Accounting Principles and Financial Statements Assignment

VerifiedAdded on 2022/12/30

|14

|2543

|91

Homework Assignment

AI Summary

This document provides a comprehensive solution to an accounting assignment, addressing key concepts in financial accounting. The solution begins with journalizing transactions and posting them to ledger accounts, followed by a discussion on the relationship between bookkeeping and accounting. The assignment then presents the preparation of an income statement and balance sheet for Indus Corp, along with an explanation of the importance of financial statements for a business. Further, the solution includes a cash budget and an analysis of zero-based budgeting. Cost behavior analysis, including the calculation of contribution margin and break-even points, is also covered. Finally, the assignment addresses inventory management, calculating the Economic Order Quantity (EOQ) and average inventory, and discussing inventory record-keeping. The document offers detailed explanations and calculations to aid in understanding the concepts.

ACCOUNTING COURSE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

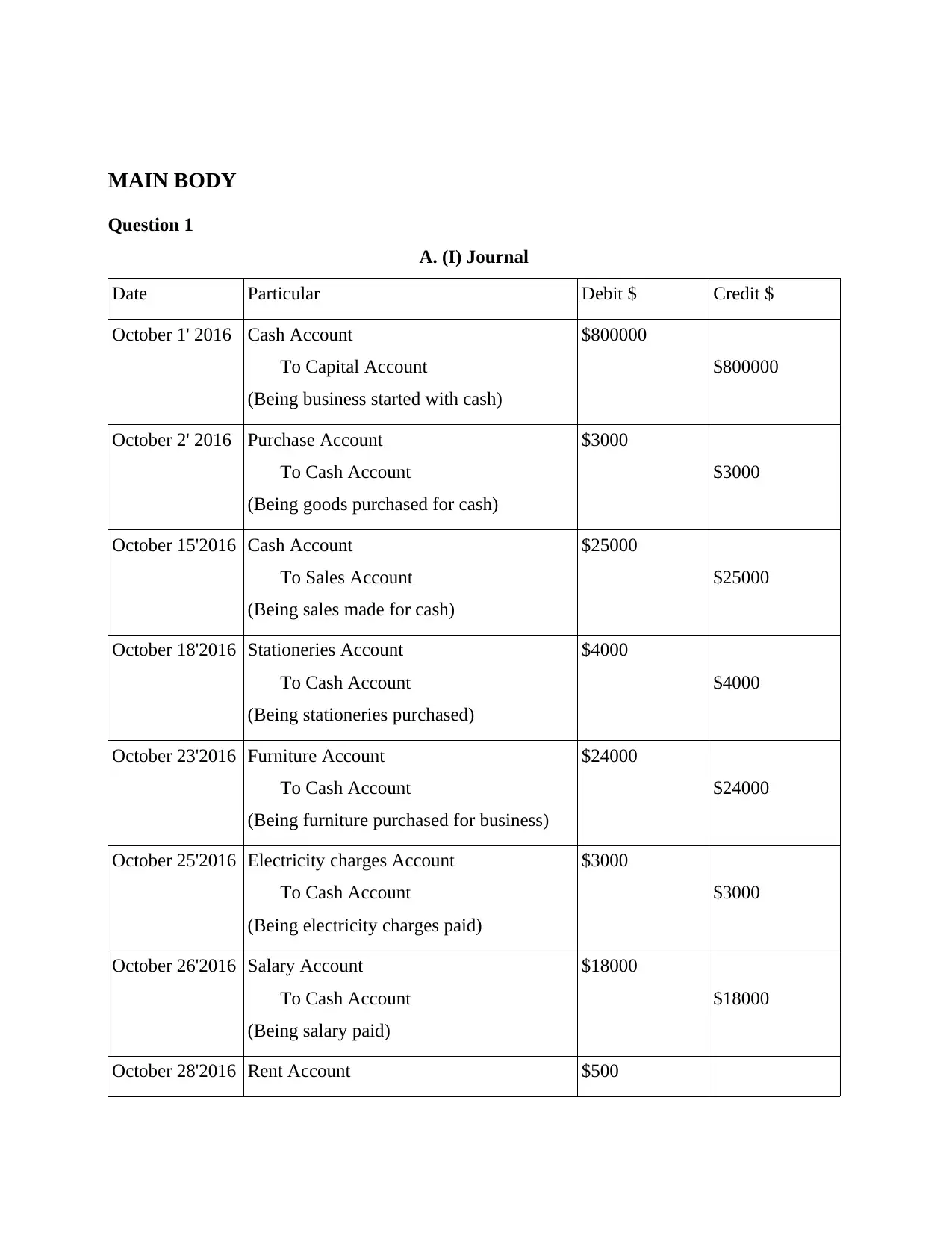

MAIN BODY

Question 1

A. (I) Journal

Date Particular Debit $ Credit $

October 1' 2016 Cash Account

To Capital Account

(Being business started with cash)

$800000

$800000

October 2' 2016 Purchase Account

To Cash Account

(Being goods purchased for cash)

$3000

$3000

October 15'2016 Cash Account

To Sales Account

(Being sales made for cash)

$25000

$25000

October 18'2016 Stationeries Account

To Cash Account

(Being stationeries purchased)

$4000

$4000

October 23'2016 Furniture Account

To Cash Account

(Being furniture purchased for business)

$24000

$24000

October 25'2016 Electricity charges Account

To Cash Account

(Being electricity charges paid)

$3000

$3000

October 26'2016 Salary Account

To Cash Account

(Being salary paid)

$18000

$18000

October 28'2016 Rent Account $500

Question 1

A. (I) Journal

Date Particular Debit $ Credit $

October 1' 2016 Cash Account

To Capital Account

(Being business started with cash)

$800000

$800000

October 2' 2016 Purchase Account

To Cash Account

(Being goods purchased for cash)

$3000

$3000

October 15'2016 Cash Account

To Sales Account

(Being sales made for cash)

$25000

$25000

October 18'2016 Stationeries Account

To Cash Account

(Being stationeries purchased)

$4000

$4000

October 23'2016 Furniture Account

To Cash Account

(Being furniture purchased for business)

$24000

$24000

October 25'2016 Electricity charges Account

To Cash Account

(Being electricity charges paid)

$3000

$3000

October 26'2016 Salary Account

To Cash Account

(Being salary paid)

