Analysis of Accounting Information System for Adam & Co. (HA2042)

VerifiedAdded on 2022/10/19

|12

|2680

|356

Report

AI Summary

This report provides an analysis of the accounting information system (AIS) of Adam & Co., a Perth-based wholesaler of industrial supplies. The report begins with an executive summary highlighting the internal control weaknesses and associated risks within the company's purchasing, cash disbursement, and payroll systems. It includes system flowcharts for each of these departments. The core of the report focuses on identifying and describing internal control weaknesses within each system, such as inadequate procedures for ordering, reliance on single authorities, and lack of checks on working hours. Furthermore, it assesses the risks associated with these weaknesses, including potential for fraud, inaccurate payments, and inventory mismanagement. The report concludes by suggesting improvements to address these issues, such as incorporating better vendor selection, monitoring procedures, and review mechanisms to strengthen internal controls and reduce risks.

Accounting information system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................4

Report to Managing director............................................................................................................4

System flowchart of purchase system..........................................................................................5

System flowchart of cash disbursements system.........................................................................6

System flowchart of payroll system............................................................................................7

Description of internal control weakness in each system and risks associated with the

identified weakness......................................................................................................................8

Internal control weakness in purchase system.........................................................................8

Internal control weakness in cash disbursements system........................................................8

Internal control weakness in payroll system............................................................................9

Risk associated with the identified weakness in purchase system..........................................9

Risk associated with the identified weakness in cash disbursements system........................10

Risk associated with the identified weakness in payroll system...........................................10

Conclusion.....................................................................................................................................10

List of references...........................................................................................................................12

Introduction......................................................................................................................................4

Report to Managing director............................................................................................................4

System flowchart of purchase system..........................................................................................5

System flowchart of cash disbursements system.........................................................................6

System flowchart of payroll system............................................................................................7

Description of internal control weakness in each system and risks associated with the

identified weakness......................................................................................................................8

Internal control weakness in purchase system.........................................................................8

Internal control weakness in cash disbursements system........................................................8

Internal control weakness in payroll system............................................................................9

Risk associated with the identified weakness in purchase system..........................................9

Risk associated with the identified weakness in cash disbursements system........................10

Risk associated with the identified weakness in payroll system...........................................10

Conclusion.....................................................................................................................................10

List of references...........................................................................................................................12

Executive summary

Internal control procedures are practices and guidelines complied by an organization in order to

protect its resources. Effective internal control activities assist in ascertaining priorities, attaining

department goals and accomplish compliance regulations. Present study relates to assessment of

internal control of Adam & CO. in order to analyze its internal control weakness and risk

associated with same. The purchasing system of company does not have adequate procedure

relating to ascertainment of items required to be order due to which risk related to out of stock

might be faced. Cash disbursement system is depended majorly on single authority which leads

to risk associated with unauthorized payments. Lastly, weak internal control management is

available in relating to recording to working hours which result in risk associated with wrong

payments to employees.

Internal control procedures are practices and guidelines complied by an organization in order to

protect its resources. Effective internal control activities assist in ascertaining priorities, attaining

department goals and accomplish compliance regulations. Present study relates to assessment of

internal control of Adam & CO. in order to analyze its internal control weakness and risk

associated with same. The purchasing system of company does not have adequate procedure

relating to ascertainment of items required to be order due to which risk related to out of stock

might be faced. Cash disbursement system is depended majorly on single authority which leads

to risk associated with unauthorized payments. Lastly, weak internal control management is

available in relating to recording to working hours which result in risk associated with wrong

payments to employees.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Internal control system of an organization comprises set of rules, procedures and provisions

which are implemented to provide direction, enhance efficiency and strengthen the existing

policies (Bedford and Malmi, 2015). An organization is able to ascertain existing loop holes in

the management through assessing the effectiveness of internal control (Buckby, Gallery and

Ma, 2015). The same can be done through segregation of duties appropriately so that single

authority is not able to manipulate records as well as enter fake transactions. Present report

relates to analysis of internal control of Adam & Co., a Perth based wholesaler of industrial

supplies. Initially system flow chart of purchases system, cash disbursement system and payroll

system has been provided. Further, internal control weakness of each department has been

analyzed along with risk associated with same in detail manner.

REPORT TO MANAGING DIRECTOR

To

ABC

Managing director

Adam & Co

Subject: This report has been prepared to evaluate the risks and internal controls in the

operational processes for the expenditure cycle of business in order to determine internal control

weakness and risks associated to it in each system.

