Accounting Information System Analysis: Adam & Co Case Study

VerifiedAdded on 2022/11/12

|14

|2633

|66

Case Study

AI Summary

This case study analyzes the accounting information system of Adam & Co, a large industrial supplier, focusing on its expenditure cycle. The analysis includes system flowcharts, processes, risks, and internal control weaknesses within the purchases, cash disbursements, and payroll systems. The purchases system involves order processing, vendor selection, receiving, and accounts payable. The cash disbursements system covers payment authorization and cheque processing. The payroll system details time card management, payroll processing, and cheque distribution. The report identifies risks like fraud, errors, and authorization issues. Weaknesses are highlighted, such as communication gaps, lack of management authorization, and time card inaccuracies. The report provides an overview of the accounting system, including the processes, risks, and internal control weaknesses associated with each system.

Accounting Information System1

<University>

Accounting Information System

By

<Your Name>

<Date>

<Lecturer’s Name and Course Number>

<University>

Accounting Information System

By

<Your Name>

<Date>

<Lecturer’s Name and Course Number>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Information System 2

Table of Contents

Contents

Table of Contents.............................................................................................................................2

Executive Summary.........................................................................................................................3

Introduction......................................................................................................................................4

System flowchart of purchases system............................................................................................5

Processes involved in purchases system of Adam & Co.............................................................5

Risks associated with purchases system of Adam & Co.............................................................7

Internal control weaknesses involved in purchases system of Adam & Co................................7

System flowchart of cash disbursements system.............................................................................8

Processes involved in cash disbursements system of Adam & Co..............................................8

Risks associated with cash disbursements system of Adam & Co..............................................9

Internal weaknesses associated with cash disbursement system of Adam & Co.........................9

System flowchart of payroll system..............................................................................................10

Processes involved in the payroll system of Adam & Co..........................................................11

Risks involved in payroll system of Adam & Co......................................................................11

Internal weaknesses associated with payroll system of Adam & Co.........................................12

Conclusion.....................................................................................................................................12

References......................................................................................................................................14

Table of Contents

Contents

Table of Contents.............................................................................................................................2

Executive Summary.........................................................................................................................3

Introduction......................................................................................................................................4

System flowchart of purchases system............................................................................................5

Processes involved in purchases system of Adam & Co.............................................................5

Risks associated with purchases system of Adam & Co.............................................................7

Internal control weaknesses involved in purchases system of Adam & Co................................7

System flowchart of cash disbursements system.............................................................................8

Processes involved in cash disbursements system of Adam & Co..............................................8

Risks associated with cash disbursements system of Adam & Co..............................................9

Internal weaknesses associated with cash disbursement system of Adam & Co.........................9

System flowchart of payroll system..............................................................................................10

Processes involved in the payroll system of Adam & Co..........................................................11

Risks involved in payroll system of Adam & Co......................................................................11

Internal weaknesses associated with payroll system of Adam & Co.........................................12

Conclusion.....................................................................................................................................12

References......................................................................................................................................14

Accounting Information System 3

Executive Summary

Adam & Co is one of the industrial suppliers in Perth that make use of a centralized accounting

system to control and manage its expenditure cycle. Purchasing, cash disbursement, and payroll

systems make up the company's expenditure cycle as a massive volume of financial resources is

spent on them. Financial resources are spent mainly on processes relating to the acquisition of

goods and services as well as compensation payments for labor services. The company makes

use of its employees and departments to ensure that all processes involved in its purchasing, cash

disbursement, and payroll systems are effectively executed to achieve set goals and objectives.

However, fraud, miscalculations, and incorrect entries that take place during execution of system

processes pose a significant threat to the achievement of desired business goals. Besides, internal

weaknesses in the form of ineffective communication, authorization concerns, and time card

errors threat the company's financial accounting system.

Executive Summary

Adam & Co is one of the industrial suppliers in Perth that make use of a centralized accounting

system to control and manage its expenditure cycle. Purchasing, cash disbursement, and payroll

systems make up the company's expenditure cycle as a massive volume of financial resources is

spent on them. Financial resources are spent mainly on processes relating to the acquisition of

goods and services as well as compensation payments for labor services. The company makes

use of its employees and departments to ensure that all processes involved in its purchasing, cash

disbursement, and payroll systems are effectively executed to achieve set goals and objectives.

