Introduction to Accounting Practices Homework Assignment Solution

VerifiedAdded on 2022/10/08

|19

|1714

|15

Homework Assignment

AI Summary

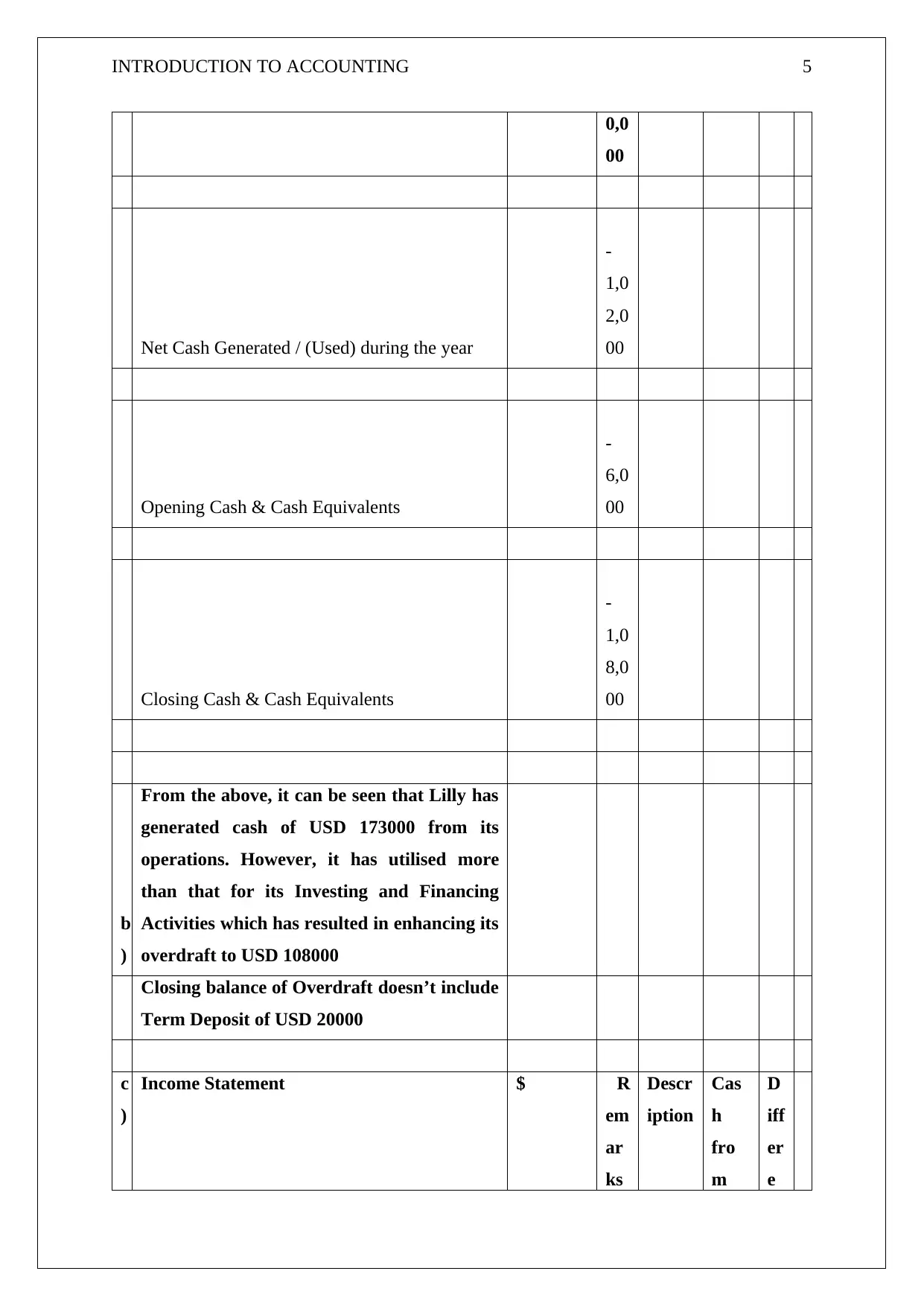

