Advanced Financial Accounting: Impairment, Leases and Bank Analysis

VerifiedAdded on 2020/05/28

|11

|1982

|47

Report

AI Summary

This report delves into advanced financial accounting, focusing on impairment testing and lease accounting, using Commonwealth Bank of Australia as a case study. Part A examines the bank's impairment testing procedures, covering goodwill allocation, recoverable amount determination, and loan impairment expenses, as well as the subjectivity involved in the process. Part B analyzes lease accounting under IAS 17, highlighting its limitations in providing a true and fair view, particularly the classification of leases. It discusses the objectives of financial reporting, controversies surrounding operating and financing leases, and the impact of the new lease accounting standard, IFRS 16. The report assesses the flaws of the new standard and its potential benefits, such as improved comparability and transparency in financial statements, and the impact on decision-making related to leasing versus buying assets.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced financial accounting

Name of the university

Name of the student

Authors note

Advanced financial accounting

Name of the university

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Part A:..............................................................................................................................................3

Requirement i).................................................................................................................................3

Requirement ii)................................................................................................................................3

Requirement iii)...............................................................................................................................3

Requirement iv)...............................................................................................................................3

Requirement v)................................................................................................................................3

Requirement vi)...............................................................................................................................3

Requirement vii)..............................................................................................................................3

Requirement viii).............................................................................................................................3

Part B:..............................................................................................................................................4

Requirement i).................................................................................................................................4

Requirement ii)................................................................................................................................4

Requirement iii)...............................................................................................................................4

Requirement iv)...............................................................................................................................4

Requirement v)................................................................................................................................4

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Part A:..............................................................................................................................................3

Requirement i).................................................................................................................................3

Requirement ii)................................................................................................................................3

Requirement iii)...............................................................................................................................3

Requirement iv)...............................................................................................................................3

Requirement v)................................................................................................................................3

Requirement vi)...............................................................................................................................3

Requirement vii)..............................................................................................................................3

Requirement viii).............................................................................................................................3

Part B:..............................................................................................................................................4

Requirement i).................................................................................................................................4

Requirement ii)................................................................................................................................4

Requirement iii)...............................................................................................................................4

Requirement iv)...............................................................................................................................4

Requirement v)................................................................................................................................4

2

ADVANCED FINANCIAL ACCOUNTING

Part A:

Requirement i)

Impairment testing is conducted by Common wealth bank of Australia on annual basis

whenever there is indication that assets recoverable amount are lower than their carrying value.

Organization has assessed impairment testing related to intangible assets such as goodwill and

brand name. For the purpose of impairment testing, allocation of goodwill is done to the cash-

generating unit for comparing it to recoverable amount. Determination of recoverable amount is

done based on fair value by deducting cost to sells (Commbank.com.au 2018). Moreover, assets

with indefinite useful lives are tested for impairment.

Requirement ii)

For conducting the impairment testing, organization allocated the goodwill to cash

generating unit and does the computation of recoverable amount. Publicly available earnings

multiples form the basis of calculation of recoverable amount. For determining the assessment of

goodwill and other assets, recoverable amount of such assets are compared with carrying amount

of individual cash generating unit or group of cash generating unit. Some of the indicators for

impairment are as for equity securities that are classified as assets available for sale. An

indication of impairment of any investment leads to testing of entire carrying amount of

investment in any associate or joint venture by comparing the carrying amount with its

recoverable amount (Commbank.com.au 2018).

ADVANCED FINANCIAL ACCOUNTING

Part A:

Requirement i)

Impairment testing is conducted by Common wealth bank of Australia on annual basis

whenever there is indication that assets recoverable amount are lower than their carrying value.

Organization has assessed impairment testing related to intangible assets such as goodwill and

brand name. For the purpose of impairment testing, allocation of goodwill is done to the cash-

generating unit for comparing it to recoverable amount. Determination of recoverable amount is

done based on fair value by deducting cost to sells (Commbank.com.au 2018). Moreover, assets

with indefinite useful lives are tested for impairment.

