Analysis of Adam & Co.'s Accounting Information System (HA2042)

VerifiedAdded on 2022/11/04

|17

|2838

|56

Case Study

AI Summary

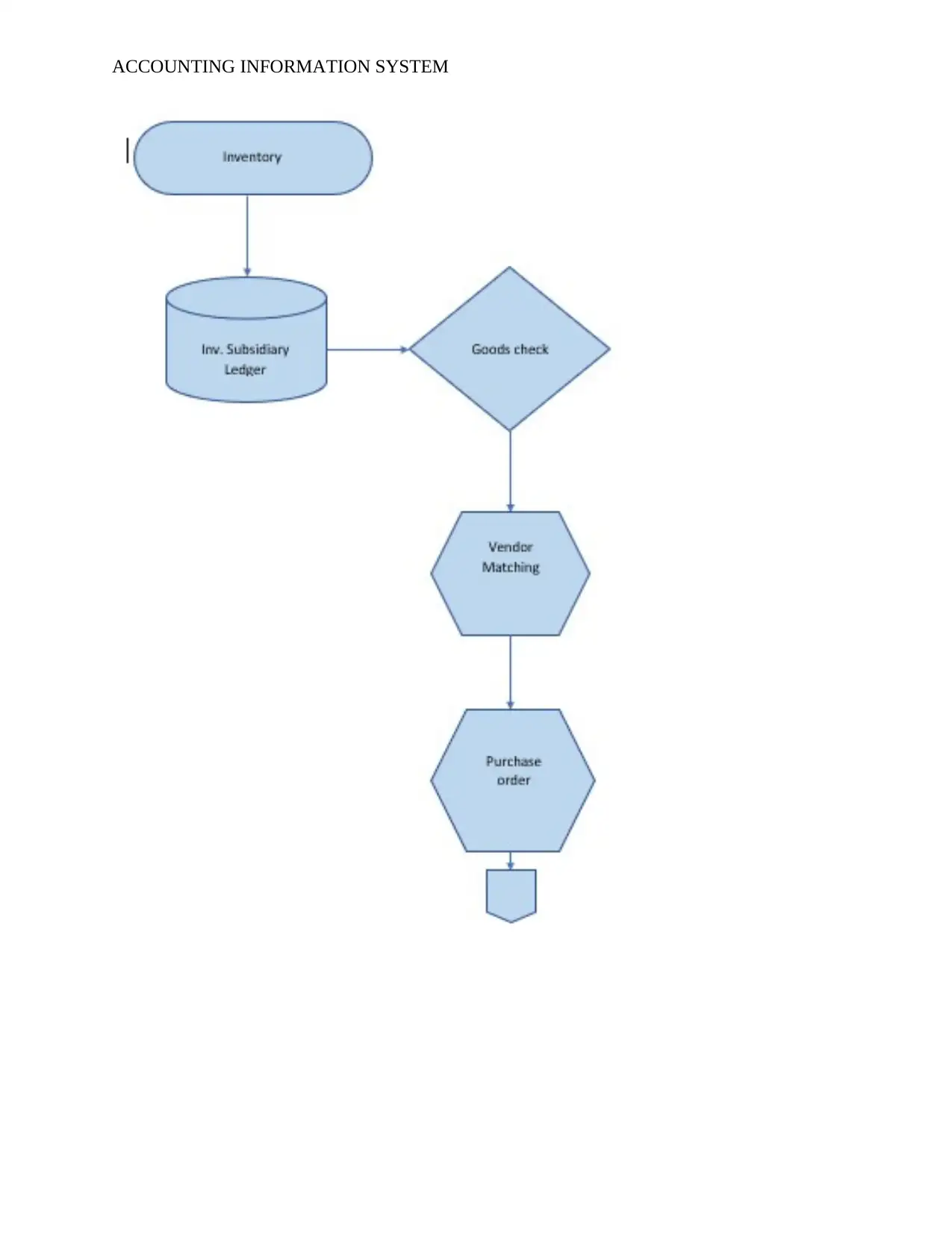

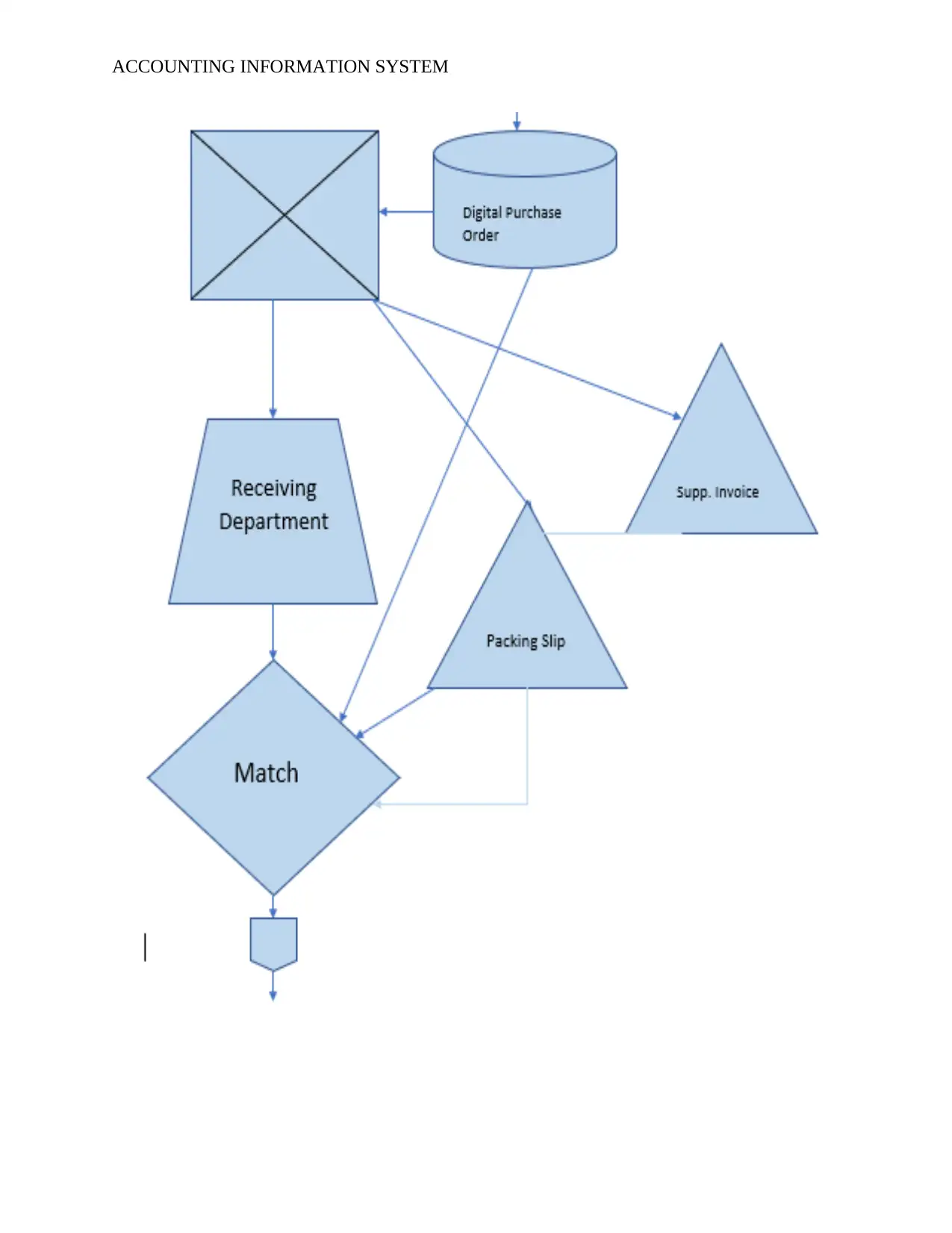

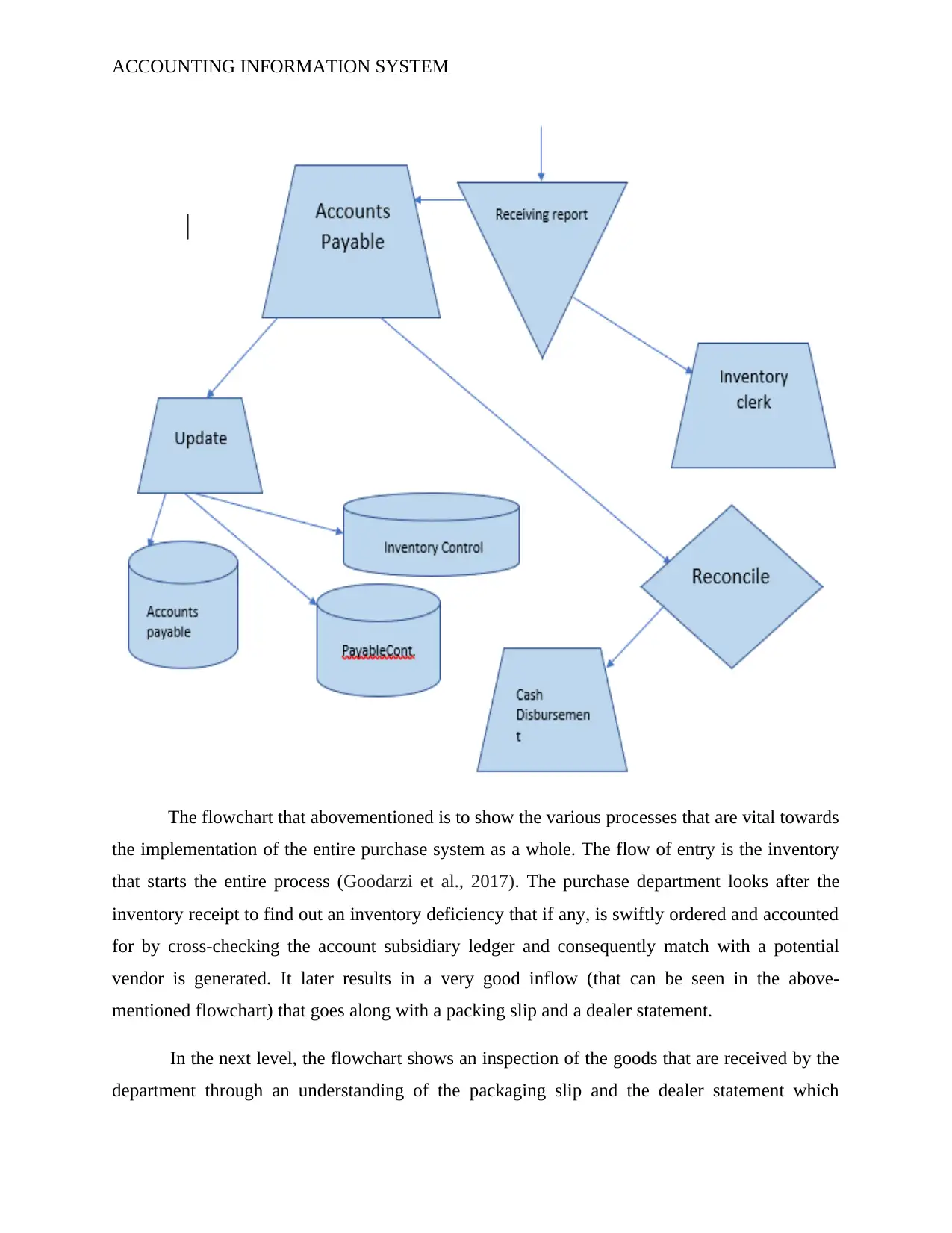