Internal control system of an organization comprises set of rules, procedures and provisions

which are implemented to provide direction, enhance efficiency and strengthen the existing

policies (Bedford and Malmi, 2015). An organization is able to ascertain existing loop holes in

the management through assessing the effectiveness of internal control (Buckby, Gallery and

Ma, 2015). The same can be done through segregation of duties appropriately so that single

authority is not able to manipulate records as well as enter fake transactions. Present report

relates to analysis of internal control of Adam & Co., a Perth based wholesaler of industrial

supplies. Initially system flow chart of purchases system, cash disbursement system and payroll

system has been provided. Further, internal control weakness of each department has been

analyzed along with risk associated with same in detail manner.

REPORT TO MANAGING DIRECTOR

To

ABC

Managing director

Adam & Co

Subject: This report has been prepared to evaluate the risks and internal controls in the

operational processes for the expenditure cycle of business in order to determine internal control

weakness and risks associated to it in each system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

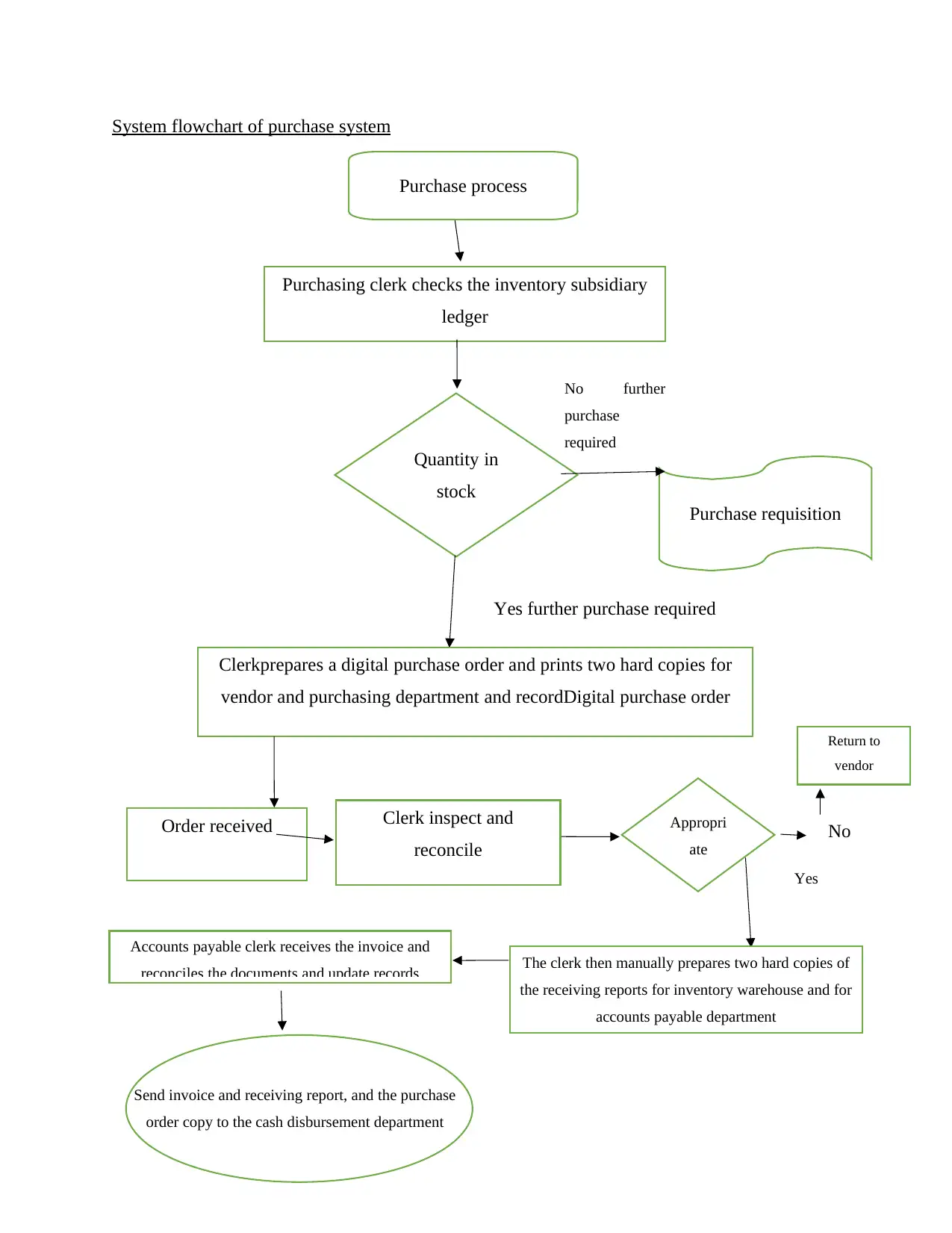

System flowchart of purchase system