However, fraud, miscalculations, and incorrect entries that take place during execution of system

processes pose a significant threat to the achievement of desired business goals. Besides, internal

weaknesses in the form of ineffective communication, authorization concerns, and time card

errors threat the company's financial accounting system.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Information System 4

Introduction

Being a large wholesaler of industrial suppliers, Adam & Co makes use of its centralized

accounting system at distinct locations to ensure that the utilization of resources is effectively

done to meet desired goals and objectives. Adam & Co focuses on providing that the flow of its

resources is effectively done basing on its organization structures at distinct locations. Most

significantly, the company consists of several departments and professionals that collaborate and

coordinate to ensure that all resources are effectively managed to achieve set goals and

objectives. Purchase clerk, vendors, payroll clerk, are some of the professionals at the company

that ensures that its expenditure cycle is effectively executed to meet desired business goals and

objectives. Besides, purchasing department, receiving department, accounts payable and

receivable are the necessary departments at Adam & Co that ensure that all processes and risks

involved in the expenditure cycle are expertly executed and managed (Belverd & Marian 2013).

As such, this report will mainly address the risks, processes, and internal control of Adam & Co's

expenditure cycle. As a business analyst, the report will be directed to the managing director at

the company regarding the expenditure cycle. Most importantly, the report will address risks,

processes, and internal control weaknesses associated with the company’s purchases system,

cash disbursements system as well as payroll systems as discussed below.

Introduction

Being a large wholesaler of industrial suppliers, Adam & Co makes use of its centralized

accounting system at distinct locations to ensure that the utilization of resources is effectively

done to meet desired goals and objectives. Adam & Co focuses on providing that the flow of its

resources is effectively done basing on its organization structures at distinct locations. Most

significantly, the company consists of several departments and professionals that collaborate and

coordinate to ensure that all resources are effectively managed to achieve set goals and

objectives. Purchase clerk, vendors, payroll clerk, are some of the professionals at the company

that ensures that its expenditure cycle is effectively executed to meet desired business goals and

objectives. Besides, purchasing department, receiving department, accounts payable and

receivable are the necessary departments at Adam & Co that ensure that all processes and risks

involved in the expenditure cycle are expertly executed and managed (Belverd & Marian 2013).

As such, this report will mainly address the risks, processes, and internal control of Adam & Co's

expenditure cycle. As a business analyst, the report will be directed to the managing director at

the company regarding the expenditure cycle. Most importantly, the report will address risks,

processes, and internal control weaknesses associated with the company’s purchases system,

cash disbursements system as well as payroll systems as discussed below.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Information System 5

