HA2042 Accounting Information Systems: Case Study of Adam & Co

VerifiedAdded on 2022/11/17

|12

|3011

|73

Case Study

AI Summary

This case study analyzes Adam & Co, a wholesaler, focusing on its expenditure cycle, including purchase, cash disbursement, and payroll systems. The assignment presents system flowcharts for each department, detailing the processes and identifying key checkpoints. The analysis reveals weaknesses in the internal control systems, such as manual processes, lack of centralized systems, and potential for errors and fraud. The purchase system's reliance on hard copies and manual reconciliation increases the risk of errors and fraud. The cash disbursement system's lack of centralized computer systems makes it prone to errors and fraud. The payroll system's reliance on manual input and review exposes it to potential inaccuracies and fraud. The report aims to evaluate the risks and internal control processes within Adam & Co, identifying areas for improvement and suggesting measures to strengthen the company's financial controls.

Running head: CASE STUDY- ADAM & CO

Case study- Adam & Co

Name of the Student

Name of the University

Author Note

Executive summary:

The report is prepared to evaluate the risk and internal control process in terms of its

strength and weakness. The analysis is based on the case study presented on the

company Adam and Co. The three department of Adam and Co has been separately

analyzed using the system flow chart that depicts the process in identified steps.

These departments include purchase department, payroll department and cash

disbursement department. The later part of the report depicts the description of the

weakness of internal control system of each departments.

Case study- Adam & Co

Name of the Student

Name of the University

Author Note

Executive summary:

The report is prepared to evaluate the risk and internal control process in terms of its

strength and weakness. The analysis is based on the case study presented on the

company Adam and Co. The three department of Adam and Co has been separately

analyzed using the system flow chart that depicts the process in identified steps.

These departments include purchase department, payroll department and cash

disbursement department. The later part of the report depicts the description of the

weakness of internal control system of each departments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CASE STUDY- ADAM & CO

Table of Contents

Introduction:..................................................................................................................2

Discussion:...................................................................................................................2

System flow chart of purchase system:........................................................................2

System flow chart of cash disbursement system:........................................................2

System flow chart of payroll system:............................................................................2

Identifying the internal control weakness in the system and its associated risks:.......2

Conclusion:...................................................................................................................2

Reference list:...............................................................................................................3

Table of Contents

Introduction:..................................................................................................................2

Discussion:...................................................................................................................2

System flow chart of purchase system:........................................................................2

System flow chart of cash disbursement system:........................................................2

System flow chart of payroll system:............................................................................2

Identifying the internal control weakness in the system and its associated risks:.......2

Conclusion:...................................................................................................................2

Reference list:...............................................................................................................3

CASE STUDY- ADAM & CO

Introduction:

The report is prepared to be presented to the managing director of Adam &

Co evaluating the risks, process and internal control of the expenditure cycle of the

company. Adam and Co is a wholesaler of supplies which source its inventories from

different countries such as Thailand, China and Vietnam. The procedure of

expenditure cycle of the company comprised of purchase system, cash

disbursement and payroll system. The risks, process and the weakness associated

with the internal control of the different systems of the company has been evaluated.

The process different systems of has been understood with the help of flow chart

which helps in evaluating the state of the current situation for further improvement

(Salimi et al. 2016).

Discussion:

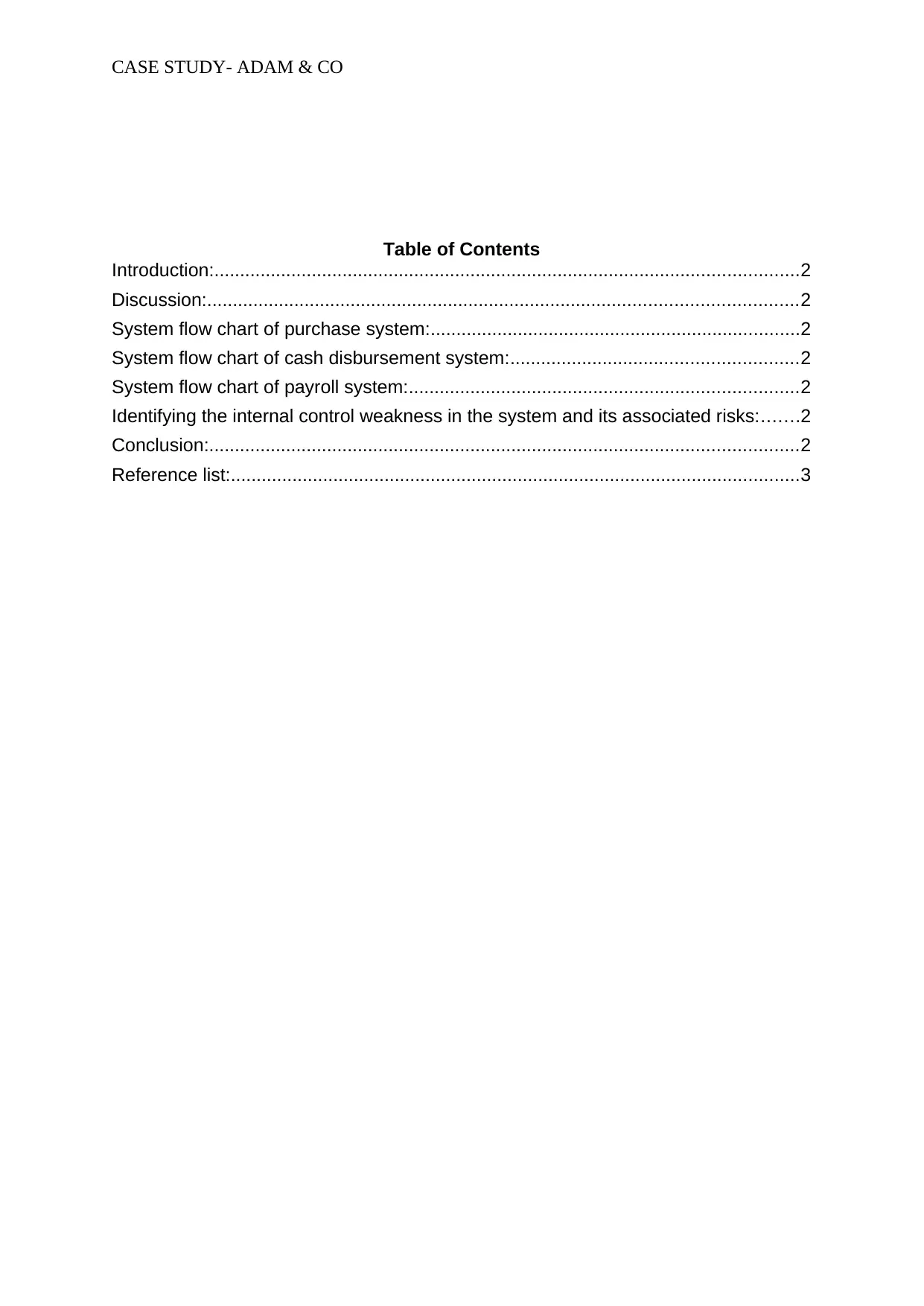

System flow chart of purchase system:

The system of purchase involves the journey from the creation of purchase

order through the approval of purchase order, delivery, invoicing and closure and the

purchase order becomes a legally binding document if the purchase order is

accepted by the vendor. The process of the purchase order comprise of various

checkpoints and approval of the tasks of input for ensuing that the processing of

purchase order is done timely. Hence, purchase system initiates with the

identification of the need of inventory, placing the order, receiving inventory and

recognizing the liability. The depletion of inventories is done by selling the finished

goods. A digital purchase order is prepared by the purchasing clerk when the level of

inventories drop below the predetermined point and the purchase order is made to

the vendor after they are chosen from the vendor file. The purchase order process

initiated when the copy of purchase order is send to vendor as well as to the

purchasing department and the purchase order file has the digital record of purchase

being done (Apostolou et al. 2017).

The process of purchase order can be made efficient if much of the routine

ordering information needed by the purchasing department from the valid vendor file

and inventory is supplied by the inventory control function. In the next step of the

purchase process, the receiving department receives the goods that has been

ordered. The information presented in the digital purchase order and the purchasing

slip is reconciled against the goods received by the receiving clerk and this is done

after inspection. Two hard copies of receiving reports is manually prepared by the

receiving clerk. Receiving report is filed by the clerk in the department after the

inventory subsidiary ledger has been updated and the goods are shelved. The

accounts payable department receives the other copy of the receiving report where

the filing is done until the arrival of the invoice from supplier. Accounts payable clerk

is also responsible for reconciling the three documents that is hard copy of digital

purchase order, invoice from suppliers and receiving report. In addition to this, the

digital accounts payable subsidiary ledger, inventory control account and the

accounts payable control account is updated by the accounts payable clerk in the

general ledger. The step of purchase process is completed after the receiving report,

Introduction:

The report is prepared to be presented to the managing director of Adam &

Co evaluating the risks, process and internal control of the expenditure cycle of the

company. Adam and Co is a wholesaler of supplies which source its inventories from

different countries such as Thailand, China and Vietnam. The procedure of

expenditure cycle of the company comprised of purchase system, cash

disbursement and payroll system. The risks, process and the weakness associated

with the internal control of the different systems of the company has been evaluated.

The process different systems of has been understood with the help of flow chart

which helps in evaluating the state of the current situation for further improvement

(Salimi et al. 2016).

