Comprehensive Accounting Assignment: Financial Statement Analysis

VerifiedAdded on 2020/02/24

|13

|2170

|53

Homework Assignment

AI Summary

This document presents a student's solutions to an accounting assignment, addressing various aspects of financial accounting. The assignment covers topics such as using Excel for financial calculations, including named cells, formatting negative numbers, and creating separate spreadsheets to avoid errors. It also delves into the application of the IF statement in Excel, periodic inventory systems, and the preparation of trading, profit and loss accounts, and balance sheets. The assignment further explores bank reconciliation processes, journal entries for accounts receivable, and methods for estimating bad debts. Additionally, it examines the impact of accounts receivable on a firm's liquidity, the conversion of credit sales to notes receivable, and the analysis of Wesfarmers' 2016 annual report. The student provides detailed explanations, examples, and relevant formulas to support the answers.

Student name:

Student ID number:

Assignment task number: 2

Subject code and name:

THIS IS MY OWN WORK, AND HASN’T BEEN PLAGIARISED with all the sources

been acknowledged

Student ID number:

Assignment task number: 2

Subject code and name:

THIS IS MY OWN WORK, AND HASN’T BEEN PLAGIARISED with all the sources

been acknowledged

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Q1................................................................................................................................................3

Q2................................................................................................................................................3

Q3................................................................................................................................................3

Q4................................................................................................................................................4

Q5................................................................................................................................................4

Q6................................................................................................................................................5

C..................................................................................................................................................8

Q7................................................................................................................................................8

Q8 Bank Reconciliation..............................................................................................................8

Q9................................................................................................................................................9

Q10..............................................................................................................................................9

Q11............................................................................................................................................10

Q12............................................................................................................................................10

Q13............................................................................................................................................11

Wesfarmers Annual Report 2016..............................................................................................11

References.................................................................................................................................13

Q1................................................................................................................................................3

Q2................................................................................................................................................3

Q3................................................................................................................................................3

Q4................................................................................................................................................4

Q5................................................................................................................................................4

Q6................................................................................................................................................5

C..................................................................................................................................................8

Q7................................................................................................................................................8

Q8 Bank Reconciliation..............................................................................................................8

Q9................................................................................................................................................9

Q10..............................................................................................................................................9

Q11............................................................................................................................................10

Q12............................................................................................................................................10

Q13............................................................................................................................................11

Wesfarmers Annual Report 2016..............................................................................................11

References.................................................................................................................................13

Q1.

It is simpler to replace the cell reference with any name so that the work becomes easy, simple

and fast. For this replacement the name box can be utilised. The formula bar's left side is for

name box. The user can simply understand with the name and file becomes simple (Szulewski,

2016). Any cell, table and function can be given a name. These named cells can be simply

updated, reviewed or managed.

Eg: excel attached

Q2

The negative numerals can be marked in red, red brackets, negative symbol etc. The choice can

be made by using the option of "format cells", and there is even a choice of using decimals

(Brennan, 2016). The signs can depend on the appearance needed by the user, content needed by

the user, option to be utilized, ease of use etc. For example, the excel spreadsheet has been

attached.

Q3

An accountant has to create a separate reported spreadsheet for avoiding the "black box effect”

as the person who creates the spreadsheet is aware of its workings and must have the capacity to

change it in the right manner (Alfian, 2013). The data doesn't get manipulated if the different

sheets are used for graphs and data presentation. This way there would be less errors and

improved decisions. Its example has been attached.

It is simpler to replace the cell reference with any name so that the work becomes easy, simple

and fast. For this replacement the name box can be utilised. The formula bar's left side is for

name box. The user can simply understand with the name and file becomes simple (Szulewski,

2016). Any cell, table and function can be given a name. These named cells can be simply

updated, reviewed or managed.

Eg: excel attached

Q2

The negative numerals can be marked in red, red brackets, negative symbol etc. The choice can

be made by using the option of "format cells", and there is even a choice of using decimals

(Brennan, 2016). The signs can depend on the appearance needed by the user, content needed by

the user, option to be utilized, ease of use etc. For example, the excel spreadsheet has been

attached.

Q3

An accountant has to create a separate reported spreadsheet for avoiding the "black box effect”

as the person who creates the spreadsheet is aware of its workings and must have the capacity to

change it in the right manner (Alfian, 2013). The data doesn't get manipulated if the different

sheets are used for graphs and data presentation. This way there would be less errors and

improved decisions. Its example has been attached.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