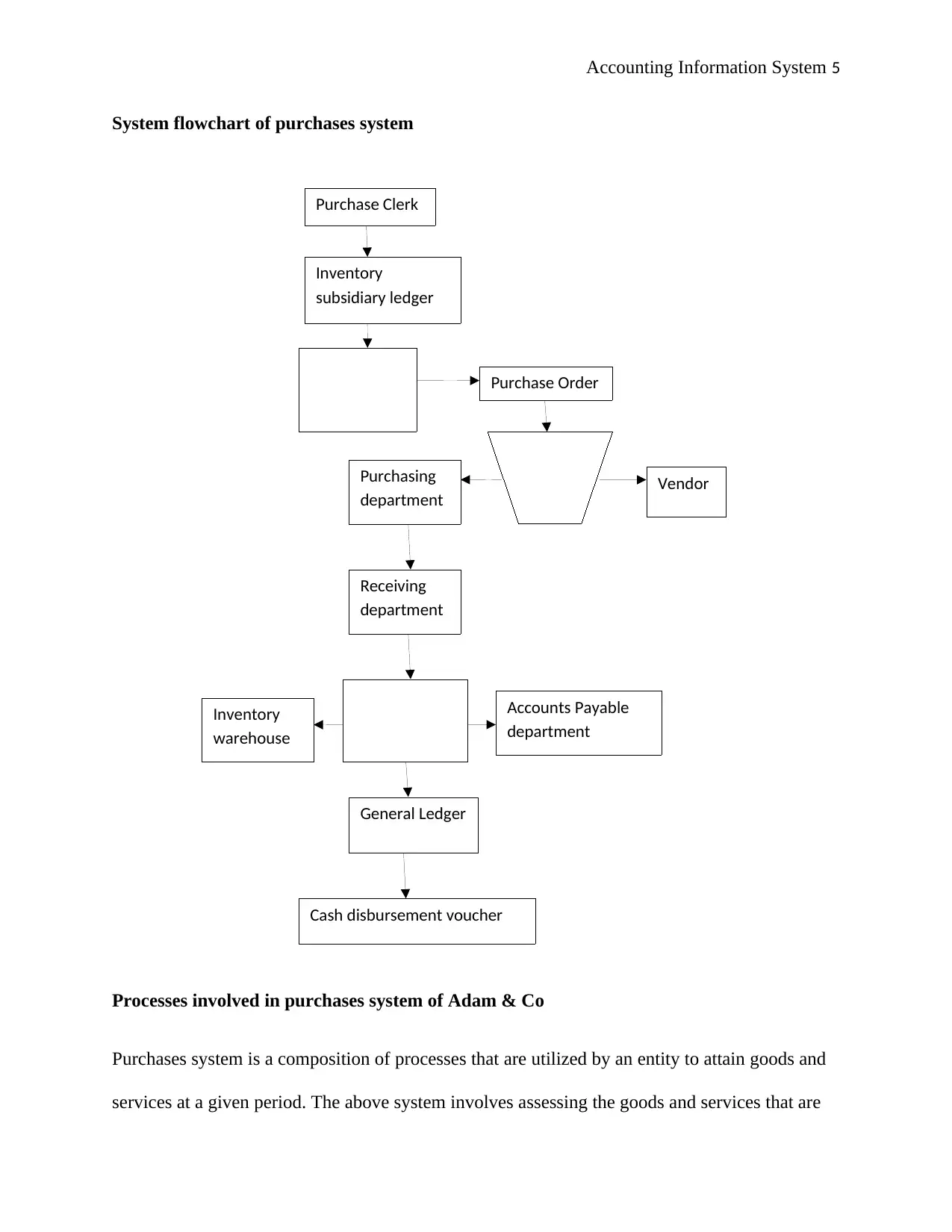

System flowchart of purchases system

Processes involved in purchases system of Adam & Co

Purchases system is a composition of processes that are utilized by an entity to attain goods and

services at a given period. The above system involves assessing the goods and services that are

Vendor

Cash disbursement voucher

General Ledger

Accounts Payable

department

Inventory

warehouse

Receiving

department

Purchase Clerk

Purchasing

department

Purchase Order

Inventory

subsidiary ledger

System flowchart of purchases system

Processes involved in purchases system of Adam & Co

Purchases system is a composition of processes that are utilized by an entity to attain goods and

services at a given period. The above system involves assessing the goods and services that are

Vendor

Cash disbursement voucher

General Ledger

Accounts Payable

department

Inventory

warehouse

Receiving

department

Purchase Clerk

Purchasing

department

Purchase Order

Inventory

subsidiary ledger

Accounting Information System 6

available at a company before making purchasing decisions. Just like any other company, Adam

& Co made use of its employees and departments to ensure that the purchasing processes are

systematically executed to obtain desired goods and services. All processes involved in

purchases systems of any company require step by step descriptions that deliver a meaningful

interpretation of how an entity can buy its goods and services. Basing on the case under

consideration, an inventory subsidiary ledger is a tool that is used at Adam & Co to determine

the need to purchase particular goods and services to achieve desired business goals and

objectives (Nathan 2019). The above role is executed by a purchasing clerk who visits his

computer terminal every morning to identify items whose quantity gas significantly reduced and

thus need to be replenished.

Having recognized and identified the need to replenish identified items, the clerk

considers approval list of vendors as a source alternative to select the most appropriate vendor

whom digital purchase orders are forwarded to. Also, purchasing clerk goes on to advance

printed copies to selected vendors and purchasing department. Receiving department plays a

clarification function by ensuring that received goods and services conform to the information

specified in packing slip and digital purchase order. As such, conformity reports that are

generated by receiving departments are provided to the inventory warehouse, accounts receivable

department and as well a copy of these report are retained at the receivable department. Upon

receiving the above report, accounts payable clerk awaits the supplier's invoice. After receiving

the invoice from supplier, accounts payable clerk reconciles and updates the digital purchase

order, supplier's invoice, and reports that are got from the receivables department in his general

ledger. Ultimately, the accounts payable clerk delivers copies of purchase order copy, receiving

the report, invoices to the department of cash disbursement (Pierre & Nikitin 2009 p.152).

available at a company before making purchasing decisions. Just like any other company, Adam

& Co made use of its employees and departments to ensure that the purchasing processes are

systematically executed to obtain desired goods and services. All processes involved in

purchases systems of any company require step by step descriptions that deliver a meaningful

interpretation of how an entity can buy its goods and services. Basing on the case under

consideration, an inventory subsidiary ledger is a tool that is used at Adam & Co to determine

the need to purchase particular goods and services to achieve desired business goals and

objectives (Nathan 2019). The above role is executed by a purchasing clerk who visits his

computer terminal every morning to identify items whose quantity gas significantly reduced and

thus need to be replenished.