Requirement ii)

For conducting the impairment testing, organization allocated the goodwill to cash

generating unit and does the computation of recoverable amount. Publicly available earnings

multiples form the basis of calculation of recoverable amount. For determining the assessment of

goodwill and other assets, recoverable amount of such assets are compared with carrying amount

of individual cash generating unit or group of cash generating unit. Some of the indicators for

impairment are as for equity securities that are classified as assets available for sale. An

indication of impairment of any investment leads to testing of entire carrying amount of

investment in any associate or joint venture by comparing the carrying amount with its

recoverable amount (Commbank.com.au 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ADVANCED FINANCIAL ACCOUNTING

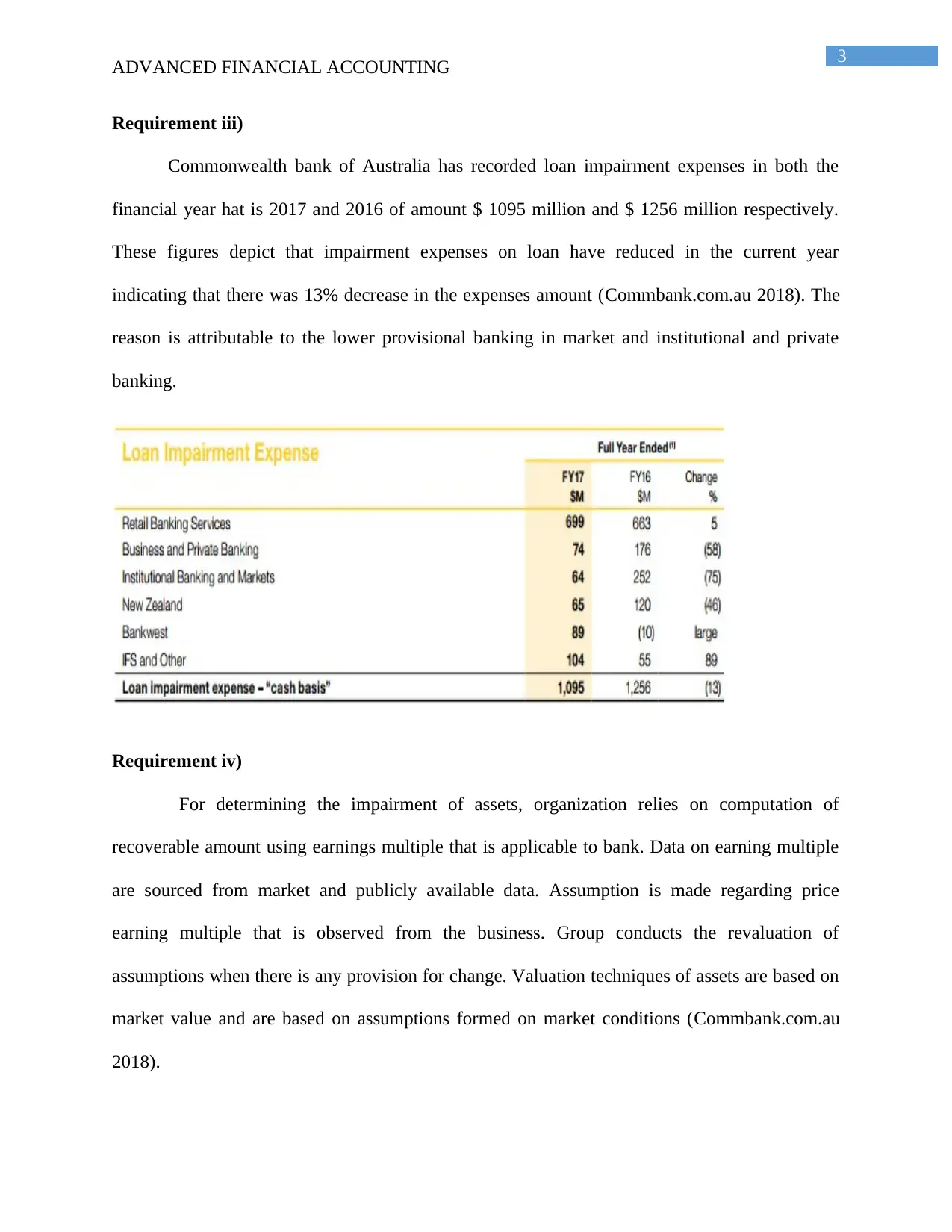

Requirement iii)

Commonwealth bank of Australia has recorded loan impairment expenses in both the

financial year hat is 2017 and 2016 of amount $ 1095 million and $ 1256 million respectively.