$18000

$18000

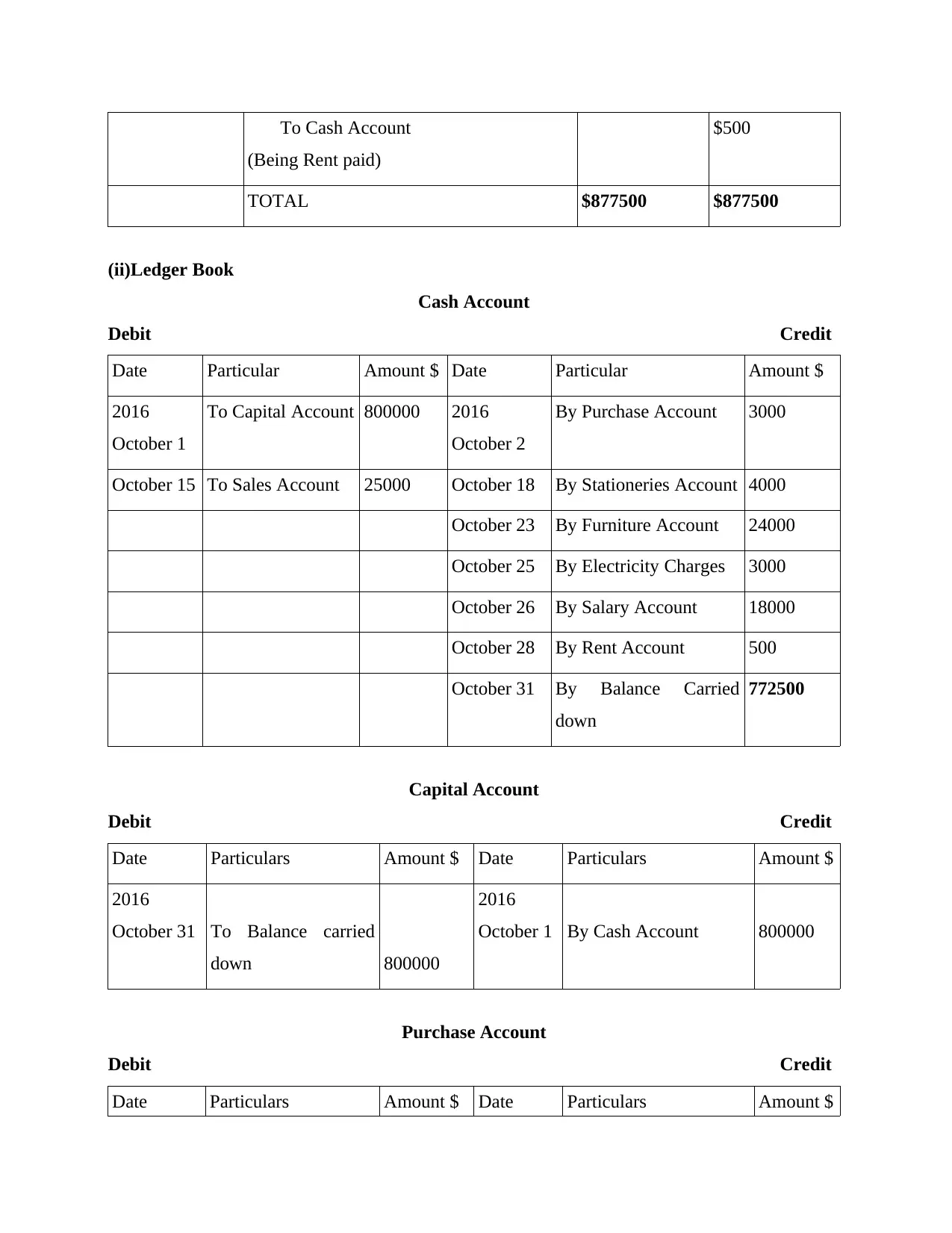

October 28'2016 Rent Account $500

To Cash Account

(Being Rent paid)

$500

TOTAL $877500 $877500

(ii)Ledger Book

Cash Account

Debit Credit

Date Particular Amount $ Date Particular Amount $

2016

October 1

To Capital Account 800000 2016

October 2

By Purchase Account 3000

October 15 To Sales Account 25000 October 18 By Stationeries Account 4000

October 23 By Furniture Account 24000

October 25 By Electricity Charges 3000

October 26 By Salary Account 18000

October 28 By Rent Account 500

October 31 By Balance Carried

down

772500

Capital Account

Debit Credit

Date Particulars Amount $ Date Particulars Amount $

2016

October 31 To Balance carried

down 800000

2016

October 1 By Cash Account 800000

Purchase Account

Debit Credit

Date Particulars Amount $ Date Particulars Amount $

(Being Rent paid)

$500

TOTAL $877500 $877500

(ii)Ledger Book

Cash Account

Debit Credit

Date Particular Amount $ Date Particular Amount $

2016

October 1

To Capital Account 800000 2016

October 2

By Purchase Account 3000

October 15 To Sales Account 25000 October 18 By Stationeries Account 4000

October 23 By Furniture Account 24000

October 25 By Electricity Charges 3000

October 26 By Salary Account 18000

October 28 By Rent Account 500

October 31 By Balance Carried

down

772500

Capital Account

Debit Credit

Date Particulars Amount $ Date Particulars Amount $

2016

October 31 To Balance carried

down 800000

2016

October 1 By Cash Account 800000

Purchase Account

Debit Credit

Date Particulars Amount $ Date Particulars Amount $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2016