Having recognized and identified the need to replenish identified items, the clerk

considers approval list of vendors as a source alternative to select the most appropriate vendor

whom digital purchase orders are forwarded to. Also, purchasing clerk goes on to advance

printed copies to selected vendors and purchasing department. Receiving department plays a

clarification function by ensuring that received goods and services conform to the information

specified in packing slip and digital purchase order. As such, conformity reports that are

generated by receiving departments are provided to the inventory warehouse, accounts receivable

department and as well a copy of these report are retained at the receivable department. Upon

receiving the above report, accounts payable clerk awaits the supplier's invoice. After receiving

the invoice from supplier, accounts payable clerk reconciles and updates the digital purchase

order, supplier's invoice, and reports that are got from the receivables department in his general

ledger. Ultimately, the accounts payable clerk delivers copies of purchase order copy, receiving

the report, invoices to the department of cash disbursement (Pierre & Nikitin 2009 p.152).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Information System 7

Risks associated with purchases system of Adam & Co

There are fraud risks particularly regarding the purchasing systems at Adam & Co as there are no

specifications for items to be purchased, their quantities as well as particulars of selected vendors

by purchasing clerk. As such, there exist high prospects of fraud by the purchasing clerk since he

is solely responsible for initiating the purchasing processes at Adam & Co. In this case, fraud

may be exhibited in the form of bribery to attain supply contracts among vendors, and as well the

purchasing clerk may exaggerate figures regarding units of items to be purchased. As a result,

there exists a high risk of purchasing clerk exercising his personal interests over the interests of

the company during the initiation of purchasing processes (Mahhaden 2013).

Internal control weaknesses involved in purchases system of Adam & Co

There exists an internal weakness in communication among the departments, particularly when

reports from the receivable department are sent to the accounts payable departments.

Evidentially, accounts payable clerk cannot proceed to make statement reconciliations and

updates unless the invoice from the supplier is received. As a result, there exists a risk of time

mismanagement which may lead to deficiencies in supply, especially when invoices from the

supplier are not timely delivered to accounts payable clerk (William & Jay 2010).

Risks associated with purchases system of Adam & Co

There are fraud risks particularly regarding the purchasing systems at Adam & Co as there are no

specifications for items to be purchased, their quantities as well as particulars of selected vendors

by purchasing clerk. As such, there exist high prospects of fraud by the purchasing clerk since he

is solely responsible for initiating the purchasing processes at Adam & Co. In this case, fraud

may be exhibited in the form of bribery to attain supply contracts among vendors, and as well the

purchasing clerk may exaggerate figures regarding units of items to be purchased. As a result,

there exists a high risk of purchasing clerk exercising his personal interests over the interests of

the company during the initiation of purchasing processes (Mahhaden 2013).

Internal control weaknesses involved in purchases system of Adam & Co

There exists an internal weakness in communication among the departments, particularly when

reports from the receivable department are sent to the accounts payable departments.

Evidentially, accounts payable clerk cannot proceed to make statement reconciliations and

updates unless the invoice from the supplier is received. As a result, there exists a risk of time

mismanagement which may lead to deficiencies in supply, especially when invoices from the

supplier are not timely delivered to accounts payable clerk (William & Jay 2010).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Information System 8