These figures depict that impairment expenses on loan have reduced in the current year

indicating that there was 13% decrease in the expenses amount (Commbank.com.au 2018). The

reason is attributable to the lower provisional banking in market and institutional and private

banking.

Requirement iv)

For determining the impairment of assets, organization relies on computation of

recoverable amount using earnings multiple that is applicable to bank. Data on earning multiple

are sourced from market and publicly available data. Assumption is made regarding price

earning multiple that is observed from the business. Group conducts the revaluation of

assumptions when there is any provision for change. Valuation techniques of assets are based on

market value and are based on assumptions formed on market conditions (Commbank.com.au

2018).

ADVANCED FINANCIAL ACCOUNTING

Requirement iii)

Commonwealth bank of Australia has recorded loan impairment expenses in both the

financial year hat is 2017 and 2016 of amount $ 1095 million and $ 1256 million respectively.

These figures depict that impairment expenses on loan have reduced in the current year

indicating that there was 13% decrease in the expenses amount (Commbank.com.au 2018). The

reason is attributable to the lower provisional banking in market and institutional and private

banking.

Requirement iv)

For determining the impairment of assets, organization relies on computation of

recoverable amount using earnings multiple that is applicable to bank. Data on earning multiple

are sourced from market and publicly available data. Assumption is made regarding price

earning multiple that is observed from the business. Group conducts the revaluation of

assumptions when there is any provision for change. Valuation techniques of assets are based on

market value and are based on assumptions formed on market conditions (Commbank.com.au

2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ADVANCED FINANCIAL ACCOUNTING

Requirement v)

Process of impairment testing of Common wealth bank of Australia does not involve any

considerable subjectivity as depicted from the analysis of financial report. The methodology of

impairment testing is considerably influenced by involvement of subjectivity in the estimates and

assumptions made by management of group. When subjectivity is considered, there then exists

possibility of recoverable value being highly sensitive (Osei 2017). If the management of

organization is acting opportunistically, then there can be manipulation in assets recoverable

amount. Value in use computation, determinants of cash flows and value generated and there is a

possibility that there will be substantial fluctuation in the assumed value because other external

factors rather than exercising subjectivity (Commbank.com.au 2018).

Requirement vi)

After conducting detailed analysis of annual report of Common wealth bank of Australia

concerning impairment, it has been ascertained that the procedure adopted for impairment testing

is a bit confusing. There has not been a segmented presentation of impairment and information

considering the impairment of various is presented in a segregated way.

Requirement vii)

It has been ascertained from the evaluation of financial report of banking group that

organizations make provision related to impairment of all financial assets. Receivables and loans

are assessed collectively for impairment is done on collectively basis. Bank has employed

expected credit loss model as per AASB 9 that has lead to replacement of existing incurred loss

model (Commbank.com.au 2018). Impairment provisions are raised for the amount that is

adequate to cover losses related to credit and when there is any existence of objective evidence.

ADVANCED FINANCIAL ACCOUNTING

Requirement v)

Process of impairment testing of Common wealth bank of Australia does not involve any

considerable subjectivity as depicted from the analysis of financial report. The methodology of

impairment testing is considerably influenced by involvement of subjectivity in the estimates and

assumptions made by management of group. When subjectivity is considered, there then exists

possibility of recoverable value being highly sensitive (Osei 2017). If the management of

organization is acting opportunistically, then there can be manipulation in assets recoverable

amount. Value in use computation, determinants of cash flows and value generated and there is a

possibility that there will be substantial fluctuation in the assumed value because other external

factors rather than exercising subjectivity (Commbank.com.au 2018).

Requirement vi)

After conducting detailed analysis of annual report of Common wealth bank of Australia

concerning impairment, it has been ascertained that the procedure adopted for impairment testing

is a bit confusing. There has not been a segmented presentation of impairment and information

considering the impairment of various is presented in a segregated way.