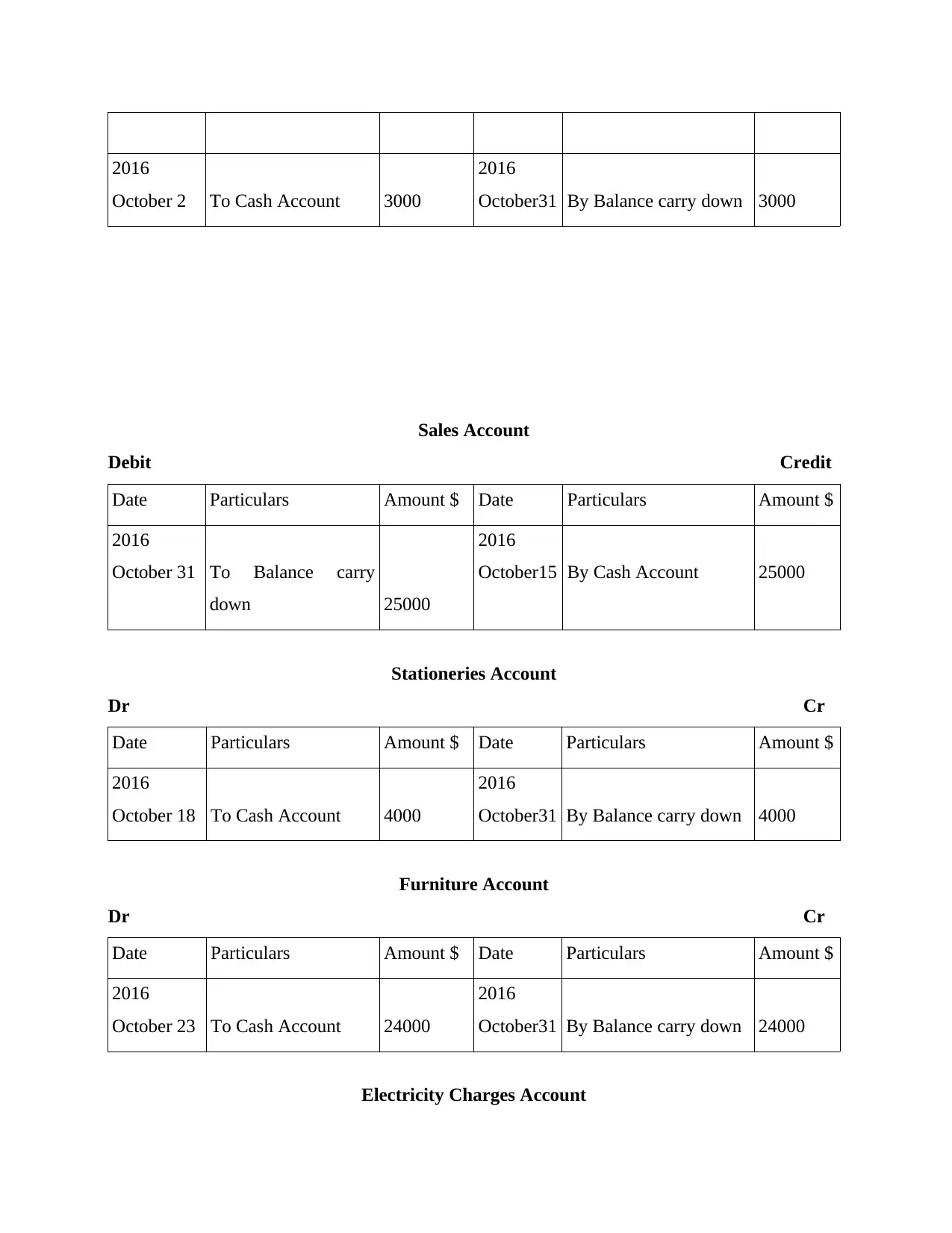

October 2 To Cash Account 3000

2016

October31 By Balance carry down 3000

Sales Account

Debit Credit

Date Particulars Amount $ Date Particulars Amount $

2016

October 31 To Balance carry

down 25000

2016

October15 By Cash Account 25000

Stationeries Account

Dr Cr

Date Particulars Amount $ Date Particulars Amount $

2016

October 18 To Cash Account 4000

2016

October31 By Balance carry down 4000

Furniture Account

Dr Cr

Date Particulars Amount $ Date Particulars Amount $

2016

October 23 To Cash Account 24000

2016

October31 By Balance carry down 24000

Electricity Charges Account

October 2 To Cash Account 3000

2016

October31 By Balance carry down 3000

Sales Account

Debit Credit

Date Particulars Amount $ Date Particulars Amount $

2016

October 31 To Balance carry

down 25000

2016

October15 By Cash Account 25000

Stationeries Account

Dr Cr

Date Particulars Amount $ Date Particulars Amount $

2016

October 18 To Cash Account 4000

2016

October31 By Balance carry down 4000

Furniture Account

Dr Cr

Date Particulars Amount $ Date Particulars Amount $

2016

October 23 To Cash Account 24000

2016

October31 By Balance carry down 24000

Electricity Charges Account

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Dr Cr

Date Particulars Amount $ Date Particulars Amount $

2016

October 25 To Cash Account 3000

2016

October31 By Balance carry down 3000

Salary Account

Dr Cr

Date Particulars Amount $ Date Particulars Amount $

2016

October 26 To Cash Account 18000

2016

October31 By Balance carry down 18000

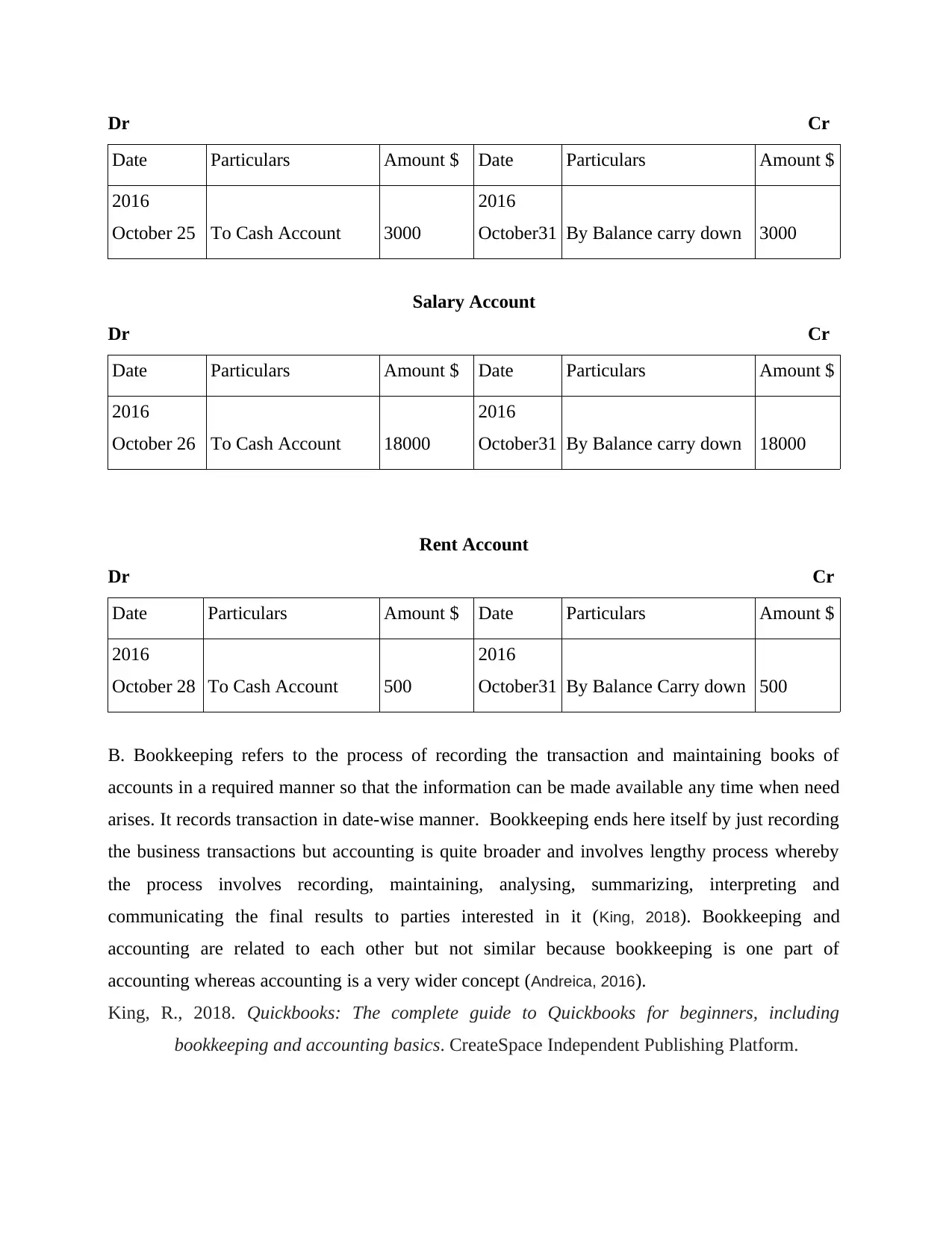

Rent Account

Dr Cr

Date Particulars Amount $ Date Particulars Amount $

2016

October 28 To Cash Account 500

2016

October31 By Balance Carry down 500

B. Bookkeeping refers to the process of recording the transaction and maintaining books of

accounts in a required manner so that the information can be made available any time when need

arises. It records transaction in date-wise manner. Bookkeeping ends here itself by just recording