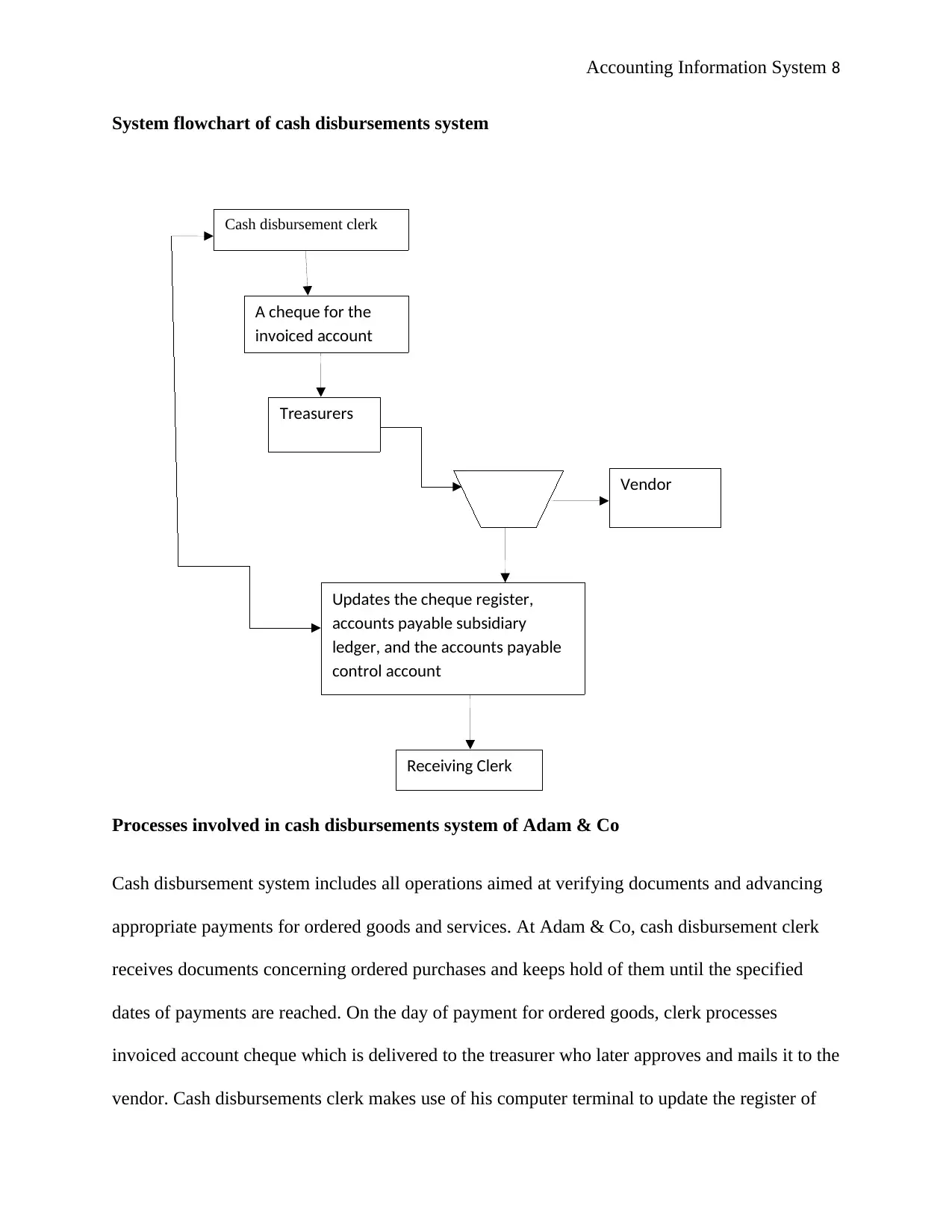

System flowchart of cash disbursements system

Processes involved in cash disbursements system of Adam & Co

Cash disbursement system includes all operations aimed at verifying documents and advancing

appropriate payments for ordered goods and services. At Adam & Co, cash disbursement clerk

receives documents concerning ordered purchases and keeps hold of them until the specified

dates of payments are reached. On the day of payment for ordered goods, clerk processes

invoiced account cheque which is delivered to the treasurer who later approves and mails it to the

vendor. Cash disbursements clerk makes use of his computer terminal to update the register of

Cash disbursement clerk

A cheque for the

invoiced account

Treasurers

Vendor

Updates the cheque register,

accounts payable subsidiary

ledger, and the accounts payable

control account

Receiving Clerk

System flowchart of cash disbursements system

Processes involved in cash disbursements system of Adam & Co

Cash disbursement system includes all operations aimed at verifying documents and advancing

appropriate payments for ordered goods and services. At Adam & Co, cash disbursement clerk

receives documents concerning ordered purchases and keeps hold of them until the specified

dates of payments are reached. On the day of payment for ordered goods, clerk processes

invoiced account cheque which is delivered to the treasurer who later approves and mails it to the

vendor. Cash disbursements clerk makes use of his computer terminal to update the register of

Cash disbursement clerk

A cheque for the

invoiced account

Treasurers

Vendor

Updates the cheque register,

accounts payable subsidiary

ledger, and the accounts payable

control account

Receiving Clerk

Accounting Information System 9

cheques, accounts payable control account and accounts payable subsidiary ledger. Ultimately,

the whole system of cash disbursement ends when the receiving clerk documents purchase order

copy, invoice, cheque copy, and receiving the report (Luke 2017 p.40).

