Accounting Information System Report for Adam & Co

VerifiedAdded on 2022/12/14

|15

|2687

|294

Report

AI Summary

This report provides a comprehensive overview of Accounting Information Systems (AIS). It begins with an executive summary and introduces the concept of AIS, emphasizing its importance in modern business environments for strategic decision-making. The report details the core principles of AIS, including source documents, data collection devices, processing devices, storage devices, and output methods. It then delves into the six key components: people, procedures and instructions, data, software, IT infrastructure, and internal controls. Furthermore, the report explores three main types of AIS: purchasing systems, cash disbursement systems, and payroll systems, discussing their functions, advantages, and disadvantages. The conclusion highlights the role of AIS in enhancing efficiency, cost-effectiveness, and decision-making within organizations, emphasizing the importance of a well-managed AIS for business success. The report includes a reference list of sources used.

Running Head: ACCOUNTING INFORMATION SYSTEM

Accounting information system

Name of the Student:

Name of the University:

Author notes:

Accounting information system

Name of the Student:

Name of the University:

Author notes:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING INFORMATION SYSTEM

Executive summary

This report explains about the accounting information system of Adam & co and its field

of operation in the market. Next it is discussed about the different types of accounting

information system by analyzing and comparing them. Then it is discussed about the

different methodology to evaluate various types of accounting information system.

ACCOUNTING INFORMATION SYSTEM

Executive summary

This report explains about the accounting information system of Adam & co and its field

of operation in the market. Next it is discussed about the different types of accounting

information system by analyzing and comparing them. Then it is discussed about the

different methodology to evaluate various types of accounting information system.

2

ACCOUNTING INFORMATION SYSTEM

Table of Contents

Introduction........................................................................................................................3

Principles...........................................................................................................................4

Components.......................................................................................................................5

Types.................................................................................................................................7

Conclusion.......................................................................................................................12

Reference list...................................................................................................................13

ACCOUNTING INFORMATION SYSTEM

Table of Contents

Introduction........................................................................................................................3

Principles...........................................................................................................................4

Components.......................................................................................................................5

Types.................................................................................................................................7

Conclusion.......................................................................................................................12

Reference list...................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING INFORMATION SYSTEM

Introduction

Accounting information system or AIS is a system that a business uses to

process the accounting, financial data and store to keep the business financial records

in order. It involves collecting and storing the financial data useful for the users in

reporting the financial information to the shareholders or owners and other. In this

modern rapid changing companies environment there is a need of high quality

information for making strategic decision which can be achieved only by an Accounting

information system (Belfo and Trigo 2013). It has a built in intelligent system which can

be customized capable of displaying the required information for a business. A well-

developed accounting information system with a well-trained accountant ensures a

highest level of accuracy in the financial statement of a company and record the

financial data easily. There are three basic functions which is available for performing

the accounting information systems like an AIS must collect and store all companies’

transaction data including recording data from the source, then AIS should be able to

provide useful and accurate information for decision making purpose in the business

and should be able to collect and process the financial data according to the

requirements. These AIS function provides the framework on which a business or

organization can rely of their information system is up to the mark. Without proper AIS

function there will be a larger threat for a company and its customers of having no

accounting information system (Brandas, Megan and Didraga 2015).

ACCOUNTING INFORMATION SYSTEM

Introduction

Accounting information system or AIS is a system that a business uses to

process the accounting, financial data and store to keep the business financial records

in order. It involves collecting and storing the financial data useful for the users in

reporting the financial information to the shareholders or owners and other. In this

modern rapid changing companies environment there is a need of high quality

information for making strategic decision which can be achieved only by an Accounting

information system (Belfo and Trigo 2013). It has a built in intelligent system which can

be customized capable of displaying the required information for a business. A well-

developed accounting information system with a well-trained accountant ensures a

highest level of accuracy in the financial statement of a company and record the

financial data easily. There are three basic functions which is available for performing

the accounting information systems like an AIS must collect and store all companies’

transaction data including recording data from the source, then AIS should be able to

provide useful and accurate information for decision making purpose in the business

and should be able to collect and process the financial data according to the

requirements. These AIS function provides the framework on which a business or

organization can rely of their information system is up to the mark. Without proper AIS

function there will be a larger threat for a company and its customers of having no

accounting information system (Brandas, Megan and Didraga 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING INFORMATION SYSTEM

Principles

Accounting information system consist of five basic principles operates on flexibility,

compatibility and cost benefit following the General Accepted Accounting Principles are

as follows:

1. Source documents – This is an important principles of accounting system that

refers to the document which contains the business transaction. They are

tangible documents which includes purchase order, invoice, sales order and

other related documents which are created during a business process (Daoud

and Triki 2013).