the business transactions but accounting is quite broader and involves lengthy process whereby

the process involves recording, maintaining, analysing, summarizing, interpreting and

communicating the final results to parties interested in it (King, 2018). Bookkeeping and

accounting are related to each other but not similar because bookkeeping is one part of

accounting whereas accounting is a very wider concept (Andreica, 2016).

King, R., 2018. Quickbooks: The complete guide to Quickbooks for beginners, including

bookkeeping and accounting basics. CreateSpace Independent Publishing Platform.

Date Particulars Amount $ Date Particulars Amount $

2016

October 25 To Cash Account 3000

2016

October31 By Balance carry down 3000

Salary Account

Dr Cr

Date Particulars Amount $ Date Particulars Amount $

2016

October 26 To Cash Account 18000

2016

October31 By Balance carry down 18000

Rent Account

Dr Cr

Date Particulars Amount $ Date Particulars Amount $

2016

October 28 To Cash Account 500

2016

October31 By Balance Carry down 500

B. Bookkeeping refers to the process of recording the transaction and maintaining books of

accounts in a required manner so that the information can be made available any time when need

arises. It records transaction in date-wise manner. Bookkeeping ends here itself by just recording

the business transactions but accounting is quite broader and involves lengthy process whereby

the process involves recording, maintaining, analysing, summarizing, interpreting and

communicating the final results to parties interested in it (King, 2018). Bookkeeping and

accounting are related to each other but not similar because bookkeeping is one part of

accounting whereas accounting is a very wider concept (Andreica, 2016).

King, R., 2018. Quickbooks: The complete guide to Quickbooks for beginners, including

bookkeeping and accounting basics. CreateSpace Independent Publishing Platform.

Andreica, I., 2016. Double entry bookkeeping vs single entry bookkeeping. Bulletin of University

of Agricultural Sciences and Veterinary Medicine Cluj-Napoca. Horticulture. 73(2).

pp.282-290.

