Accounting Information System Report: Bucks Phyz Analysis

VerifiedAdded on 2020/05/28

|10

|2251

|113

Report

AI Summary

This report provides an analysis of the accounting information system (AIS) of Bucks Phyz, a medium-sized company with an annual turnover of $2.5 million. The report examines the sales process, identifying internal control weaknesses stemming from data entry procedures, the new pricing tool, the authorization policy, and the credit check process. It highlights the impact of these weaknesses, such as potential data errors, fraudulent activities, and financial losses. The report also discusses the introduction of corporate credit cards and their potential benefits, while emphasizing the need for strict monitoring. Recommendations include restricting access to the ERP system, providing proper training on the pricing tool, modifying the authorization policy, and implementing a system that enforces credit checks before finalizing sales. The report concludes with a discussion on the importance of a code of conduct to prevent conflicts of interest and promote ethical behavior within the organization.

Running head: ACCOUNTING INFORMATION SYSTEM

Accounting Information System

Name of the Student:

Name of the University:

Author Note

Accounting Information System

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING INFORMATION SYSTEM

Executive Summary

The situation that has been proposed in the case study is that as a part of delegating the

role of the accountant of Bucks Phyz , the sales process of the company has to be reviewed. The

reviewing has to be carried out on the basis of the key information that has been derived from the

interview of the staff and other related personnel. The decision of introducing corporate credit

cards has also been analyzed in this particular study.

The purpose of this study is to look into the internal control weaknesses of the

organization, Bucks Phyz. This will help in understanding the concepts of internal control that

are implemented within an organization for the purpose of exercising improved corporate

governance.

ACCOUNTING INFORMATION SYSTEM

Executive Summary

The situation that has been proposed in the case study is that as a part of delegating the

role of the accountant of Bucks Phyz , the sales process of the company has to be reviewed. The

reviewing has to be carried out on the basis of the key information that has been derived from the

interview of the staff and other related personnel. The decision of introducing corporate credit

cards has also been analyzed in this particular study.

The purpose of this study is to look into the internal control weaknesses of the

organization, Bucks Phyz. This will help in understanding the concepts of internal control that

are implemented within an organization for the purpose of exercising improved corporate

governance.

2

ACCOUNTING INFORMATION SYSTEM

Table of Contents

Introduction......................................................................................................................................3

Overview of the Sales process.........................................................................................................3

Issues in the internal control in the Bucks Phyz sales process........................................................4

Introduction of the corporate credit cards........................................................................................7

References........................................................................................................................................8

ACCOUNTING INFORMATION SYSTEM

Table of Contents

Introduction......................................................................................................................................3

Overview of the Sales process.........................................................................................................3

Issues in the internal control in the Bucks Phyz sales process........................................................4

Introduction of the corporate credit cards........................................................................................7

References........................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING INFORMATION SYSTEM

Introduction

The information that has been provided in regards to Bucks Phyz is that it is a medium

sized company that derives an yearly turnover of $2.5 million. The issue that has been presented

in the question is that as a part of delegating the role of the accountant of Bucks Phyz , the sales

process of the company has to be reviewed. The reviewing has to be carried out on the basis of

the key information that has been derived from the interview of the staff and other related

personnel. It has also been mentioned in the case study that the company has gone through a

restructuring program that has particularly taken place within the sales team. This has been

majorly due to the changes in the operating environment that took place within the company. The

impact of the change, as mentioned in the case study has been such that the employees do not

have a clear view about the new responsibilities. There also have been fraudulent events in the

accounts department. This further states that the current condition of the company has been such

that it cannot allow any further leakage in terms of revenue. Thus, the identification of the

particular areas of concern and the implementation of the required internal controls have been

discussed in this particular study. The policy of introduction of the corporate credit cards has also

been analyzed (Heise, Strecker & Frank, 2014).

Overview of the Sales process

The sales process in Bucks Phyz that has been adopted by business pivots around the new

pricing tool that has been introduced by the sales manager. This tool can effectively impact

business in a positive way as it can effectively compute the prices of the offers that are sent out

by the executives of the organization. The authorization policy however, has not been complied

with. This is further reinstated by the Head of Sales, Barry who mentions in his interview that in

spite of the availability of a standardized process that states the particular way in which the

managers can send the offers to the customers, it is not strictly followed. This is mainly because

the standardized process has not been mapped yet (Chang, 2014).