Discussion:

System flow chart of purchase system:

The system of purchase involves the journey from the creation of purchase

order through the approval of purchase order, delivery, invoicing and closure and the

purchase order becomes a legally binding document if the purchase order is

accepted by the vendor. The process of the purchase order comprise of various

checkpoints and approval of the tasks of input for ensuing that the processing of

purchase order is done timely. Hence, purchase system initiates with the

identification of the need of inventory, placing the order, receiving inventory and

recognizing the liability. The depletion of inventories is done by selling the finished

goods. A digital purchase order is prepared by the purchasing clerk when the level of

inventories drop below the predetermined point and the purchase order is made to

the vendor after they are chosen from the vendor file. The purchase order process

initiated when the copy of purchase order is send to vendor as well as to the

purchasing department and the purchase order file has the digital record of purchase

being done (Apostolou et al. 2017).

The process of purchase order can be made efficient if much of the routine

ordering information needed by the purchasing department from the valid vendor file

and inventory is supplied by the inventory control function. In the next step of the

purchase process, the receiving department receives the goods that has been

ordered. The information presented in the digital purchase order and the purchasing

slip is reconciled against the goods received by the receiving clerk and this is done

after inspection. Two hard copies of receiving reports is manually prepared by the

receiving clerk. Receiving report is filed by the clerk in the department after the

inventory subsidiary ledger has been updated and the goods are shelved. The

accounts payable department receives the other copy of the receiving report where

the filing is done until the arrival of the invoice from supplier. Accounts payable clerk

is also responsible for reconciling the three documents that is hard copy of digital

purchase order, invoice from suppliers and receiving report. In addition to this, the

digital accounts payable subsidiary ledger, inventory control account and the

accounts payable control account is updated by the accounts payable clerk in the

general ledger. The step of purchase process is completed after the receiving report,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CASE STUDY- ADAM & CO

invoice and the purchase order copy is send to the cash disbursement department

(Loo and Bots 2018).

invoice and the purchase order copy is send to the cash disbursement department

(Loo and Bots 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Purchasing

department Receiving department Accounts payable

department

Monitoring inventory records

Inventory levels

Preparing digital purchase order

Choosing a vendor

Sending to vendor

Filing in the department

Preparing two hard copies

Adding to purchase order file

Receive goods

Reconciliation and inspection

Hard copies of receiving report

Manual preparation of receiving report

Inventory warehouse

Updating inventory subsidiary ledger

Filing of the report

Filing of the report

Arrival of supplier’s invoice

Printing digital purchase order hard copy

Digital purchase order, supplier’s invoice and receiving repo

Reconciliation

General ledger

Updating of accounts

payable, accounts payable

subsidiary ledger and

inventory control account

Cash disbursement department

CASE STUDY- ADAM & CO

Chart 1: System flowchart of purchase system

Source: created by author

The above flowchart depicts the whole process of purchase system of Adam

and Co.

department Receiving department Accounts payable

department

Monitoring inventory records

Inventory levels

Preparing digital purchase order

Choosing a vendor

Sending to vendor

Filing in the department

Preparing two hard copies

Adding to purchase order file

Receive goods

Reconciliation and inspection

Hard copies of receiving report

Manual preparation of receiving report

Inventory warehouse

Updating inventory subsidiary ledger

Filing of the report

Filing of the report

Arrival of supplier’s invoice

Printing digital purchase order hard copy

Digital purchase order, supplier’s invoice and receiving repo

Reconciliation

General ledger

Updating of accounts

payable, accounts payable

subsidiary ledger and

inventory control account

Cash disbursement department

CASE STUDY- ADAM & CO

Chart 1: System flowchart of purchase system

Source: created by author

The above flowchart depicts the whole process of purchase system of Adam

and Co.

