – It consist of that party which owe money to the company. Hence it is

necessary that they are provided with all the required data so that they get the

assurance regarding the performance of company.

▪ Suppliers – It is that section of an institution from where goods are received to

carry out the operations. They need to be keep informed so that they can

accordingly maintain long term relation with the company.

2.

In order to achieve the goals and objectives it is necessary that the duties of director are

raised to a good level. The management should ensure that corporate social responsibility are

fulfilled as only than profitability can be achieved. According to case study of James Hardie

experience:

Management must know how to perform their duties rather than just doing what they are

asked to do (Fan and Wong, 2005).

It is the responsibility of management to test the decision so that it can be assured that

what is being expected out of them.

Question 3

operating effectively or not (Hope, 2003). It is necessary that every organisation

full fills all its social responsibility for which company needs to give the

knowledge of its work to the present legal authority in order to remain free from

any legal action.

▪ Investors – These are those parties which do investment in the company. Hence it

is very important that they are given complete knowledge so that accordingly they

can decide weather to continue investment or not. After going through the

financial data provided by the organisation an individual decides that weather he

will invest in that firm or not (Ajinkya, Bhojraj and Sengupta, 2005).

▪ Creditors – It consist of that party which owe money to the company. Hence it is

necessary that they are provided with all the required data so that they get the

assurance regarding the performance of company.

▪ Suppliers – It is that section of an institution from where goods are received to

carry out the operations. They need to be keep informed so that they can

accordingly maintain long term relation with the company.

2.

In order to achieve the goals and objectives it is necessary that the duties of director are

raised to a good level. The management should ensure that corporate social responsibility are

fulfilled as only than profitability can be achieved. According to case study of James Hardie

experience:

Management must know how to perform their duties rather than just doing what they are

asked to do (Fan and Wong, 2005).

It is the responsibility of management to test the decision so that it can be assured that

what is being expected out of them.

Question 3

MEMORANDUM25th September, 2017

To: Board of Directors

From: Compliance officer

Subject: For addressing the key issues occurred due to strike and environmental issues.

I know and respect few decisions regarding corporate governance issues which are going to

cover under this.

Problems

Under mine 1, the issues arises due to strike have been identified and also implementing some

factors which are striving hard to eliminate these issues.

Under mine 2, various environmental issues have been identified and there is a need to

overcome these issues by complying environmental laws.

Solutions

Under mine 1, the company considers various management accounting tools which are

used in order to attain various compliance requirements and this will help out the firm to attain

various corporate governance tools that are attained. Due to strike, unemployment occurred,

which are overcome by way of effective compliance of corporate governance.

Under mine 2, productive life of the mine is finished due to exhaustion of minerals. The

company also need to make effective compliance of environmental laws so that corporate social

responsibilities. The compliance officer needs to opts all the compliance regulations in order to

attain compliance regulations.

There are different ways through which the monitoring can be done like the most important

thing is to recognise that good governance is not just about compliance, it needs to be balanced

with legislation. Than the value of boards need to be clarified and effective monitoring over the

performance of the company is most crucial. Management needs to realise that to govern the

risk is the prime responsibility of board for which all the required information should be well

communicated to the concern directors. Apart from this building an effective governance

infrastructure can also be of great help which has a competent chairperson.

Organisation must have a set criteria in order to control its internal operations so that failure

can be minimised. For this company can set a code of conduct which will be ensured while

performing the various operations. This code will include al the description of different projects

To: Board of Directors

From: Compliance officer

Subject: For addressing the key issues occurred due to strike and environmental issues.

I know and respect few decisions regarding corporate governance issues which are going to

cover under this.

Problems

Under mine 1, the issues arises due to strike have been identified and also implementing some

factors which are striving hard to eliminate these issues.

Under mine 2, various environmental issues have been identified and there is a need to

overcome these issues by complying environmental laws.

Solutions

Under mine 1, the company considers various management accounting tools which are

used in order to attain various compliance requirements and this will help out the firm to attain

various corporate governance tools that are attained. Due to strike, unemployment occurred,

which are overcome by way of effective compliance of corporate governance.

Under mine 2, productive life of the mine is finished due to exhaustion of minerals. The

company also need to make effective compliance of environmental laws so that corporate social

responsibilities. The compliance officer needs to opts all the compliance regulations in order to

attain compliance regulations.