ACCOUNTING INFORMATION SYSTEM

Introduction

The information that has been provided in regards to Bucks Phyz is that it is a medium

sized company that derives an yearly turnover of $2.5 million. The issue that has been presented

in the question is that as a part of delegating the role of the accountant of Bucks Phyz , the sales

process of the company has to be reviewed. The reviewing has to be carried out on the basis of

the key information that has been derived from the interview of the staff and other related

personnel. It has also been mentioned in the case study that the company has gone through a

restructuring program that has particularly taken place within the sales team. This has been

majorly due to the changes in the operating environment that took place within the company. The

impact of the change, as mentioned in the case study has been such that the employees do not

have a clear view about the new responsibilities. There also have been fraudulent events in the

accounts department. This further states that the current condition of the company has been such

that it cannot allow any further leakage in terms of revenue. Thus, the identification of the

particular areas of concern and the implementation of the required internal controls have been

discussed in this particular study. The policy of introduction of the corporate credit cards has also

been analyzed (Heise, Strecker & Frank, 2014).

Overview of the Sales process

The sales process in Bucks Phyz that has been adopted by business pivots around the new

pricing tool that has been introduced by the sales manager. This tool can effectively impact

business in a positive way as it can effectively compute the prices of the offers that are sent out

by the executives of the organization. The authorization policy however, has not been complied

with. This is further reinstated by the Head of Sales, Barry who mentions in his interview that in

spite of the availability of a standardized process that states the particular way in which the

managers can send the offers to the customers, it is not strictly followed. This is mainly because

the standardized process has not been mapped yet (Chang, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING INFORMATION SYSTEM