Filing of the documents received

Until the due date

Cash disbursement clerk

Preparing a cheque

Invoiced account

Treasurer

Vendor

Sign

Updating

Receiving clerk

Purchase order copy, invoice, cheque copy and receiving report

Filing

CASE STUDY- ADAM & CO

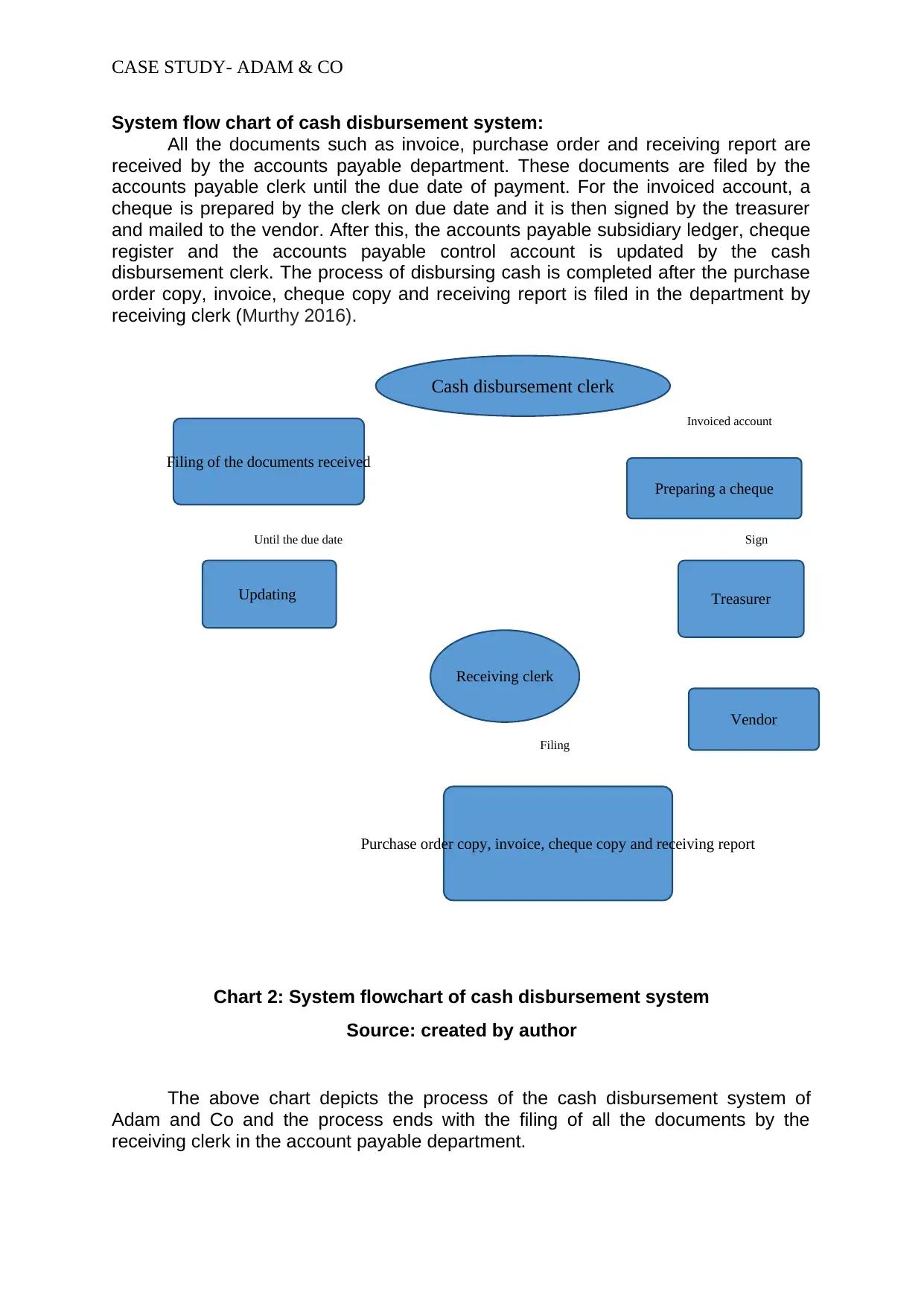

System flow chart of cash disbursement system:

All the documents such as invoice, purchase order and receiving report are

received by the accounts payable department. These documents are filed by the

accounts payable clerk until the due date of payment. For the invoiced account, a

cheque is prepared by the clerk on due date and it is then signed by the treasurer

and mailed to the vendor. After this, the accounts payable subsidiary ledger, cheque

register and the accounts payable control account is updated by the cash

disbursement clerk. The process of disbursing cash is completed after the purchase

order copy, invoice, cheque copy and receiving report is filed in the department by

receiving clerk (Murthy 2016).

Chart 2: System flowchart of cash disbursement system

Source: created by author

The above chart depicts the process of the cash disbursement system of

Adam and Co and the process ends with the filing of all the documents by the

receiving clerk in the account payable department.

Until the due date

Cash disbursement clerk

Preparing a cheque

Invoiced account

Treasurer

Vendor

Sign

Updating

Receiving clerk

Purchase order copy, invoice, cheque copy and receiving report

Filing

CASE STUDY- ADAM & CO

System flow chart of cash disbursement system:

All the documents such as invoice, purchase order and receiving report are

received by the accounts payable department. These documents are filed by the

accounts payable clerk until the due date of payment. For the invoiced account, a

cheque is prepared by the clerk on due date and it is then signed by the treasurer

and mailed to the vendor. After this, the accounts payable subsidiary ledger, cheque

register and the accounts payable control account is updated by the cash

disbursement clerk. The process of disbursing cash is completed after the purchase

order copy, invoice, cheque copy and receiving report is filed in the department by

receiving clerk (Murthy 2016).