2. Device to collect input data – Accounting information system is connected with a

device which collects all input data received from the accountant of a business. It

has the ability to store bulky accounting data in seconds. Then this system

processes it and saves it in its digital file. All information is stored in it for decision

making and utilizing the information when required.

3. Processing device – Processing device is also connected to the AIS input device

which receives the input data from the collecting device and then process them

to store it in a customized digital format. Its main important objective is to

transform the accounting information into a decision making report. It has the

capability of processing huge information in few seconds (Galliers and Leidner

2014).

4. Storage device – Under this system it stores the information processed from the

processing device in a computer based storage device, flash drives, memory

ACCOUNTING INFORMATION SYSTEM

Principles

Accounting information system consist of five basic principles operates on flexibility,

compatibility and cost benefit following the General Accepted Accounting Principles are

as follows:

1. Source documents – This is an important principles of accounting system that

refers to the document which contains the business transaction. They are

tangible documents which includes purchase order, invoice, sales order and

other related documents which are created during a business process (Daoud

and Triki 2013).

2. Device to collect input data – Accounting information system is connected with a

device which collects all input data received from the accountant of a business. It

has the ability to store bulky accounting data in seconds. Then this system

processes it and saves it in its digital file. All information is stored in it for decision

making and utilizing the information when required.

3. Processing device – Processing device is also connected to the AIS input device

which receives the input data from the collecting device and then process them

to store it in a customized digital format. Its main important objective is to

transform the accounting information into a decision making report. It has the

capability of processing huge information in few seconds (Galliers and Leidner

2014).

4. Storage device – Under this system it stores the information processed from the

processing device in a computer based storage device, flash drives, memory

5

ACCOUNTING INFORMATION SYSTEM

cards and also cloud storage. This system can help to store data for giving

backup and also for decision making process.

5. Output – Accounting information system stores the processing data and provides

information when decision making is required and also provide backup in case of

any loss of data. This data are provided to the organization by a output media

which includes printer, projector, computers and other available technologies

(Hilton and Platt 2013).

Components

Accounting information consists of six components that help them to operate

efficiently are as follows:

1. People – This are the one who uses the information system. They are the

professionals who use the AIS which include an accountant, manager, auditor or

financial officers of the organization. This system helps every department to work

together to control the financial matter efficiently. With well-designed AIS within

an organization everyone can access the same information as all are using the

same system. This system is designed to meet the user’s needs, improve

efficiency without any obstruction (Ismail and King 2014).

2. Procedure and instruction - This includes the methods of collecting, processing,

storing and retrieval of data made up of both automated and manual component

after compiling data from the internal and external sources. This includes all

aspects of how a company’s AIS actually work.

3. Data – It includes all the information that is processed by the AIS by storing the

information into its database structure. AIS have various inputs for different users

ACCOUNTING INFORMATION SYSTEM

cards and also cloud storage. This system can help to store data for giving

backup and also for decision making process.

5. Output – Accounting information system stores the processing data and provides

information when decision making is required and also provide backup in case of

any loss of data. This data are provided to the organization by a output media

which includes printer, projector, computers and other available technologies

(Hilton and Platt 2013).

Components

Accounting information consists of six components that help them to operate

efficiently are as follows:

1. People – This are the one who uses the information system. They are the

professionals who use the AIS which include an accountant, manager, auditor or

financial officers of the organization. This system helps every department to work

together to control the financial matter efficiently. With well-designed AIS within

an organization everyone can access the same information as all are using the

same system. This system is designed to meet the user’s needs, improve

efficiency without any obstruction (Ismail and King 2014).

2. Procedure and instruction - This includes the methods of collecting, processing,

storing and retrieval of data made up of both automated and manual component

after compiling data from the internal and external sources. This includes all

aspects of how a company’s AIS actually work.

