Managerial Accounting Assignment Solution - University Name

VerifiedAdded on 2022/09/18

|9

|990

|22

Homework Assignment

AI Summary

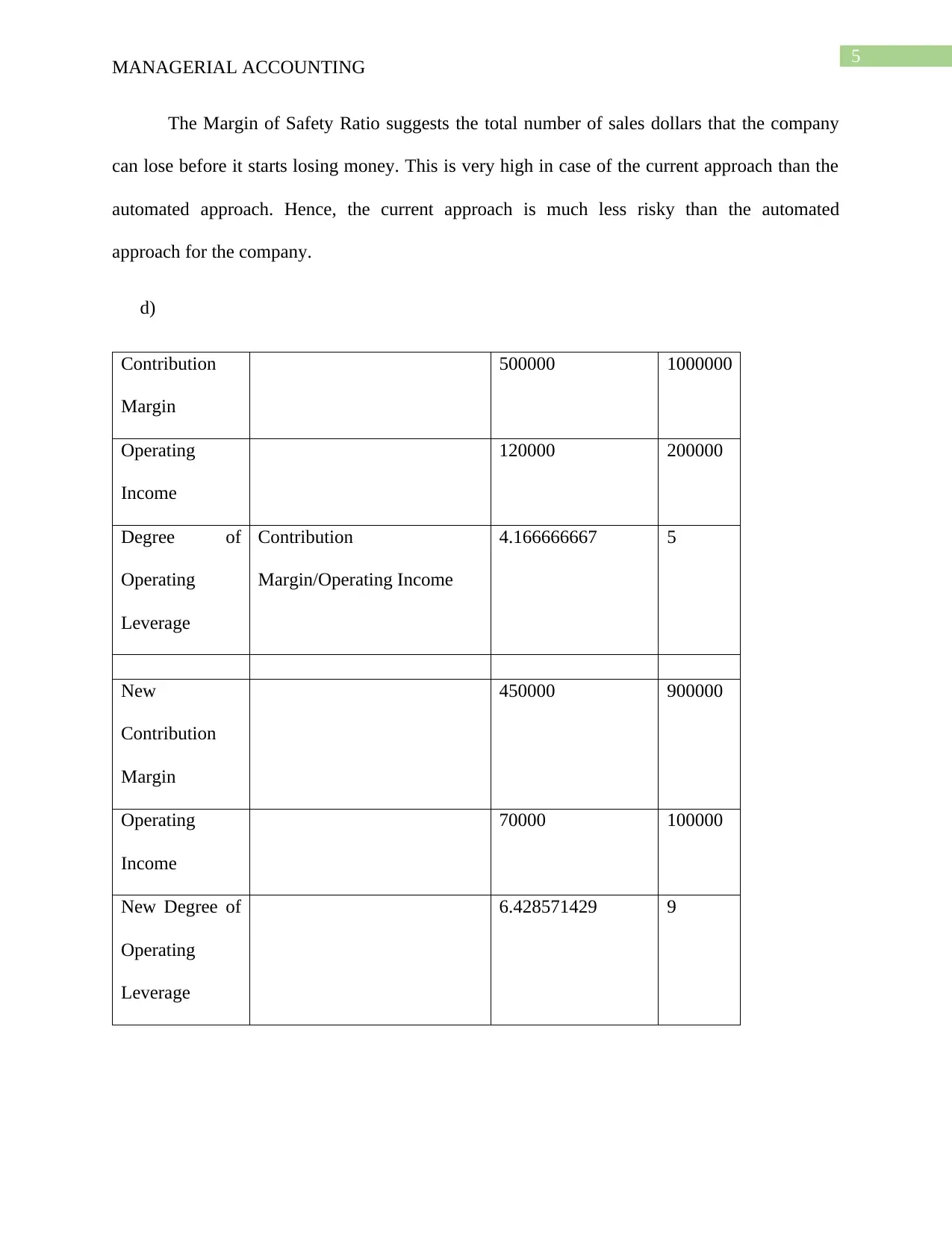

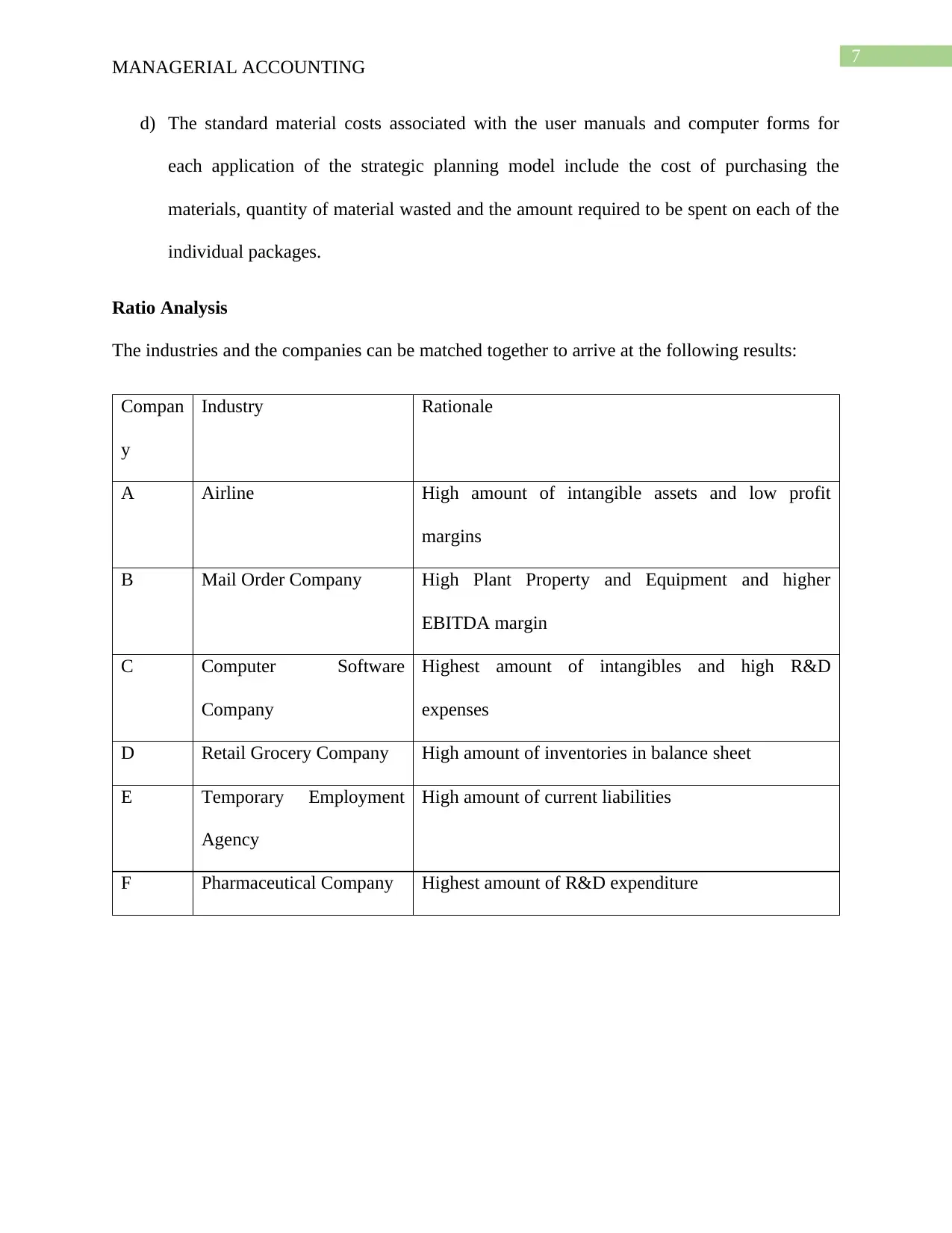

This managerial accounting assignment solution addresses various key concepts within the field. It begins with cost accounting, calculating overhead allocation using both traditional and activity-based costing methods. The solution proceeds to incremental analysis, assessing the profitability of different purchasing and manufacturing options. It then delves into cost-volume-profit (CVP) analysis, comparing the current and automated approaches, including breakeven points, margin of safety, and operating leverage. Standard costs are explored, focusing on determining labor hour standards and material costs. Finally, the assignment includes ratio analysis, matching companies with their respective industries based on financial characteristics. The assignment also provides answers to multiple-choice questions related to cost accounting and equivalent units of production.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.