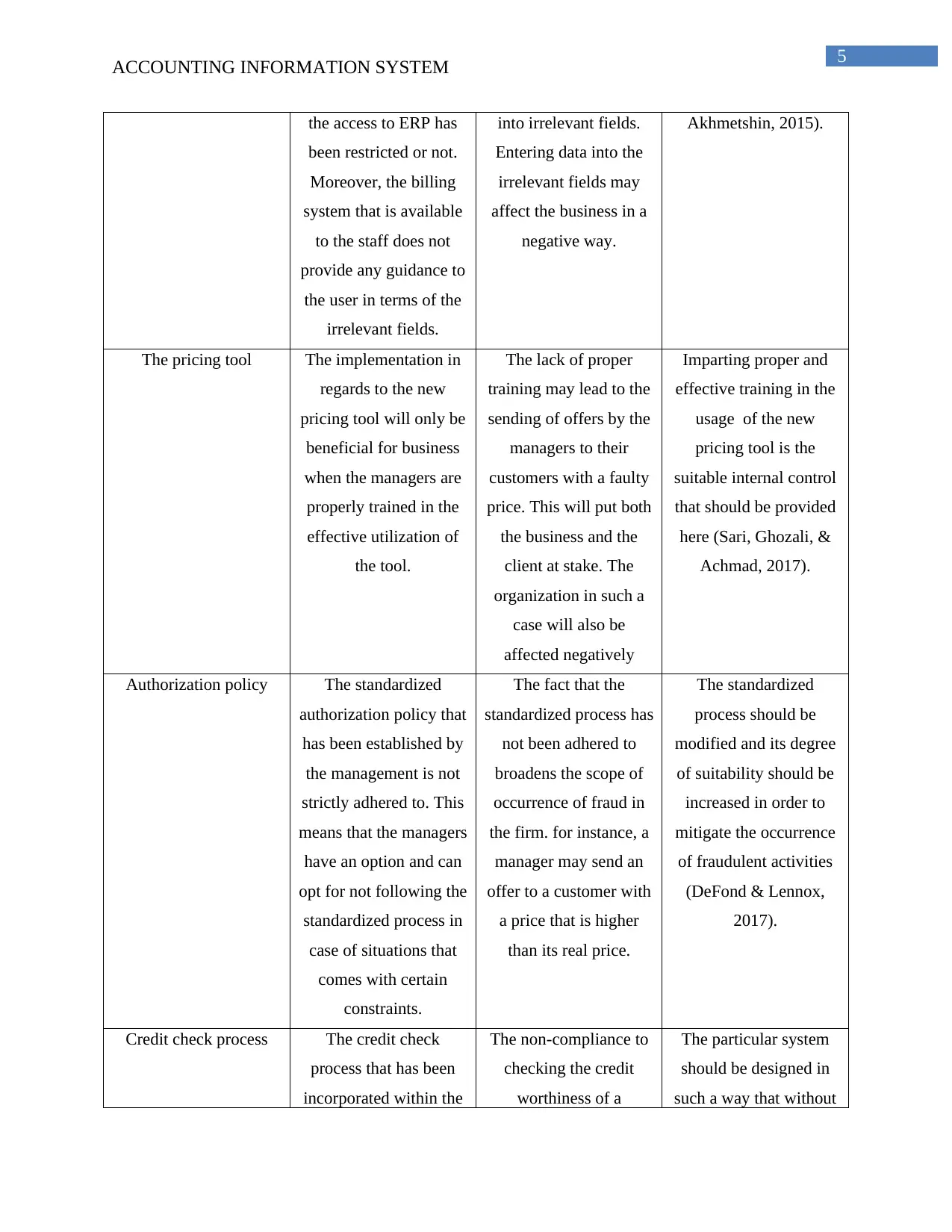

Issues in the internal control in the Bucks Phyz sales process

The sales process that has been monitored and evaluated has helped in the identification

of a number of weaknesses in the operational proceedings of the company. These weaknesses are

as follows:

Sales Process Internal control

weakness

Impact Recommendation

The process of data

entry

Alfred and Joy are

delegated with the

responsibilities of

entering the information

about the new

customers in the

operating system of the

company. The area of

concern in regards to the

data entry process is that

is the creation of a

pricing template. The

review of the customer

data that has been

entered into the pricing

template would be

irrational according to

the management. The

management is of the

opinion that

implementation of such

a procedure will also

affect the cost benefit

ratio. Furthermore, no

information has been

provided as to whether

The way the lack of

review of the pricing

template can affect

business is that critical

information in regards

to customer data might

be wrongly entered or

lost. This might hamper

the entire business and

its goodwill might be

affected. The access to

the ERP system should

also be restricted. This

is because unrestricted

access to the ERP

system will broaden the

chances of data

manipulation and thus

widen the scope of

occurrence of fraudulent

events. The billing

system should be

modified in such a way

that it guides the user

effectively in case the

data has been entered

The particular internal

control applicable in

such a situation is the

segregation of duty. The

appointment of a

particular employee for

checking the pricing

template will decrease

the chances of wrong

input of data into the

operating system.

Moreover, the cost

benefit ratio will also

not be affected by such

a change. Thus, other

than Alfred and Joy

another employee

should also be trained in

the usage of the pricing

template. The access to

the ERP system should

also be restricted within

the core comprehensive

management so that the

chances of fraud are

mitigated (Osadchy, &

ACCOUNTING INFORMATION SYSTEM

Issues in the internal control in the Bucks Phyz sales process

The sales process that has been monitored and evaluated has helped in the identification

of a number of weaknesses in the operational proceedings of the company. These weaknesses are

as follows:

Sales Process Internal control

weakness

Impact Recommendation

The process of data

entry

Alfred and Joy are

delegated with the

responsibilities of

entering the information

about the new

customers in the

operating system of the

company. The area of

concern in regards to the

data entry process is that

is the creation of a

pricing template. The

review of the customer

data that has been

entered into the pricing

template would be

irrational according to

the management. The

management is of the

opinion that

implementation of such

a procedure will also

affect the cost benefit

ratio. Furthermore, no

information has been

provided as to whether

The way the lack of

review of the pricing

template can affect

business is that critical

information in regards

to customer data might

be wrongly entered or

lost. This might hamper

the entire business and

its goodwill might be

affected. The access to

the ERP system should

also be restricted. This

is because unrestricted

access to the ERP

system will broaden the

chances of data

manipulation and thus

widen the scope of

occurrence of fraudulent

events. The billing

system should be

modified in such a way

that it guides the user

effectively in case the

data has been entered

The particular internal

control applicable in

such a situation is the

segregation of duty. The

appointment of a

particular employee for

checking the pricing

template will decrease

the chances of wrong

input of data into the

operating system.