Purchase process

Purchasing clerk checks the inventory subsidiary

ledger

Quantity in

stock

Purchase requisition

No further

purchase

required

Yes further purchase required

Clerkprepares a digital purchase order and prints two hard copies for

vendor and purchasing department and recordDigital purchase order

Order received Clerk inspect and

reconcile

Appropri

ate

No

Return to

vendor

Yes

The clerk then manually prepares two hard copies of

the receiving reports for inventory warehouse and for

accounts payable department

Accounts payable clerk receives the invoice and

reconciles the documents and update records

Send invoice and receiving report, and the purchase

order copy to the cash disbursement department

Purchase process

Purchasing clerk checks the inventory subsidiary

ledger

Quantity in

stock

Purchase requisition

No further

purchase

required

Yes further purchase required

Clerkprepares a digital purchase order and prints two hard copies for

vendor and purchasing department and recordDigital purchase order

Order received Clerk inspect and

reconcile

Appropri

ate

No

Return to

vendor

Yes

The clerk then manually prepares two hard copies of

the receiving reports for inventory warehouse and for

accounts payable department

Accounts payable clerk receives the invoice and

reconciles the documents and update records

Send invoice and receiving report, and the purchase

order copy to the cash disbursement department

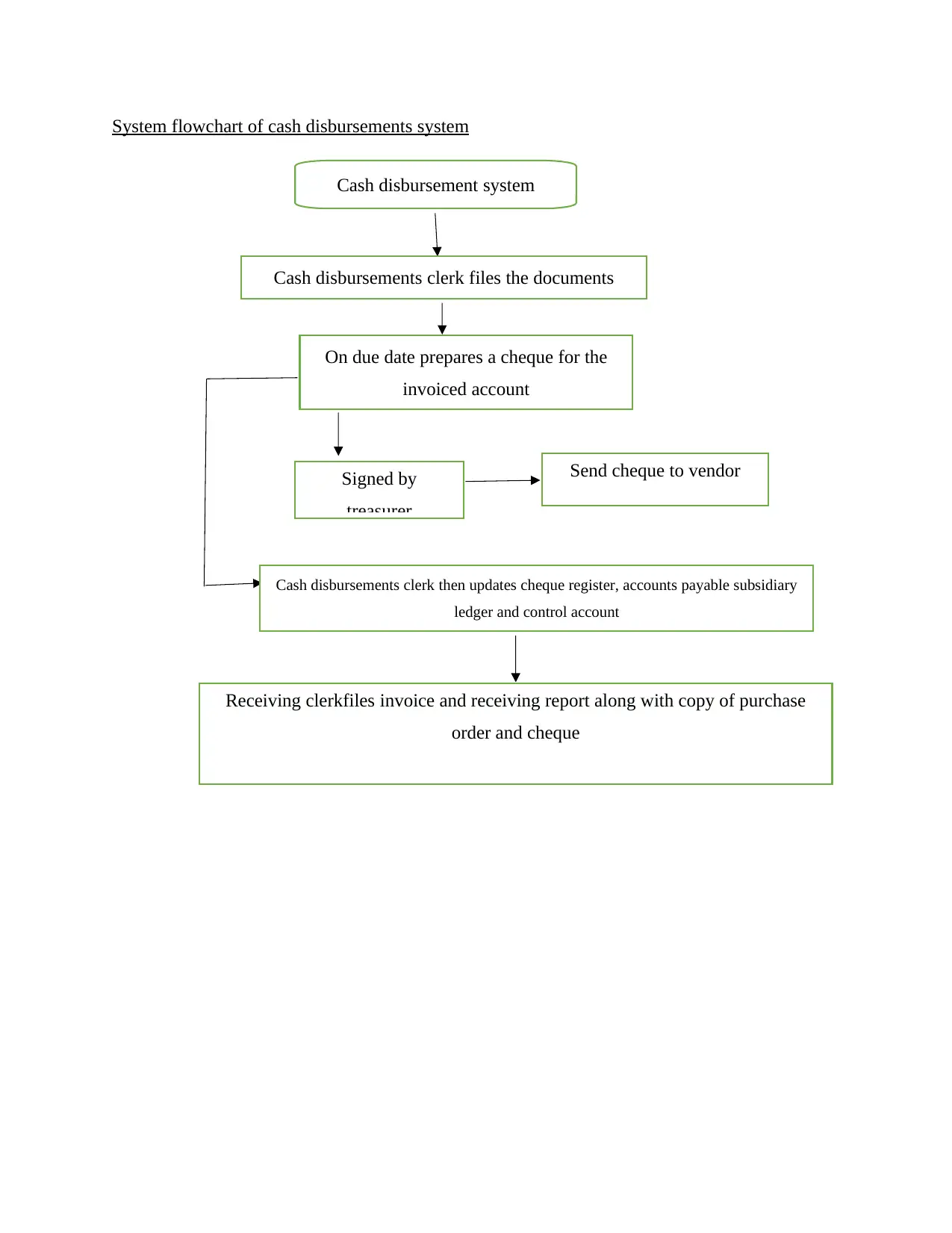

System flowchart of cash disbursements system

Cash disbursement system

Cash disbursements clerk files the documents

On due date prepares a cheque for the

invoiced account

Signed by

treasurer

Send cheque to vendor

Cash disbursements clerk then updates cheque register, accounts payable subsidiary

ledger and control account

Receiving clerkfiles invoice and receiving report along with copy of purchase

order and cheque

Cash disbursement system

Cash disbursements clerk files the documents

On due date prepares a cheque for the

invoiced account

Signed by

treasurer

Send cheque to vendor

Cash disbursements clerk then updates cheque register, accounts payable subsidiary

ledger and control account

Receiving clerkfiles invoice and receiving report along with copy of purchase

order and cheque

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

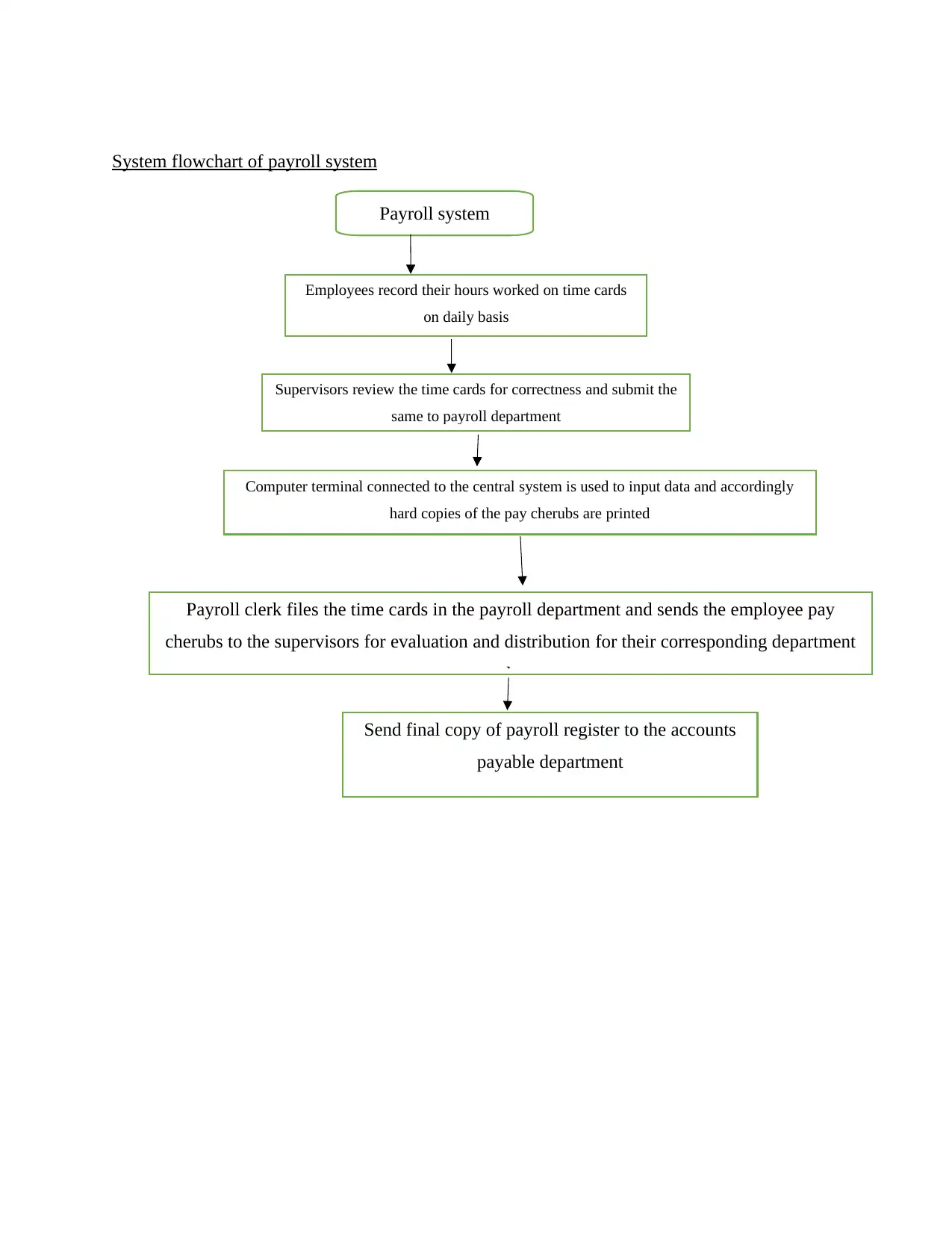

System flowchart of payroll system

Payroll system

Employees record their hours worked on time cards

on daily basis

Supervisors review the time cards for correctness and submit the

same to payroll department

Computer terminal connected to the central system is used to input data and accordingly