3. Data – It includes all the information that is processed by the AIS by storing the

information into its database structure. AIS have various inputs for different users

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING INFORMATION SYSTEM

and entries as different output is needed to different users. Data’s in AIS contains

all financial information of a business which contains information like sales order,

customer information, sales report, payroll information and tax information. This

data helps to create accounting statements and reports which facilitates auditing

and decision making (Mancini, Vaassen and Dameri 2013).

4. Software – AIS uses computer programing software which is used to store,

retrieve, analyze and process the financial data. It is a user friendly, efficient and

reliable system for a big organization. Reliability and quality are the key

components of AIS software on which the organization rely on for outputs to help

decision making. This software can be customized to meet the user’s needs and

according to their business types.

5. IT Infrastructure - Information technology infrastructure consist of normal office

equipment’s like computers, monitors, routers, software’s and other required

equipment. IT infrastructure helps the organization to run efficiently by optimizing

all software requirements. IT infrastructure also has a backup plan in case of

hardware crash, power failure or any equipment failure. It is an important part as

hardware selection is a vital component for AIS (Neogy 2014).

6. Internal control – AIS has internal control system to provide securities measure to

protect sensitive information or data’s. These internal controls protect the data

from viruses, hacker and other who wants to take advantage of the business

data. So AIS must have an internal control system to protect from unauthorized

access. AIS consist of not only companies’ data but also customer’s information

and it is an important part of the accounting system. These controls can be taken

ACCOUNTING INFORMATION SYSTEM

and entries as different output is needed to different users. Data’s in AIS contains

all financial information of a business which contains information like sales order,

customer information, sales report, payroll information and tax information. This

data helps to create accounting statements and reports which facilitates auditing

and decision making (Mancini, Vaassen and Dameri 2013).

4. Software – AIS uses computer programing software which is used to store,

retrieve, analyze and process the financial data. It is a user friendly, efficient and

reliable system for a big organization. Reliability and quality are the key

components of AIS software on which the organization rely on for outputs to help

decision making. This software can be customized to meet the user’s needs and

according to their business types.

5. IT Infrastructure - Information technology infrastructure consist of normal office

equipment’s like computers, monitors, routers, software’s and other required

equipment. IT infrastructure helps the organization to run efficiently by optimizing

all software requirements. IT infrastructure also has a backup plan in case of

hardware crash, power failure or any equipment failure. It is an important part as

hardware selection is a vital component for AIS (Neogy 2014).

6. Internal control – AIS has internal control system to provide securities measure to

protect sensitive information or data’s. These internal controls protect the data

from viruses, hacker and other who wants to take advantage of the business

data. So AIS must have an internal control system to protect from unauthorized

access. AIS consist of not only companies’ data but also customer’s information

and it is an important part of the accounting system. These controls can be taken

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING INFORMATION SYSTEM

by applying different types of securities measures like applying password in the

system or by providing biometric (Otley and Emmanuel 2013).

Types

Accounting information system of Adam & co that helps to simplify the making of

financial reporting to make a decision making purpose including all the components of

the accounting process. AIS are basically computer based device using software. There

are three types of accounting information system which are as follows:

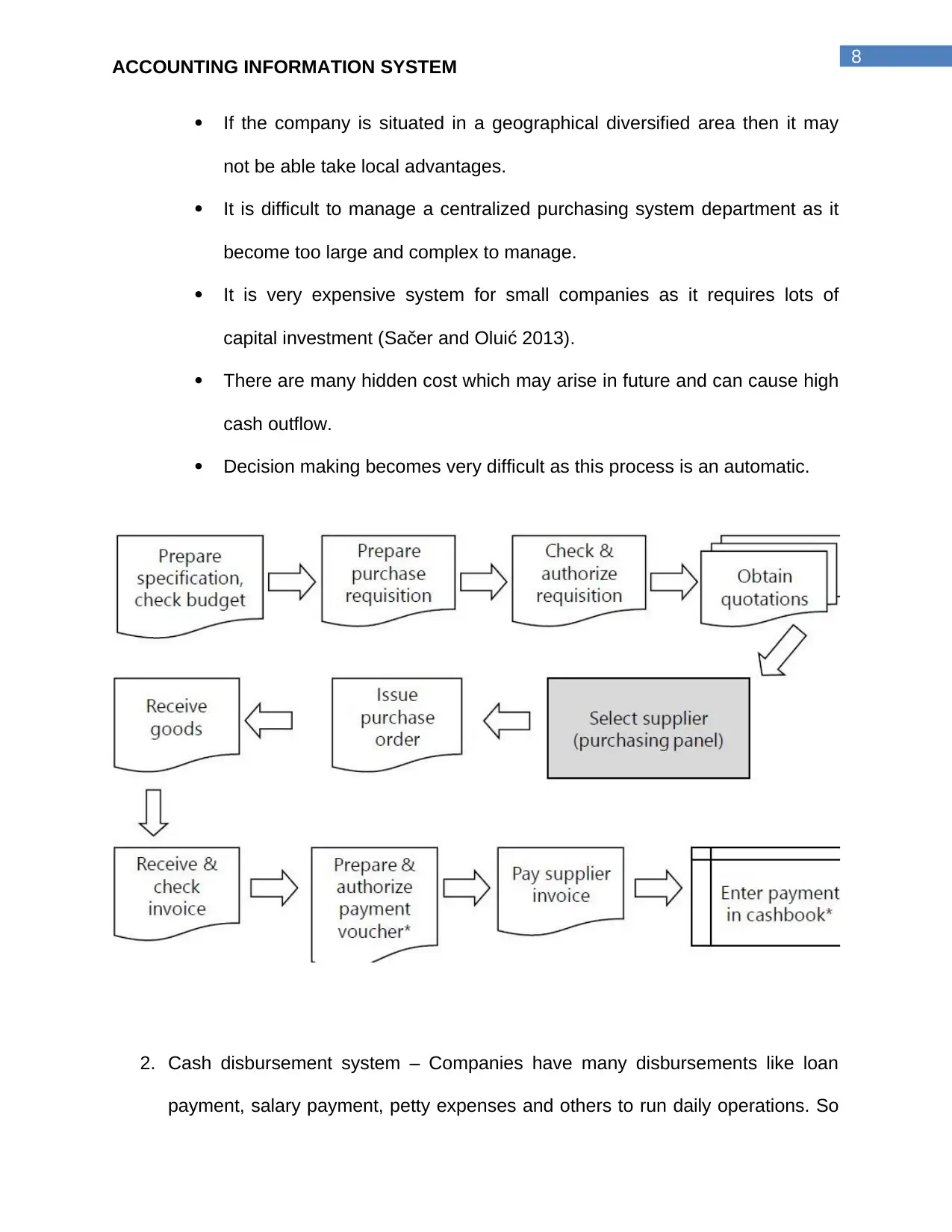

1. Purchasing system – It is a system or set of processes used to purchase goods

and services for an organization which includes purchase requisition, evaluating

suppliers, negotiating for price, purchase order and disposal of assets.

Purchasing system is an important component of the management that helps the

companies to determine what to buy, how much to buy and when to buy. This

system is based on economic order quantity which helps to control the

companies’ cash outflow and reduce supply cost to ensure effective use of

resources and cash (Rikhardsson 2017). Purchasing system is a computerized

based system which helps the company to reduce administrative cost, human

errors and also minimize shortage of stock. The key element of purchasing

system is planning the production system which can automatically know the need

of purchase to restore the stock supplies. But there are still some disadvantage

of this system like as follows:

Sending purchase requirement from purchase department to the creditor

is a time consuming process.

ACCOUNTING INFORMATION SYSTEM

by applying different types of securities measures like applying password in the

system or by providing biometric (Otley and Emmanuel 2013).

Types

Accounting information system of Adam & co that helps to simplify the making of

financial reporting to make a decision making purpose including all the components of

the accounting process. AIS are basically computer based device using software. There

are three types of accounting information system which are as follows:

1. Purchasing system – It is a system or set of processes used to purchase goods

and services for an organization which includes purchase requisition, evaluating

suppliers, negotiating for price, purchase order and disposal of assets.

Purchasing system is an important component of the management that helps the

companies to determine what to buy, how much to buy and when to buy. This

system is based on economic order quantity which helps to control the

companies’ cash outflow and reduce supply cost to ensure effective use of

resources and cash (Rikhardsson 2017). Purchasing system is a computerized

based system which helps the company to reduce administrative cost, human

errors and also minimize shortage of stock. The key element of purchasing

system is planning the production system which can automatically know the need

of purchase to restore the stock supplies. But there are still some disadvantage

of this system like as follows:

Sending purchase requirement from purchase department to the creditor

is a time consuming process.