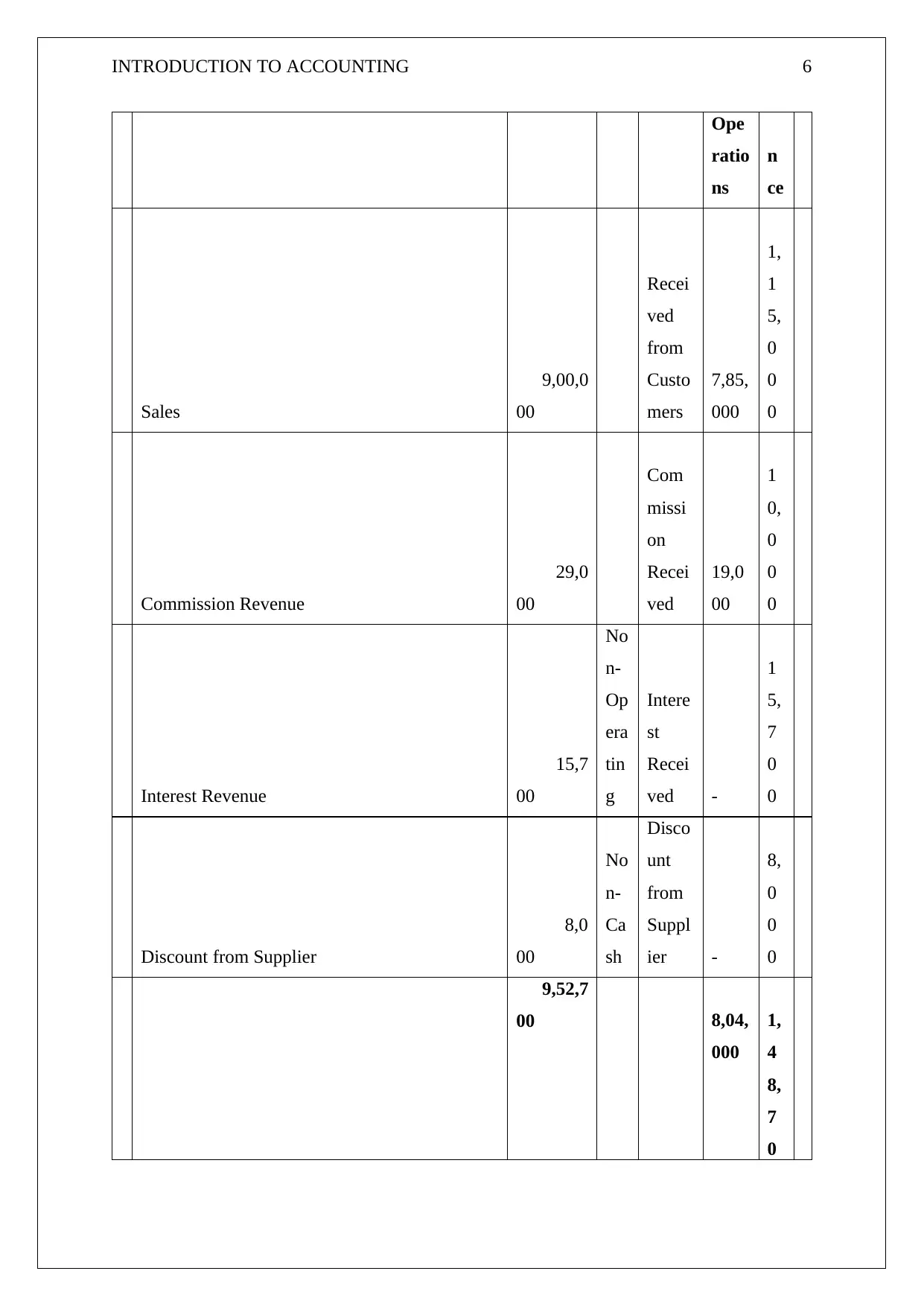

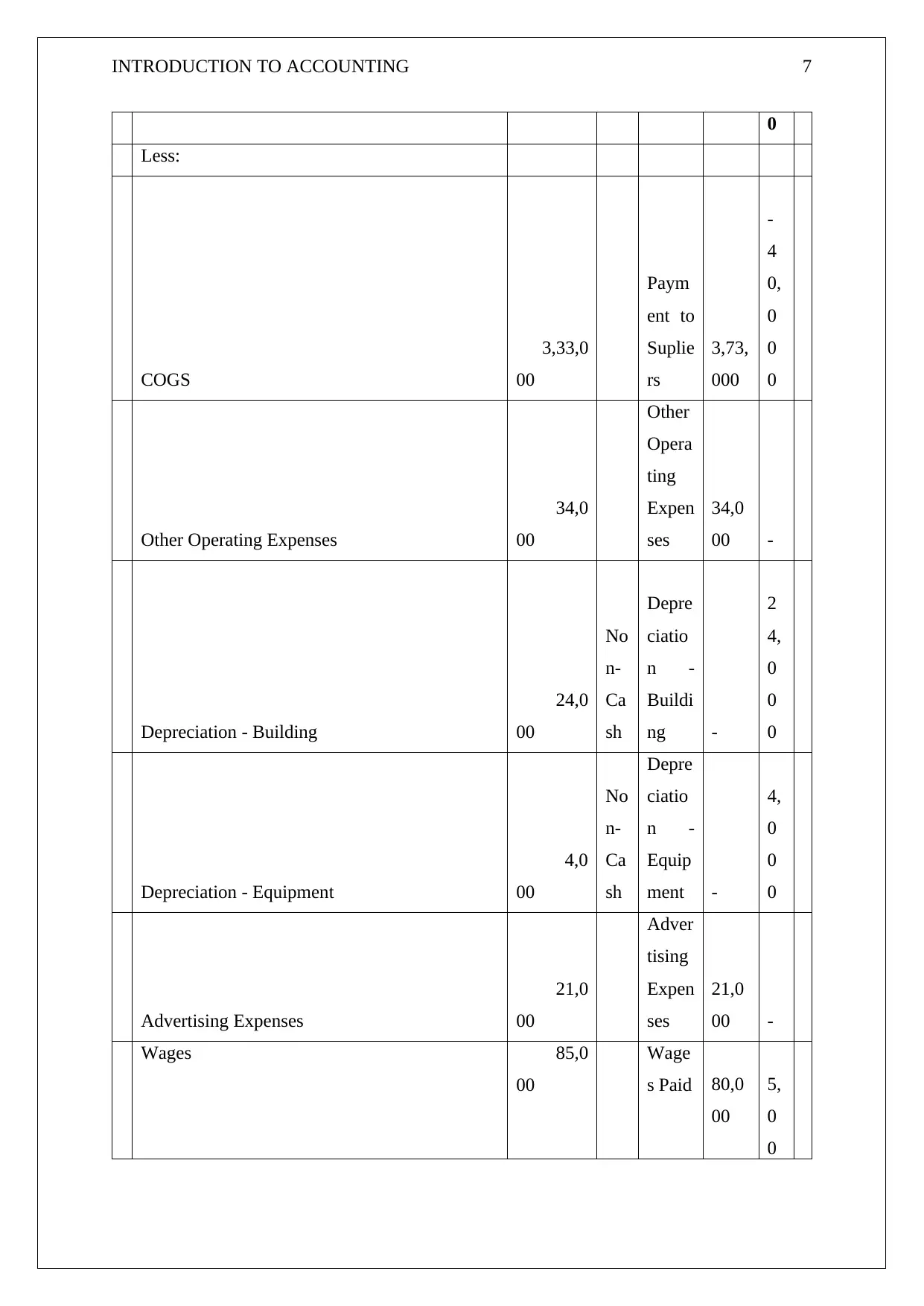

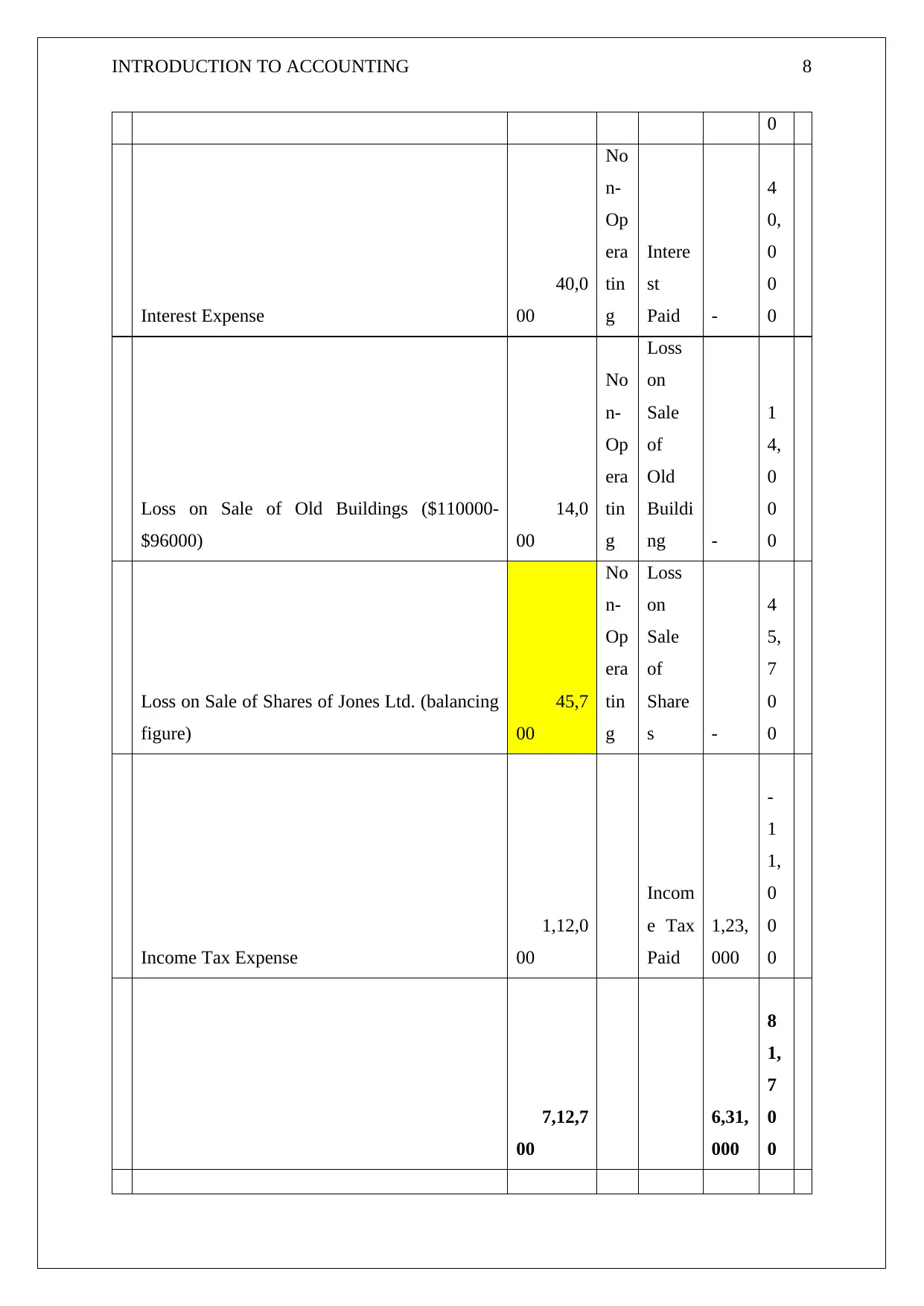

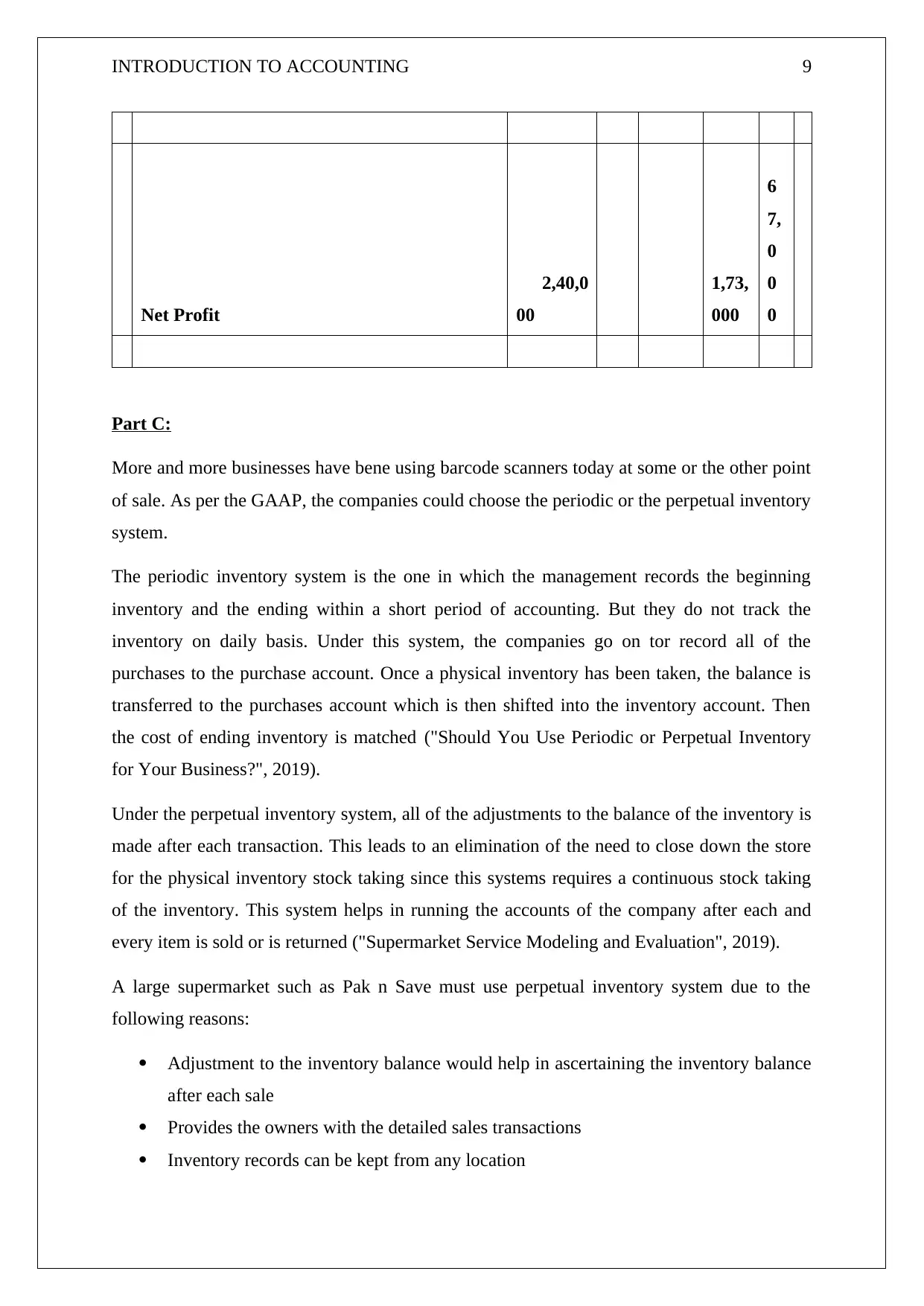