hard copies of the pay cherubs are printed

Payroll clerk files the time cards in the payroll department and sends the employee pay

cherubs to the supervisors for evaluation and distribution for their corresponding department

employee

Send final copy of payroll register to the accounts

payable department

Payroll system

Employees record their hours worked on time cards

on daily basis

Supervisors review the time cards for correctness and submit the

same to payroll department

Computer terminal connected to the central system is used to input data and accordingly

hard copies of the pay cherubs are printed

Payroll clerk files the time cards in the payroll department and sends the employee pay

cherubs to the supervisors for evaluation and distribution for their corresponding department

employee

Send final copy of payroll register to the accounts

payable department

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Description of internal control weakness in each system and risks associated with the identified

weakness

Internal control can be referred as process applied by management to produce correct, reliable

financial statements and for safeguarding of assets and inventories of company (Kline and

Hutchins, 2017). An organization having weak internal control than it is easy for employees and

staff to make fraud and mistakes (Hisrich and Ramadani, 2017). In order to decrease the

probability of existence of fraud whether intentionally or due to mistake it is necessary to

monitor internal control on a continue basis and modify in accordance with their requirement

(Turner, Weickgenannt and Copeland, 2016).

Internal control weakness in purchase system

The main internal control weakness associated with purchase system is that order relating to

required item is provided when it is deemed to be too low. It is not an appropriate manner of

assessing the quantum of required items or products. The method followed by the organization

would not be able to fulfill any surprise order or significant order. As items are ordered only

when the quantum of same is too low. It is necessary for management to maintain accountability

while authorize, review and approved purchased based system (Luo, 2017). Each item is not

required on continue basis, thus the company requires to assess as well as bifurcate the items as

per the requirement of demand. A quantity level should be ascertained in relation with each item

and new orders should be made on same basis

Another weakness in purchase system was that no new vendors were searched and purchases

were made from existing vendors only. Thus, the organization was unaware of new schemes

available with other vendors. Even no procedure exists in order to assess whether any

misstatement or fraud exist or not. Due to same reason the effectiveness of existing internal

control has affected and available sources could not be applied in effective manner. Even no

inventory count method is being followed by the organization due to which even though, goods

are present in books of accounts but it is possible that the same are not physical available.

Internal control weakness in cash disbursements system

It can be assessed that cash disbursement procedure is mainly depended on clerk responsible for

preparing check as well as updating same in accounts payable account. In present case one

person is responsible for all the significant activities and no provisions are made to check his

weakness

Internal control can be referred as process applied by management to produce correct, reliable

financial statements and for safeguarding of assets and inventories of company (Kline and

Hutchins, 2017). An organization having weak internal control than it is easy for employees and

staff to make fraud and mistakes (Hisrich and Ramadani, 2017). In order to decrease the

probability of existence of fraud whether intentionally or due to mistake it is necessary to

monitor internal control on a continue basis and modify in accordance with their requirement

(Turner, Weickgenannt and Copeland, 2016).

Internal control weakness in purchase system

The main internal control weakness associated with purchase system is that order relating to

required item is provided when it is deemed to be too low. It is not an appropriate manner of

assessing the quantum of required items or products. The method followed by the organization

would not be able to fulfill any surprise order or significant order. As items are ordered only

when the quantum of same is too low. It is necessary for management to maintain accountability

while authorize, review and approved purchased based system (Luo, 2017). Each item is not

required on continue basis, thus the company requires to assess as well as bifurcate the items as

per the requirement of demand. A quantity level should be ascertained in relation with each item

and new orders should be made on same basis

Another weakness in purchase system was that no new vendors were searched and purchases

were made from existing vendors only. Thus, the organization was unaware of new schemes

available with other vendors. Even no procedure exists in order to assess whether any

misstatement or fraud exist or not. Due to same reason the effectiveness of existing internal

control has affected and available sources could not be applied in effective manner. Even no

inventory count method is being followed by the organization due to which even though, goods

are present in books of accounts but it is possible that the same are not physical available.

