Accounting Analysis: Hedge Instruments, GAAP/IFRS Comparison

VerifiedAdded on 2022/08/11

|11

|632

|24

Homework Assignment

AI Summary

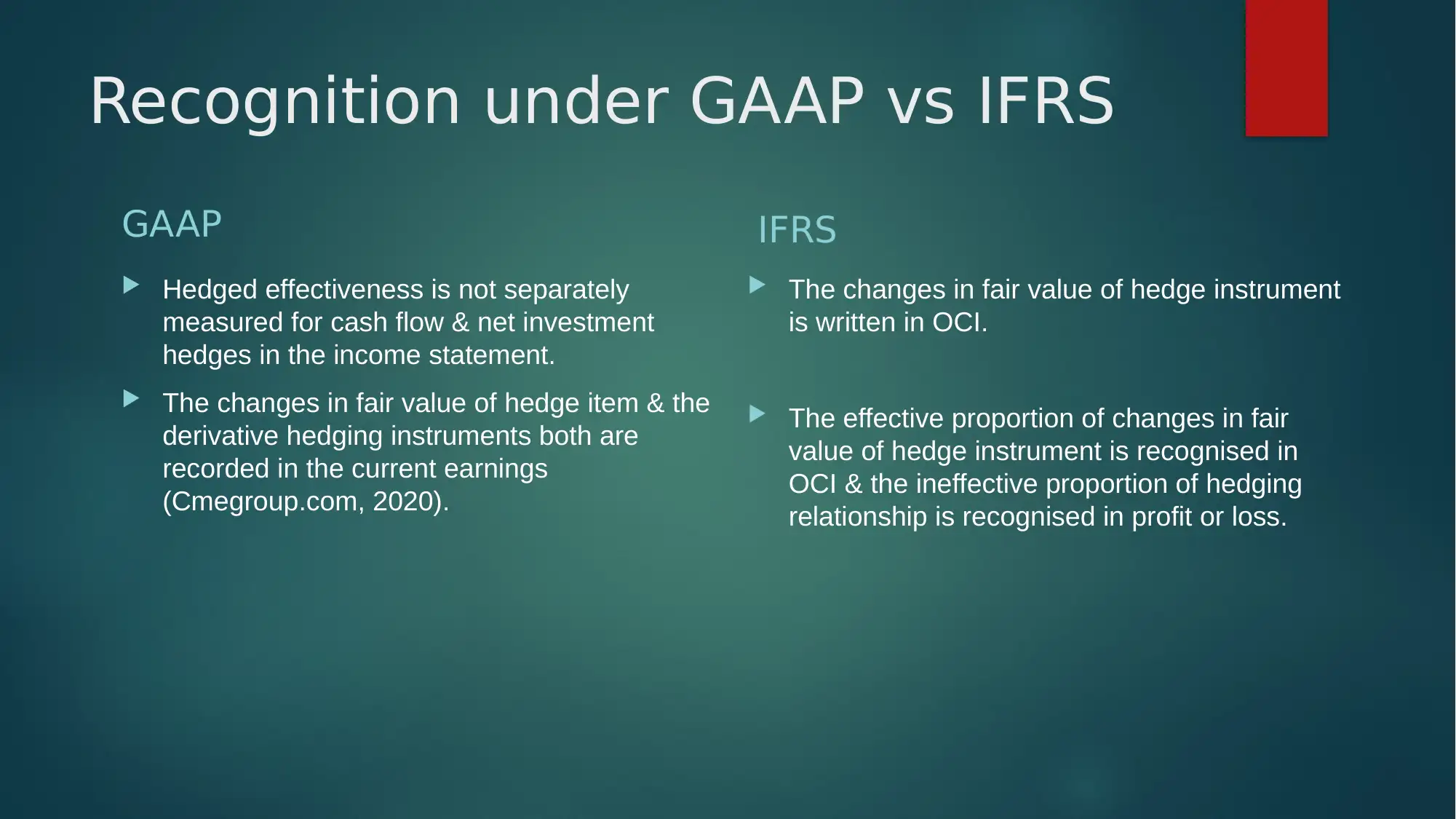

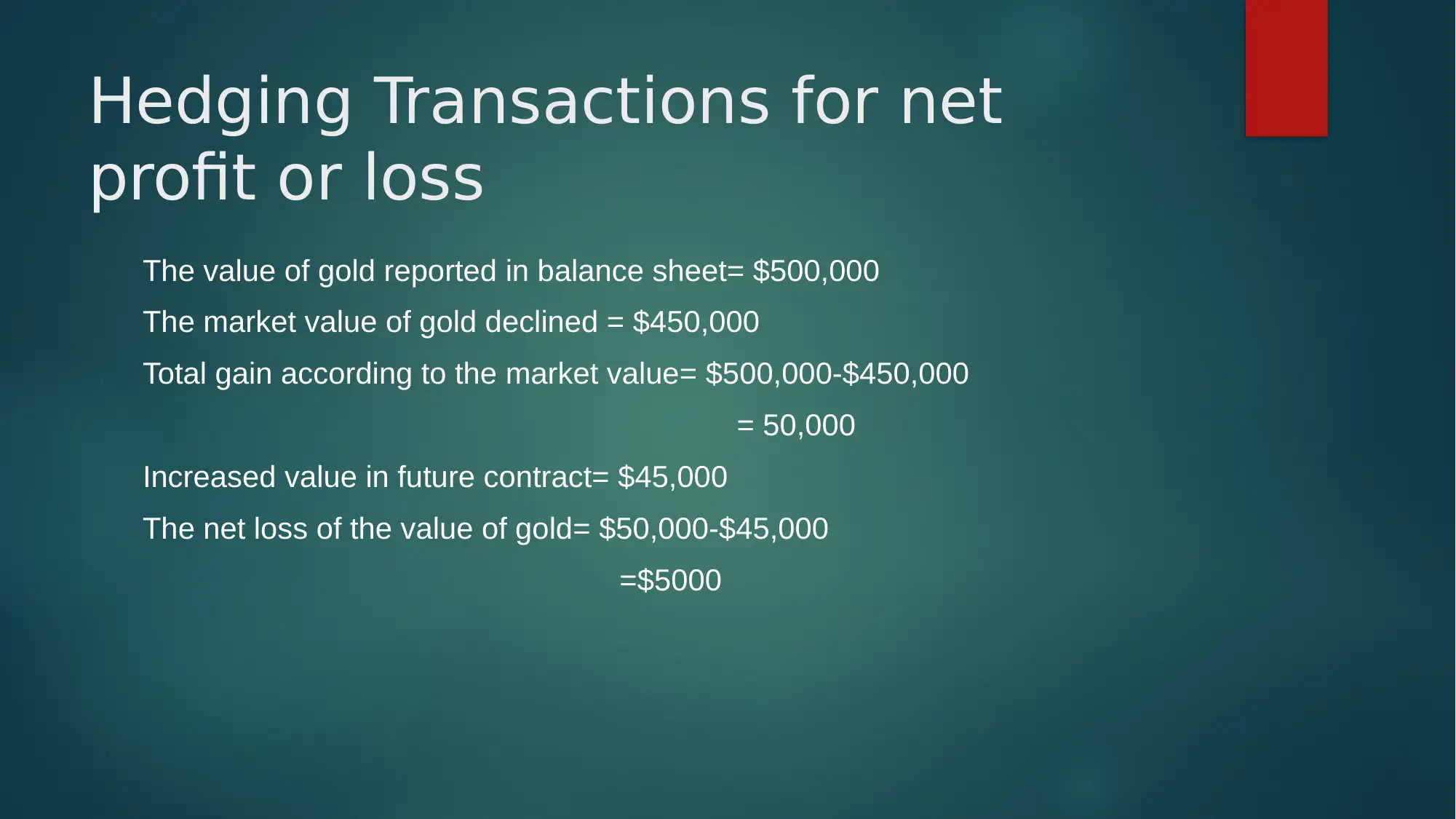

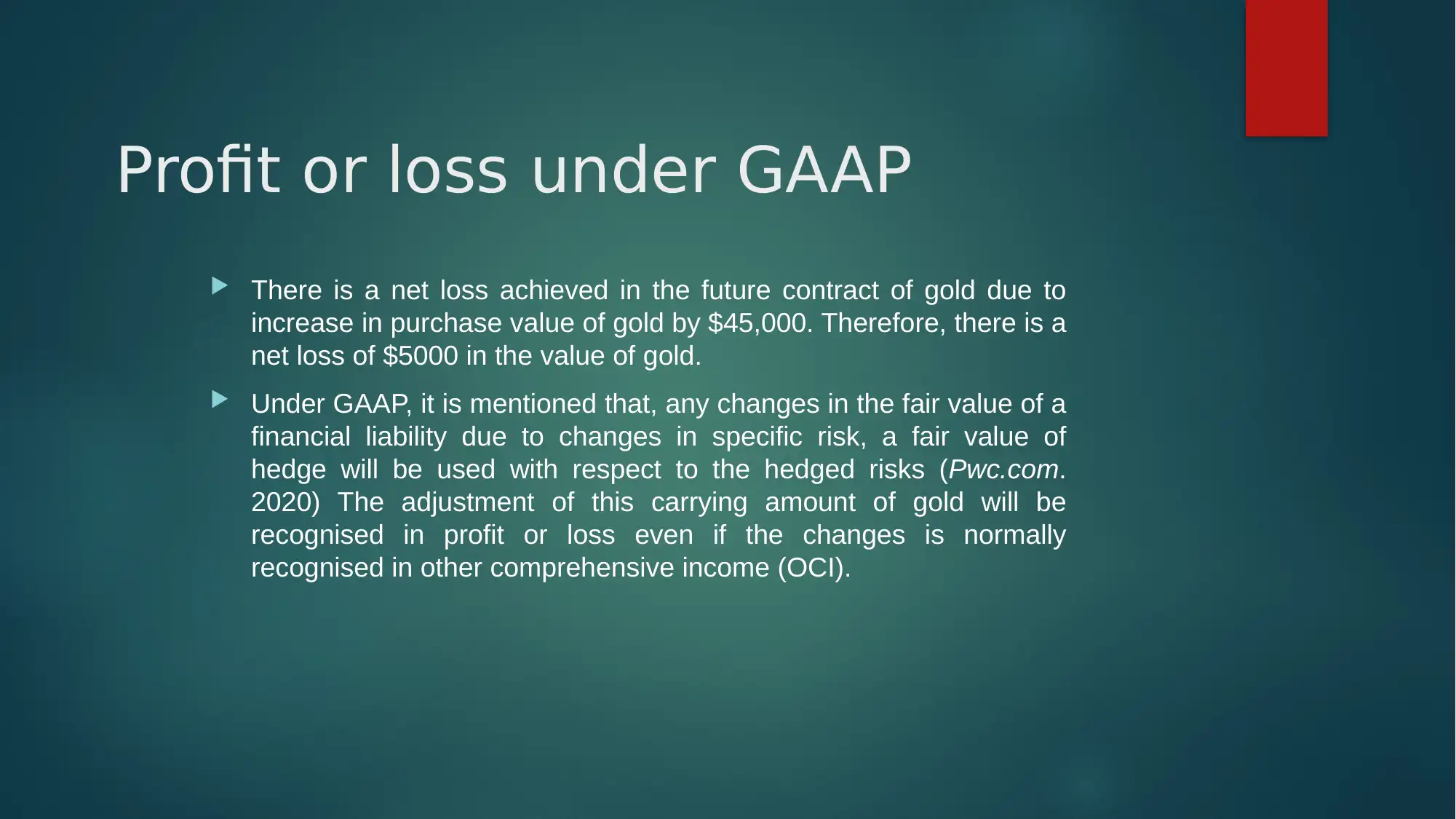

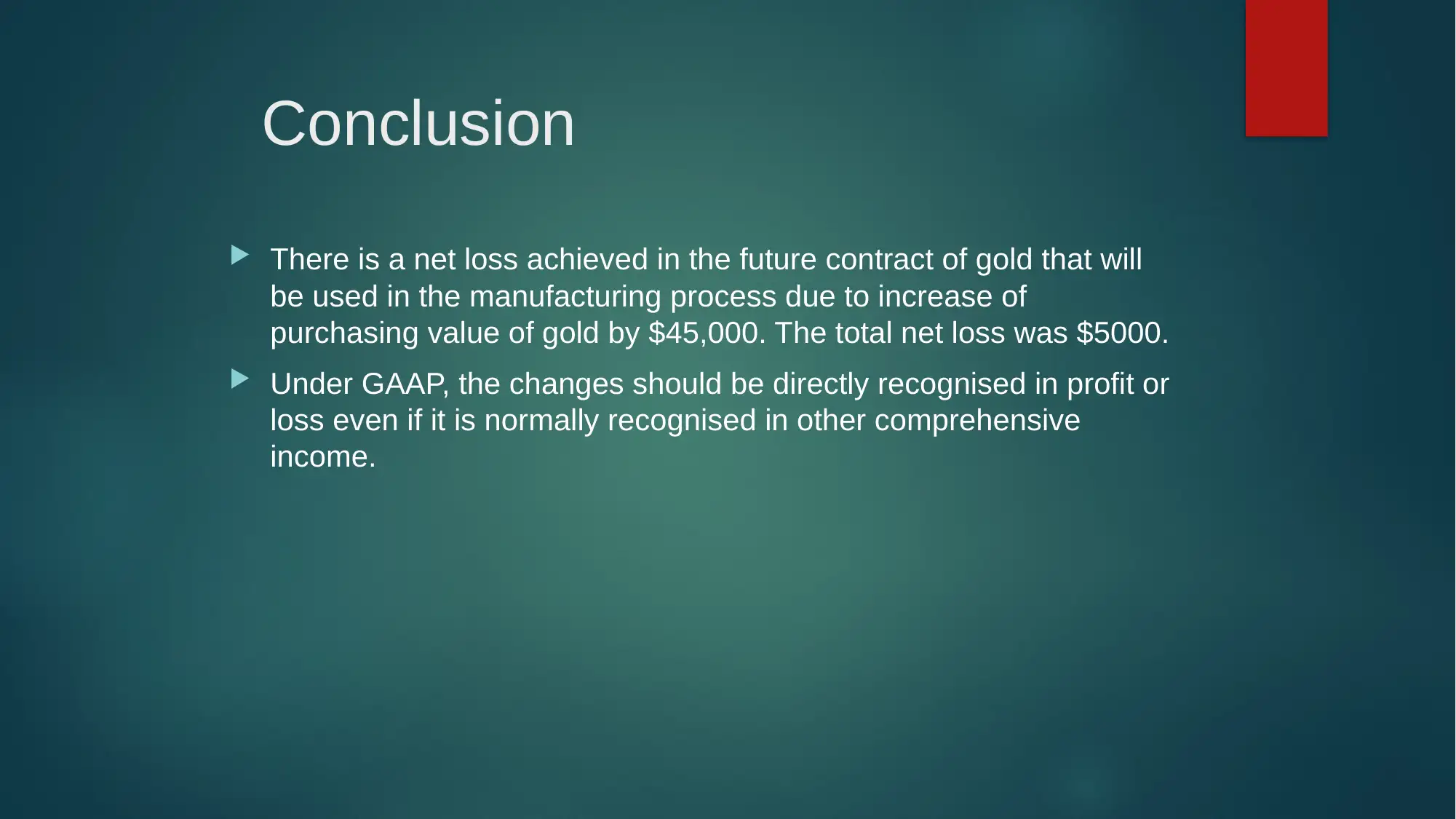

This assignment explores hedge instruments, which are financial tools used to offset changes in the value of hedged items, minimizing risks and securing future exchange rates. The document covers various instruments like stocks, forward contracts, and options. It details hedge accounting under GAAP and IFRS, highlighting differences in effectiveness measurement and recognition of fair value changes. A practical example illustrates a hedging transaction for net profit or loss, showing the accounting treatment under both standards. The assignment concludes by emphasizing that under GAAP, changes are directly recognized in profit or loss, even if usually recognized in other comprehensive income. The document provides references from reputable sources like CME Group and PwC to support the information.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.