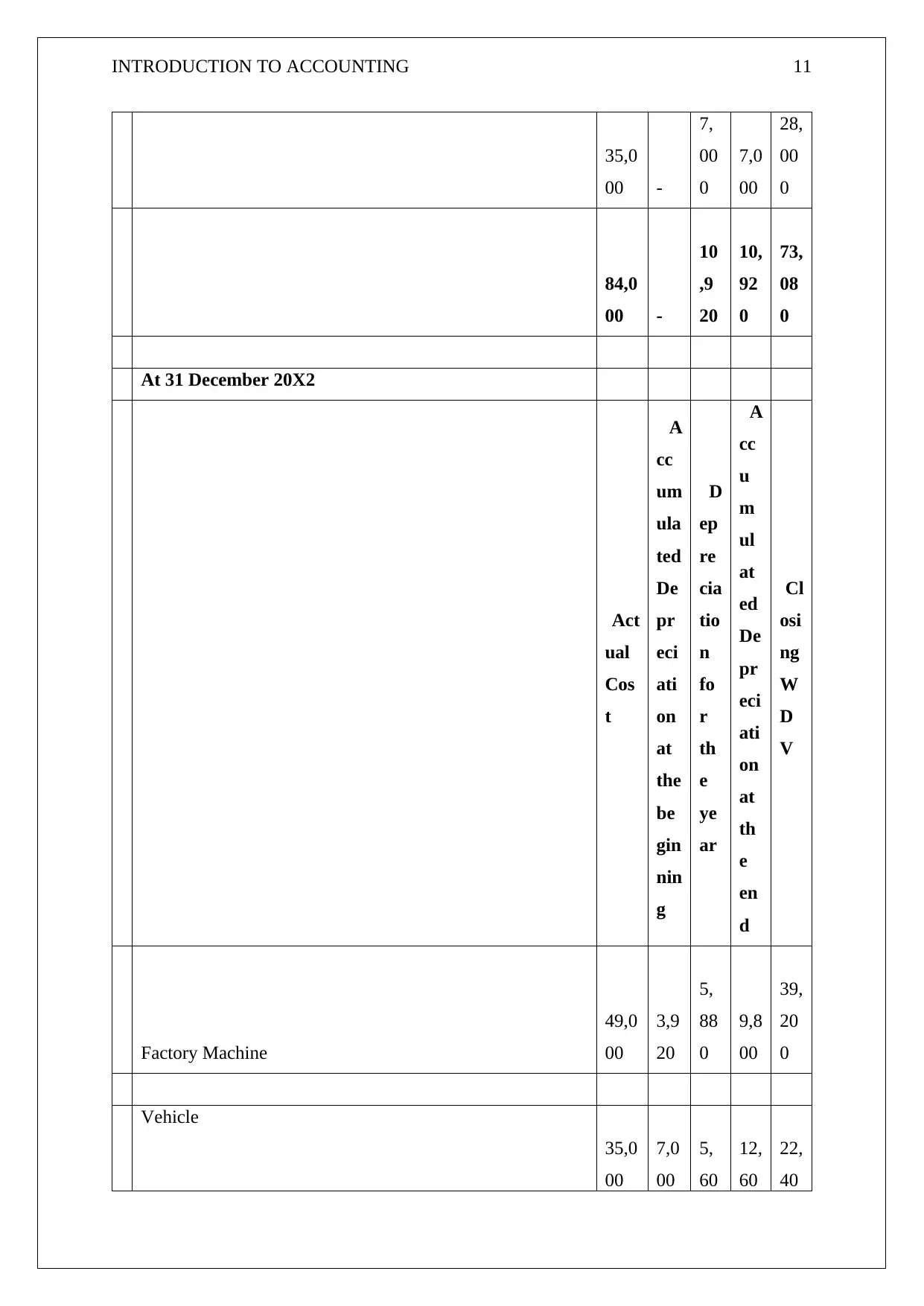

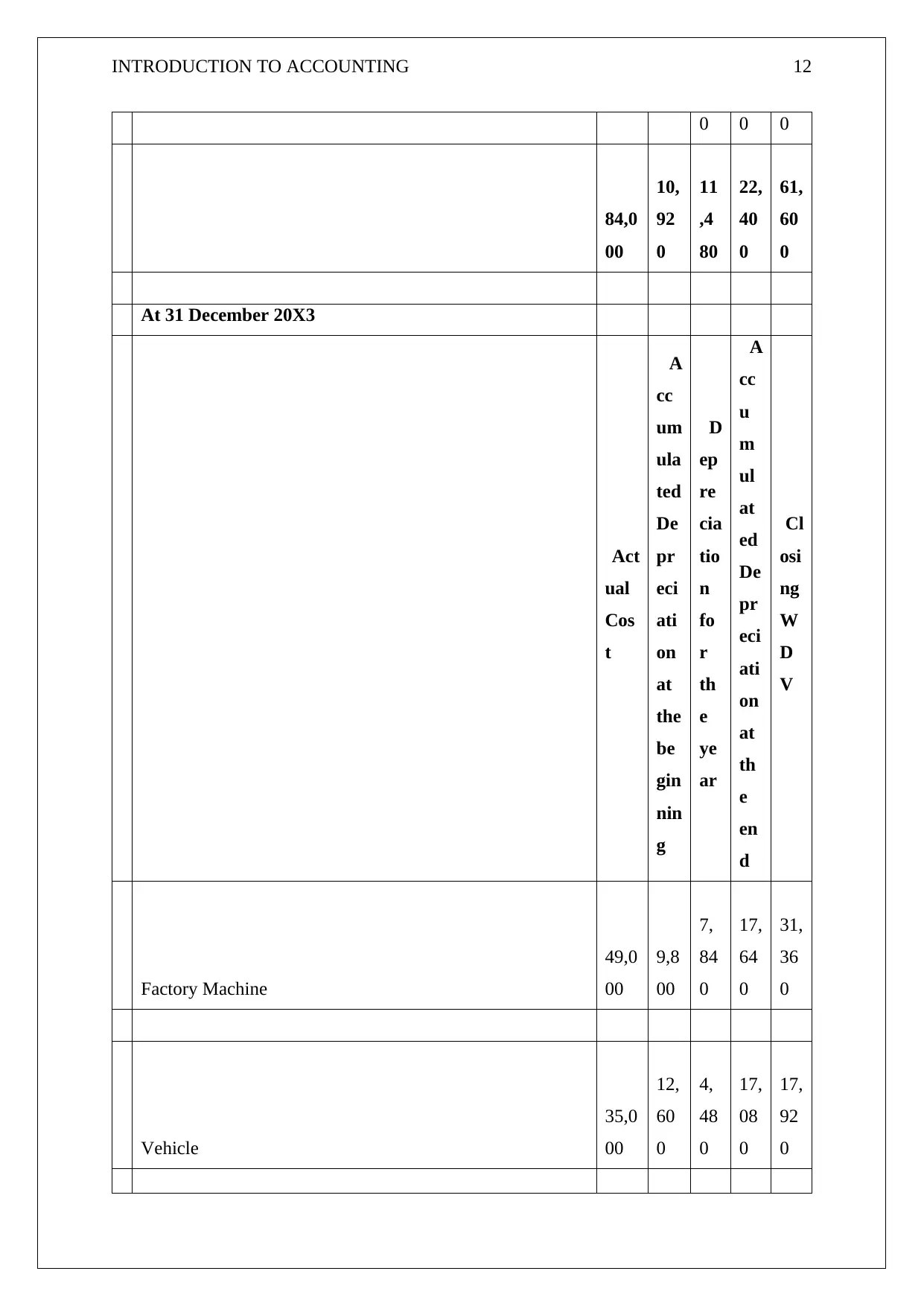

This accounting assignment solution covers key aspects of financial accounting, including cash flow statements, income statements, and inventory systems. Part A explores the differences between cash flow and net income, detailing operating, investing, and financing activities. Part B provides a cash flow statement and income statement, along with relevant calculations. Part C delves into periodic and perpetual inventory systems, discussing their suitability for different business types. Part D focuses on depreciation methods, comparing straight-line and diminishing value methods, and their impact on financial statements. The solution includes detailed calculations, explanations, and references, offering a comprehensive understanding of accounting principles and practices.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.