Requirement vii)

It has been ascertained from the evaluation of financial report of banking group that

organizations make provision related to impairment of all financial assets. Receivables and loans

are assessed collectively for impairment is done on collectively basis. Bank has employed

expected credit loss model as per AASB 9 that has lead to replacement of existing incurred loss

model (Commbank.com.au 2018). Impairment provisions are raised for the amount that is

adequate to cover losses related to credit and when there is any existence of objective evidence.

5

ADVANCED FINANCIAL ACCOUNTING

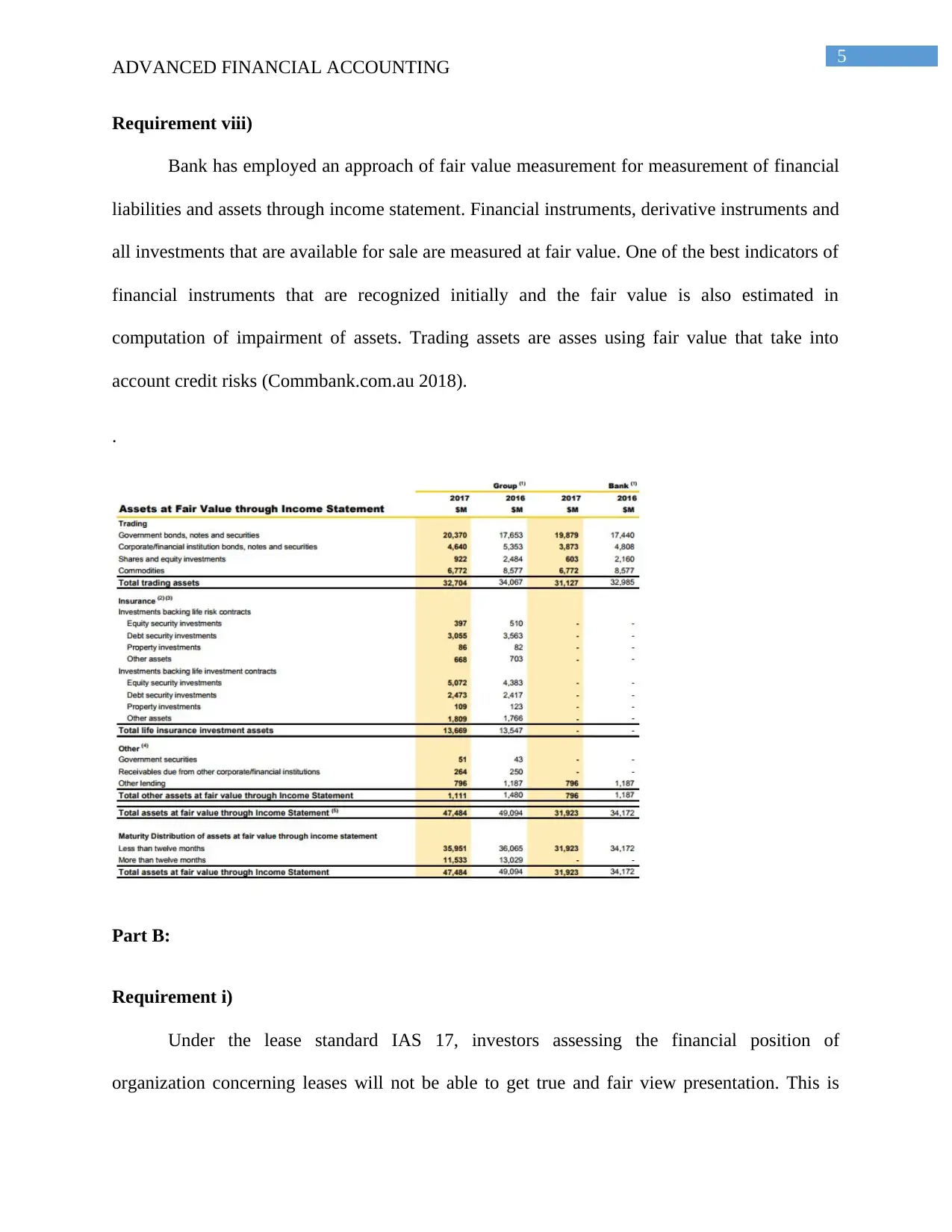

Requirement viii)

Bank has employed an approach of fair value measurement for measurement of financial

liabilities and assets through income statement. Financial instruments, derivative instruments and

all investments that are available for sale are measured at fair value. One of the best indicators of

financial instruments that are recognized initially and the fair value is also estimated in

computation of impairment of assets. Trading assets are asses using fair value that take into

account credit risks (Commbank.com.au 2018).