Moreover, the cost

benefit ratio will also

not be affected by such

a change. Thus, other

than Alfred and Joy

another employee

should also be trained in

the usage of the pricing

template. The access to

the ERP system should

also be restricted within

the core comprehensive

management so that the

chances of fraud are

mitigated (Osadchy, &

5

ACCOUNTING INFORMATION SYSTEM

the access to ERP has

been restricted or not.

Moreover, the billing

system that is available

to the staff does not

provide any guidance to

the user in terms of the

irrelevant fields.

into irrelevant fields.

Entering data into the

irrelevant fields may

affect the business in a

negative way.

Akhmetshin, 2015).

The pricing tool The implementation in

regards to the new

pricing tool will only be

beneficial for business

when the managers are

properly trained in the

effective utilization of

the tool.

The lack of proper

training may lead to the

sending of offers by the

managers to their

customers with a faulty

price. This will put both

the business and the

client at stake. The

organization in such a

case will also be

affected negatively

Imparting proper and

effective training in the

usage of the new

pricing tool is the

suitable internal control

that should be provided

here (Sari, Ghozali, &

Achmad, 2017).

Authorization policy The standardized

authorization policy that

has been established by

the management is not

strictly adhered to. This

means that the managers

have an option and can

opt for not following the

standardized process in

case of situations that

comes with certain

constraints.

The fact that the

standardized process has

not been adhered to

broadens the scope of

occurrence of fraud in

the firm. for instance, a

manager may send an

offer to a customer with

a price that is higher

than its real price.

The standardized

process should be

modified and its degree

of suitability should be

increased in order to

mitigate the occurrence

of fraudulent activities

(DeFond & Lennox,

2017).

Credit check process The credit check

process that has been

incorporated within the

The non-compliance to

checking the credit

worthiness of a

The particular system

should be designed in

such a way that without

ACCOUNTING INFORMATION SYSTEM

the access to ERP has

been restricted or not.

Moreover, the billing

system that is available

to the staff does not

provide any guidance to

the user in terms of the

irrelevant fields.

into irrelevant fields.

Entering data into the

irrelevant fields may

affect the business in a

negative way.

Akhmetshin, 2015).

The pricing tool The implementation in

regards to the new

pricing tool will only be

beneficial for business

when the managers are

properly trained in the

effective utilization of

the tool.

The lack of proper

training may lead to the

sending of offers by the

managers to their

customers with a faulty

price. This will put both

the business and the

client at stake. The

organization in such a

case will also be

affected negatively

Imparting proper and

effective training in the

usage of the new

pricing tool is the

suitable internal control

that should be provided

here (Sari, Ghozali, &

Achmad, 2017).

Authorization policy The standardized

authorization policy that

has been established by

the management is not

strictly adhered to. This

means that the managers

have an option and can

opt for not following the

standardized process in

case of situations that

comes with certain

constraints.

The fact that the

standardized process has

not been adhered to

broadens the scope of

occurrence of fraud in

the firm. for instance, a

manager may send an

offer to a customer with

a price that is higher

than its real price.

The standardized

process should be

modified and its degree

of suitability should be

increased in order to

mitigate the occurrence

of fraudulent activities

(DeFond & Lennox,

2017).