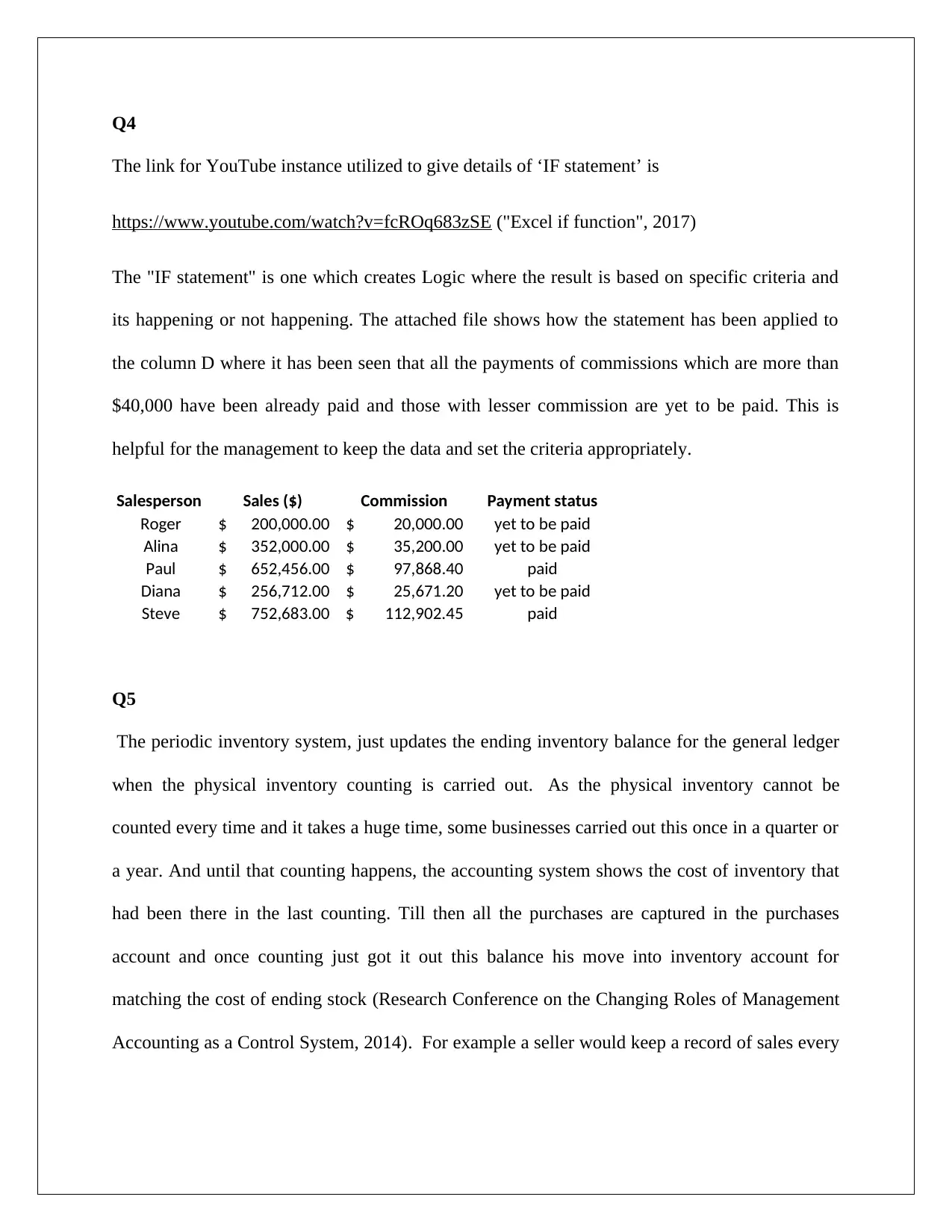

Q4

The link for YouTube instance utilized to give details of ‘IF statement’ is

https://www.youtube.com/watch?v=fcROq683zSE ("Excel if function", 2017)

The "IF statement" is one which creates Logic where the result is based on specific criteria and

its happening or not happening. The attached file shows how the statement has been applied to

the column D where it has been seen that all the payments of commissions which are more than

$40,000 have been already paid and those with lesser commission are yet to be paid. This is

helpful for the management to keep the data and set the criteria appropriately.

Salesperson Sales ($) Commission Payment status

Roger 200,000.00$ 20,000.00$ yet to be paid

Alina 352,000.00$ 35,200.00$ yet to be paid

Paul 652,456.00$ 97,868.40$ paid

Diana 256,712.00$ 25,671.20$ yet to be paid

Steve 752,683.00$ 112,902.45$ paid

Q5

The periodic inventory system, just updates the ending inventory balance for the general ledger

when the physical inventory counting is carried out. As the physical inventory cannot be

counted every time and it takes a huge time, some businesses carried out this once in a quarter or

a year. And until that counting happens, the accounting system shows the cost of inventory that

had been there in the last counting. Till then all the purchases are captured in the purchases

account and once counting just got it out this balance his move into inventory account for

matching the cost of ending stock (Research Conference on the Changing Roles of Management

Accounting as a Control System, 2014). For example a seller would keep a record of sales every

The link for YouTube instance utilized to give details of ‘IF statement’ is

https://www.youtube.com/watch?v=fcROq683zSE ("Excel if function", 2017)

The "IF statement" is one which creates Logic where the result is based on specific criteria and

its happening or not happening. The attached file shows how the statement has been applied to

the column D where it has been seen that all the payments of commissions which are more than

$40,000 have been already paid and those with lesser commission are yet to be paid. This is

helpful for the management to keep the data and set the criteria appropriately.

