Corporate Accounting and Reporting Assignment: Impairment Analysis

VerifiedAdded on 2020/04/01

|10

|1937

|69

Homework Assignment

AI Summary

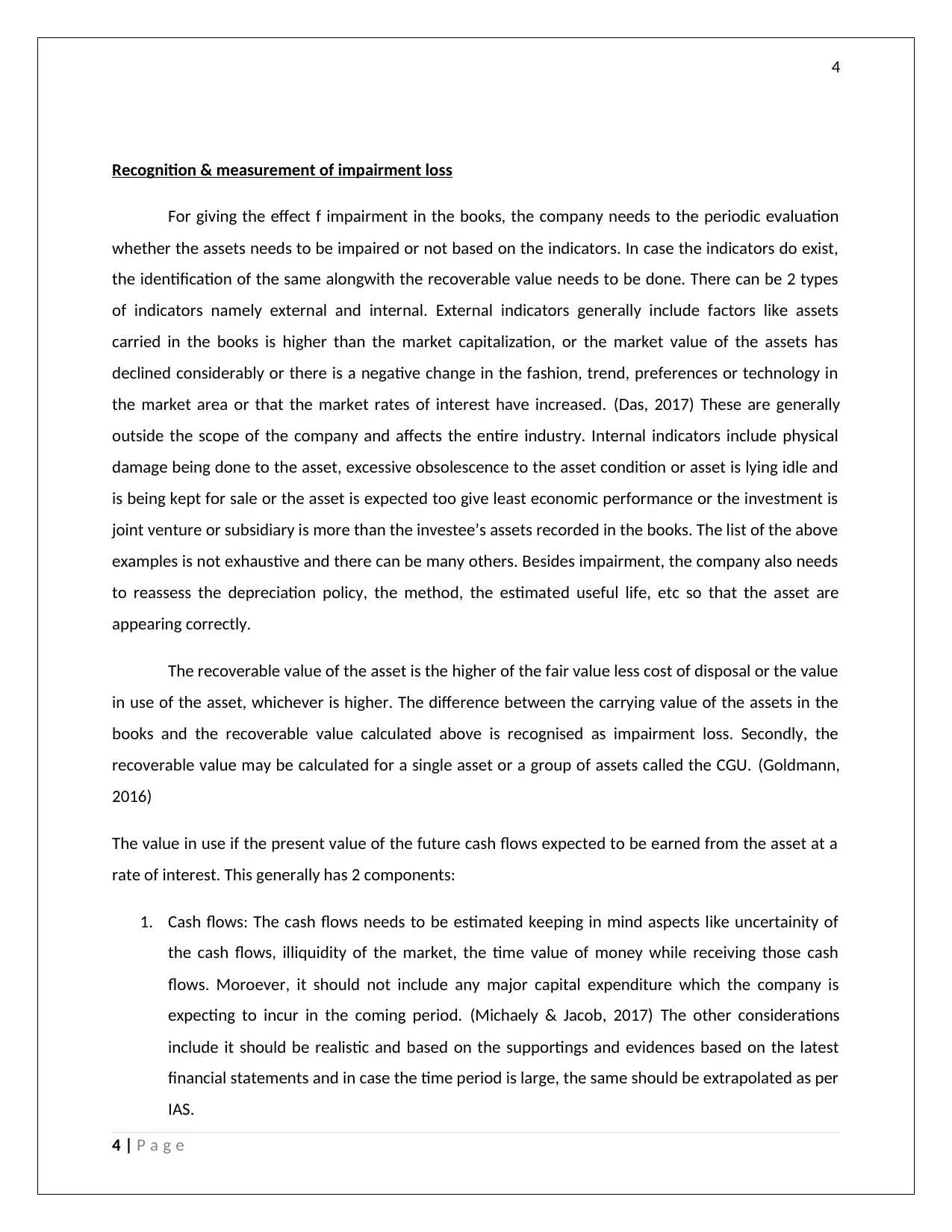

This assignment delves into the critical aspects of corporate accounting and reporting, with a specific focus on asset impairment. The introduction provides an overview of impairment accounting, referencing both IAS 36 and AS 28, and emphasizes the importance of regularly assessing tangible and intangible assets for potential write-downs. The assignment explores the identification of impairment indicators, differentiating between internal and external factors, and the calculation of recoverable value, which is the higher of the value in use and fair value less costs of disposal. The assignment also discusses the concept of Cash Generating Units (CGUs) and their significance in impairment testing. The solution section provides a detailed analysis of a case study involving Gali Limited, demonstrating the allocation of impairment loss across various assets, including goodwill, plant, equipment, and fittings. The conclusion stresses the importance of judgment, estimates, and proper disclosures in financial statements, including the basis of impairment, loss recognition, and any reversals. The assignment provides the journal entry to effect the impairment loss. The reference section provides citations to support the assignment.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.