.

Part B:

Requirement i)

Under the lease standard IAS 17, investors assessing the financial position of

organization concerning leases will not be able to get true and fair view presentation. This is

ADVANCED FINANCIAL ACCOUNTING

Requirement viii)

Bank has employed an approach of fair value measurement for measurement of financial

liabilities and assets through income statement. Financial instruments, derivative instruments and

all investments that are available for sale are measured at fair value. One of the best indicators of

financial instruments that are recognized initially and the fair value is also estimated in

computation of impairment of assets. Trading assets are asses using fair value that take into

account credit risks (Commbank.com.au 2018).

.

Part B:

Requirement i)

Under the lease standard IAS 17, investors assessing the financial position of

organization concerning leases will not be able to get true and fair view presentation. This is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ADVANCED FINANCIAL ACCOUNTING

because of the critics associated with the existing standard as it makes the classification between

financing and operating leases. Balance sheet profiles of companies do not reflect the actual

amount of debt that company currently owes (Edeigba and Amenkhienan 2017). It is so because

this standard does not obliges company to disclose operating lease in their balance sheet and

most of them select to treat lease as operating lease rather than financing lease. Therefore, the

existing lease standard does not reflect economic reality. It has been estimated by the accounting

standard that is IASB out of total amount of commitment attributable to leases of worth 3.3

million, only 25% of lease appear on balance sheet (Sandblom and Strandberg 2015).

Requirement ii)

One of the objectives of presentation of financial report is to provide users with the

information that helps in making economic decision. Under the existing standard, there is

possibility that there will be unfaithful classification of leasing transactions. Investors are

required to make rough estimation and calculations for computing lease commitment and brining

them on balance sheets. Operating lease is also a type of liabilities but they are not represented

on balance sheet but in actual sense, there is a liability that is more than total amount debt

reported (Demir and Bas 2017). This explains why the debt reported on balance sheet is 66 times

less than off balance sheet liabilities.

Requirement iii)

Controversy associated with existing standard regarding the leases classification into

operating and financing lease explains why there is no level playing field between some airline

companies. Airline companies either leases most of their aircraft fleets or they finance that is buy

the fleets. It would indicate that the financial position of such organizations is different, but in

ADVANCED FINANCIAL ACCOUNTING

because of the critics associated with the existing standard as it makes the classification between

financing and operating leases. Balance sheet profiles of companies do not reflect the actual

amount of debt that company currently owes (Edeigba and Amenkhienan 2017). It is so because

this standard does not obliges company to disclose operating lease in their balance sheet and

most of them select to treat lease as operating lease rather than financing lease. Therefore, the

existing lease standard does not reflect economic reality. It has been estimated by the accounting

standard that is IASB out of total amount of commitment attributable to leases of worth 3.3

million, only 25% of lease appear on balance sheet (Sandblom and Strandberg 2015).

Requirement ii)

One of the objectives of presentation of financial report is to provide users with the

information that helps in making economic decision. Under the existing standard, there is

possibility that there will be unfaithful classification of leasing transactions. Investors are

required to make rough estimation and calculations for computing lease commitment and brining

them on balance sheets. Operating lease is also a type of liabilities but they are not represented

on balance sheet but in actual sense, there is a liability that is more than total amount debt

reported (Demir and Bas 2017). This explains why the debt reported on balance sheet is 66 times

less than off balance sheet liabilities.

Requirement iii)

Controversy associated with existing standard regarding the leases classification into

operating and financing lease explains why there is no level playing field between some airline

companies. Airline companies either leases most of their aircraft fleets or they finance that is buy

the fleets. It would indicate that the financial position of such organizations is different, but in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ADVANCED FINANCIAL ACCOUNTING

reality, there might not be any difference in their financial position and they are identical (Nobes

2015).