8

ACCOUNTING INFORMATION SYSTEM

If the company is situated in a geographical diversified area then it may

not be able take local advantages.

It is difficult to manage a centralized purchasing system department as it

become too large and complex to manage.

It is very expensive system for small companies as it requires lots of

capital investment (Sačer and Oluić 2013).

There are many hidden cost which may arise in future and can cause high

cash outflow.

Decision making becomes very difficult as this process is an automatic.

2. Cash disbursement system – Companies have many disbursements like loan

payment, salary payment, petty expenses and others to run daily operations. So

ACCOUNTING INFORMATION SYSTEM

If the company is situated in a geographical diversified area then it may

not be able take local advantages.

It is difficult to manage a centralized purchasing system department as it

become too large and complex to manage.

It is very expensive system for small companies as it requires lots of

capital investment (Sačer and Oluić 2013).

There are many hidden cost which may arise in future and can cause high

cash outflow.

Decision making becomes very difficult as this process is an automatic.

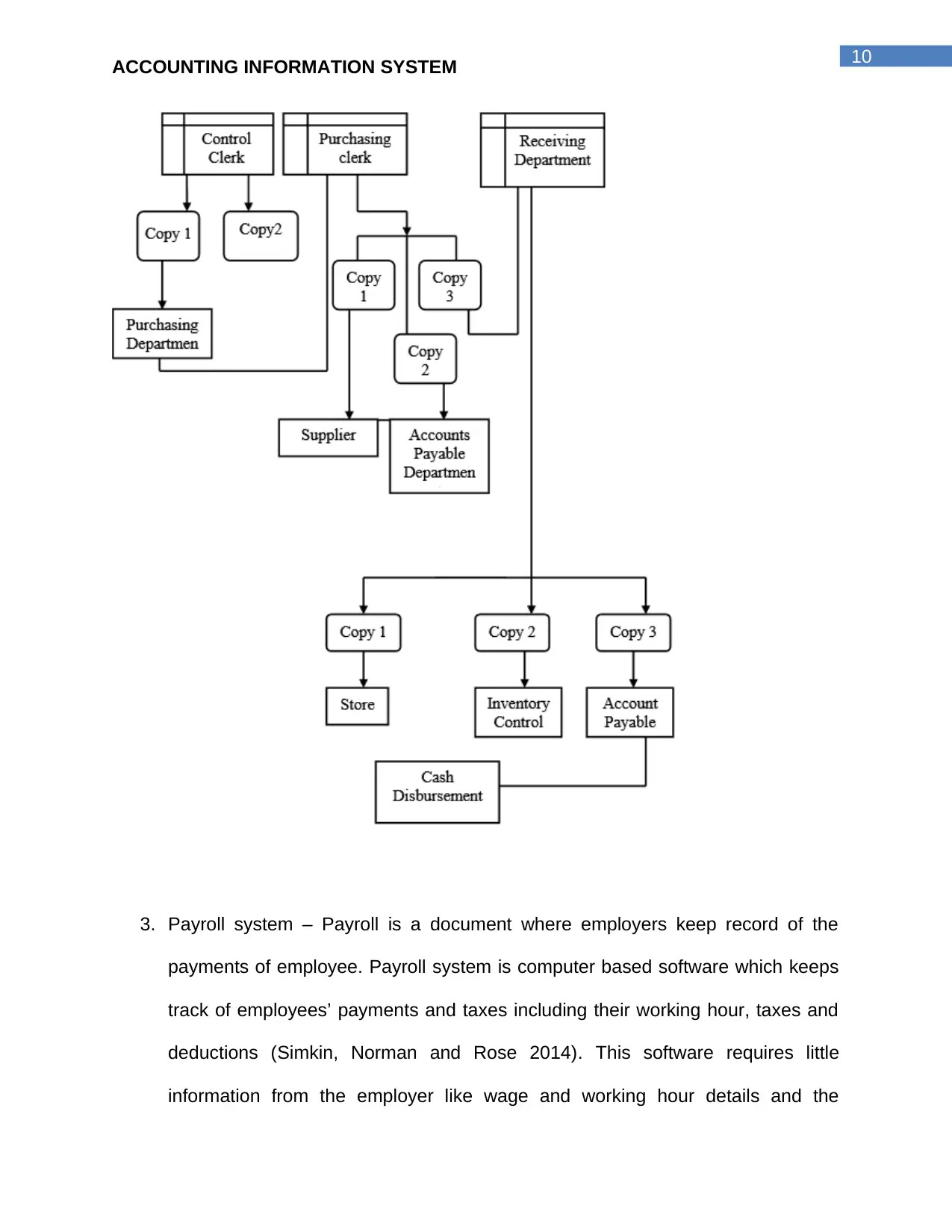

2. Cash disbursement system – Companies have many disbursements like loan

payment, salary payment, petty expenses and others to run daily operations. So

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING INFORMATION SYSTEM

to handle these payment accountants uses cash disbursement system which

involves repeatable process of payment with tracking of all expenditures. This

process requires the approval of manger to optimize the use of company’s capital

(Sledgianowski, Gomaa and Tan 2017). This system efficiently and securely

controls all of the companies’ cash payments as it is important to record all

financial information. Some of the disadvantages of this system are as follows:

If internal control system is not strong then this system may not be

effective or serve the purpose for which it should be used.

If a single department fails in internal control then there is a potential of

creation of weakness.

There is a chance of fraud if duties are not properly assigned.

Proper documents may not be available for every cash disbursement.

Without a proper book keeping department it would not be possible to

reflect the cash balance in the books of accounts.

ACCOUNTING INFORMATION SYSTEM

to handle these payment accountants uses cash disbursement system which

involves repeatable process of payment with tracking of all expenditures. This

process requires the approval of manger to optimize the use of company’s capital

(Sledgianowski, Gomaa and Tan 2017). This system efficiently and securely

controls all of the companies’ cash payments as it is important to record all

financial information. Some of the disadvantages of this system are as follows:

If internal control system is not strong then this system may not be

effective or serve the purpose for which it should be used.

If a single department fails in internal control then there is a potential of

creation of weakness.

