Accounting and Financial Reporting Homework: Superstore Ltd

VerifiedAdded on 2023/03/17

|17

|1146

|85

Homework Assignment

AI Summary

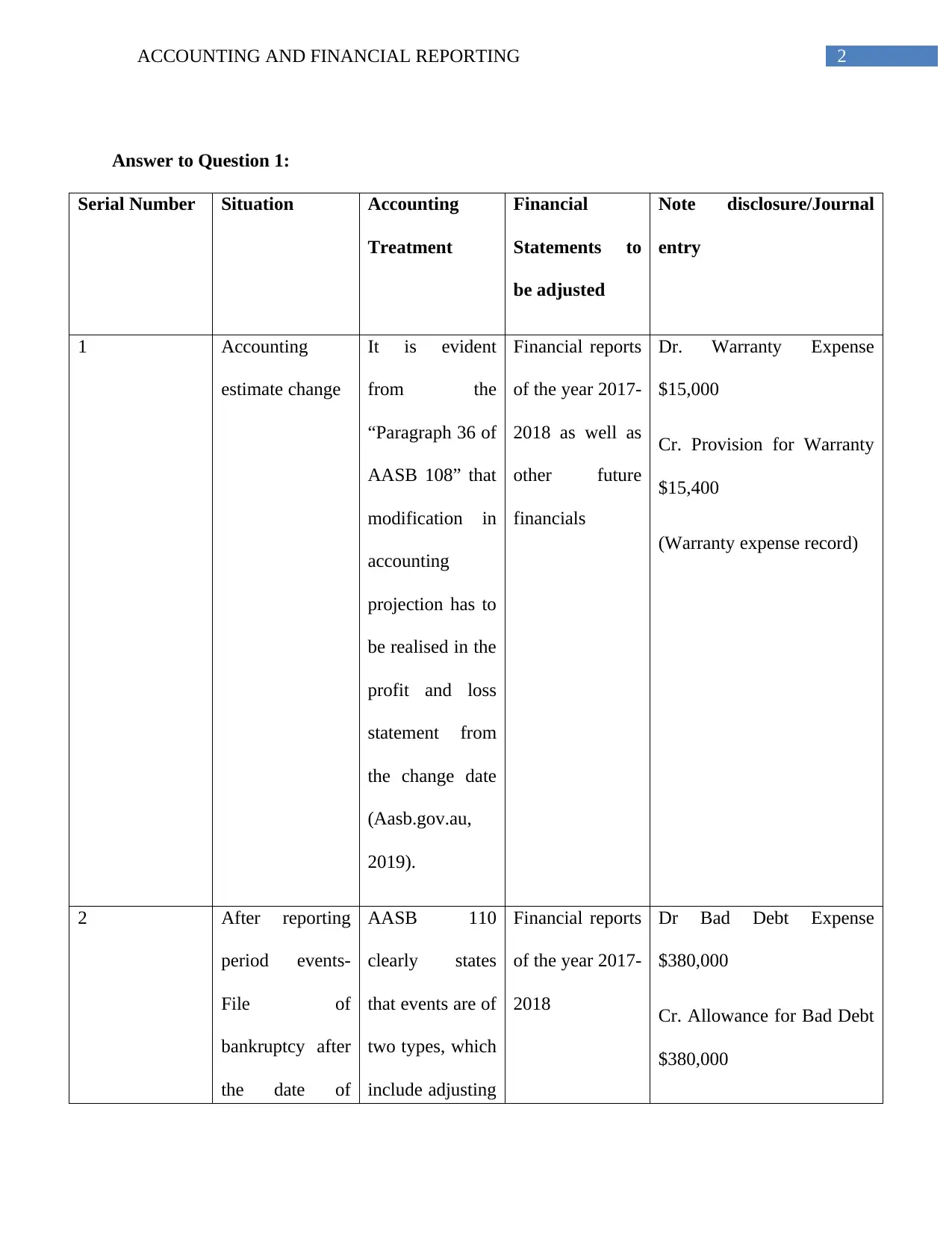

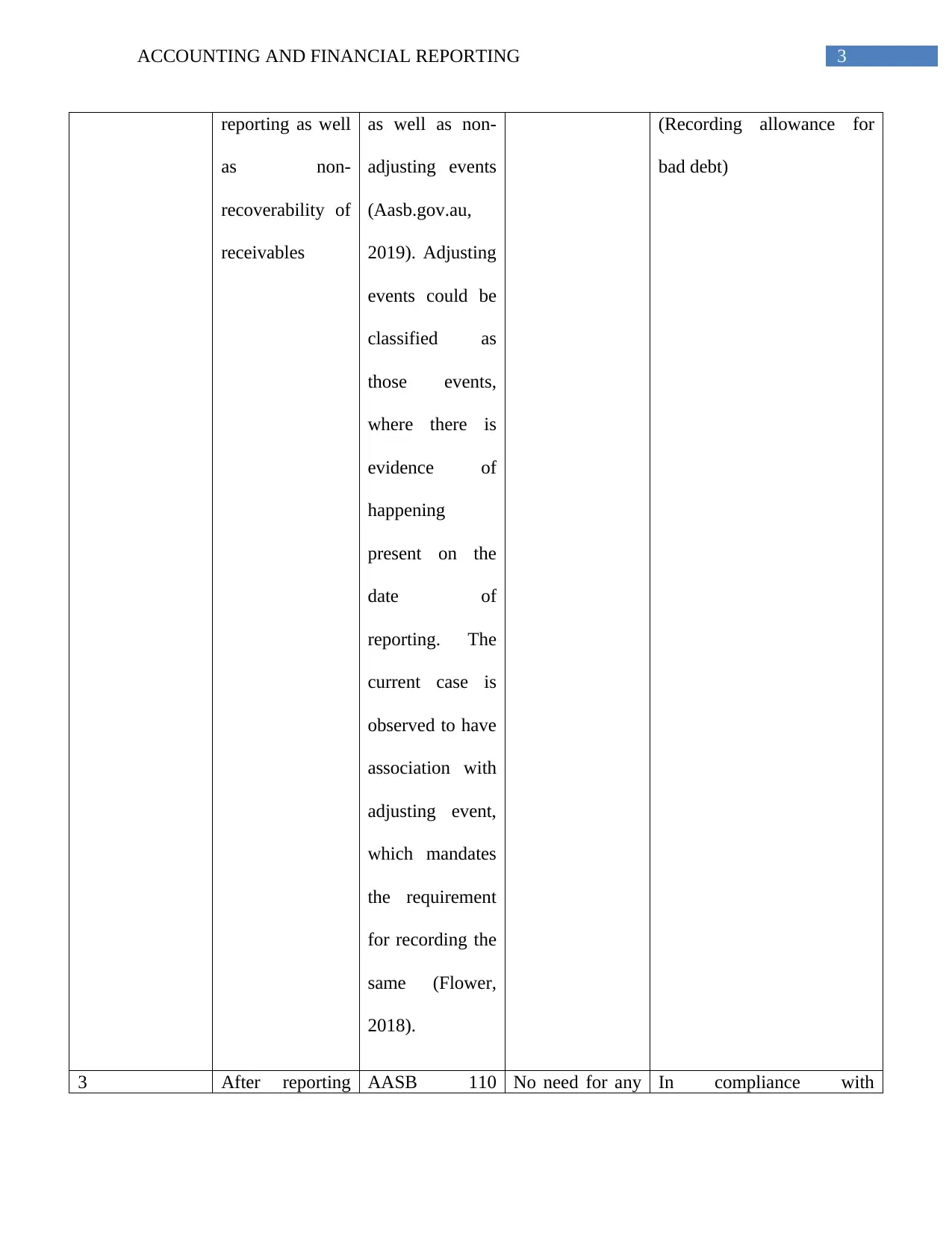