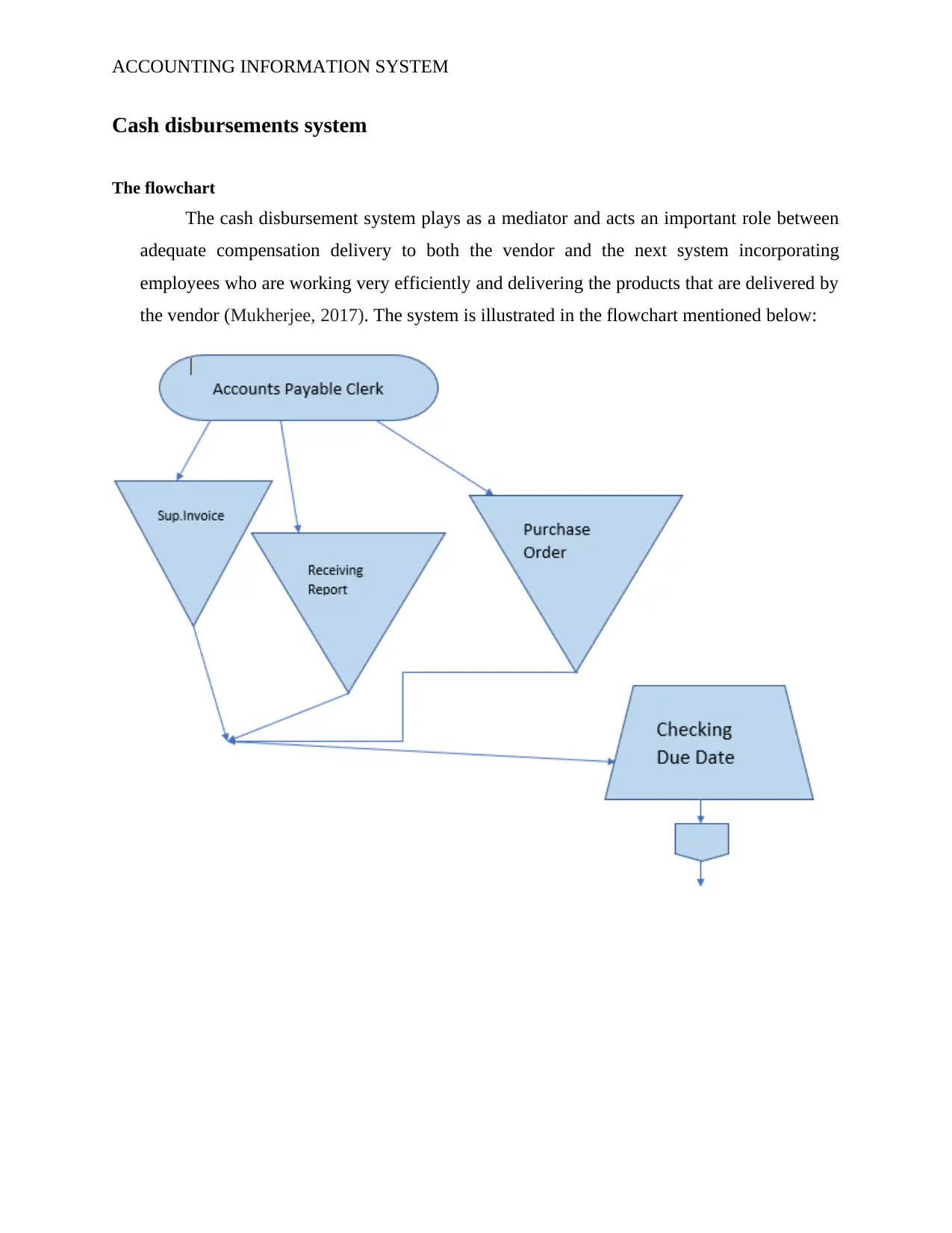

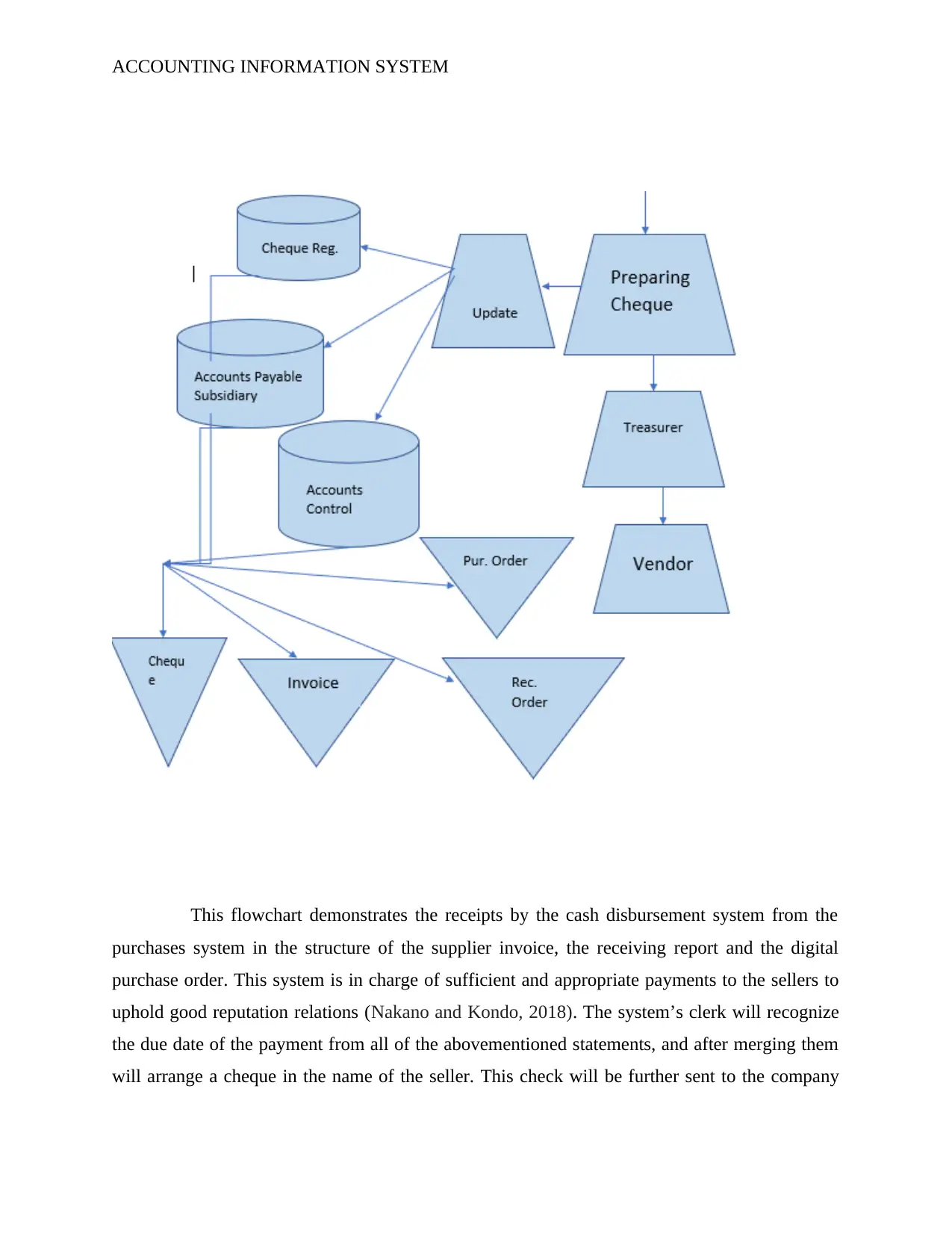

This case study analyzes the accounting information system (AIS) of Adam & Co., a wholesaler based in Perth. It examines the expenditure cycle, which is divided into three key processes: the purchase system, the cash disbursement system, and the payroll system. The analysis includes flowcharts illustrating the data flow and internal controls for each process. The purchase system covers inventory management, vendor selection, and goods receipt, while the cash disbursement system focuses on payments to vendors. The payroll system addresses employee time tracking and payment processing. The report identifies potential risks and internal control weaknesses within each system, offering solutions to improve efficiency and mitigate errors. The assignment aims to provide a comprehensive overview of Adam & Co.'s AIS, highlighting areas for improvement and ensuring the stability and accuracy of its financial processes.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.