Chart 2: System flowchart of cash disbursement system

Source: created by author

The above chart depicts the process of the cash disbursement system of

Adam and Co and the process ends with the filing of all the documents by the

receiving clerk in the account payable department.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CASE STUDY- ADAM & CO

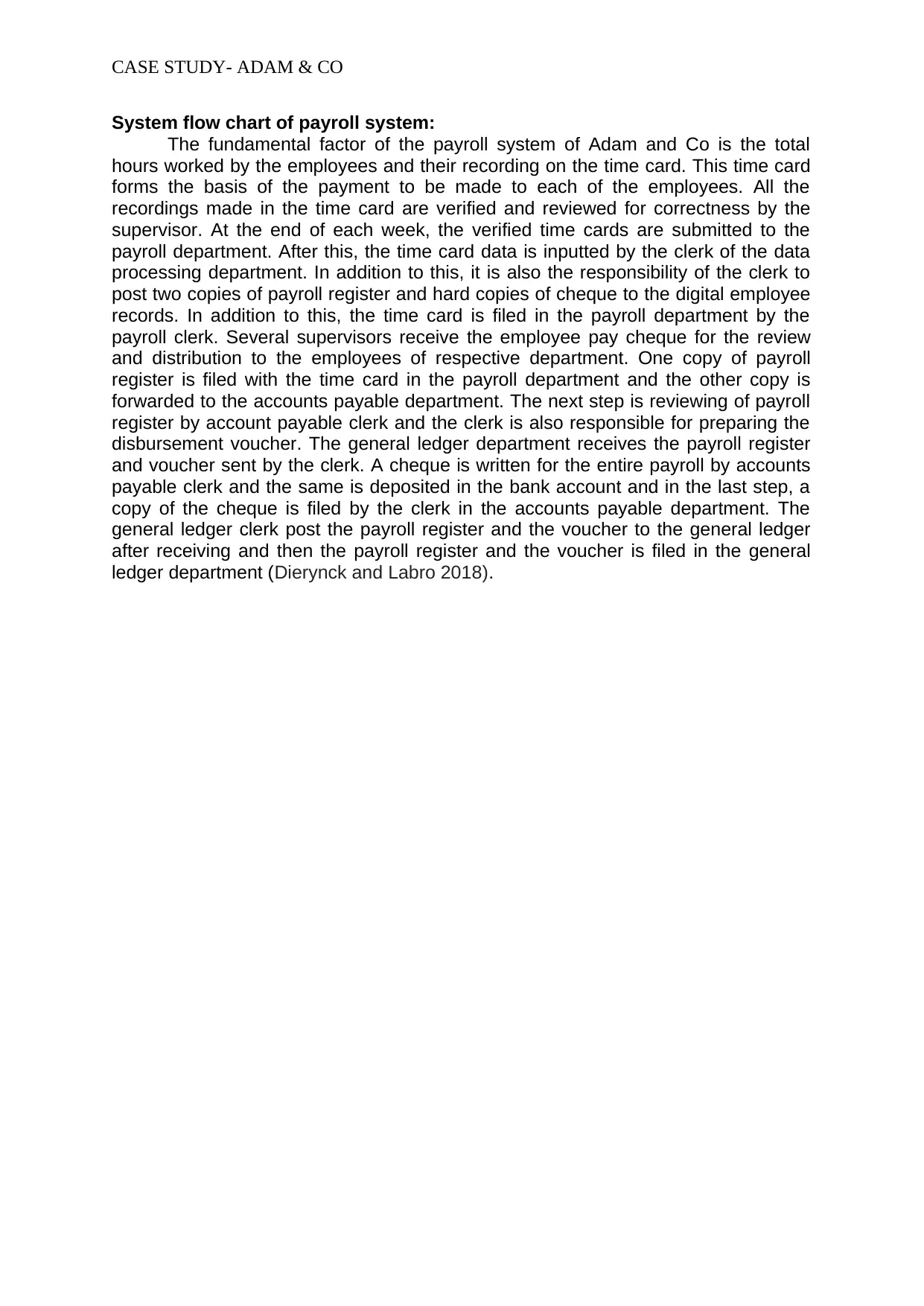

System flow chart of payroll system:

The fundamental factor of the payroll system of Adam and Co is the total

hours worked by the employees and their recording on the time card. This time card

forms the basis of the payment to be made to each of the employees. All the

recordings made in the time card are verified and reviewed for correctness by the

supervisor. At the end of each week, the verified time cards are submitted to the

payroll department. After this, the time card data is inputted by the clerk of the data

processing department. In addition to this, it is also the responsibility of the clerk to

post two copies of payroll register and hard copies of cheque to the digital employee

records. In addition to this, the time card is filed in the payroll department by the

payroll clerk. Several supervisors receive the employee pay cheque for the review

and distribution to the employees of respective department. One copy of payroll

register is filed with the time card in the payroll department and the other copy is

forwarded to the accounts payable department. The next step is reviewing of payroll

register by account payable clerk and the clerk is also responsible for preparing the

disbursement voucher. The general ledger department receives the payroll register

and voucher sent by the clerk. A cheque is written for the entire payroll by accounts

payable clerk and the same is deposited in the bank account and in the last step, a

copy of the cheque is filed by the clerk in the accounts payable department. The

general ledger clerk post the payroll register and the voucher to the general ledger

after receiving and then the payroll register and the voucher is filed in the general

ledger department (Dierynck and Labro 2018).