Credit check process The credit check

process that has been

incorporated within the

The non-compliance to

checking the credit

worthiness of a

The particular system

should be designed in

such a way that without

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

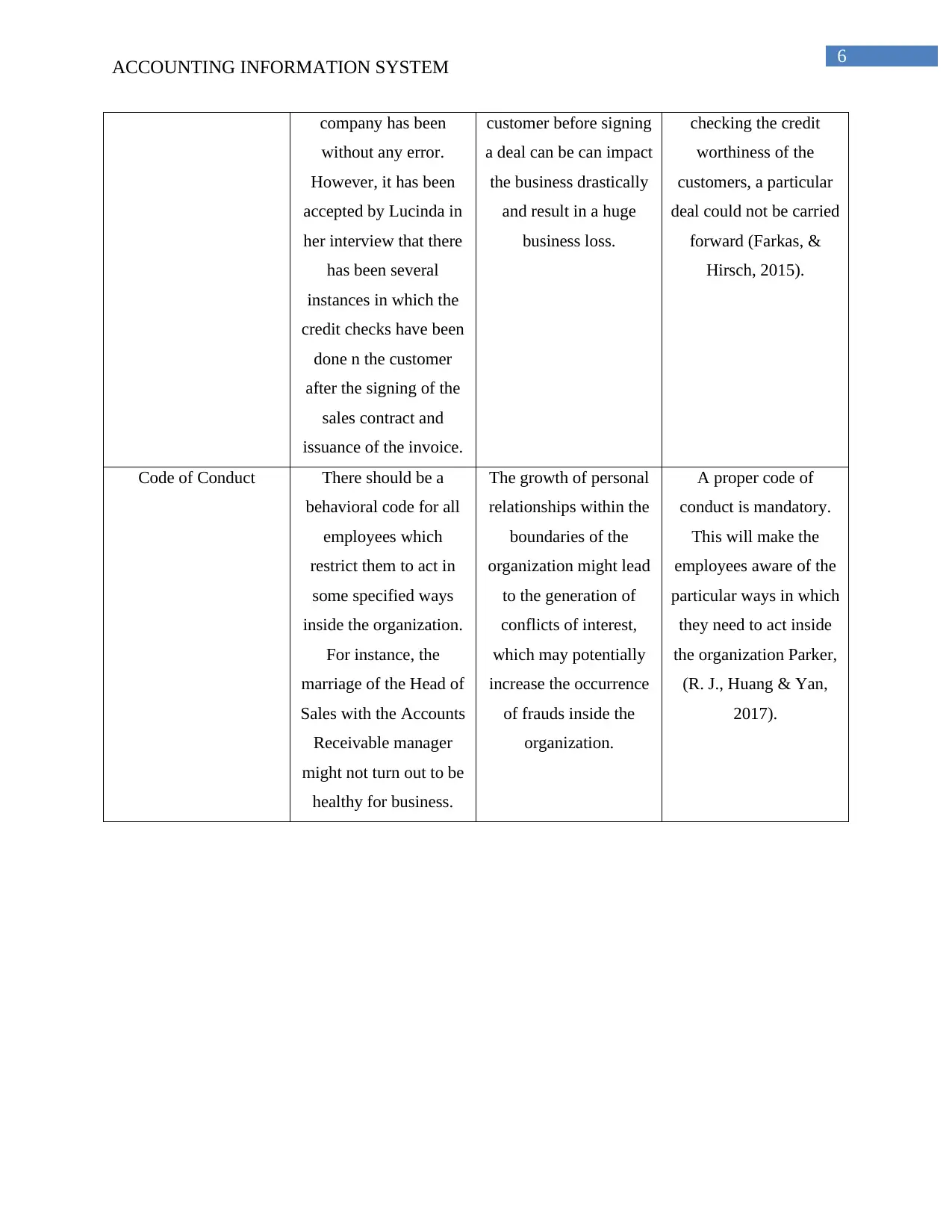

ACCOUNTING INFORMATION SYSTEM

company has been

without any error.

However, it has been

accepted by Lucinda in

her interview that there

has been several

instances in which the

credit checks have been

done n the customer

after the signing of the

sales contract and

issuance of the invoice.

customer before signing

a deal can be can impact

the business drastically

and result in a huge

business loss.

checking the credit

worthiness of the

customers, a particular

deal could not be carried

forward (Farkas, &

Hirsch, 2015).

Code of Conduct There should be a

behavioral code for all

employees which

restrict them to act in

some specified ways

inside the organization.

For instance, the

marriage of the Head of

Sales with the Accounts

Receivable manager

might not turn out to be

healthy for business.

The growth of personal

relationships within the

boundaries of the

organization might lead

to the generation of

conflicts of interest,

which may potentially

increase the occurrence

of frauds inside the

organization.

A proper code of

conduct is mandatory.