Risks associated with cash disbursements system of Adam & Co

There exist a risk omitted amounts, notably when errors are exhibited in the accounts payable

department. The above is attributed to the fact that the cash disbursement process relies on

documentation from the accounts payable department. As such, there exist high risks of

inaccuracy when errors of omission are committed in the aforementioned department as they

cannot be rectified in the cash disbursements system (Mahhaden 2013).

Internal weaknesses associated with cash disbursement system of Adam & Co

Authorization of actual payments is one of the internal weaknesses at Adam & Co as the process

does not consider management members like board of directors or managing directors. Instead,

the authorization process for actual cash payments is done upon authorization by cash

disbursements clerk and treasurer at the company. More so, bank accounts on which the cash

payments may be advanced may be in the names of the board of directors and thus would need

their authorization. As a result, excluding management members in the process of authorizing

actual payment increases the risk of no payment of cheques due to lack of signatures from

authorized approvers of cheques (William & Jay 2010).

cheques, accounts payable control account and accounts payable subsidiary ledger. Ultimately,

the whole system of cash disbursement ends when the receiving clerk documents purchase order

copy, invoice, cheque copy, and receiving the report (Luke 2017 p.40).

Risks associated with cash disbursements system of Adam & Co

There exist a risk omitted amounts, notably when errors are exhibited in the accounts payable

department. The above is attributed to the fact that the cash disbursement process relies on

documentation from the accounts payable department. As such, there exist high risks of

inaccuracy when errors of omission are committed in the aforementioned department as they

cannot be rectified in the cash disbursements system (Mahhaden 2013).

Internal weaknesses associated with cash disbursement system of Adam & Co

Authorization of actual payments is one of the internal weaknesses at Adam & Co as the process

does not consider management members like board of directors or managing directors. Instead,

the authorization process for actual cash payments is done upon authorization by cash

disbursements clerk and treasurer at the company. More so, bank accounts on which the cash

payments may be advanced may be in the names of the board of directors and thus would need

their authorization. As a result, excluding management members in the process of authorizing

actual payment increases the risk of no payment of cheques due to lack of signatures from

authorized approvers of cheques (William & Jay 2010).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Information System 10