Question 2

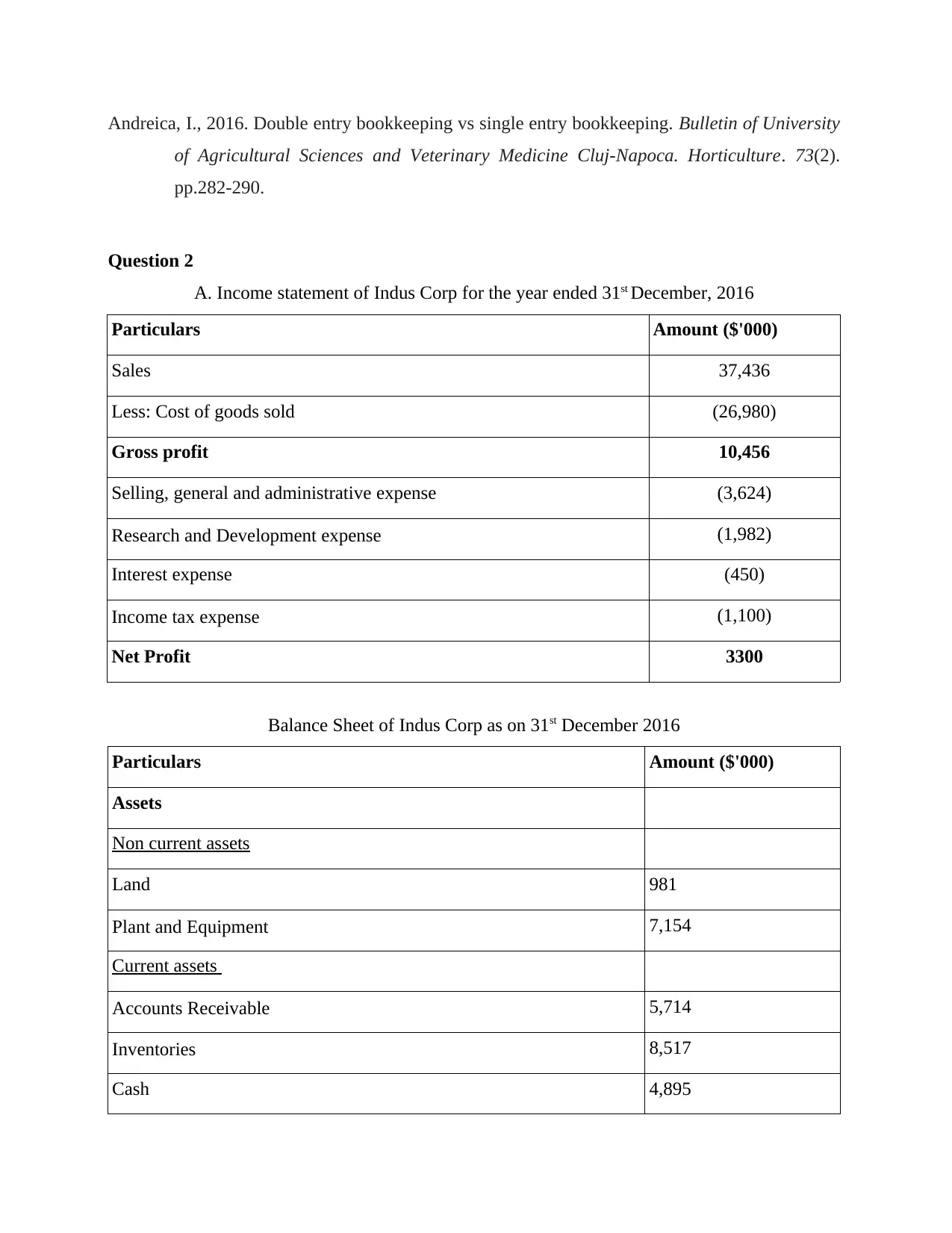

A. Income statement of Indus Corp for the year ended 31st December, 2016

Particulars Amount ($'000)

Sales 37,436

Less: Cost of goods sold (26,980)

Gross profit 10,456

Selling, general and administrative expense (3,624)

Research and Development expense (1,982)

Interest expense (450)

Income tax expense (1,100)

Net Profit 3300

Balance Sheet of Indus Corp as on 31st December 2016

Particulars Amount ($'000)

Assets

Non current assets

Land 981

Plant and Equipment 7,154

Current assets

Accounts Receivable 5,714

Inventories 8,517

Cash 4,895

of Agricultural Sciences and Veterinary Medicine Cluj-Napoca. Horticulture. 73(2).

pp.282-290.

Question 2

A. Income statement of Indus Corp for the year ended 31st December, 2016

Particulars Amount ($'000)

Sales 37,436

Less: Cost of goods sold (26,980)

Gross profit 10,456

Selling, general and administrative expense (3,624)

Research and Development expense (1,982)

Interest expense (450)

Income tax expense (1,100)

Net Profit 3300

Balance Sheet of Indus Corp as on 31st December 2016

Particulars Amount ($'000)

Assets

Non current assets

Land 981

Plant and Equipment 7,154

Current assets

Accounts Receivable 5,714

Inventories 8,517

Cash 4,895

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

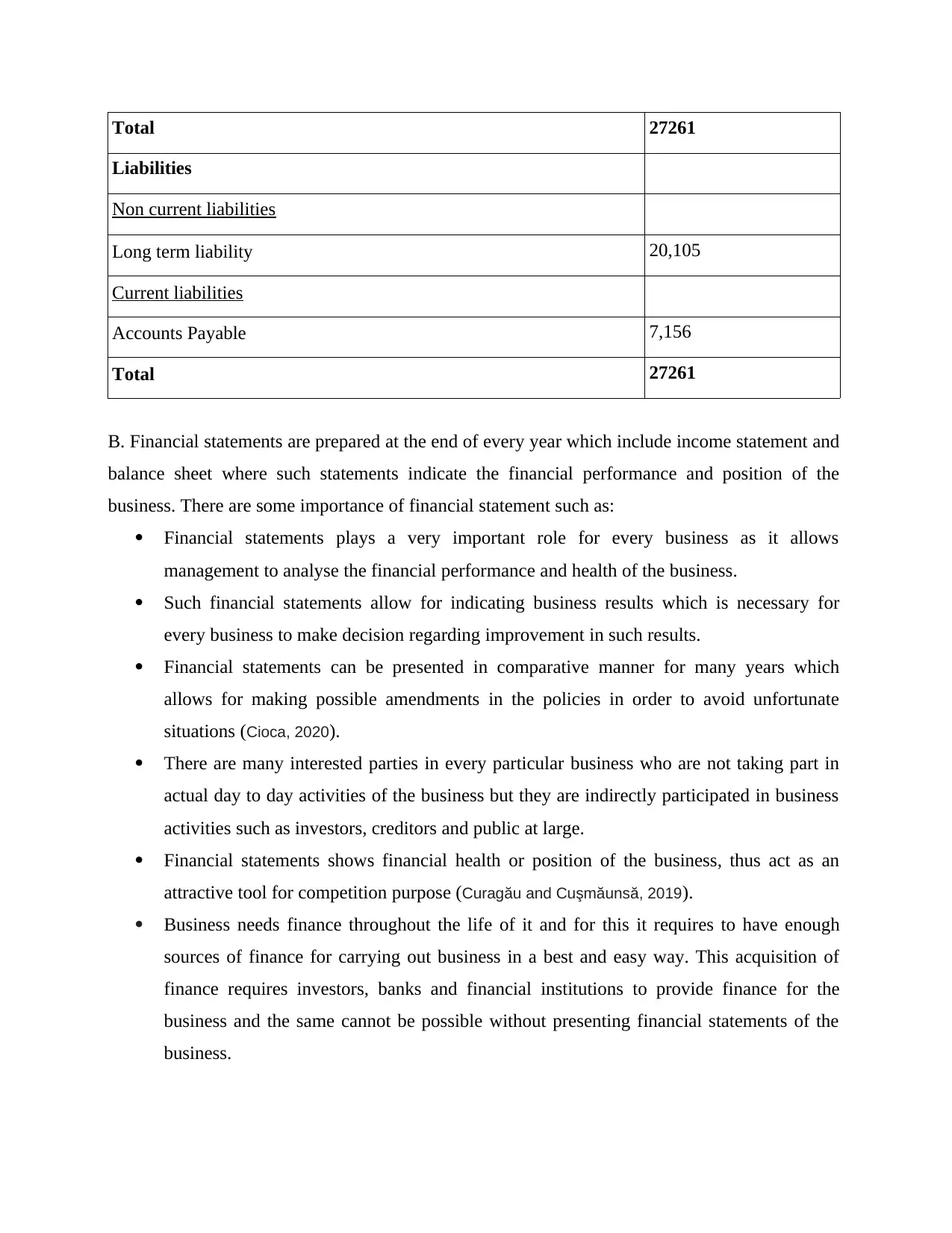

Total 27261

Liabilities

Non current liabilities

Long term liability 20,105

Current liabilities

Accounts Payable 7,156

Total 27261

B. Financial statements are prepared at the end of every year which include income statement and

balance sheet where such statements indicate the financial performance and position of the

business. There are some importance of financial statement such as:

Financial statements plays a very important role for every business as it allows

management to analyse the financial performance and health of the business.