This will make the

employees aware of the

particular ways in which

they need to act inside

the organization Parker,

(R. J., Huang & Yan,

2017).

ACCOUNTING INFORMATION SYSTEM

company has been

without any error.

However, it has been

accepted by Lucinda in

her interview that there

has been several

instances in which the

credit checks have been

done n the customer

after the signing of the

sales contract and

issuance of the invoice.

customer before signing

a deal can be can impact

the business drastically

and result in a huge

business loss.

checking the credit

worthiness of the

customers, a particular

deal could not be carried

forward (Farkas, &

Hirsch, 2015).

Code of Conduct There should be a

behavioral code for all

employees which

restrict them to act in

some specified ways

inside the organization.

For instance, the

marriage of the Head of

Sales with the Accounts

Receivable manager

might not turn out to be

healthy for business.

The growth of personal

relationships within the

boundaries of the

organization might lead

to the generation of

conflicts of interest,

which may potentially

increase the occurrence

of frauds inside the

organization.

A proper code of

conduct is mandatory.

This will make the

employees aware of the

particular ways in which

they need to act inside

the organization Parker,

(R. J., Huang & Yan,

2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING INFORMATION SYSTEM

Introduction of the corporate credit cards

The introduction of the corporate credit cards might bring huge profits into business.

However, the particular point that should be noted here is that the specified transactions that are

proceeded with the help of the corporate credit cards should be strictly monitored and evaluated

as to whether the purchased service or product was really needed by business or not. The facility

of corporate credit cards exposes the business to high amounts of risk. But the particular

advantages provided cover for the proposed risks. The corporate credit cards will free the

business from the unnecessary workload of transferring the payments from the business to the

supplier account. In fact, the reimbursement process will also be simplified by the incorporation

of the corporate credit cards (Al-Matari, Mohammed& Al-Matari, 2017).

The management of Bucks Phyz should consider the formation of a particular group that

will monitor the transactions that are incurred with the help of the corporate credit cards. To be

more precise, this team will authorize the transactions before debiting real cash from the business

account. The finance department personnel may be chosen for building the particular team.

The recommendation to the chief executive officer in regards to the issuance of the

corporate credit cards is that the proposal apparently is brilliant and will benefit business.

However, it is highly recommended that the corporate credit cards should only be issued to the

key personnel of the management of the organization. For an instance, in case of the training

course mentioned in the provided case study, the service should be purchased with the corporate

credit card allotted to the human resource manager post the authorization by the finance team.

ACCOUNTING INFORMATION SYSTEM

Introduction of the corporate credit cards

The introduction of the corporate credit cards might bring huge profits into business.

However, the particular point that should be noted here is that the specified transactions that are

proceeded with the help of the corporate credit cards should be strictly monitored and evaluated

as to whether the purchased service or product was really needed by business or not. The facility

of corporate credit cards exposes the business to high amounts of risk. But the particular

advantages provided cover for the proposed risks. The corporate credit cards will free the

business from the unnecessary workload of transferring the payments from the business to the

supplier account. In fact, the reimbursement process will also be simplified by the incorporation

of the corporate credit cards (Al-Matari, Mohammed& Al-Matari, 2017).

The management of Bucks Phyz should consider the formation of a particular group that

will monitor the transactions that are incurred with the help of the corporate credit cards. To be

more precise, this team will authorize the transactions before debiting real cash from the business

account. The finance department personnel may be chosen for building the particular team.

The recommendation to the chief executive officer in regards to the issuance of the

corporate credit cards is that the proposal apparently is brilliant and will benefit business.

However, it is highly recommended that the corporate credit cards should only be issued to the

key personnel of the management of the organization. For an instance, in case of the training

course mentioned in the provided case study, the service should be purchased with the corporate

credit card allotted to the human resource manager post the authorization by the finance team.

8

ACCOUNTING INFORMATION SYSTEM

References

Al-Matari, Y. A., Mohammed, S. A. S., & Al-Matari, E. M. (2017). Audit Committee Activities

and the Internal Control System of Commercial Banks operating in Yemen. International

Review of Management and Marketing, 7(1).

Chang, S. I., Yen, D. C., Chang, I. C., & Jan, D. (2014). Internal control framework for a

compliant ERP system. Information & Management, 51(2), 187-205.