Internal control weakness in cash disbursements system

It can be assessed that cash disbursement procedure is mainly depended on clerk responsible for

preparing check as well as updating same in accounts payable account. In present case one

person is responsible for all the significant activities and no provisions are made to check his

work. He is authorized to make the cheque and provide same to the treasurer to sign and mail the

cheque the vendor. Even, the receiving clerk files the received invoice, receiving report but does

not reconcile the same with accounts payable account.

Internal control weakness in payroll system

No checking policy or process relating to recording of hours worked by employees is available in

internal control procedure. It means in case an employee has entered wrong working hours and

no has accessed same than he might get payment for the hours for which he has not worked. The

time cards are reviewed at weekly basis but provision does exist for making entry for workers

who are absent; thus an employee can make wrong entry in his card before it is provided for

correcting to the supervisor. The cheque made available by the accounts payable clerk comprises

amount for entire payroll and no reconciliation procedure does exists that whether individual

payments made to the employees are correct or not.

Even the responsibility of accounting in department computer terminal and filing same in payroll

register is provided to single authority. As both the responsibility is to be conducted by single

person, it is easy to make fault or higher probability of occurring of error exist as transactions are

neither reconciled nor rechecked by another authority (Zakaria, Nawawi, and Salin, 2016).

Risk associated with the identified weakness in purchase system

The risk associated weakness relating to ordering products at very low level is excessive

availability of dead stock (items which are not sold). It could lead to inappropriate application of

available resources i.e. the existing funds are applied for items which are not required and

shortage of necessary items could exist. As mere low level of quantum of item does not mean

that it is required to be ordered (Bhattacharjee, Maletta and Moreno, 2015.). It is necessary that

specific item should be in demand for ordering same. The purchase system does not comprise

any procedure relating to checking whether purchase order has been received within specified

time or not. The same had negative impact on inventory management. The risk relating to fraud

does exist as no policy relating to selection of vendor is available in present system. It is possible

that the purchasing clerk might make agreement with existing vendor and make personal profits

through charging higher price for items purchased.

The risk relating to loss of items presented at inventory register but physically not available does

exist due to absence of physical checks of items. It is necessary to assess whether the existing

cheque the vendor. Even, the receiving clerk files the received invoice, receiving report but does

not reconcile the same with accounts payable account.

Internal control weakness in payroll system

No checking policy or process relating to recording of hours worked by employees is available in

internal control procedure. It means in case an employee has entered wrong working hours and

no has accessed same than he might get payment for the hours for which he has not worked. The

time cards are reviewed at weekly basis but provision does exist for making entry for workers

who are absent; thus an employee can make wrong entry in his card before it is provided for

correcting to the supervisor. The cheque made available by the accounts payable clerk comprises

amount for entire payroll and no reconciliation procedure does exists that whether individual

payments made to the employees are correct or not.

Even the responsibility of accounting in department computer terminal and filing same in payroll

register is provided to single authority. As both the responsibility is to be conducted by single

person, it is easy to make fault or higher probability of occurring of error exist as transactions are

neither reconciled nor rechecked by another authority (Zakaria, Nawawi, and Salin, 2016).

Risk associated with the identified weakness in purchase system

The risk associated weakness relating to ordering products at very low level is excessive

availability of dead stock (items which are not sold). It could lead to inappropriate application of

available resources i.e. the existing funds are applied for items which are not required and

shortage of necessary items could exist. As mere low level of quantum of item does not mean

that it is required to be ordered (Bhattacharjee, Maletta and Moreno, 2015.). It is necessary that

specific item should be in demand for ordering same. The purchase system does not comprise

any procedure relating to checking whether purchase order has been received within specified

time or not. The same had negative impact on inventory management. The risk relating to fraud

does exist as no policy relating to selection of vendor is available in present system. It is possible

that the purchasing clerk might make agreement with existing vendor and make personal profits

through charging higher price for items purchased.

The risk relating to loss of items presented at inventory register but physically not available does

exist due to absence of physical checks of items. It is necessary to assess whether the existing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

items are available in useable quality or not. It might be possible that items do exists but they are

of no more use and unnecessarily taking space in shelves. This weakness will lead to risk relating

to obsolete items available in stores. Further, management will not be able to order required

amount of items as it is unaware of its vacancy due to absence of physical count check method.

Risk associated with the identified weakness in cash disbursements system

Risk relating to dependency on single person for major operation does exist in case of cash

disbursement system. The cash disbursement clerk does not reconcile the documents receipts

from accounts payable department and prepares cheque without rechecking the amounts. Even

risk of happening of fraud is higher in the organization if same authority of making cheque and

updating accounts payable control accounts (Brasel, Doxey, Grenier, and Reffett, 2016). He can

make fake entries or manipulate the amount due to vendors.