Salesperson Sales ($) Commission Payment status

Roger 200,000.00$ 20,000.00$ yet to be paid

Alina 352,000.00$ 35,200.00$ yet to be paid

Paul 652,456.00$ 97,868.40$ paid

Diana 256,712.00$ 25,671.20$ yet to be paid

Steve 752,683.00$ 112,902.45$ paid

Q5

The periodic inventory system, just updates the ending inventory balance for the general ledger

when the physical inventory counting is carried out. As the physical inventory cannot be

counted every time and it takes a huge time, some businesses carried out this once in a quarter or

a year. And until that counting happens, the accounting system shows the cost of inventory that

had been there in the last counting. Till then all the purchases are captured in the purchases

account and once counting just got it out this balance his move into inventory account for

matching the cost of ending stock (Research Conference on the Changing Roles of Management

Accounting as a Control System, 2014). For example a seller would keep a record of sales every

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sunday and manages the invoices until those are recorded in the ledger (Starling, 2013). Till then

the balance of the ledger remains same as the past week's balance.

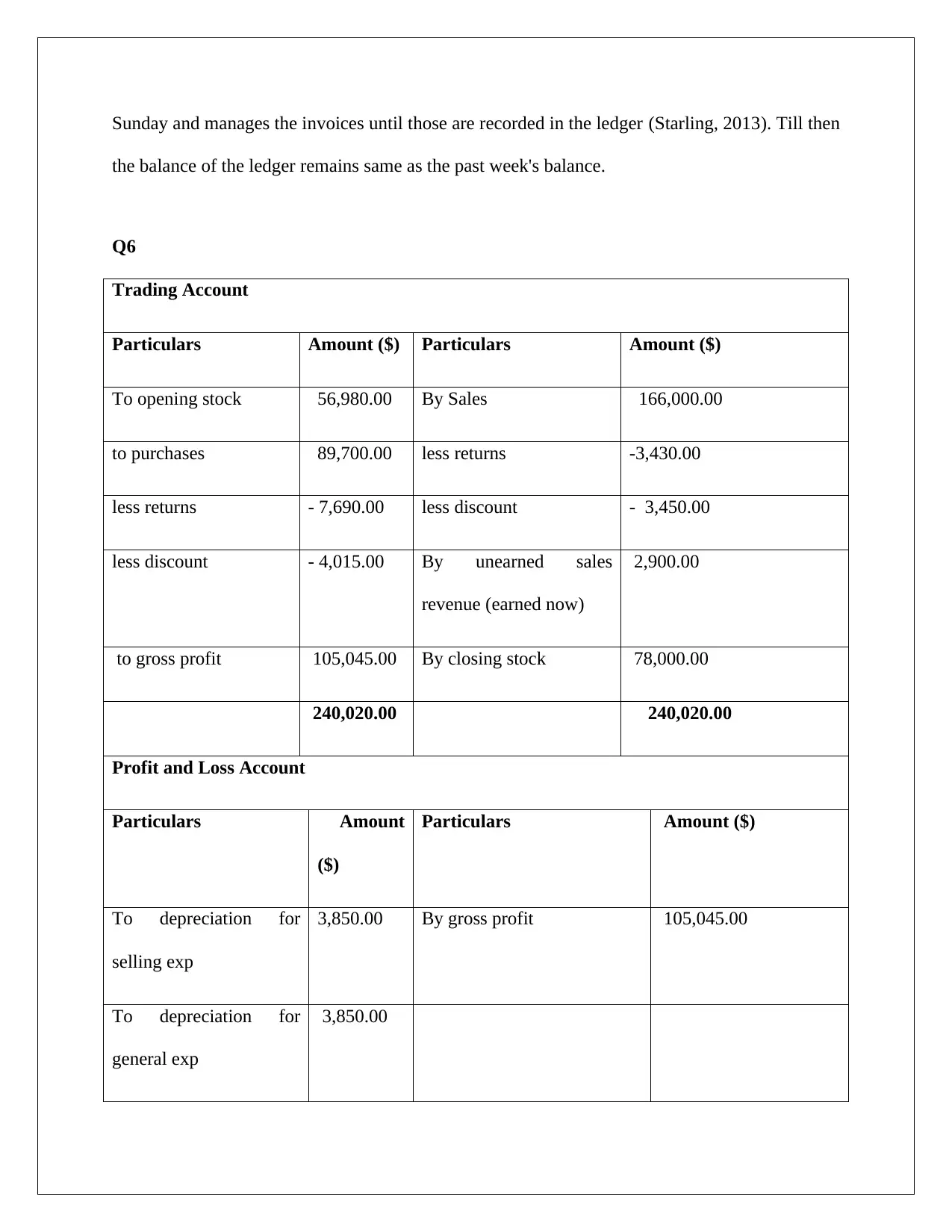

Q6

Trading Account

Particulars Amount ($) Particulars Amount ($)