Such financial statements allow for indicating business results which is necessary for

every business to make decision regarding improvement in such results.

Financial statements can be presented in comparative manner for many years which

allows for making possible amendments in the policies in order to avoid unfortunate

situations (Cioca, 2020).

There are many interested parties in every particular business who are not taking part in

actual day to day activities of the business but they are indirectly participated in business

activities such as investors, creditors and public at large.

Financial statements shows financial health or position of the business, thus act as an

attractive tool for competition purpose (Curagău and Cuşmăunsă, 2019).

Business needs finance throughout the life of it and for this it requires to have enough

sources of finance for carrying out business in a best and easy way. This acquisition of

finance requires investors, banks and financial institutions to provide finance for the

business and the same cannot be possible without presenting financial statements of the

business.

Liabilities

Non current liabilities

Long term liability 20,105

Current liabilities

Accounts Payable 7,156

Total 27261

B. Financial statements are prepared at the end of every year which include income statement and

balance sheet where such statements indicate the financial performance and position of the

business. There are some importance of financial statement such as:

Financial statements plays a very important role for every business as it allows

management to analyse the financial performance and health of the business.

Such financial statements allow for indicating business results which is necessary for

every business to make decision regarding improvement in such results.

Financial statements can be presented in comparative manner for many years which

allows for making possible amendments in the policies in order to avoid unfortunate

situations (Cioca, 2020).

There are many interested parties in every particular business who are not taking part in

actual day to day activities of the business but they are indirectly participated in business

activities such as investors, creditors and public at large.

Financial statements shows financial health or position of the business, thus act as an

attractive tool for competition purpose (Curagău and Cuşmăunsă, 2019).

Business needs finance throughout the life of it and for this it requires to have enough

sources of finance for carrying out business in a best and easy way. This acquisition of

finance requires investors, banks and financial institutions to provide finance for the

business and the same cannot be possible without presenting financial statements of the

business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cioca, I. C., 2020. The Importance Of Financial Statements In The Decision-Making Process.

Annales Universitatis Apulensis Series Oeconomica. 1(22). pp.73-83.

Curagău, N. and Cuşmăunsă, R., 2019. The importance of consolidated financial statements in

financial communication. In Competitivitatea şi inovarea în economia cunoaşterii. (pp.

467-472).

Question 3

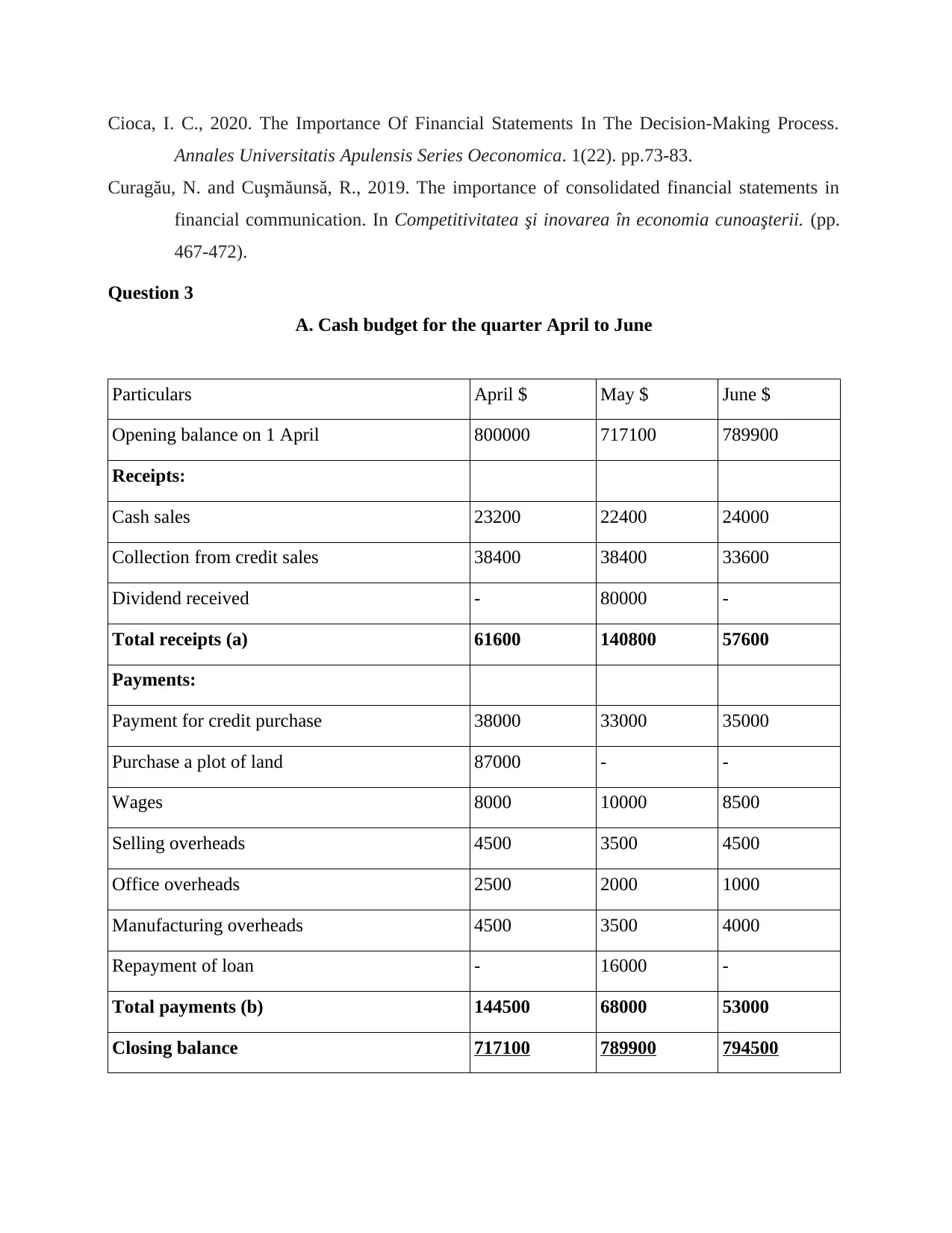

A. Cash budget for the quarter April to June

Particulars April $ May $ June $

Opening balance on 1 April 800000 717100 789900

Receipts:

Cash sales 23200 22400 24000

Collection from credit sales 38400 38400 33600

Dividend received - 80000 -

Total receipts (a) 61600 140800 57600

Payments:

Payment for credit purchase 38000 33000 35000

Purchase a plot of land 87000 - -

Wages 8000 10000 8500

Selling overheads 4500 3500 4500

Office overheads 2500 2000 1000

Manufacturing overheads 4500 3500 4000

Repayment of loan - 16000 -

Total payments (b) 144500 68000 53000

Closing balance 717100 789900 794500

Annales Universitatis Apulensis Series Oeconomica. 1(22). pp.73-83.

Curagău, N. and Cuşmăunsă, R., 2019. The importance of consolidated financial statements in

financial communication. In Competitivitatea şi inovarea în economia cunoaşterii. (pp.

467-472).

Question 3

A. Cash budget for the quarter April to June

Particulars April $ May $ June $

Opening balance on 1 April 800000 717100 789900

Receipts:

Cash sales 23200 22400 24000

Collection from credit sales 38400 38400 33600

Dividend received - 80000 -

Total receipts (a) 61600 140800 57600

Payments:

Payment for credit purchase 38000 33000 35000

Purchase a plot of land 87000 - -

Wages 8000 10000 8500

Selling overheads 4500 3500 4500

Office overheads 2500 2000 1000

Manufacturing overheads 4500 3500 4000

Repayment of loan - 16000 -

Total payments (b) 144500 68000 53000

Closing balance 717100 789900 794500

B. Zero-based budgeting involves budget preparation from zero level where each and every item

of the budget are justified before taking them into budgets for every new period. These items are

justified in terms of their utilities and costs. The budget is then prepared for the future period

without considering that whether the budget is more or less than the period before. Under this

items of the budget are evaluated in terms of their costs for the business and how much revenue

can be generated from these items. Such technique of budgeting helps the management to

concentrate on those areas which are helpful in growth and profitability of the business.

Management can answer to questions like what activities and how such activities to be performed

so that both efficiency and effectiveness can be achieved (Ibrahim, 2019). So that the business

can be able to generate more revenues with lower costs. Zero-based budgeting allows for

probable changes in the budget by considering the time factor and changes in the market. Only

those items are included which are necessary for running the operations of the business by cutting

costs associated with unnecessary expenditures. Such technique is helpful in avoiding

incremental budgeting as in the case of traditional budgeting where budgets are made by

increasing and decreasing some percentage of the amounts in the previous budget. Zero-based

budgeting takes into consideration all the important changes in the business environment and

situations by preparing it with zero base (Hardin, 2018.). The biggest advantage of this budgeting

technique is that it improves financial performance, operating efficiency through cost reduction.

Although it may be considered as the disadvantage of this technique that it is quite costly and

time consuming affair and required higher level of expertise and qualified personnel.

Ibrahim, M. M., 2019. Designing zero-based budgeting for public organizations. Problems and

Perspectives in Management. 17(2).

Hardin, M., 2018. Zero-base Budgeting.

Question 5

A. 1. Calculation of contribution margin per unit

Sales price (SP) per unit = $250

Variable cost (VC) per unit = $100

Contribution Margin per unit = SP – VC

of the budget are justified before taking them into budgets for every new period. These items are

justified in terms of their utilities and costs. The budget is then prepared for the future period

without considering that whether the budget is more or less than the period before. Under this

items of the budget are evaluated in terms of their costs for the business and how much revenue

can be generated from these items. Such technique of budgeting helps the management to

concentrate on those areas which are helpful in growth and profitability of the business.

Management can answer to questions like what activities and how such activities to be performed

so that both efficiency and effectiveness can be achieved (Ibrahim, 2019). So that the business

can be able to generate more revenues with lower costs. Zero-based budgeting allows for

probable changes in the budget by considering the time factor and changes in the market. Only

those items are included which are necessary for running the operations of the business by cutting

costs associated with unnecessary expenditures. Such technique is helpful in avoiding

incremental budgeting as in the case of traditional budgeting where budgets are made by

increasing and decreasing some percentage of the amounts in the previous budget. Zero-based

budgeting takes into consideration all the important changes in the business environment and

situations by preparing it with zero base (Hardin, 2018.). The biggest advantage of this budgeting

technique is that it improves financial performance, operating efficiency through cost reduction.

Although it may be considered as the disadvantage of this technique that it is quite costly and

time consuming affair and required higher level of expertise and qualified personnel.

Ibrahim, M. M., 2019. Designing zero-based budgeting for public organizations. Problems and

Perspectives in Management. 17(2).

Hardin, M., 2018. Zero-base Budgeting.

Question 5

A. 1. Calculation of contribution margin per unit

Sales price (SP) per unit = $250

Variable cost (VC) per unit = $100

Contribution Margin per unit = SP – VC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 250-100 = $150

2. Calculation of contribution margin ratio

SP = $250 per unit

Contribution Margin per unit = $150

Contribution Margin ratio = Contribution Margin per unit/ SP per unit * 100

= $150/ $250 * 100 = 60%

3. BEP in units

Fixed cost = $56000

Contribution Margin per unit = $150

BEP in units = Fixed cost / Contribution margin per unit

= $56000 / $150 = 373 units.

4. BEP in sales

SP per unit = $250

Contribution margin / unit = $150

Total fixed cost = $56000

BEP in sales = SP per unit / contribution margin per unit * Total fixed cost

= $250/ $150 * $56000 = $93333.

B. Cost behaviour analysis refers to the technique used by the managers or management of the

company who usually carries out studies to understand the behaviour of total cost with the change

in level of production or activity. It requires qualified personnel with enough experience and

expertise who cannot just able to understand the behaviour of costs associated with the activity

but also be able to understand or mention the reason of such behaviour. For example they can be

able to categorise cost on the basis of variability in level of activity because fixed cost are such

which remains the same at all level of activity of production while on the other hand variable

costs keep changing with every change in the level of production, like direct material, direct

labour and direct overheads which are considered to be the direct costs associated with the

production and changes with every change in number of units (Drury, 2018). Here managers tries

to understand and analyse the relationship between various drivers of costs and the total cost.