There are different ways through which the monitoring can be done like the most important

thing is to recognise that good governance is not just about compliance, it needs to be balanced

with legislation. Than the value of boards need to be clarified and effective monitoring over the

performance of the company is most crucial. Management needs to realise that to govern the

risk is the prime responsibility of board for which all the required information should be well

communicated to the concern directors. Apart from this building an effective governance

infrastructure can also be of great help which has a competent chairperson.

Organisation must have a set criteria in order to control its internal operations so that failure

can be minimised. For this company can set a code of conduct which will be ensured while

performing the various operations. This code will include al the description of different projects

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which can provide a general guideline to all the employees. It should also provide a clear

channel to worker as to whom they have to report so that accountability can be set.

PART B

SET 1

1.

The different factors that can help in determining weather partnership exists or not are the

availability of partnership registration formal, than the contribution of each part in monitory or

non monitory terms.

2.

Joint liability is the situation in which two or more person agree on same thing to the

third party. In this case both the parties involved in the contract has equal obligation to complete

the promise. It is different from that of joint and several liability as in this case the loss can be

recovered from one of those partners also which further helps the injured person to recover.

3.

A partner can avoid his future liability by disclosing all the related facts at the time of

retirement and paying off all the liabilities which are present against him.

4.

Agency is an important concept in partnership as an agreement created by any agency can

be expressed and implied. Also the agent is accountable if any law is not maintained while

framing the partnership. This way the partner also gets direction as how they will be performing

their duties which makes them responsible in case if any law is violated (Biddle, Hilary and

Verdi, 2009).

5.

Limited partnership is the concept in which the different individuals come together and

form partnership in a unique manner. The liability of each individual under this situation is

limited to the extent they have invested in a particular business. It is suitable for that kind of

channel to worker as to whom they have to report so that accountability can be set.

PART B

SET 1

1.

The different factors that can help in determining weather partnership exists or not are the

availability of partnership registration formal, than the contribution of each part in monitory or

non monitory terms.

2.

Joint liability is the situation in which two or more person agree on same thing to the

third party. In this case both the parties involved in the contract has equal obligation to complete

the promise. It is different from that of joint and several liability as in this case the loss can be

recovered from one of those partners also which further helps the injured person to recover.

3.

A partner can avoid his future liability by disclosing all the related facts at the time of

retirement and paying off all the liabilities which are present against him.

4.

Agency is an important concept in partnership as an agreement created by any agency can

be expressed and implied. Also the agent is accountable if any law is not maintained while

framing the partnership. This way the partner also gets direction as how they will be performing

their duties which makes them responsible in case if any law is violated (Biddle, Hilary and

Verdi, 2009).

5.

Limited partnership is the concept in which the different individuals come together and

form partnership in a unique manner. The liability of each individual under this situation is

limited to the extent they have invested in a particular business. It is suitable for that kind of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

individuals who do not want to take excessive risk and wants to do business with maximum

security.