Risk associated with the identified weakness in payroll system

Inaccurate calculation of working hours leads to risk relating to unfair payments to the

employees (Euchner and Ganguly, 2014). As no separate presentation of time off and unpaid

absence have been provided on time card. It is possible that it might affect the environment of

organization negatively as improper payments would result in misappropriation of funds. In

present case as cheque provided comprises total amount payable to employees of each

department. But no reviewing or reconciliation procedure is applied to assess whether payment

received to individual employees are correct or not.

As inadequate internal procedures are available in pay-roll system, the risk of compensation

being issued for non-existing or terminated employees. Even possibility of mistake in calculation

of working hours is high which might lead to issues such as overpayments to dishonest

employees and incurring expenditure through redo payroll records.

CONCLUSION

It can be concluded from above discussion that expenditure cycle of Adam & Co’s mainly lacks

in monitoring and assessing risk assessment relating existing internal control weakness. In order

to address these issues control activities can be incorporated in policies and procedures to risk-

prone areas. For instance as in case of purchasing system, adequate procedures should be

incorporated so that vendor choice is made appropriately. It should be not the choice of

of no more use and unnecessarily taking space in shelves. This weakness will lead to risk relating

to obsolete items available in stores. Further, management will not be able to order required

amount of items as it is unaware of its vacancy due to absence of physical count check method.

Risk associated with the identified weakness in cash disbursements system

Risk relating to dependency on single person for major operation does exist in case of cash

disbursement system. The cash disbursement clerk does not reconcile the documents receipts

from accounts payable department and prepares cheque without rechecking the amounts. Even

risk of happening of fraud is higher in the organization if same authority of making cheque and

updating accounts payable control accounts (Brasel, Doxey, Grenier, and Reffett, 2016). He can

make fake entries or manipulate the amount due to vendors.

Risk associated with the identified weakness in payroll system

Inaccurate calculation of working hours leads to risk relating to unfair payments to the

employees (Euchner and Ganguly, 2014). As no separate presentation of time off and unpaid

absence have been provided on time card. It is possible that it might affect the environment of

organization negatively as improper payments would result in misappropriation of funds. In

present case as cheque provided comprises total amount payable to employees of each

department. But no reviewing or reconciliation procedure is applied to assess whether payment

received to individual employees are correct or not.

As inadequate internal procedures are available in pay-roll system, the risk of compensation

being issued for non-existing or terminated employees. Even possibility of mistake in calculation

of working hours is high which might lead to issues such as overpayments to dishonest

employees and incurring expenditure through redo payroll records.

CONCLUSION

It can be concluded from above discussion that expenditure cycle of Adam & Co’s mainly lacks

in monitoring and assessing risk assessment relating existing internal control weakness. In order

to address these issues control activities can be incorporated in policies and procedures to risk-

prone areas. For instance as in case of purchasing system, adequate procedures should be

incorporated so that vendor choice is made appropriately. It should be not the choice of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

purchasing manager but the best option for organization and even the new available options

should be considered. Through same organization will be able to attain gain from existing

opportunities.

Monitoring procedure is required to be incorporate at each expenditure process in order to attain

information relating to potential and actual break down in control system (Soudani, 2013). It will

assist in ascertaining the loop holes in existing procedures at initiative stages. Measures can be

taken by company though including informal monitoring activities such as management

checking with subordinates to assess whether objectives are met or not (Sheedy, and Griffin,

2018). Reviewing and reassessing procedure are main part of internal control process as internal

control can be maintained effectively only when existing flaws in procedures are ascertained and

rectified timely. As in case of payroll internal control, working hours are not recorded

appropriately due to which fair payments are not provided to employees. Thus, the possibility

exists that excessive or unfair payments are made to the employees. The fact cannot be denied

that each employees of organization is integral part of internal control which comprises board of

director, management, internal and external auditors. Thus, through making specified changes in

existing internal control system Adam & Co would be able to enhance the integrity of existing

internal control system.

should be considered. Through same organization will be able to attain gain from existing

opportunities.

Monitoring procedure is required to be incorporate at each expenditure process in order to attain

information relating to potential and actual break down in control system (Soudani, 2013). It will

assist in ascertaining the loop holes in existing procedures at initiative stages. Measures can be

taken by company though including informal monitoring activities such as management

checking with subordinates to assess whether objectives are met or not (Sheedy, and Griffin,

2018). Reviewing and reassessing procedure are main part of internal control process as internal

control can be maintained effectively only when existing flaws in procedures are ascertained and

rectified timely. As in case of payroll internal control, working hours are not recorded

appropriately due to which fair payments are not provided to employees. Thus, the possibility

exists that excessive or unfair payments are made to the employees. The fact cannot be denied

that each employees of organization is integral part of internal control which comprises board of

director, management, internal and external auditors. Thus, through making specified changes in

existing internal control system Adam & Co would be able to enhance the integrity of existing

internal control system.