2. Calculation of contribution margin ratio

SP = $250 per unit

Contribution Margin per unit = $150

Contribution Margin ratio = Contribution Margin per unit/ SP per unit * 100

= $150/ $250 * 100 = 60%

3. BEP in units

Fixed cost = $56000

Contribution Margin per unit = $150

BEP in units = Fixed cost / Contribution margin per unit

= $56000 / $150 = 373 units.

4. BEP in sales

SP per unit = $250

Contribution margin / unit = $150

Total fixed cost = $56000

BEP in sales = SP per unit / contribution margin per unit * Total fixed cost

= $250/ $150 * $56000 = $93333.

B. Cost behaviour analysis refers to the technique used by the managers or management of the

company who usually carries out studies to understand the behaviour of total cost with the change

in level of production or activity. It requires qualified personnel with enough experience and

expertise who cannot just able to understand the behaviour of costs associated with the activity

but also be able to understand or mention the reason of such behaviour. For example they can be

able to categorise cost on the basis of variability in level of activity because fixed cost are such

which remains the same at all level of activity of production while on the other hand variable

costs keep changing with every change in the level of production, like direct material, direct

labour and direct overheads which are considered to be the direct costs associated with the

production and changes with every change in number of units (Drury, 2018). Here managers tries

to understand and analyse the relationship between various drivers of costs and the total cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managers get aids in understanding the areas which are causing the overall costs to be higher.

Manager can plan for further expansion through cost behaviour analysis. Cost behaviour analysis

also facilitates examination and effect of cost and volume on the profits of the company. It is

always helpful in carrying out better planning and controlling in the business. Cost behaviour can

be categorised in three types, that is fixed, variable and semi variable which behaves differently

with the change in business level of activity (Azeez, DongPing and Mahmood, 2018). At last, cost

behaviour analysis is considered to be the most important study in accounting for achieving

operating efficiency and improving profitability of the business but it requires manager's ability

too towards application of such conceptual behaviour in the real world business arena which

behaves quite differently.

Drury, C., 2018. Cost and management accounting. Cengage Learning.

Azeez, K. A., DongPing, H. and Mahmood, M. A., 2018. Capacity expansion decisions into

asymmetric cost behaviour: reviews and search for new determinants. International

Journal of Services Operations and Informatics. 9(2). pp.139-159.

Manager can plan for further expansion through cost behaviour analysis. Cost behaviour analysis

also facilitates examination and effect of cost and volume on the profits of the company. It is

always helpful in carrying out better planning and controlling in the business. Cost behaviour can

be categorised in three types, that is fixed, variable and semi variable which behaves differently

with the change in business level of activity (Azeez, DongPing and Mahmood, 2018). At last, cost

behaviour analysis is considered to be the most important study in accounting for achieving

operating efficiency and improving profitability of the business but it requires manager's ability

too towards application of such conceptual behaviour in the real world business arena which

behaves quite differently.

Drury, C., 2018. Cost and management accounting. Cengage Learning.

Azeez, K. A., DongPing, H. and Mahmood, M. A., 2018. Capacity expansion decisions into

asymmetric cost behaviour: reviews and search for new determinants. International

Journal of Services Operations and Informatics. 9(2). pp.139-159.

QUESTION 6

A. Calculation of EOQ for APEX Inc.

Annual Demand (A) = 90000 units

Cost of placing order (O) = $30

Carrying cost per unit (C)= $9

EOQ = sqrt(2* A* O)/ C

= sqrt (2 * 90000 * 30) / 9

= sqrt (5400000) / 9

= sqrt 600000

= 774 units.

B. Calculation of average inventory when safety stock is 2000 units

Average inventory = EOQ / 2 + Safety Stock (SS)

= 774 / 2 + 2000

= 387 + 2000 = 2387 units.

C. Maintaining Inventory records, physical counting of goods and chances of occurring errors

Physical recording method of stock valuation is a prominent approach to record the stock

in company's books of accounts. Under this approach physical calculation and valuation is done

over the stock available in the company's warehouse in the end of the financial year. Physical

verification and valuation is done by the employee delegated the respective position in the stock

department of company. Physical counting is an effective approach as it also help to resist the

corruption in the stock counting (Adamska and Szewczuk-Stepien, 2020). This method of stock

valuation improve authenticity in the overall value of stock. Along with all the advantage this

method also lead to error in physical counting of number of units available in stock. Many times'

employee do not get to focus over the work that also lead to wrong counting and valuation of

stock. Many times errors are done due top motive of the employee and also many times it also

entertains without any motive (Rossi, Pozzi and Testa, 2017). Many times in order to improve the

value of closing stock management might intervene in the overall counting of stock. This

unethical practice might mislead the overall results against the stock valuation method.

A. Calculation of EOQ for APEX Inc.

Annual Demand (A) = 90000 units

Cost of placing order (O) = $30

Carrying cost per unit (C)= $9

EOQ = sqrt(2* A* O)/ C

= sqrt (2 * 90000 * 30) / 9

= sqrt (5400000) / 9

= sqrt 600000

= 774 units.

B. Calculation of average inventory when safety stock is 2000 units

Average inventory = EOQ / 2 + Safety Stock (SS)

= 774 / 2 + 2000

= 387 + 2000 = 2387 units.

C. Maintaining Inventory records, physical counting of goods and chances of occurring errors

Physical recording method of stock valuation is a prominent approach to record the stock

in company's books of accounts. Under this approach physical calculation and valuation is done

over the stock available in the company's warehouse in the end of the financial year. Physical

verification and valuation is done by the employee delegated the respective position in the stock

department of company. Physical counting is an effective approach as it also help to resist the

corruption in the stock counting (Adamska and Szewczuk-Stepien, 2020). This method of stock

valuation improve authenticity in the overall value of stock. Along with all the advantage this

method also lead to error in physical counting of number of units available in stock. Many times'

employee do not get to focus over the work that also lead to wrong counting and valuation of

stock. Many times errors are done due top motive of the employee and also many times it also

entertains without any motive (Rossi, Pozzi and Testa, 2017). Many times in order to improve the

value of closing stock management might intervene in the overall counting of stock. This

unethical practice might mislead the overall results against the stock valuation method.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.