To opening stock 56,980.00 By Sales 166,000.00

to purchases 89,700.00 less returns -3,430.00

less returns - 7,690.00 less discount - 3,450.00

less discount - 4,015.00 By unearned sales

revenue (earned now)

2,900.00

to gross profit 105,045.00 By closing stock 78,000.00

240,020.00 240,020.00

Profit and Loss Account

Particulars Amount

($)

Particulars Amount ($)

To depreciation for

selling exp

3,850.00 By gross profit 105,045.00

To depreciation for

general exp

3,850.00

the balance of the ledger remains same as the past week's balance.

Q6

Trading Account

Particulars Amount ($) Particulars Amount ($)

To opening stock 56,980.00 By Sales 166,000.00

to purchases 89,700.00 less returns -3,430.00

less returns - 7,690.00 less discount - 3,450.00

less discount - 4,015.00 By unearned sales

revenue (earned now)

2,900.00

to gross profit 105,045.00 By closing stock 78,000.00

240,020.00 240,020.00

Profit and Loss Account

Particulars Amount

($)

Particulars Amount ($)

To depreciation for

selling exp

3,850.00 By gross profit 105,045.00

To depreciation for

general exp

3,850.00

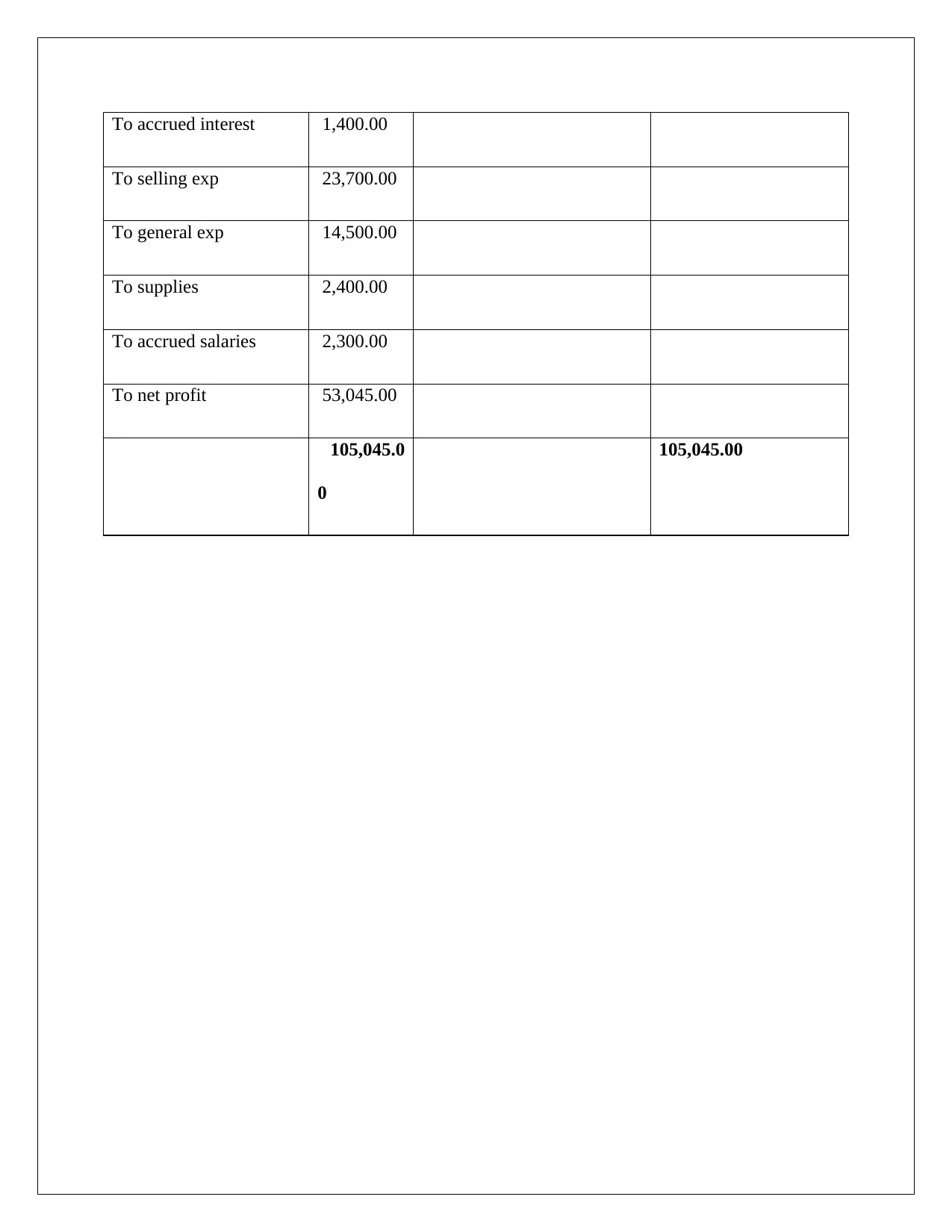

To accrued interest 1,400.00

To selling exp 23,700.00

To general exp 14,500.00

To supplies 2,400.00

To accrued salaries 2,300.00

To net profit 53,045.00

105,045.0

0

105,045.00

To selling exp 23,700.00

To general exp 14,500.00

To supplies 2,400.00

To accrued salaries 2,300.00

To net profit 53,045.00

105,045.0

0

105,045.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

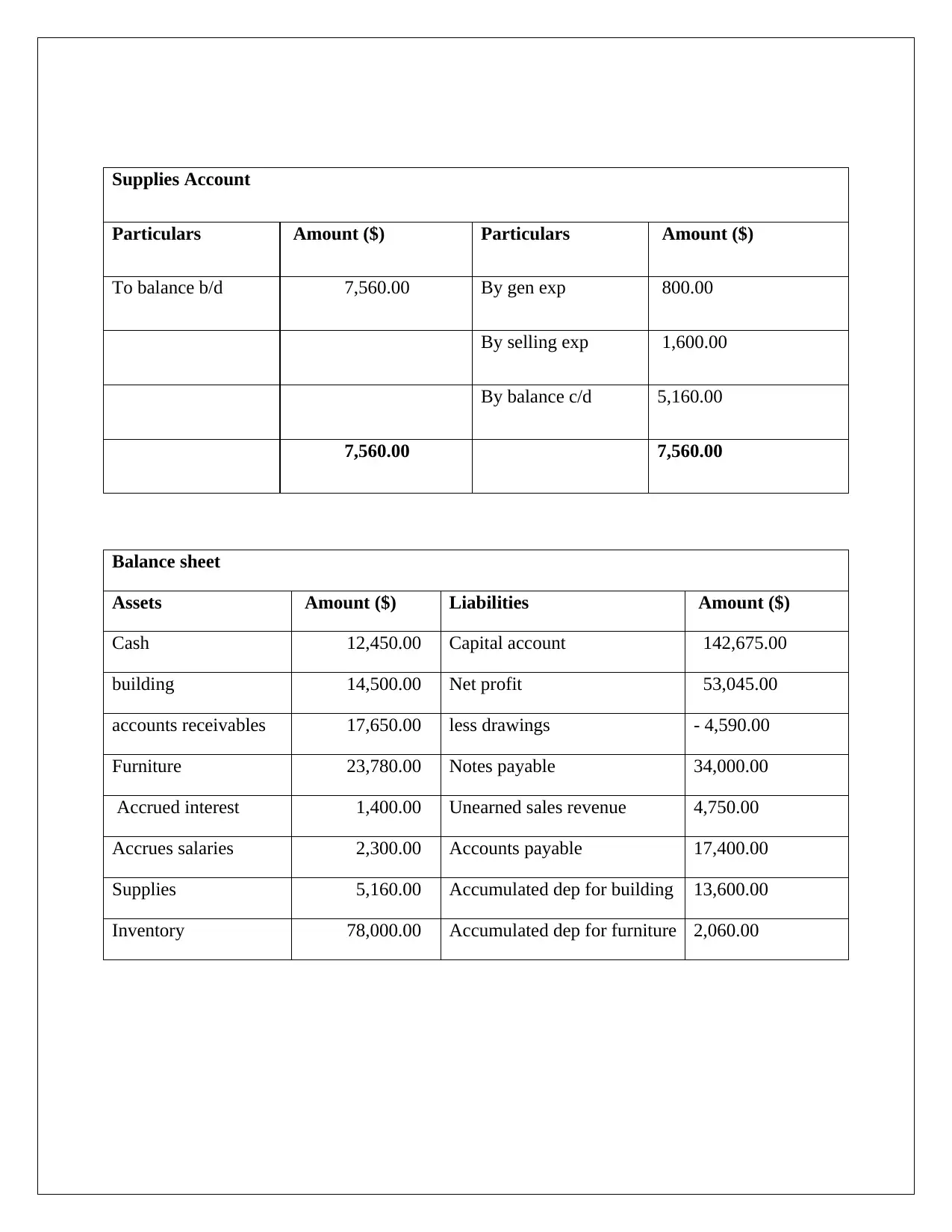

Supplies Account

Particulars Amount ($) Particulars Amount ($)