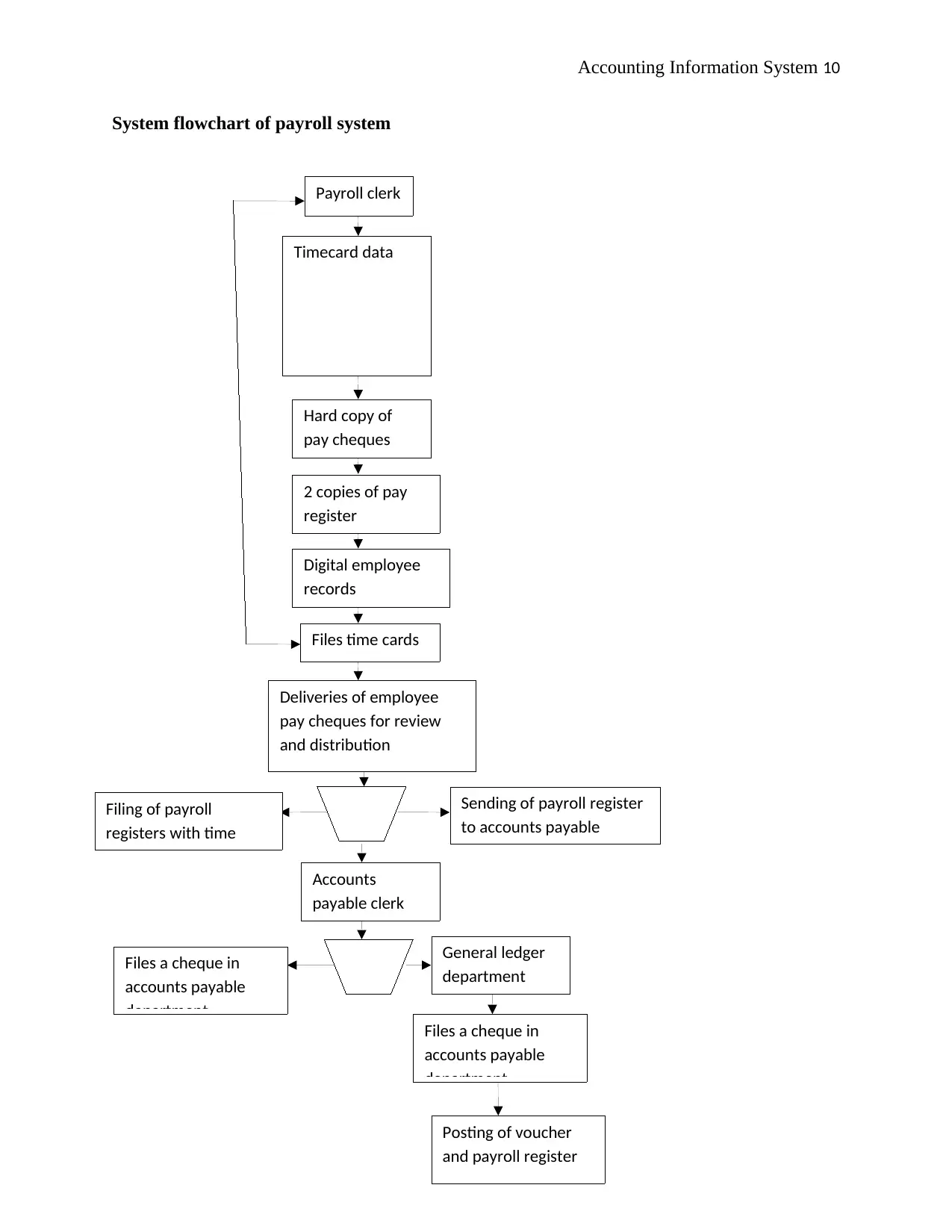

System flowchart of payroll system

Sending of payroll register

to accounts payable

department

Filing of payroll

registers with time

cards

Accounts

payable clerk

General ledger

department

Files a cheque in

accounts payable

department

Files a cheque in

accounts payable

department

Posting of voucher

and payroll register

Files time cards

Timecard data

Hard copy of

pay cheques

2 copies of pay

register

Digital employee

records

Payroll clerk

Deliveries of employee

pay cheques for review

and distribution

System flowchart of payroll system

Sending of payroll register

to accounts payable

department

Filing of payroll

registers with time

cards

Accounts

payable clerk

General ledger

department

Files a cheque in

accounts payable

department

Files a cheque in

accounts payable

department

Posting of voucher

and payroll register

Files time cards

Timecard data

Hard copy of

pay cheques

2 copies of pay

register

Digital employee

records

Payroll clerk

Deliveries of employee

pay cheques for review

and distribution

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Information System 11

Processes involved in the payroll system of Adam & Co

Employees at Adam & Co make use of time cards to record the number of hours they have

worked for on a daily basis. Time cards offer pivotal information to the supervisors regarding the

attendance of employees whereby corrections are made, and records are sent to the payroll

department at the end of every week. Thereafter, the payroll department makes use of its

computer terminals to input data from time cards so as to aid the process of printing pay cheques,

digital employee records, and payroll registers. Payroll clerk documents time cards and delivers

pay cheques of employees to a number of supervisors at the company. Supervisors make a

review of the received pay cheques of employees so as to rectify any issues and later distribute

them to employees who work under various departments (Luke 2017 p.40). In addition, the

payroll clerk then makes two copies of the payroll register and delivers them to the payroll

department and accounts payable departments. A disbursement voucher is prepared by accounts

payable clerk after making thorough reviews of payroll register that later send these two

documents to the general ledger department. Additionally, a cheque is written and deposited in

imprest account by accounts payable clerk who later retains a copy of the aforementioned cheque

at the accounts payable department. Ultimately, the general ledger clerk utilizes his computer

terminal to file payroll register and voucher in the general ledger department upon receiving the

aforementioned documents from accounts payable clerk (Nathan 2019).

