University Accounting Principles Assignment - Semester 1

VerifiedAdded on 2021/04/24

|20

|1397

|43

Homework Assignment

AI Summary

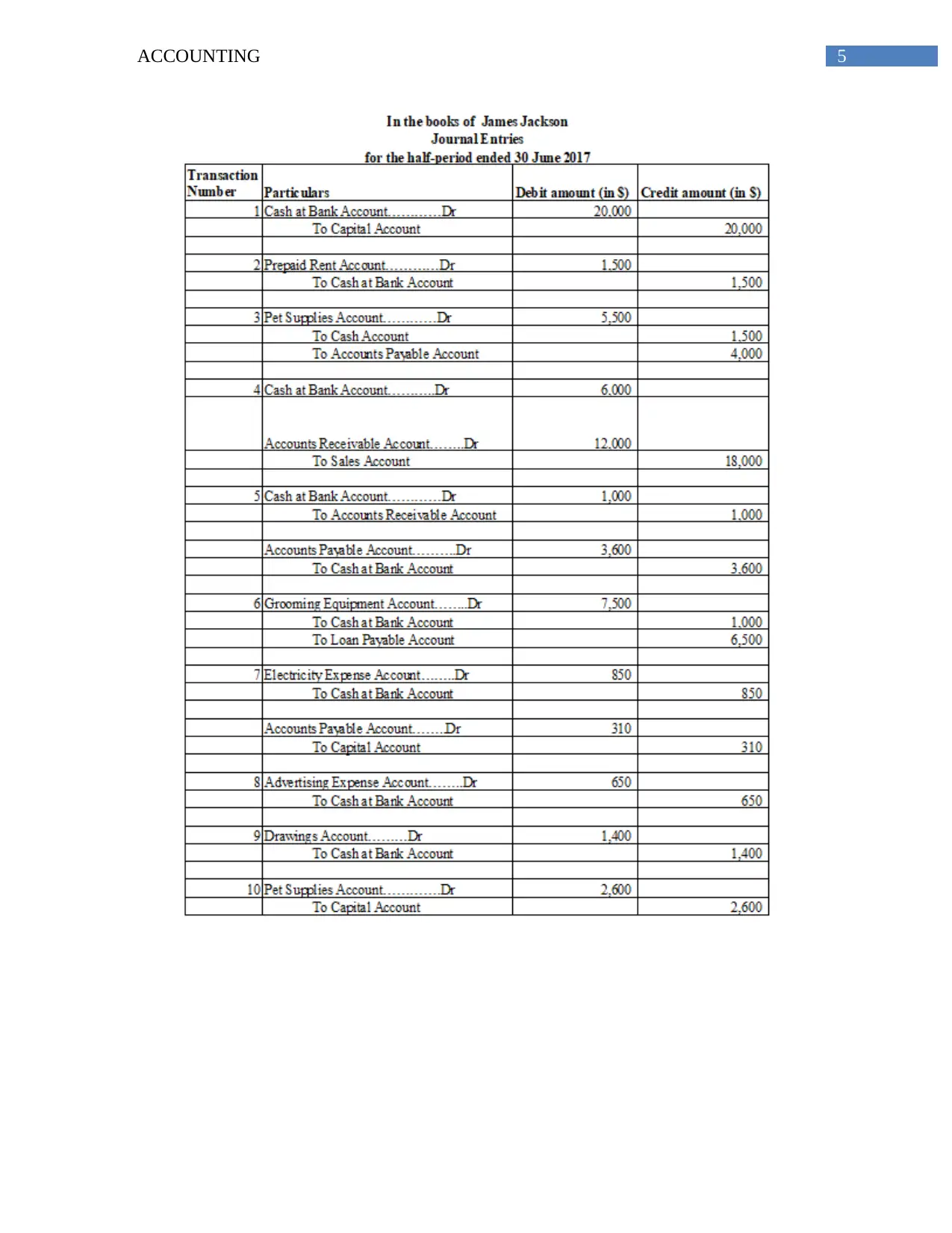

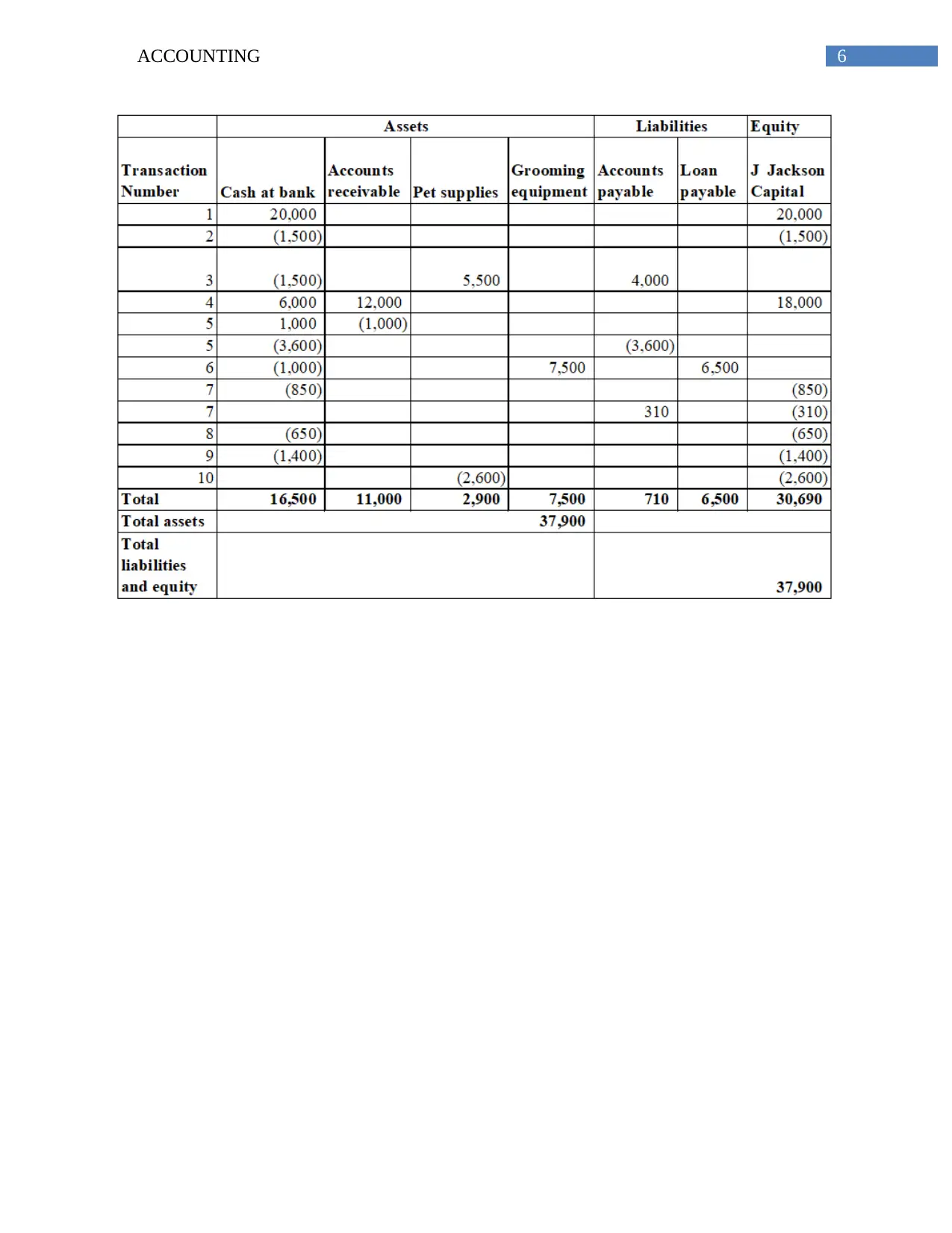

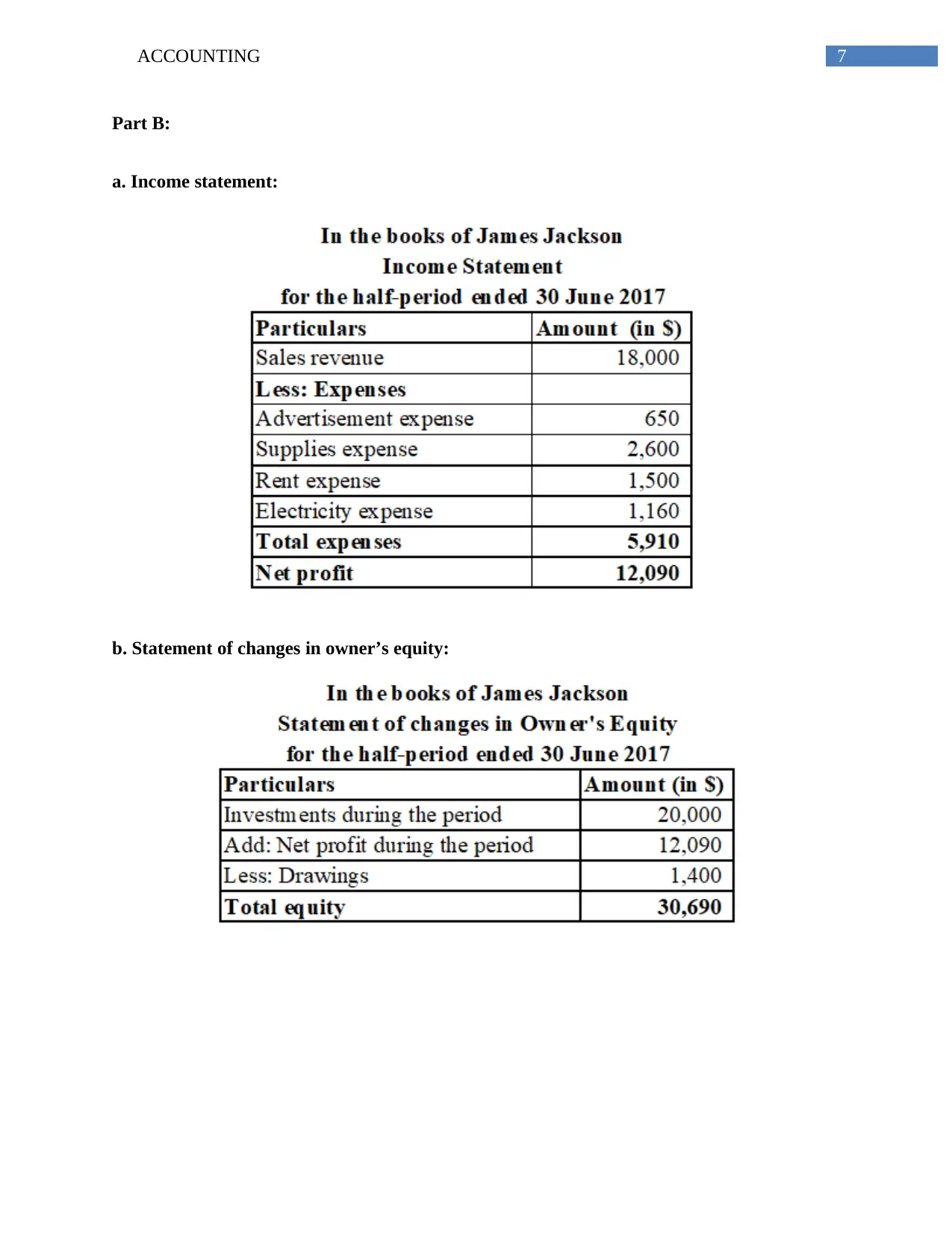

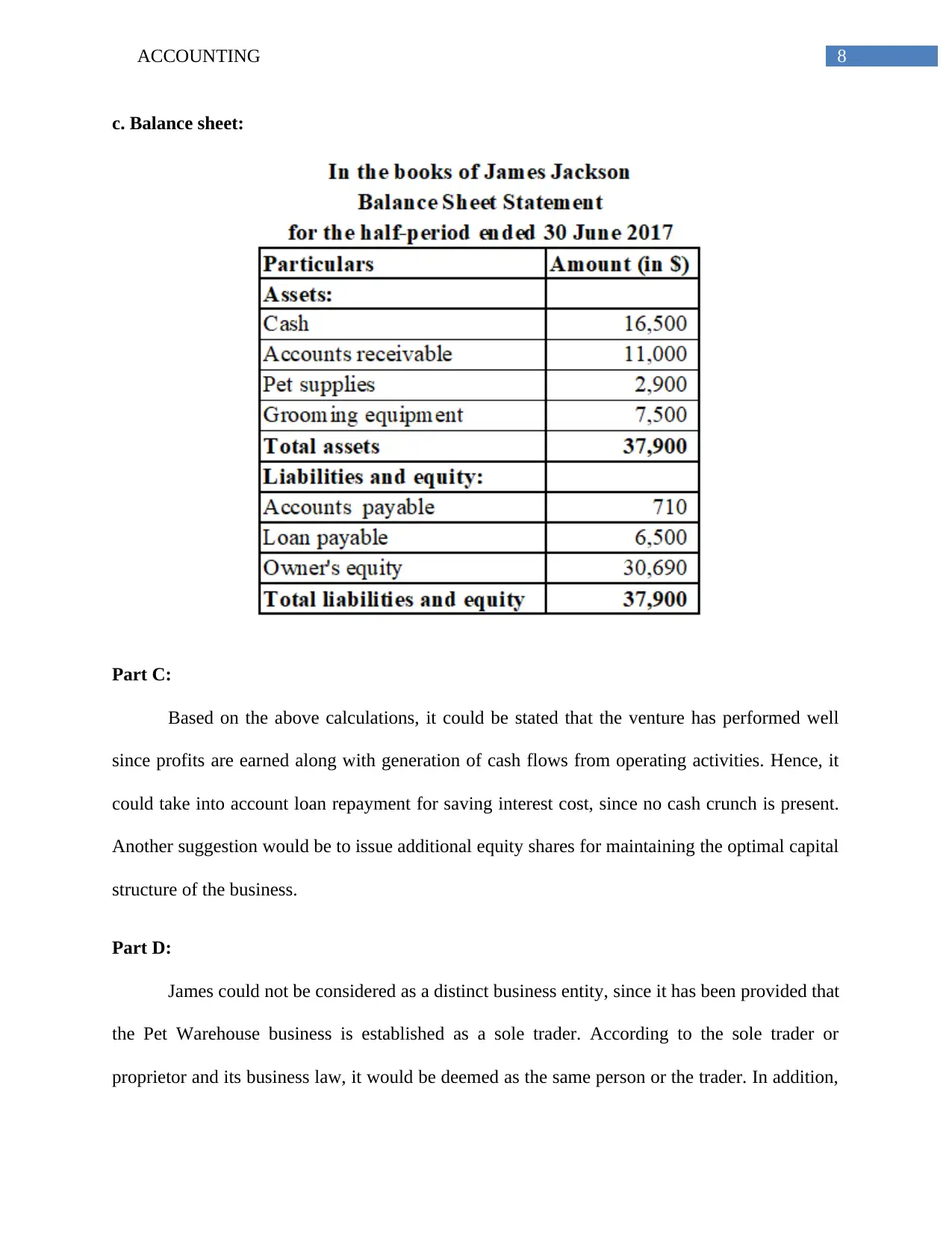

This accounting assignment solution addresses key concepts in financial accounting. It begins by differentiating between economic and non-economic decisions, illustrated with examples from various business scenarios, including production management, non-profit organizations, and small businesses. The solution then provides a detailed analysis of financial statements, including journal entries, income statements, statements of changes in owner’s equity, and balance sheets, along with recommendations for business performance improvement. The assignment also explores the legal and operational differences between sole traders and distinct business entities. Furthermore, it covers trial balance adjustments and potential accounting errors. Finally, the assignment delves into corporate social responsibility and ethical issues, particularly the debate surrounding health warnings on cigarette packs, providing a nuanced perspective on stakeholder interests and ethical decision-making.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.