To balance b/d 7,560.00 By gen exp 800.00

By selling exp 1,600.00

By balance c/d 5,160.00

7,560.00 7,560.00

Balance sheet

Assets Amount ($) Liabilities Amount ($)

Cash 12,450.00 Capital account 142,675.00

building 14,500.00 Net profit 53,045.00

accounts receivables 17,650.00 less drawings - 4,590.00

Furniture 23,780.00 Notes payable 34,000.00

Accrued interest 1,400.00 Unearned sales revenue 4,750.00

Accrues salaries 2,300.00 Accounts payable 17,400.00

Supplies 5,160.00 Accumulated dep for building 13,600.00

Inventory 78,000.00 Accumulated dep for furniture 2,060.00

Particulars Amount ($) Particulars Amount ($)

To balance b/d 7,560.00 By gen exp 800.00

By selling exp 1,600.00

By balance c/d 5,160.00

7,560.00 7,560.00

Balance sheet

Assets Amount ($) Liabilities Amount ($)

Cash 12,450.00 Capital account 142,675.00

building 14,500.00 Net profit 53,045.00

accounts receivables 17,650.00 less drawings - 4,590.00

Furniture 23,780.00 Notes payable 34,000.00

Accrued interest 1,400.00 Unearned sales revenue 4,750.00

Accrues salaries 2,300.00 Accounts payable 17,400.00

Supplies 5,160.00 Accumulated dep for building 13,600.00

Inventory 78,000.00 Accumulated dep for furniture 2,060.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

C.

The use of spreadsheets is beneficial as the spreadsheets can be simply exchanged with any tools

or systems. These can be attached in the mail or any application. In case any highly skilled

person makes its template or uses formula in the templates then anyone can use these simple.

Q7

The question seventh in the sheet shows both along with the formula view and the same view can

be attained by using simple steps:

Ctrl+A,

Ctrl+~ (Goldmeier, n.d.)