Requirement iv)

Various flaws associated with the new lease accounting standard are responsible for

making it unpopular among everyone. New standard would be focusing on capitalization of

operating lease that would increase the balance sheets and debt structure of companies.

Companies in receiving credit have also raised concerns and there is a possibility of violation of

debt covenants. Adoption of standard will lead to hundred percent of balance sheets and this will

require them to renegotiate debt covenants and exclusion of lease agreements. There would be

increased administrative burden on part of management and increased cost of reporting that is

making companies hesitant to adopt this standard (Czajor and Michalak 2017). There will be

alterations in the system of control process, increased consultation fees, educational efforts and

process of IT. Moreover, organizations are required to make an estimation of detail relating to

right to lease liabilities and assets.

Requirement v)

Implementation of new standard will help in facilitating the comparison between the

financial statements of different companies. This standard will help in addressing the unfaithful

presentation of lease accounting. Investors will not be required to make any rough computation

and estimation of bringing back leases into balance sheets. Investors will be informed in a better

way because of transparency of information relating to leases. Accounting model of organization

will be altered and will benefit organizations in providing detailed information concerning leases

and therefore investors will be informed and take into account the benefits that would arrive

ADVANCED FINANCIAL ACCOUNTING

reality, there might not be any difference in their financial position and they are identical (Nobes

2015).

Requirement iv)

Various flaws associated with the new lease accounting standard are responsible for

making it unpopular among everyone. New standard would be focusing on capitalization of

operating lease that would increase the balance sheets and debt structure of companies.

Companies in receiving credit have also raised concerns and there is a possibility of violation of

debt covenants. Adoption of standard will lead to hundred percent of balance sheets and this will

require them to renegotiate debt covenants and exclusion of lease agreements. There would be

increased administrative burden on part of management and increased cost of reporting that is

making companies hesitant to adopt this standard (Czajor and Michalak 2017). There will be

alterations in the system of control process, increased consultation fees, educational efforts and

process of IT. Moreover, organizations are required to make an estimation of detail relating to

right to lease liabilities and assets.

Requirement v)

Implementation of new standard will help in facilitating the comparison between the

financial statements of different companies. This standard will help in addressing the unfaithful

presentation of lease accounting. Investors will not be required to make any rough computation

and estimation of bringing back leases into balance sheets. Investors will be informed in a better

way because of transparency of information relating to leases. Accounting model of organization

will be altered and will benefit organizations in providing detailed information concerning leases

and therefore investors will be informed and take into account the benefits that would arrive

8

ADVANCED FINANCIAL ACCOUNTING

(Morales and Zamora 2018). Decision relating to leased will improved and allocation of capital

will improve. Therefore, organization adopting this standard will lead to a more balanced lease

versus buy decisions on part of management.

ADVANCED FINANCIAL ACCOUNTING

(Morales and Zamora 2018). Decision relating to leased will improved and allocation of capital

will improve. Therefore, organization adopting this standard will lead to a more balanced lease

versus buy decisions on part of management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ADVANCED FINANCIAL ACCOUNTING

References list:

Commbank.com.au. (2018). [online] Available at:

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-

reports/annual_report_2017_14_aug_2017.pdf [Accessed 23 Jan. 2018].

Czajor, P. and Michalak, M., 2017. Operating Lease Capitalization-Reasons and its Impact on

Financial Ratios of WIG30 and sWIG80 Companies. Przedsiębiorczość i Zarządzanie, 18(1, cz.

1 Practical and Theoretical Issues in Contemporary Financial Management), pp.23-36.

Demir, Z. and Bas, E., 2017. THE EFFECT OF TAS 17 “LEASING” STANDARD AND

IMPLEMENTATION OF THE NEW IFRS 16 “LEASES” STANDARD ON THE AIRLINE

COMPANIES. PressAcademia Procedia, 3(1), pp.153-173.

Edeigba, J. and Amenkhienan, F., 2017. The Influence of IFRS Adoption on Corporate

Transparency and Accountability: Evidence from New Zealand. Australasian Accounting,

Business and Finance Journal, 11(3), pp.3-19.

Karwowski, M., 2016. The risk in using financial reports in the study of airline business

models. Journal of Air Transport Management, 55, pp.185-192.