Risks involved in payroll system of Adam & Co

Given that the number of hours worked by employees is recorded by use of time cards, there are

likely to be high risks of incorrect documentation due to manual entry of records by supervisors

and employees. At the time, such errors may arise when computer systems are associated with

Processes involved in the payroll system of Adam & Co

Employees at Adam & Co make use of time cards to record the number of hours they have

worked for on a daily basis. Time cards offer pivotal information to the supervisors regarding the

attendance of employees whereby corrections are made, and records are sent to the payroll

department at the end of every week. Thereafter, the payroll department makes use of its

computer terminals to input data from time cards so as to aid the process of printing pay cheques,

digital employee records, and payroll registers. Payroll clerk documents time cards and delivers

pay cheques of employees to a number of supervisors at the company. Supervisors make a

review of the received pay cheques of employees so as to rectify any issues and later distribute

them to employees who work under various departments (Luke 2017 p.40). In addition, the

payroll clerk then makes two copies of the payroll register and delivers them to the payroll

department and accounts payable departments. A disbursement voucher is prepared by accounts

payable clerk after making thorough reviews of payroll register that later send these two

documents to the general ledger department. Additionally, a cheque is written and deposited in

imprest account by accounts payable clerk who later retains a copy of the aforementioned cheque

at the accounts payable department. Ultimately, the general ledger clerk utilizes his computer

terminal to file payroll register and voucher in the general ledger department upon receiving the

aforementioned documents from accounts payable clerk (Nathan 2019).

Risks involved in payroll system of Adam & Co

Given that the number of hours worked by employees is recorded by use of time cards, there are

likely to be high risks of incorrect documentation due to manual entry of records by supervisors

and employees. At the time, such errors may arise when computer systems are associated with

Accounting Information System 12

faults that may lead to miscalculations. As a result, inaccuracies during documentation and

calculation of a number of hours worked by employees are likely to lead to an inaccurate

paycheck. Also, it may lead to deficiencies in the accrual of remunerations to all workers at

Adam & Co (Mahhaden 2013).

Internal weaknesses associated with payroll system of Adam & Co

Payroll system of Adam & Co only considers the number of hours worked by its workers as a

standard for determining advancement of salaries and wages to its employees. In this regard, the

company ignores social security, tax imposition, and other deduction on the remunerations that

are advanced unto its workers whilst preparing its payroll systems. Moreover, entities are

required to withhold taxes that are imposed on salaries and wages of their employees and also

make deposits whilst relying on the magnitude of return. As such, there exists a high risk of

failing to make timely deposits to internal revenue service, which may lead to fines and penalties

(William & Jay 2010). Therefore, Adam & Co is exposed to a risk of losing significant volumes

of finances to internal revenue service in the form of penalties and fines arising from delayed

deposits.

Conclusion

Expenditure cycle at Adam & Co is quite critical in that it directly deals with purchases, cash

disbursements, and payroll systems. As such, mishandling of the processes that take place in all

the aforementioned systems may hinder the company from achieving its desired business

objectives and goals. The above claim is attributed to the fact that the above systems directly

deal with the financial resources of Adam & Co. Most significantly, the company has clearly

stipulated departments and employees who collaboratively execute all necessary documentation

faults that may lead to miscalculations. As a result, inaccuracies during documentation and

calculation of a number of hours worked by employees are likely to lead to an inaccurate

paycheck. Also, it may lead to deficiencies in the accrual of remunerations to all workers at

Adam & Co (Mahhaden 2013).

Internal weaknesses associated with payroll system of Adam & Co

Payroll system of Adam & Co only considers the number of hours worked by its workers as a

standard for determining advancement of salaries and wages to its employees. In this regard, the

company ignores social security, tax imposition, and other deduction on the remunerations that

are advanced unto its workers whilst preparing its payroll systems. Moreover, entities are

required to withhold taxes that are imposed on salaries and wages of their employees and also

make deposits whilst relying on the magnitude of return. As such, there exists a high risk of

failing to make timely deposits to internal revenue service, which may lead to fines and penalties

(William & Jay 2010). Therefore, Adam & Co is exposed to a risk of losing significant volumes

of finances to internal revenue service in the form of penalties and fines arising from delayed

deposits.

Conclusion

Expenditure cycle at Adam & Co is quite critical in that it directly deals with purchases, cash

disbursements, and payroll systems. As such, mishandling of the processes that take place in all

the aforementioned systems may hinder the company from achieving its desired business

objectives and goals. The above claim is attributed to the fact that the above systems directly

deal with the financial resources of Adam & Co. Most significantly, the company has clearly

stipulated departments and employees who collaboratively execute all necessary documentation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.