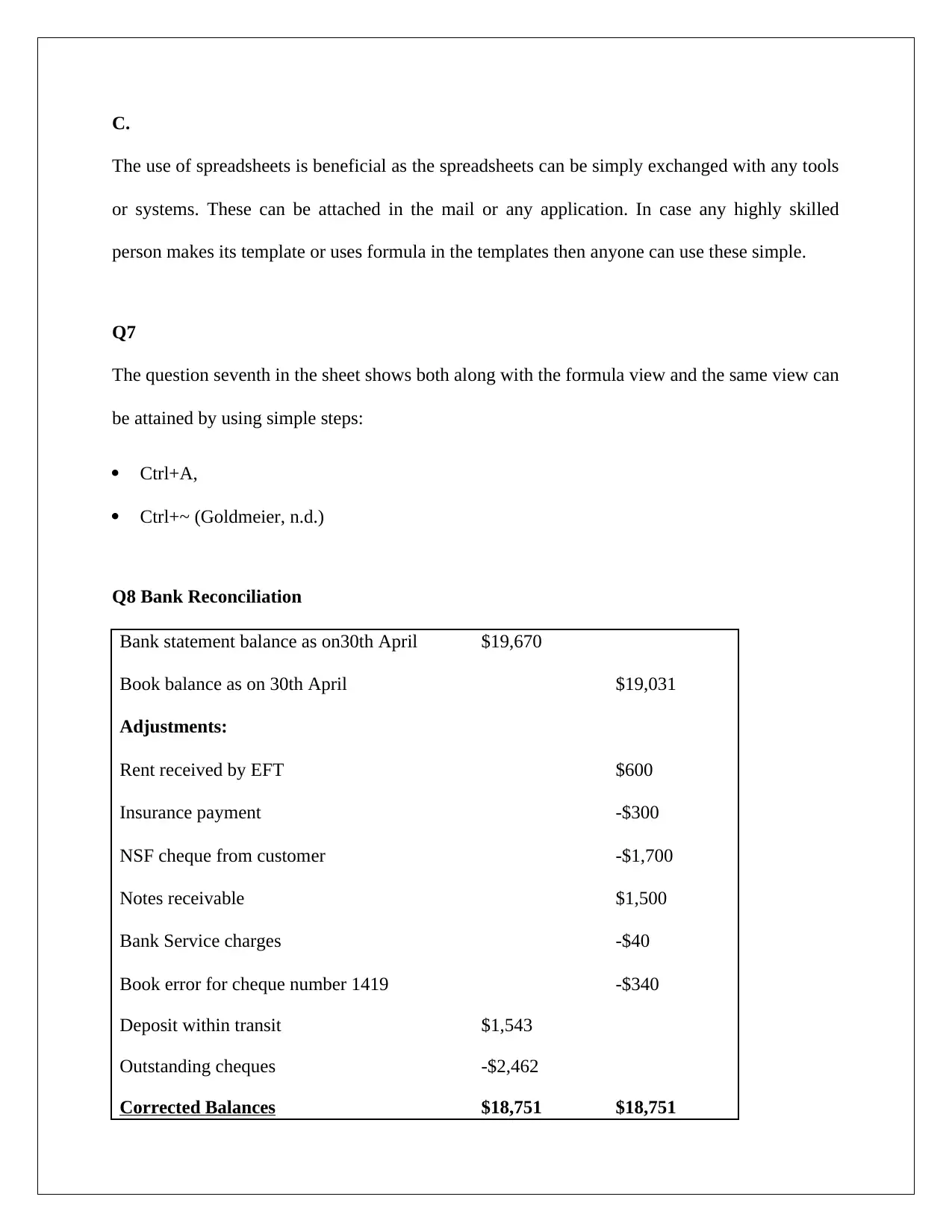

Q8 Bank Reconciliation

Bank statement balance as on30th April $19,670

Book balance as on 30th April $19,031

Adjustments:

Rent received by EFT $600

Insurance payment -$300

NSF cheque from customer -$1,700

Notes receivable $1,500

Bank Service charges -$40

Book error for cheque number 1419 -$340

Deposit within transit $1,543

Outstanding cheques -$2,462

Corrected Balances $18,751 $18,751

The use of spreadsheets is beneficial as the spreadsheets can be simply exchanged with any tools

or systems. These can be attached in the mail or any application. In case any highly skilled

person makes its template or uses formula in the templates then anyone can use these simple.

Q7

The question seventh in the sheet shows both along with the formula view and the same view can

be attained by using simple steps:

Ctrl+A,

Ctrl+~ (Goldmeier, n.d.)

Q8 Bank Reconciliation

Bank statement balance as on30th April $19,670

Book balance as on 30th April $19,031

Adjustments:

Rent received by EFT $600

Insurance payment -$300

NSF cheque from customer -$1,700

Notes receivable $1,500

Bank Service charges -$40

Book error for cheque number 1419 -$340

Deposit within transit $1,543

Outstanding cheques -$2,462

Corrected Balances $18,751 $18,751

Q9

a) Accounts receivables A/c Dr $34,000

To Sales $34,000

(For sales on credit)

b) Cash A/c Dr $17,400

To Accounts receivables $17,400

(For collection of part amount owed)

c) Bad debt A/c Dr $16,600

To Accounts Receivables $16,600

(For writing off the accounts receivable)

d) Accounts receivables A/c Dr $16,600

To Bad debt A/c $16,600

(For reinstating an amount written off)

e) Cash A/c Dr $16,600

To Accounts receivables $16,600

(For collection in full of the amount owed)

Q10

Taking an example of a supplier which supplies cosmetics to their different businesses, the

balance for accounts receivable is $10,000. Looking at the previous few ears trend it has been

a) Accounts receivables A/c Dr $34,000

To Sales $34,000

(For sales on credit)

b) Cash A/c Dr $17,400

To Accounts receivables $17,400

(For collection of part amount owed)

c) Bad debt A/c Dr $16,600

To Accounts Receivables $16,600

(For writing off the accounts receivable)

d) Accounts receivables A/c Dr $16,600

To Bad debt A/c $16,600

(For reinstating an amount written off)

e) Cash A/c Dr $16,600

To Accounts receivables $16,600

(For collection in full of the amount owed)

Q10

Taking an example of a supplier which supplies cosmetics to their different businesses, the

balance for accounts receivable is $10,000. Looking at the previous few ears trend it has been

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

seen usually the 3% of the receivable score for better. Therefore under the method of sales, if the

income statement has sales for $6000 then the journal entry would be passed for 3% * $6000=

$180

Bad debts a/c dr $180

To allowances for losses $180

As per the income method, it would be evaluated as 3% of $10000 that is $300. For this, the

journal entry would be

Bad debts a/c dr $300

To allowances for losses $300

Q11

The accounts receivable form a part of financial position and these can be used to see how much

cash would be coming up with the business. With the past trends of business can also see how

much collectables would be converted into cash and how much are expected to be bad debts.

Therefore the receivables have a huge effect on the liquidity of the firm. The business uses it

stock to produce the goods and then the same is changed into accounts receivable and finally

cash generated from the same. So it can be said that receivables if it the liquidity of firm and

therefore these affect the financial position also.

Q12

An example of this is when Angels Company sells the supplies to Rogers Ltd for $70,000.

This payment has to made within 45 days however, the contract states that after the two months

there would be notes payables given to Rogers Ltd and that would be of $85,000 with 10%

interest for payment on quarterly basis. Therefore the journal entries would be as below.

income statement has sales for $6000 then the journal entry would be passed for 3% * $6000=

$180

Bad debts a/c dr $180

To allowances for losses $180

As per the income method, it would be evaluated as 3% of $10000 that is $300. For this, the

journal entry would be

Bad debts a/c dr $300

To allowances for losses $300

Q11

The accounts receivable form a part of financial position and these can be used to see how much

cash would be coming up with the business. With the past trends of business can also see how

much collectables would be converted into cash and how much are expected to be bad debts.