System flow chart of payroll system:

The fundamental factor of the payroll system of Adam and Co is the total

hours worked by the employees and their recording on the time card. This time card

forms the basis of the payment to be made to each of the employees. All the

recordings made in the time card are verified and reviewed for correctness by the

supervisor. At the end of each week, the verified time cards are submitted to the

payroll department. After this, the time card data is inputted by the clerk of the data

processing department. In addition to this, it is also the responsibility of the clerk to

post two copies of payroll register and hard copies of cheque to the digital employee

records. In addition to this, the time card is filed in the payroll department by the

payroll clerk. Several supervisors receive the employee pay cheque for the review

and distribution to the employees of respective department. One copy of payroll

register is filed with the time card in the payroll department and the other copy is

forwarded to the accounts payable department. The next step is reviewing of payroll

register by account payable clerk and the clerk is also responsible for preparing the

disbursement voucher. The general ledger department receives the payroll register

and voucher sent by the clerk. A cheque is written for the entire payroll by accounts

payable clerk and the same is deposited in the bank account and in the last step, a

copy of the cheque is filed by the clerk in the accounts payable department. The

general ledger clerk post the payroll register and the voucher to the general ledger

after receiving and then the payroll register and the voucher is filed in the general

ledger department (Dierynck and Labro 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Supervisor Department of

Payroll

Department of

Accounts payable Department of

general ledger

Time card is reviewed for correctness

Reviewing Employee pay cheque

Employee cheque are distributed to different departments

Time card data is inputted

Hard copies of pay cheque are printed

Two copies of payroll register

Filing one copy of payroll with the time card

Clerk reviews the register

Disbursement voucher is prepared

Clerk Writes the cheque

Depositing in the bank account

Cheque copy is filed

Posting to general ledge

Filing in the department

CASE STUDY- ADAM & CO

Chart 2: System flowchart of payroll system

Source: created by author

Description of the weakness in the internal control of system and its

associated risks:

The weakness which are faced by the purchase system of Adam and Co are listed

here as under:

There is a manual preparation of the receiving reports which are in the form of

hard copies of the goods.

Payroll

Department of

Accounts payable Department of

general ledger

Time card is reviewed for correctness

Reviewing Employee pay cheque

Employee cheque are distributed to different departments

Time card data is inputted

Hard copies of pay cheque are printed

Two copies of payroll register

Filing one copy of payroll with the time card

Clerk reviews the register

Disbursement voucher is prepared

Clerk Writes the cheque

Depositing in the bank account

Cheque copy is filed

Posting to general ledge

Filing in the department

CASE STUDY- ADAM & CO

Chart 2: System flowchart of payroll system

Source: created by author

Description of the weakness in the internal control of system and its

associated risks:

The weakness which are faced by the purchase system of Adam and Co are listed

here as under:

There is a manual preparation of the receiving reports which are in the form of

hard copies of the goods.

CASE STUDY- ADAM & CO

Only until the invoice of the supplied goods in arrived the account payable

clerk files the receiving report. Thereby, it becomes a time consuming task to

fill in the receiving reports at that point of time.

Consequently, it can be said that the company has a low or poor records for

the intake as well as the records and the needs of the goods. The subordinate

employees are not found to question the incorrect transactions within the company.

Apart from this, also it can be said that by making the record of the receiving report

in the form of a hardcopy it becomes very hectic and also the chances of fraudulence

of the total amount of the goods might also occur (Chiu et al. 2019). As, it is

manually entered, thereby increasing the risk of errors might also be faced thereby

reducing the strength of the internal control of the purchase system.

The evaluation of the Adam and Co. and the internal control of the cash

distribution system has be done in terms of its effectiveness and it can be further

explained as follows:

The documents which are obtained for verification purpose also does not

suffice as received by the treasurer prior to the signing and mailing as the

system of the distribution of the cash also faces problems.

These factors are also found to pay way to the occurrence of fraud as the

figures which are mentioned on the cheque also might be misappropriate or

incorrect. The system of a centralized computer must be practiced so as avoid the

mistakes or the errors. Also in case there is centralized system record can help

detect the fraud activities that can easily be tracked, as a result of which the

transparency can be maintained (Ahmed et al. 2017).

The below listed factors are drawbacks which are faced by the payroll system

of the Adam and Co. and it can be explained here as under:

There is scarcity of the task distribution amongst the accounts department,

starting from the data input task to time card data, printing of the hard copies

of the payroll register and the cheque and also the posting of all the record

are done by a single person that is the account clerk. So, this increases the

risk of fraudulence or data mismatch.