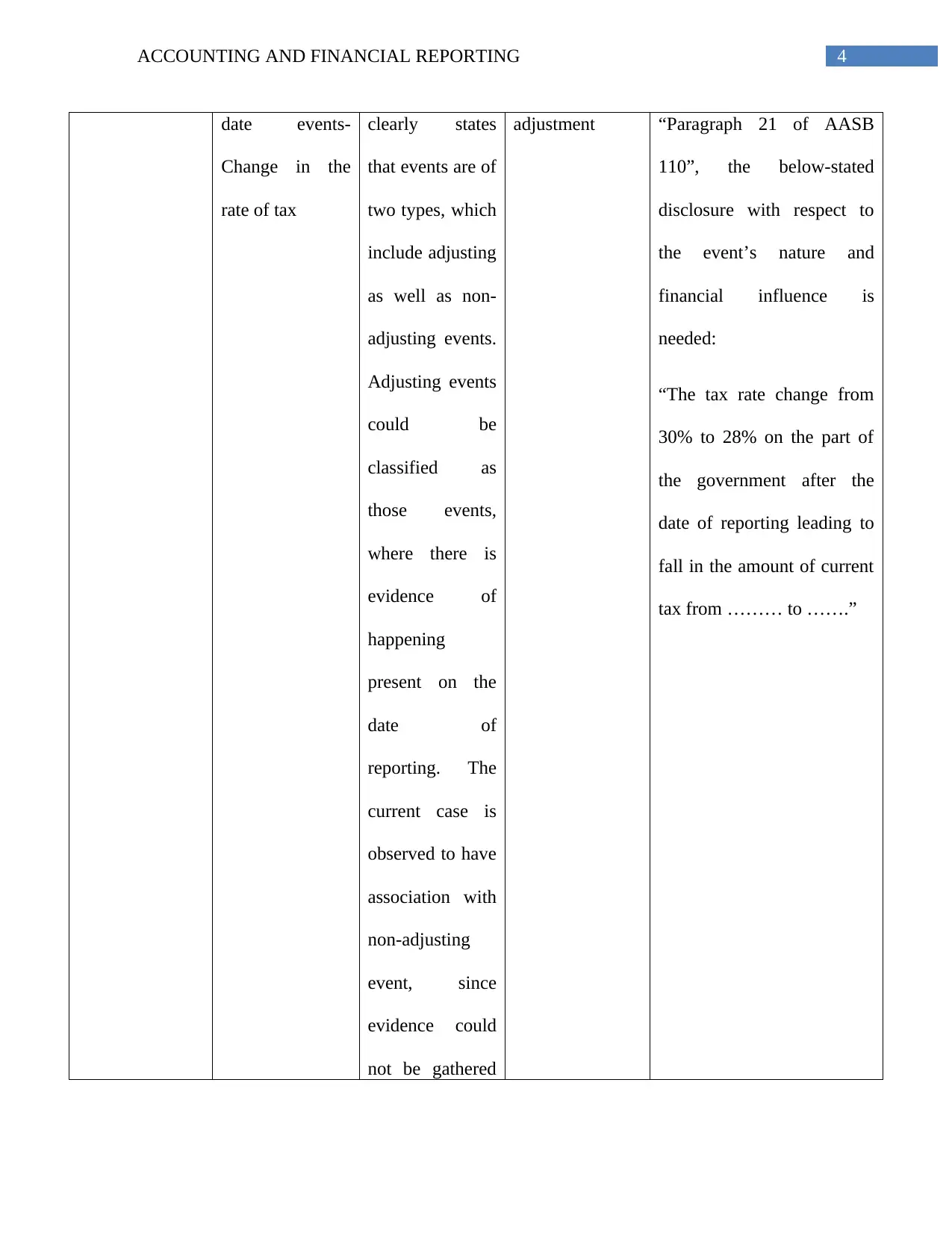

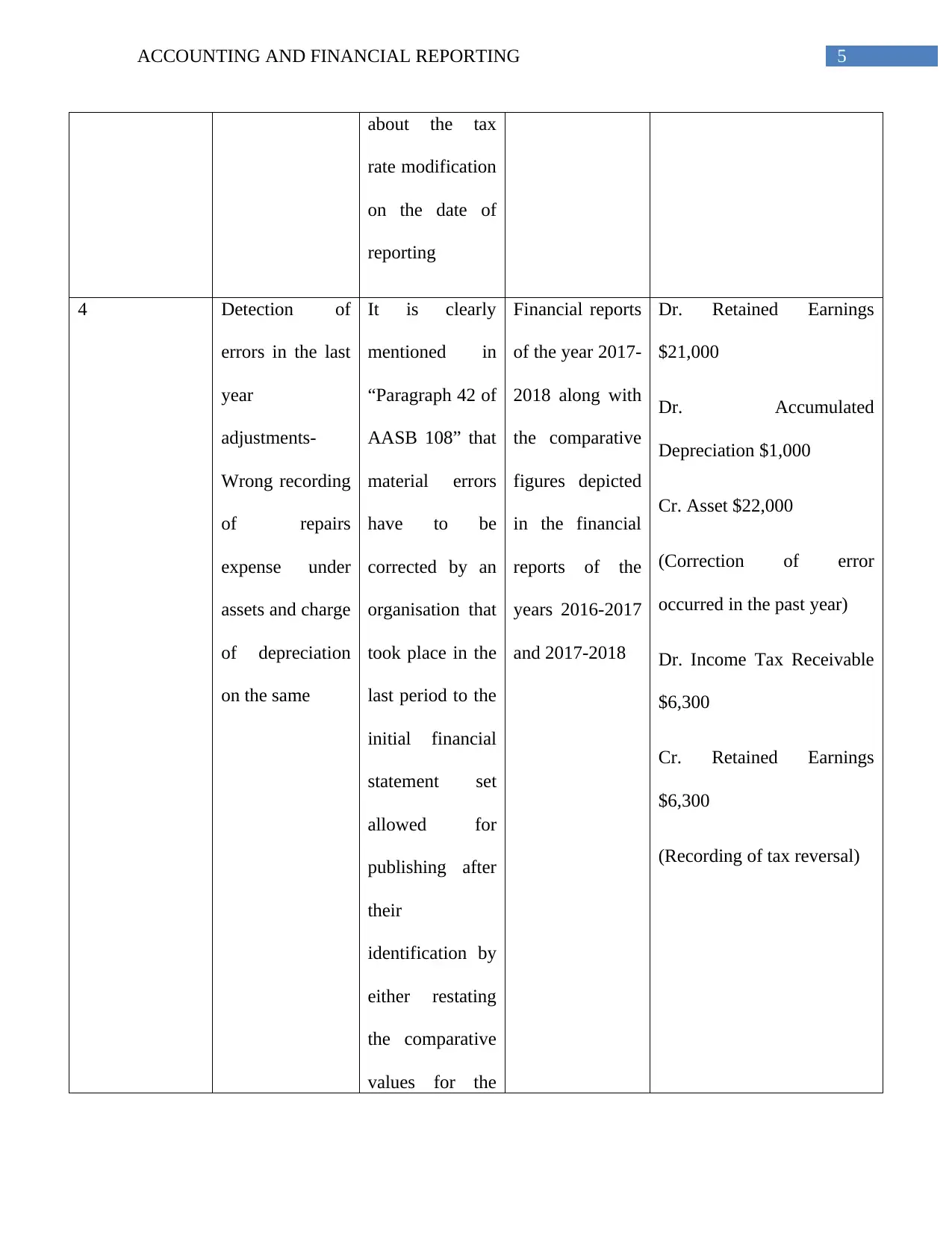

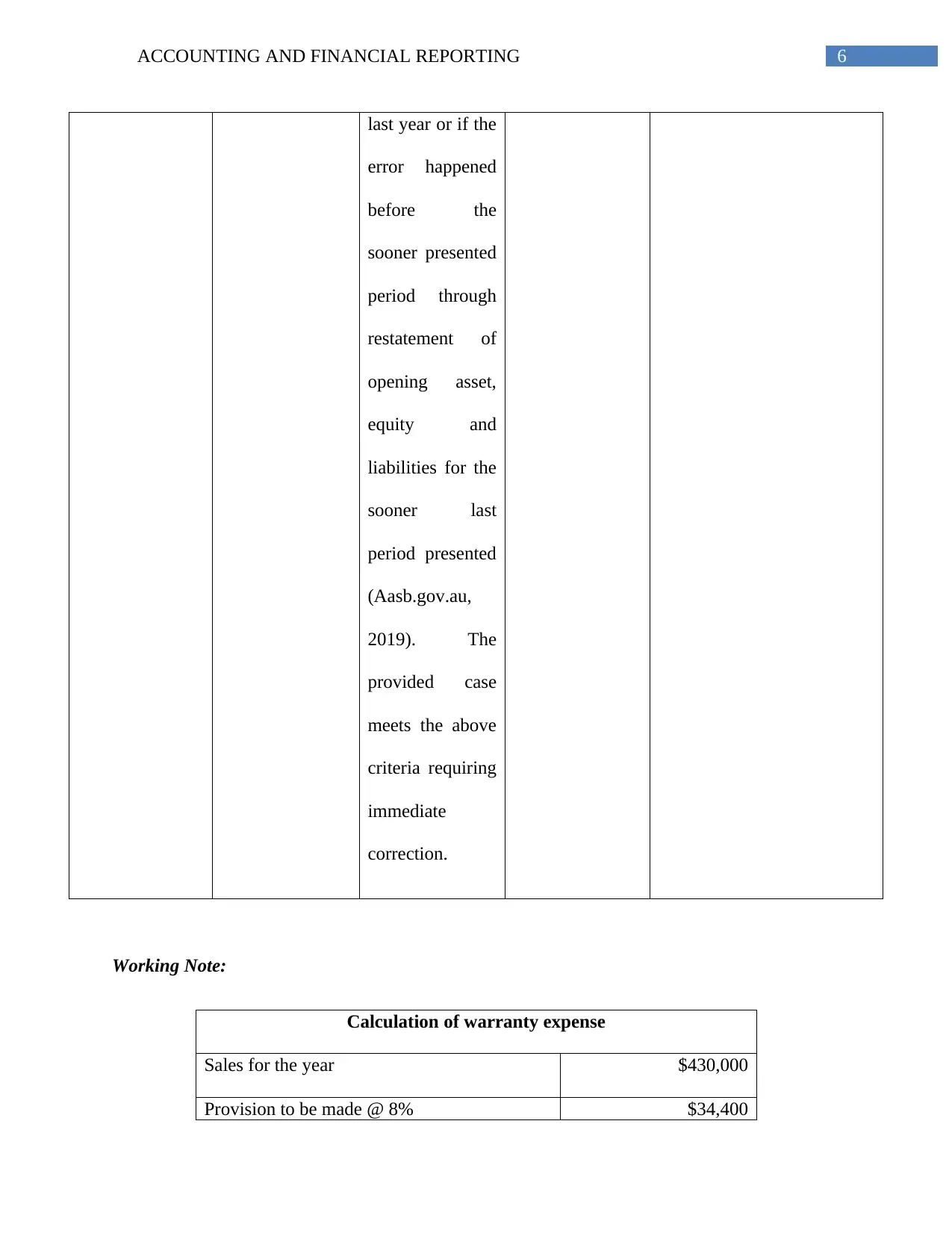

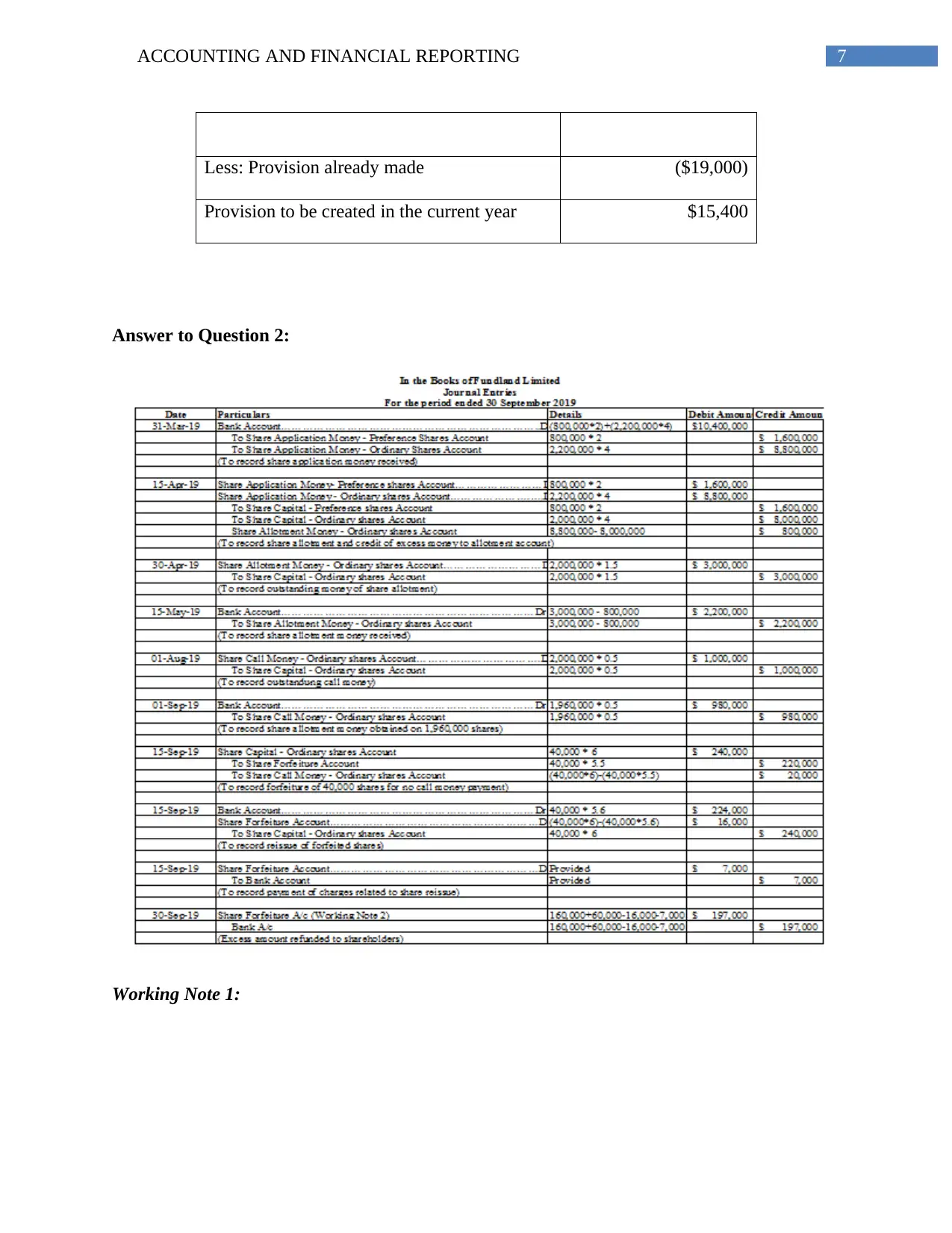

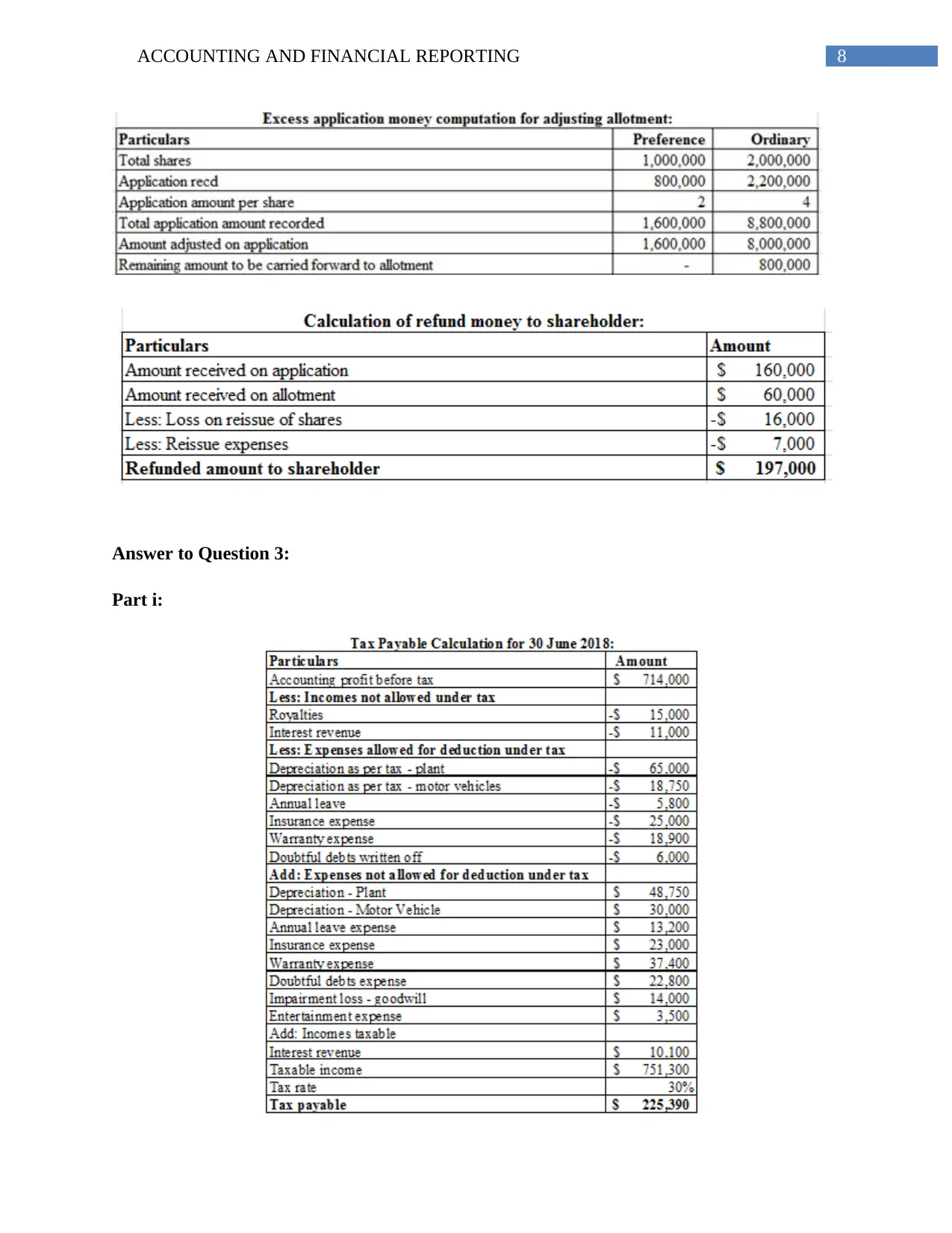