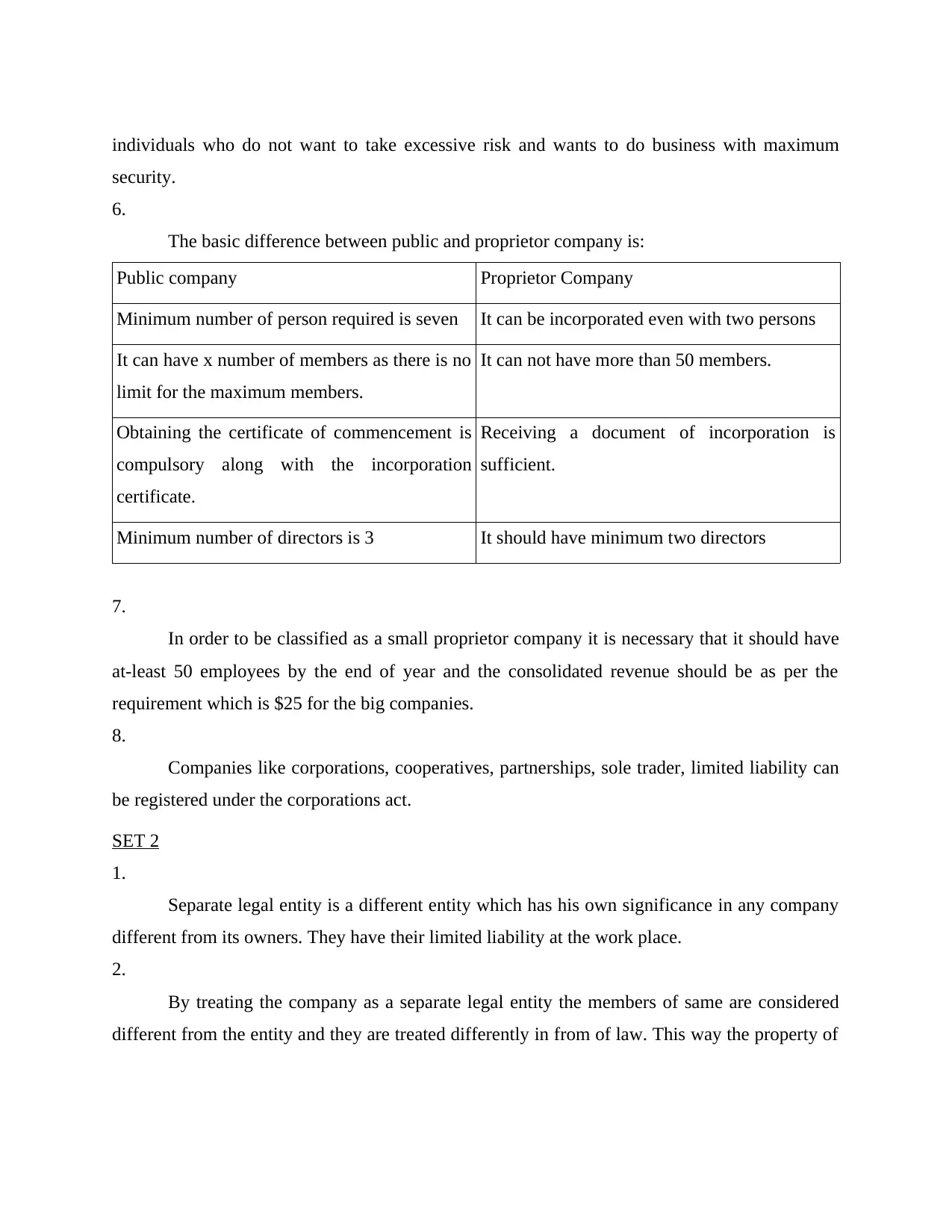

6.

The basic difference between public and proprietor company is:

Public company Proprietor Company

Minimum number of person required is seven It can be incorporated even with two persons

It can have x number of members as there is no

limit for the maximum members.

It can not have more than 50 members.

Obtaining the certificate of commencement is

compulsory along with the incorporation

certificate.

Receiving a document of incorporation is

sufficient.

Minimum number of directors is 3 It should have minimum two directors

7.

In order to be classified as a small proprietor company it is necessary that it should have

at-least 50 employees by the end of year and the consolidated revenue should be as per the

requirement which is $25 for the big companies.

8.

Companies like corporations, cooperatives, partnerships, sole trader, limited liability can

be registered under the corporations act.

SET 2

1.

Separate legal entity is a different entity which has his own significance in any company

different from its owners. They have their limited liability at the work place.

2.

By treating the company as a separate legal entity the members of same are considered

different from the entity and they are treated differently in from of law. This way the property of

security.

6.

The basic difference between public and proprietor company is:

Public company Proprietor Company

Minimum number of person required is seven It can be incorporated even with two persons

It can have x number of members as there is no

limit for the maximum members.

It can not have more than 50 members.

Obtaining the certificate of commencement is

compulsory along with the incorporation

certificate.

Receiving a document of incorporation is

sufficient.

Minimum number of directors is 3 It should have minimum two directors

7.

In order to be classified as a small proprietor company it is necessary that it should have

at-least 50 employees by the end of year and the consolidated revenue should be as per the

requirement which is $25 for the big companies.

8.

Companies like corporations, cooperatives, partnerships, sole trader, limited liability can

be registered under the corporations act.

SET 2

1.

Separate legal entity is a different entity which has his own significance in any company

different from its owners. They have their limited liability at the work place.

2.

By treating the company as a separate legal entity the members of same are considered

different from the entity and they are treated differently in from of law. This way the property of

the company is not considered of its members and operations can be done on the name of

organisation (Ali, Chen and Radhakrishnan, 2007).

3.

Under the case of fraud, group enterprise, agency, trust, tort, tax courts have to pierced

the corporate veil.

SET 3

1.

Company itself can enforce a breach of directors fiduciary duties.

2.

Different remedies present under the companies civil breach of common law duties are

disqualification order, competition order and pecuniary penalty.

3.

ASIC enforces a breach of directors duties under the corporation act.

4.

Yes directors can be criminally liable under the corporations act.