Morales-Díaz, J. and Zamora-Ramírez, C., 2018. IFRS 16 (leases) implementation: Impact of

entities' decisions on financial statements. Aestimatio, (17), pp.60-97.

Nobes, C., 2015. IFRS Ten Years on: Has the IASB Imposed Extensive Use of Fair Value? Has

the EU Learnt to Love IFRS? And Does the Use of Fair Value make IFRS Illegal in the

EU?. Accounting in Europe, 12(2), pp.153-170.

Osei, E., 2017. THE FINANCIAL ACCOUNTING STANDARDS BOARD (FASB), AND THE

INTERNATIONAL ACCOUNTING STANDARDS BOARD (IASB) SINGS SIMILAR TUNE:

ADVANCED FINANCIAL ACCOUNTING

References list:

Commbank.com.au. (2018). [online] Available at:

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-

reports/annual_report_2017_14_aug_2017.pdf [Accessed 23 Jan. 2018].

Czajor, P. and Michalak, M., 2017. Operating Lease Capitalization-Reasons and its Impact on

Financial Ratios of WIG30 and sWIG80 Companies. Przedsiębiorczość i Zarządzanie, 18(1, cz.

1 Practical and Theoretical Issues in Contemporary Financial Management), pp.23-36.

Demir, Z. and Bas, E., 2017. THE EFFECT OF TAS 17 “LEASING” STANDARD AND

IMPLEMENTATION OF THE NEW IFRS 16 “LEASES” STANDARD ON THE AIRLINE

COMPANIES. PressAcademia Procedia, 3(1), pp.153-173.

Edeigba, J. and Amenkhienan, F., 2017. The Influence of IFRS Adoption on Corporate

Transparency and Accountability: Evidence from New Zealand. Australasian Accounting,

Business and Finance Journal, 11(3), pp.3-19.

Karwowski, M., 2016. The risk in using financial reports in the study of airline business

models. Journal of Air Transport Management, 55, pp.185-192.

Morales-Díaz, J. and Zamora-Ramírez, C., 2018. IFRS 16 (leases) implementation: Impact of

entities' decisions on financial statements. Aestimatio, (17), pp.60-97.

Nobes, C., 2015. IFRS Ten Years on: Has the IASB Imposed Extensive Use of Fair Value? Has

the EU Learnt to Love IFRS? And Does the Use of Fair Value make IFRS Illegal in the

EU?. Accounting in Europe, 12(2), pp.153-170.

Osei, E., 2017. THE FINANCIAL ACCOUNTING STANDARDS BOARD (FASB), AND THE

INTERNATIONAL ACCOUNTING STANDARDS BOARD (IASB) SINGS SIMILAR TUNE:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ADVANCED FINANCIAL ACCOUNTING

COMPARING THE ACCOUNTING TREATMENT OF NEW IFRS 16 WITH THE IAS 17,

AND THE NEW FASB MODEL ON LEASES. Journal of Theoretical Accounting

Research, 13(1).

Sacarin, M., 2017. IFRS 16 “Leases”–consequences on the financial statements and financial

indicators. The Audit Financiar journal, 15(145), pp.114-114.

Sandblom, P. and Strandberg, A., 2015. The Value Relevance of the Proposed New Leasing

Standard. An event study of the European Stock Markets’ Reaction to the proposed replacement

of IAS17.

You, J., 2017. The Impact of IFRS 16 Lease on Financial Statement of Airline

Companies (Doctoral dissertation, Auckland University of Technology).

ADVANCED FINANCIAL ACCOUNTING

COMPARING THE ACCOUNTING TREATMENT OF NEW IFRS 16 WITH THE IAS 17,

AND THE NEW FASB MODEL ON LEASES. Journal of Theoretical Accounting

Research, 13(1).

Sacarin, M., 2017. IFRS 16 “Leases”–consequences on the financial statements and financial

indicators. The Audit Financiar journal, 15(145), pp.114-114.

Sandblom, P. and Strandberg, A., 2015. The Value Relevance of the Proposed New Leasing

Standard. An event study of the European Stock Markets’ Reaction to the proposed replacement

of IAS17.

You, J., 2017. The Impact of IFRS 16 Lease on Financial Statement of Airline

Companies (Doctoral dissertation, Auckland University of Technology).

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.