Therefore the receivables have a huge effect on the liquidity of the firm. The business uses it

stock to produce the goods and then the same is changed into accounts receivable and finally

cash generated from the same. So it can be said that receivables if it the liquidity of firm and

therefore these affect the financial position also.

Q12

An example of this is when Angels Company sells the supplies to Rogers Ltd for $70,000.

This payment has to made within 45 days however, the contract states that after the two months

there would be notes payables given to Rogers Ltd and that would be of $85,000 with 10%

interest for payment on quarterly basis. Therefore the journal entries would be as below.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Entry for credit sales:

a) Rogers Ltd Dr $70,000

To sales $70,000

b) Accounts receivable A/c Dr $70,000

To sales $70,000

Entry to change to notes receivables

Notes receivable Dr $85,000

To accounts receivable $85,000

Entry for dishonouring of note

Bad debts A/c Dr $93,500

To notes receivable $85,000

To interest receivable $8,500

Entry for next delayed payment

Cash account Dr $93,500

To bad debts account $93,500

Q13

Wesfarmers Annual Report 2016

The report has made for the understanding of accounting and its impact on this Wesfarmers.

After studying the net profit of the business and its financial reports, it is suggested to one of the

friends that it is absolutely okay to purchase of course these are likely to be beneficial

a) Rogers Ltd Dr $70,000

To sales $70,000

b) Accounts receivable A/c Dr $70,000

To sales $70,000

Entry to change to notes receivables

Notes receivable Dr $85,000

To accounts receivable $85,000

Entry for dishonouring of note

Bad debts A/c Dr $93,500

To notes receivable $85,000

To interest receivable $8,500

Entry for next delayed payment

Cash account Dr $93,500

To bad debts account $93,500

Q13

Wesfarmers Annual Report 2016

The report has made for the understanding of accounting and its impact on this Wesfarmers.

After studying the net profit of the business and its financial reports, it is suggested to one of the

friends that it is absolutely okay to purchase of course these are likely to be beneficial

It is a huge group of companies which are dealing into supermarts, liquor, coal, energy products,

improvement goods, convenience stores, safety items, chemicals and fertilisers and the office

supplies.

Looking at the reports of the business its net profit after tax had been $407 million for that year

ending 2016. The same has been shown in the spreadsheet attached along with the 3-D graph.

This is one of the famous companies all of the world and it is also a court of the stock exchange

of Australia. The stakeholders look into its reports to see how to businesses performing and to

protect its profitability in the liquidity. It is also used for assessing the business in comparison to

its competitors.

The financial reports show that $2.87 billion have been earned as net profit after tax in the year

2016, which had been approximately 606% more than the previous year’s $407 millions.

Looking at the graphs it can also be seen that the cash reserves for the business had become

better and its casual margins also improved because The Company was capable of running $4.23

billion through its operations.

The company is performing better because its dividends per share and earnings per share have

been improving yearly. This trend of betterment has made the business capable of sustaining in

such a competitive environment where many businesses have surrendered to losses or to

liquidation. This capacity and its debt capital ratio show how the business has been capable to

survive and is expected to continue growing. Even though the risk of investment is always there,

still after studying the financial reports of this company it is advisable that the investment can be

made. There has been a rise in the working capital due to this business acquiring home-base

along with the retail portfolios.

Working capital ratio =Current assets/ current liabilities

improvement goods, convenience stores, safety items, chemicals and fertilisers and the office

supplies.

Looking at the reports of the business its net profit after tax had been $407 million for that year

ending 2016. The same has been shown in the spreadsheet attached along with the 3-D graph.

This is one of the famous companies all of the world and it is also a court of the stock exchange

of Australia. The stakeholders look into its reports to see how to businesses performing and to

protect its profitability in the liquidity. It is also used for assessing the business in comparison to

its competitors.

The financial reports show that $2.87 billion have been earned as net profit after tax in the year

2016, which had been approximately 606% more than the previous year’s $407 millions.

Looking at the graphs it can also be seen that the cash reserves for the business had become

better and its casual margins also improved because The Company was capable of running $4.23

billion through its operations.

The company is performing better because its dividends per share and earnings per share have

been improving yearly. This trend of betterment has made the business capable of sustaining in

such a competitive environment where many businesses have surrendered to losses or to

liquidation. This capacity and its debt capital ratio show how the business has been capable to

survive and is expected to continue growing. Even though the risk of investment is always there,

still after studying the financial reports of this company it is advisable that the investment can be

made. There has been a rise in the working capital due to this business acquiring home-base

along with the retail portfolios.

Working capital ratio =Current assets/ current liabilities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.