DeFond, M. L., & Lennox, C. S. (2017). Do PCAOB Inspections Improve the Quality of Internal

Control Audits?. Journal of Accounting Research, 55(3), 591-627.

Farkas, M. J., & Hirsch, R. M. (2015). The effect of frequency and automation of internal control

testing on external auditor reliance on the internal audit function. Journal of Information

Systems, 30(1), 21-40.

Farkas, M. J., & Hirsch, R. M. (2015). The effect of frequency and automation of internal control

testing on external auditor reliance on the internal audit function. Journal of Information

Systems, 30(1), 21-40.

Heise, D., Strecker, S., & Frank, U. (2014). ControlML: A domain-specific modeling language

in support of assessing internal controls and the internal control system. International

Journal of Accounting Information Systems, 15(3), 224-245.

Kieseberg, P., Malle, B., Frühwirt, P., Weippl, E., & Holzinger, A. (2016). A tamper-proof audit

and control system for the doctor in the loop. Brain informatics, 3(4), 269-279.

Osadchy, E. A., & Akhmetshin, E. M. (2015). Development of the financial control system in the

company in crisis. Mediterranean Journal of Social Sciences, 6(5), 390.

Parker, R. J., Dao, M., Huang, H. W., & Yan, Y. C. (2017). Disclosing material weakness in

internal controls: Does the gender of audit committee members matter?. Asia-Pacific

Journal of Accounting & Economics, 24(3-4), 407-420.

Sari, N., Ghozali, I., & Achmad, T. (2017). THE EFFECT OF INTERNAL AUDIT AND

INTERNAL CONTROL SYSTEM ON PUBLIC ACCOUNTABILITY: THE

ACCOUNTING INFORMATION SYSTEM

References

Al-Matari, Y. A., Mohammed, S. A. S., & Al-Matari, E. M. (2017). Audit Committee Activities

and the Internal Control System of Commercial Banks operating in Yemen. International

Review of Management and Marketing, 7(1).

Chang, S. I., Yen, D. C., Chang, I. C., & Jan, D. (2014). Internal control framework for a

compliant ERP system. Information & Management, 51(2), 187-205.

DeFond, M. L., & Lennox, C. S. (2017). Do PCAOB Inspections Improve the Quality of Internal

Control Audits?. Journal of Accounting Research, 55(3), 591-627.

Farkas, M. J., & Hirsch, R. M. (2015). The effect of frequency and automation of internal control

testing on external auditor reliance on the internal audit function. Journal of Information

Systems, 30(1), 21-40.

Farkas, M. J., & Hirsch, R. M. (2015). The effect of frequency and automation of internal control

testing on external auditor reliance on the internal audit function. Journal of Information

Systems, 30(1), 21-40.

Heise, D., Strecker, S., & Frank, U. (2014). ControlML: A domain-specific modeling language

in support of assessing internal controls and the internal control system. International

Journal of Accounting Information Systems, 15(3), 224-245.

Kieseberg, P., Malle, B., Frühwirt, P., Weippl, E., & Holzinger, A. (2016). A tamper-proof audit

and control system for the doctor in the loop. Brain informatics, 3(4), 269-279.

Osadchy, E. A., & Akhmetshin, E. M. (2015). Development of the financial control system in the

company in crisis. Mediterranean Journal of Social Sciences, 6(5), 390.

Parker, R. J., Dao, M., Huang, H. W., & Yan, Y. C. (2017). Disclosing material weakness in

internal controls: Does the gender of audit committee members matter?. Asia-Pacific

Journal of Accounting & Economics, 24(3-4), 407-420.

Sari, N., Ghozali, I., & Achmad, T. (2017). THE EFFECT OF INTERNAL AUDIT AND

INTERNAL CONTROL SYSTEM ON PUBLIC ACCOUNTABILITY: THE

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING INFORMATION SYSTEM

EMPERICAL STUDY IN INDONESIA STATE UNIVERSITIES. Technology, 8(9),

157-166.

ACCOUNTING INFORMATION SYSTEM

EMPERICAL STUDY IN INDONESIA STATE UNIVERSITIES. Technology, 8(9),

157-166.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.