University Accounting Information System Report and Analysis

VerifiedAdded on 2023/01/03

|11

|2292

|42

Report

AI Summary

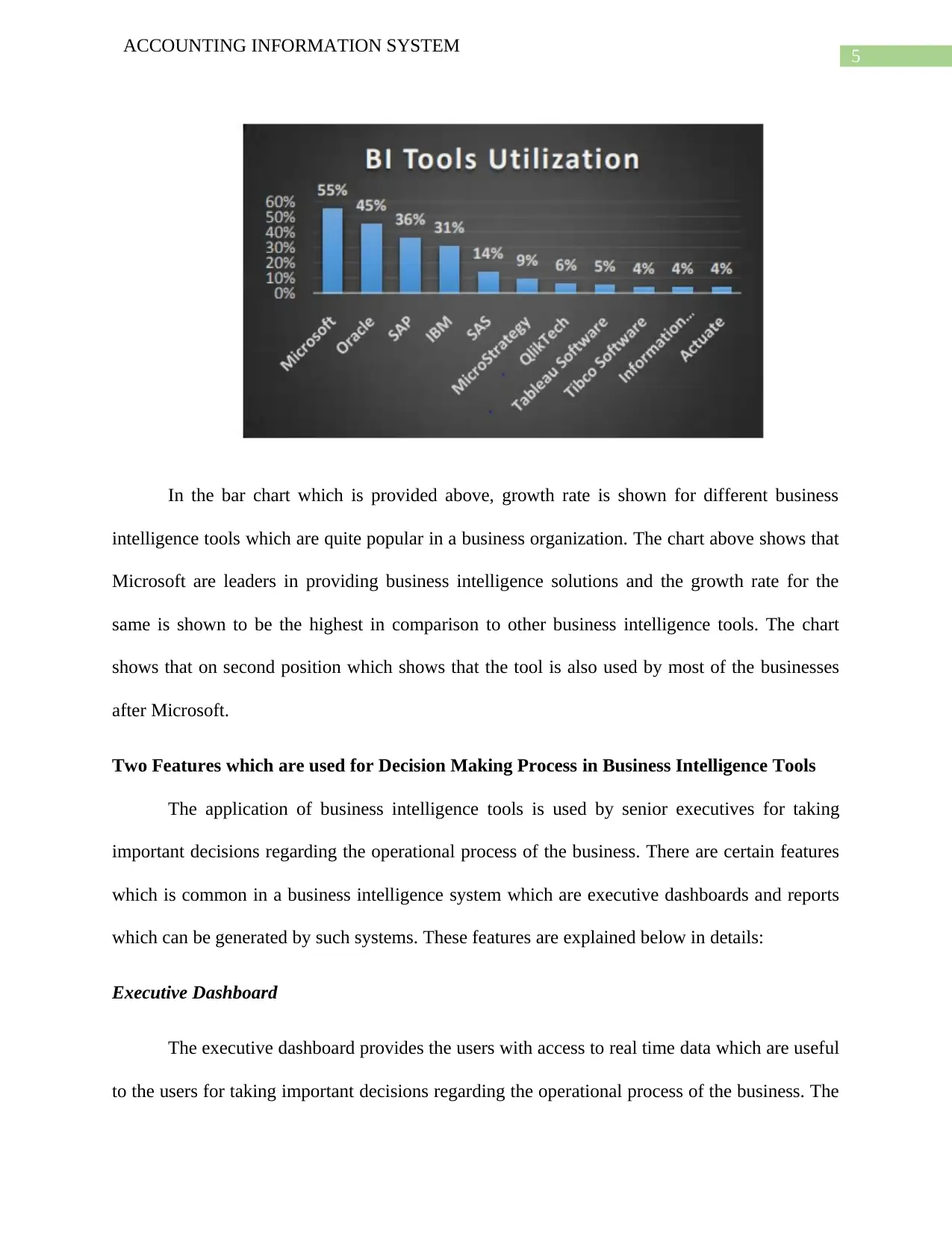

This report delves into the intricacies of Accounting Information Systems (AIS), addressing key aspects such as business intelligence, ethical conduct, and practical applications. The report begins by examining the growth of business intelligence over recent years, highlighting the increasing use of tools like CRM and Big Data for enhanced decision-making and improved consumer experiences. It then explores two critical features of business intelligence tools: executive dashboards and interactive reports, emphasizing their role in data analysis and strategic decision-making. The report further examines the importance of ethics in business, using the Enron scandal as a case study to illustrate the consequences of unethical accounting practices and the subsequent implementation of regulations like the Sarbanes-Oxley Act. The analysis incorporates visual aids such as graphs and charts to illustrate trends and findings, providing a comprehensive overview of AIS principles and their practical implications within the business environment. This report is a valuable resource for students studying accounting, providing insights into the practical application of AIS concepts and the importance of ethical considerations in financial reporting.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.