LIST OF REFERENCES

Bedford, D.S. and Malmi, T., 2015. Configurations of control: An exploratory

analysis. Management Accounting Research, 27, pp.2-26.

Bhattacharjee, S., Maletta, M.J. and Moreno, K.K., 2015. The role of account subjectivity and

risk of material misstatement on auditors' internal audit reliance judgments. Accounting

Horizons, 30(2), pp.225-238.

Brasel, K., Doxey, M.M., Grenier, J.H. and Reffett, A., 2016. Risk disclosure preceding negative

outcomes: The effects of reporting critical audit matters on judgments of auditor liability. The

Accounting Review, 91(5), pp.1345-1362.

Buckby, S., Gallery, G. and Ma, J., 2015. An analysis of risk management disclosures:

Australian evidence. Managerial Auditing Journal, 30(8/9), pp.812-869.

Euchner, J. and Ganguly, A., 2014. Business model innovation in practice. Research-Technology

Management, 57(6), pp.33-39.

Hisrich, R.D. and Ramadani, V., 2017. Entrepreneurial risk management. In Effective

Entrepreneurial Management (pp. 55-73). Springer, Cham.

Kline, J.J. and Hutchins, G., 2017. Enterprise risk management: a global focus on

standardization. Global Business and Organizational Excellence, 36(6), pp.44-53.

Luo, M., 2017. Enterprise Internal Control and Accounting Information Quality. Journal of

Financial Risk Management, 6(1), pp.16-26.

Sheedy, E. and Griffin, B., 2018. Risk governance, structures, culture, and behavior: A view

from the inside. Corporate Governance: An International Review, 26(1), pp.4-22.

Soudani, S.N., 2013. The impact of implementation of e-accounting system on financial

performance with effects of internal control systems. Research Journal of Finance and

Accounting, 4(11), pp.2222-1697.

Turner, L., Weickgenannt, A.B. and Copeland, M.K., 2016. Accounting Information Systems:

The Processes and Controls. John Wiley & Sons.

Zakaria, K.M., Nawawi, A. and Salin, A.S.A.P., 2016. Internal controls and fraud–empirical

evidence from oil and gas company. Journal of Financial crime, 23(4), pp.1154-1168.

Bedford, D.S. and Malmi, T., 2015. Configurations of control: An exploratory

analysis. Management Accounting Research, 27, pp.2-26.

Bhattacharjee, S., Maletta, M.J. and Moreno, K.K., 2015. The role of account subjectivity and

risk of material misstatement on auditors' internal audit reliance judgments. Accounting

Horizons, 30(2), pp.225-238.

Brasel, K., Doxey, M.M., Grenier, J.H. and Reffett, A., 2016. Risk disclosure preceding negative

outcomes: The effects of reporting critical audit matters on judgments of auditor liability. The

Accounting Review, 91(5), pp.1345-1362.

Buckby, S., Gallery, G. and Ma, J., 2015. An analysis of risk management disclosures:

Australian evidence. Managerial Auditing Journal, 30(8/9), pp.812-869.

Euchner, J. and Ganguly, A., 2014. Business model innovation in practice. Research-Technology

Management, 57(6), pp.33-39.

Hisrich, R.D. and Ramadani, V., 2017. Entrepreneurial risk management. In Effective

Entrepreneurial Management (pp. 55-73). Springer, Cham.

Kline, J.J. and Hutchins, G., 2017. Enterprise risk management: a global focus on

standardization. Global Business and Organizational Excellence, 36(6), pp.44-53.

Luo, M., 2017. Enterprise Internal Control and Accounting Information Quality. Journal of

Financial Risk Management, 6(1), pp.16-26.

Sheedy, E. and Griffin, B., 2018. Risk governance, structures, culture, and behavior: A view

from the inside. Corporate Governance: An International Review, 26(1), pp.4-22.

Soudani, S.N., 2013. The impact of implementation of e-accounting system on financial

performance with effects of internal control systems. Research Journal of Finance and

Accounting, 4(11), pp.2222-1697.

Turner, L., Weickgenannt, A.B. and Copeland, M.K., 2016. Accounting Information Systems:

The Processes and Controls. John Wiley & Sons.

Zakaria, K.M., Nawawi, A. and Salin, A.S.A.P., 2016. Internal controls and fraud–empirical

evidence from oil and gas company. Journal of Financial crime, 23(4), pp.1154-1168.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.