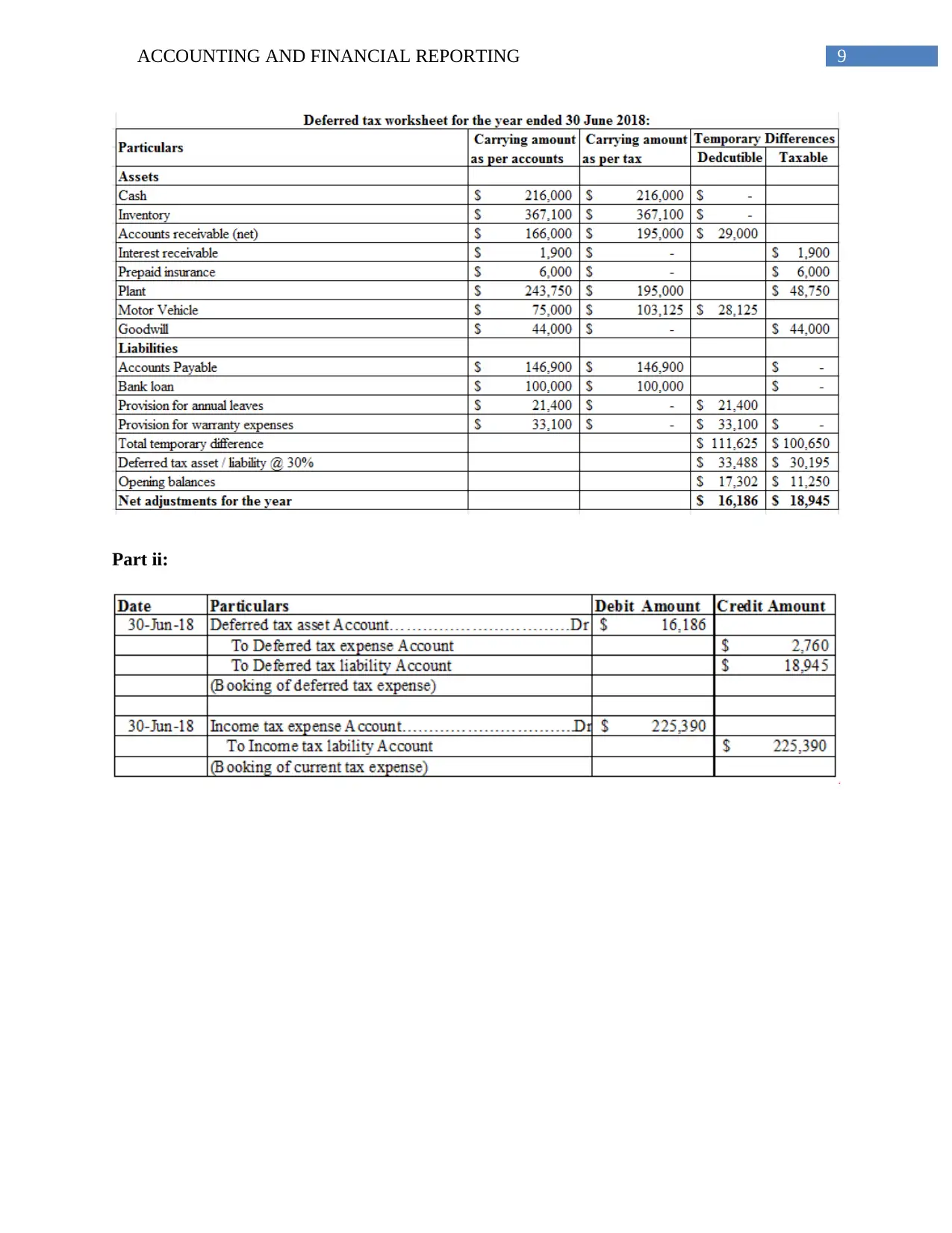

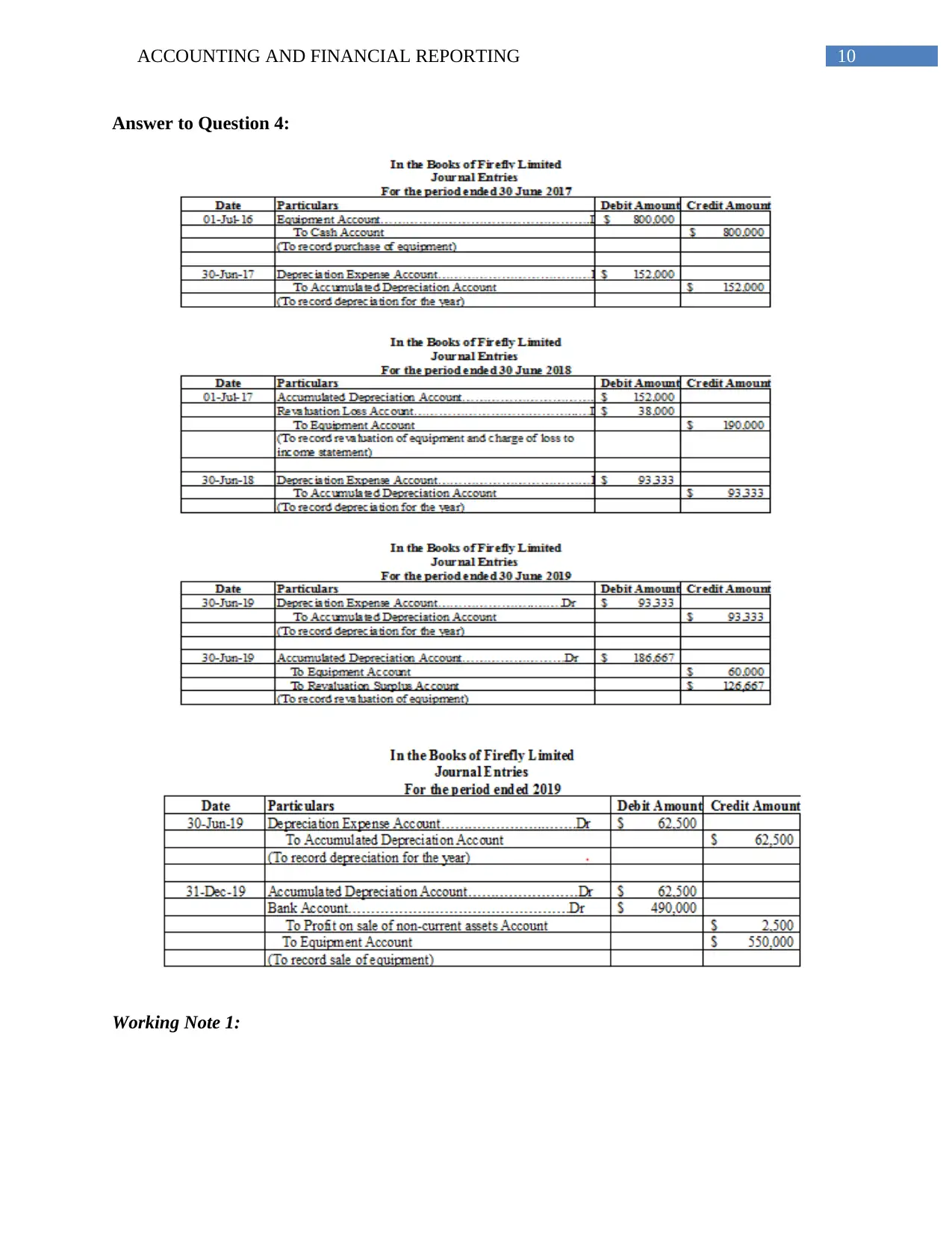

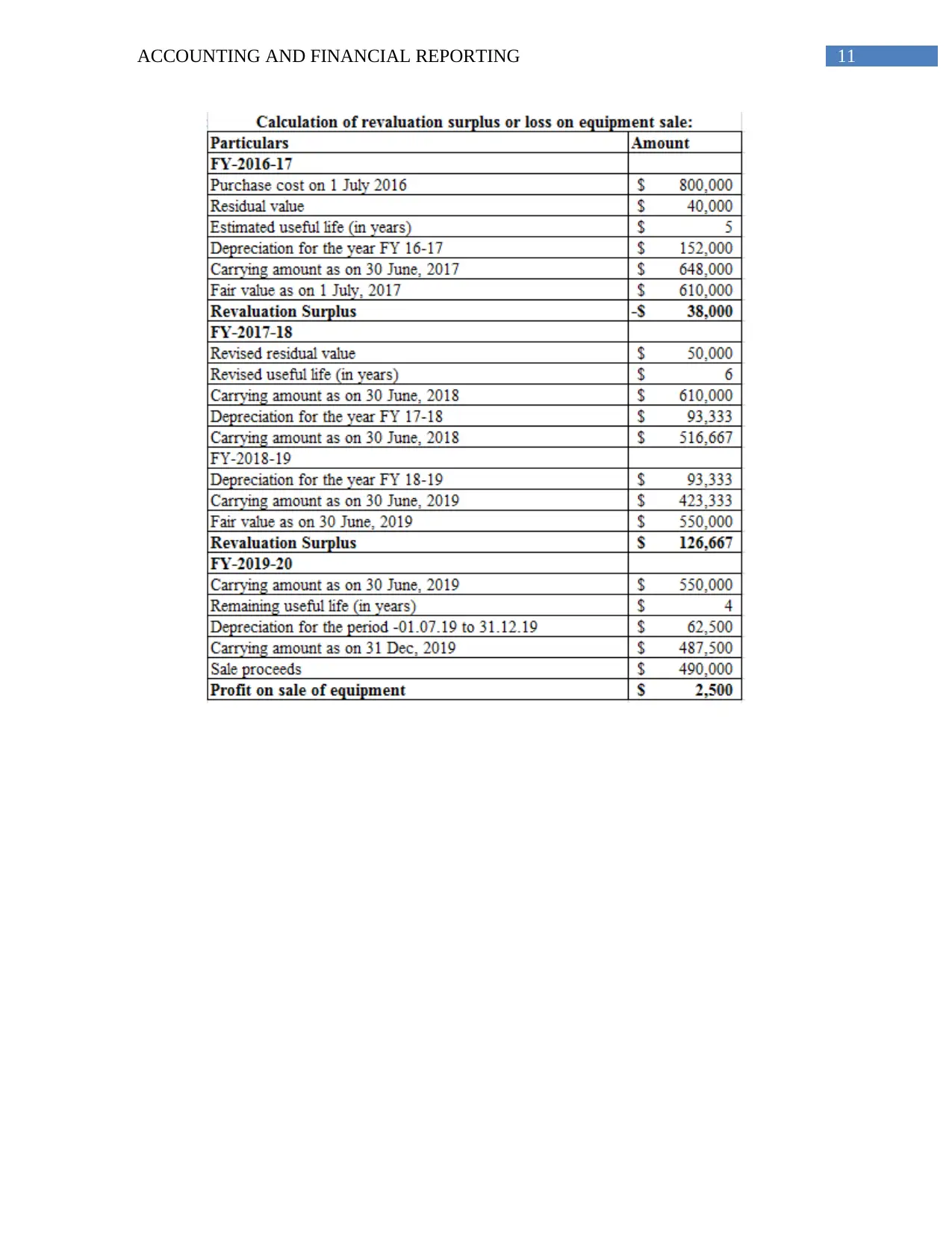

This document presents a complete solution to an accounting and financial reporting assignment, addressing five key questions related to financial statement disclosures, warranty provisions, after-reporting date events, and impairment losses. The solution includes detailed journal entries, working notes, and calculations to support the answers. Question 1 focuses on financial statement disclosures, including the adjustment of warranty provisions and the treatment of after-reporting date events. Question 2 provides working notes and calculations. Question 3 involves the preparation of financial statements. Question 4 covers the detection and correction of errors. Finally, Question 5 addresses the measurement of assets at fair values, the allocation of impairment losses, and the reversal of impairment losses in accordance with AASB standards. The assignment provides a practical application of accounting principles and financial reporting standards. This assignment is contributed by a student to be published on the website Desklib. Desklib is a platform which provides all the necessary AI based study tools for students.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.