Furthermore, the disbursement coupon or the voucher is prepared manually

which might result in the probability of occurrence of the mistakes. It can also

be found out that one of the major reasons of the fraudulence to happen might

be because of the lack of monitoring the transactions and also the

preparations of the documents for verifications, consequently, the reliability is

endangered. Additionally the procedure of the documentation is not

established properly thereby leading to an increase in the occurrence of

mistakes during the transactions verifications by the clerks (Pearlson et al.

2016).

Conclusion:

The above discussions briefly explains the risks which are associated with the

internal control system of the Adam and Co. expenditure cycle .The categorized

three departments that is the purchase system, the cash distribution system and the

payroll system has been taken into consideration for evaluating its efficiency and

effectiveness. The process of all the three departments has been explained by

Only until the invoice of the supplied goods in arrived the account payable

clerk files the receiving report. Thereby, it becomes a time consuming task to

fill in the receiving reports at that point of time.

Consequently, it can be said that the company has a low or poor records for

the intake as well as the records and the needs of the goods. The subordinate

employees are not found to question the incorrect transactions within the company.

Apart from this, also it can be said that by making the record of the receiving report

in the form of a hardcopy it becomes very hectic and also the chances of fraudulence

of the total amount of the goods might also occur (Chiu et al. 2019). As, it is

manually entered, thereby increasing the risk of errors might also be faced thereby

reducing the strength of the internal control of the purchase system.

The evaluation of the Adam and Co. and the internal control of the cash

distribution system has be done in terms of its effectiveness and it can be further

explained as follows:

The documents which are obtained for verification purpose also does not

suffice as received by the treasurer prior to the signing and mailing as the

system of the distribution of the cash also faces problems.

These factors are also found to pay way to the occurrence of fraud as the

figures which are mentioned on the cheque also might be misappropriate or

incorrect. The system of a centralized computer must be practiced so as avoid the

mistakes or the errors. Also in case there is centralized system record can help

detect the fraud activities that can easily be tracked, as a result of which the

transparency can be maintained (Ahmed et al. 2017).

The below listed factors are drawbacks which are faced by the payroll system

of the Adam and Co. and it can be explained here as under:

There is scarcity of the task distribution amongst the accounts department,

starting from the data input task to time card data, printing of the hard copies

of the payroll register and the cheque and also the posting of all the record

are done by a single person that is the account clerk. So, this increases the

risk of fraudulence or data mismatch.

Furthermore, the disbursement coupon or the voucher is prepared manually

which might result in the probability of occurrence of the mistakes. It can also

be found out that one of the major reasons of the fraudulence to happen might

be because of the lack of monitoring the transactions and also the

preparations of the documents for verifications, consequently, the reliability is

endangered. Additionally the procedure of the documentation is not

established properly thereby leading to an increase in the occurrence of

mistakes during the transactions verifications by the clerks (Pearlson et al.

2016).

Conclusion:

The above discussions briefly explains the risks which are associated with the

internal control system of the Adam and Co. expenditure cycle .The categorized

three departments that is the purchase system, the cash distribution system and the

payroll system has been taken into consideration for evaluating its efficiency and

effectiveness. The process of all the three departments has been explained by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CASE STUDY- ADAM & CO

preparing a system flow chart which helps in understanding each of the stages

properly. It can also be understood from the above discussions that the internal

control faces the weaknesses that also might rise the fraudulent activities and also

chances of mistakes by the staff members also is found to increase. One of the most

important drawback faced by this expenditure cycle is that the staffs are manually

engaged in the making and managing of the reports which in itself is a major factor

which leads to fraud. Also the lack of task segregation causes the data to be less

reliable and accurate, there is also not enough adequate data verification which

results in increase the risk of indulging in the fraud activities.

preparing a system flow chart which helps in understanding each of the stages

properly. It can also be understood from the above discussions that the internal

control faces the weaknesses that also might rise the fraudulent activities and also

chances of mistakes by the staff members also is found to increase. One of the most

important drawback faced by this expenditure cycle is that the staffs are manually

engaged in the making and managing of the reports which in itself is a major factor

which leads to fraud. Also the lack of task segregation causes the data to be less

reliable and accurate, there is also not enough adequate data verification which

results in increase the risk of indulging in the fraud activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CASE STUDY- ADAM & CO

CASE STUDY- ADAM & CO

References list:

Ahmed, A.E., El Refae, G.A. and Elkhatib, S.M., 2017. Integrating Employability

Competencies: A framework for accounting education. International Journal of

Research in Business, Economics and Management, 1(1), pp.135-144.