There is a chance of fraud if duties are not properly assigned.

Proper documents may not be available for every cash disbursement.

Without a proper book keeping department it would not be possible to

reflect the cash balance in the books of accounts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING INFORMATION SYSTEM

3. Payroll system – Payroll is a document where employers keep record of the

payments of employee. Payroll system is computer based software which keeps

track of employees’ payments and taxes including their working hour, taxes and

deductions (Simkin, Norman and Rose 2014). This software requires little

information from the employer like wage and working hour details and the

ACCOUNTING INFORMATION SYSTEM

3. Payroll system – Payroll is a document where employers keep record of the

payments of employee. Payroll system is computer based software which keeps

track of employees’ payments and taxes including their working hour, taxes and

deductions (Simkin, Norman and Rose 2014). This software requires little

information from the employer like wage and working hour details and the

11

ACCOUNTING INFORMATION SYSTEM

remaining calculation will be done by the software. If any businesses have more

than one employee they must have this system to automatically process the

payroll which will simplify the legal and tax matters also. Some of the

disadvantages of payroll system are as follows:

Small business firms cannot implement this system as it is an expensive

system.

Choosing wrong payroll system may hamper the business as it is difficult

to decide the perfect system. Choosing system depends on some factors

like the size of the business and price of the payroll software.

Proper trained employees are required to handle this system or it can

hamper the business processes (Worrell, Wasko and Johnston 2013).

It requires some investment on computer equipment’s, resources and

skilled operators.

Using third party payroll system can cause security problems.

It is difficult to fix if any error occurred especially human error and

software error with inefficient customer care service.

ACCOUNTING INFORMATION SYSTEM

remaining calculation will be done by the software. If any businesses have more

than one employee they must have this system to automatically process the

payroll which will simplify the legal and tax matters also. Some of the

disadvantages of payroll system are as follows:

Small business firms cannot implement this system as it is an expensive

system.

Choosing wrong payroll system may hamper the business as it is difficult

to decide the perfect system. Choosing system depends on some factors

like the size of the business and price of the payroll software.

Proper trained employees are required to handle this system or it can

hamper the business processes (Worrell, Wasko and Johnston 2013).

It requires some investment on computer equipment’s, resources and

skilled operators.

Using third party payroll system can cause security problems.

It is difficult to fix if any error occurred especially human error and

software error with inefficient customer care service.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.