PART C

Covered in PPT

CONCLUSION

From above report it can be summarised that there are different options with which a

business can be incorporated and each has their own advantages and disadvantages. Later

memorandum of association is prepared which shows it is necessary to follow the basic guideline

for preparing an effective document. Thereafter, answers to different questions are given related

to the laws that are present in Australia for proprietorship.

organisation (Ali, Chen and Radhakrishnan, 2007).

3.

Under the case of fraud, group enterprise, agency, trust, tort, tax courts have to pierced

the corporate veil.

SET 3

1.

Company itself can enforce a breach of directors fiduciary duties.

2.

Different remedies present under the companies civil breach of common law duties are

disqualification order, competition order and pecuniary penalty.

3.

ASIC enforces a breach of directors duties under the corporation act.

4.

Yes directors can be criminally liable under the corporations act.

PART C

Covered in PPT

CONCLUSION

From above report it can be summarised that there are different options with which a

business can be incorporated and each has their own advantages and disadvantages. Later

memorandum of association is prepared which shows it is necessary to follow the basic guideline

for preparing an effective document. Thereafter, answers to different questions are given related

to the laws that are present in Australia for proprietorship.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Bushman, R.M., Piotroski, J.D. and Smith, A.J., 2004. What determines corporate transparency?.

Journal of accounting research.42(2). pp.207-252.

Ittner, C.D. and Larcker, D.F., 2001. Assessing empirical research in managerial accounting: a

value-based management perspective. Journal of accounting and economics.32(1).

pp.349-410.

Solomon, J., 2007. Corporate governance and accountability. John Wiley & Sons.

Bhattacharya, U., Daouk, H. and Welker, M., 2003. The world price of earnings opacity. The

Accounting Review .78(3). pp.641-678.

Larcker, D.F., Richardson, S.A. and Tuna, I., 2007. Corporate governance, accounting outcomes,

and organizational performance. The Accounting Review.82(4). pp.963-1008.

Hope, O.K., 2003. Disclosure practices, enforcement of accounting standards, and analysts'

forecast accuracy: An international study. Journal of accounting research.41(2).

pp.235-272.

Ajinkya, B., Bhojraj, S. and Sengupta, P., 2005. The association between outside directors,

institutional investors and the properties of management earnings forecasts. Journal of

accounting Research.43(3). pp.343-376.

Fan, J.P. and Wong, T.J., 2005. Do external auditors perform a corporate governance role in

emerging markets? Evidence from East Asia. Journal of accounting research.43(1).

pp.35-72.

Biddle, G.C., Hilary, G. and Verdi, R.S., 2009. How does financial reporting quality relate to

investment efficiency?. Journal of accounting and economics.48(2). pp.112-131.

Ali, A., Chen, T.Y. and Radhakrishnan, S., 2007. Corporate disclosures by family firms. Journal

of accounting and economics.44(1). pp.238-286.

Books and Journals

Bushman, R.M., Piotroski, J.D. and Smith, A.J., 2004. What determines corporate transparency?.

Journal of accounting research.42(2). pp.207-252.

Ittner, C.D. and Larcker, D.F., 2001. Assessing empirical research in managerial accounting: a

value-based management perspective. Journal of accounting and economics.32(1).

pp.349-410.

Solomon, J., 2007. Corporate governance and accountability. John Wiley & Sons.

Bhattacharya, U., Daouk, H. and Welker, M., 2003. The world price of earnings opacity. The

Accounting Review .78(3). pp.641-678.

Larcker, D.F., Richardson, S.A. and Tuna, I., 2007. Corporate governance, accounting outcomes,

and organizational performance. The Accounting Review.82(4). pp.963-1008.

Hope, O.K., 2003. Disclosure practices, enforcement of accounting standards, and analysts'

forecast accuracy: An international study. Journal of accounting research.41(2).

pp.235-272.

Ajinkya, B., Bhojraj, S. and Sengupta, P., 2005. The association between outside directors,

institutional investors and the properties of management earnings forecasts. Journal of

accounting Research.43(3). pp.343-376.

Fan, J.P. and Wong, T.J., 2005. Do external auditors perform a corporate governance role in

emerging markets? Evidence from East Asia. Journal of accounting research.43(1).

pp.35-72.

Biddle, G.C., Hilary, G. and Verdi, R.S., 2009. How does financial reporting quality relate to

investment efficiency?. Journal of accounting and economics.48(2). pp.112-131.

Ali, A., Chen, T.Y. and Radhakrishnan, S., 2007. Corporate disclosures by family firms. Journal

of accounting and economics.44(1). pp.238-286.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.