Apostolou, B., Dorminey, J.W., Hassell, J.M. and Rebele, J.E., 2018. Accounting

education literature review (2017). Journal of accounting education, 43, pp.1-23.

Chiu, V., Liu, Q., Muehlmann, B. and Baldwin, A.A., 2019. A bibliometric analysis of

accounting information systems journals and their emerging technologies

contributions. International Journal of Accounting Information Systems, 32, pp.24-43.

Coyne, J.G., Coyne, E.M. and Walker, K.B., 2016. A model to update accounting

curricula for emerging technologies. Journal of Emerging Technologies in

Accounting, 13(1), pp.161-169.

Dierynck, B. and Labro, E., 2018. Management accounting information properties

and operations management. Foundations and Trends® in Technology, Information

and Operations Management, 12(1), pp.1-114.

Loo, I.D. and Bots, J., 2018. The life of an accounting information systems research

course. Accounting Education, 27(4), pp.358-382.

Murthy, U.S., 2016. Researching at the intersection of accounting and information

technology: A call for action. Journal of Information systems, 30(2), pp.159-167.

Neely, P., Forsgren, N., Premuroso, R., Vician, C. and White, C.E., 2015. Accounting

Information Systems (AIS) Course Design: Current Practices and Future

Trajectories. CAIS, 36, p.30.

Pan, G., Shankararaman, V., Seow, P.S. and Tan, G.H., 2017. Designing an

accounting analytics course using experiential learning approach. Accountancy

Business and the Public Interest, 16, pp.1-23.

Pearlson, K.E., Saunders, C.S. and Galletta, D.F., 2016. Managing and using

information systems, binder ready version: a strategic approach. John Wiley & Sons.

Riley, J. and Ward, K., 2015. Active learning, cooperative active learning, and

passive learning methods in an accounting information systems course. Issues in

Accounting Education, 32(2), pp.1-16.

Salimi, A.Y., Kornelus, A. and Abo-Hebeish, A., 2016. Improvement in Accounting

Students' Perception and Judgment on Ethical Issues as They Progress Through the

Accounting Curriculum. Journal of Higher Education Theory and Practice, 16(3),

p.51.

Singh, K., 2016. Implementing Enterprise Resource Planning Education in a

Postgraduate Accounting Information Systems Course. Business Education &

Accreditation, 8(1), pp.27-37.

References list:

Ahmed, A.E., El Refae, G.A. and Elkhatib, S.M., 2017. Integrating Employability

Competencies: A framework for accounting education. International Journal of

Research in Business, Economics and Management, 1(1), pp.135-144.

Apostolou, B., Dorminey, J.W., Hassell, J.M. and Rebele, J.E., 2018. Accounting

education literature review (2017). Journal of accounting education, 43, pp.1-23.

Chiu, V., Liu, Q., Muehlmann, B. and Baldwin, A.A., 2019. A bibliometric analysis of

accounting information systems journals and their emerging technologies

contributions. International Journal of Accounting Information Systems, 32, pp.24-43.

Coyne, J.G., Coyne, E.M. and Walker, K.B., 2016. A model to update accounting

curricula for emerging technologies. Journal of Emerging Technologies in

Accounting, 13(1), pp.161-169.

Dierynck, B. and Labro, E., 2018. Management accounting information properties

and operations management. Foundations and Trends® in Technology, Information

and Operations Management, 12(1), pp.1-114.

Loo, I.D. and Bots, J., 2018. The life of an accounting information systems research

course. Accounting Education, 27(4), pp.358-382.

Murthy, U.S., 2016. Researching at the intersection of accounting and information

technology: A call for action. Journal of Information systems, 30(2), pp.159-167.

Neely, P., Forsgren, N., Premuroso, R., Vician, C. and White, C.E., 2015. Accounting

Information Systems (AIS) Course Design: Current Practices and Future

Trajectories. CAIS, 36, p.30.

Pan, G., Shankararaman, V., Seow, P.S. and Tan, G.H., 2017. Designing an

accounting analytics course using experiential learning approach. Accountancy

Business and the Public Interest, 16, pp.1-23.

Pearlson, K.E., Saunders, C.S. and Galletta, D.F., 2016. Managing and using

information systems, binder ready version: a strategic approach. John Wiley & Sons.

Riley, J. and Ward, K., 2015. Active learning, cooperative active learning, and

passive learning methods in an accounting information systems course. Issues in

Accounting Education, 32(2), pp.1-16.

Salimi, A.Y., Kornelus, A. and Abo-Hebeish, A., 2016. Improvement in Accounting

Students' Perception and Judgment on Ethical Issues as They Progress Through the

Accounting Curriculum. Journal of Higher Education Theory and Practice, 16(3),

p.51.

Singh, K., 2016. Implementing Enterprise Resource Planning Education in a

Postgraduate Accounting Information Systems Course. Business Education &

Accreditation, 8(1), pp.27-37.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.