ACC1135: Analysis of Accounting Information Systems at FC Ltd.

VerifiedAdded on 2020/10/22

|11

|3283

|107

Report

AI Summary

This report analyzes the accounting information system (AIS) of Fabrik Clothing Ltd., a UK-based clothing company. It begins by defining useful information attributes such as reliability, relevance, and accuracy, providing examples relevant to the company's operations. The report then identifies threats to the revenue processing cycle, differentiating between intentional and unintentional acts, and pinpointing specific threats faced by Fabrik Clothing Ltd., such as cash theft and personnel performance issues. It explains how these threats damage the company's operations, particularly through weak internal controls and a lack of employee training. Furthermore, the report discusses threats to the existing information system, including weaknesses in the internal control environment, and suggests prevention methods. The report defines the COSO cube as a framework for internal control. The report identifies weaknesses in the company's existing internal control environment, explaining their impact on the business. The report concludes with a VAT return pivot table and final sheet of VAT returns.

ACC1135

ACCOUNTING INFORMATIONS SYSTEMS

MANAGEMENT OF FABRIK CLOTHING (FC LTD)

ACCOUNTING INFORMATIONS SYSTEMS

MANAGEMENT OF FABRIK CLOTHING (FC LTD)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction......................................................................................................................................3

TASK 1............................................................................................................................................3

1. Attributes to useful information.........................................................................................3

2. Useful information has different characteristics which are stated as below:.....................4

3. An example of useful information in the context of Fabrik Clothing Ltd..........................5

TASK 2............................................................................................................................................5

1. Threats to the revenue processing cycle.............................................................................5

The differences between unintentional and intentional acts...................................................5

2. Identification of threats that Fabrik Clothing Ltd face.......................................................6

3. Explanation of why threats are damaging the operation of Fabrik Clothing Ltd...............7

TASK 3............................................................................................................................................8

1. Threats to existing information system and potential prevention methods........................8

Defining COSO cube..............................................................................................................8

2. Identification of weaknesses in Fabrik Clothing Ltd.’s existing internal control environment

................................................................................................................................................9

3. Explanation of identifying them as weaknesses and their impact on the business............9

Conclusion.....................................................................................................................................10

REFERENCES..............................................................................................................................11

Introduction......................................................................................................................................3

TASK 1............................................................................................................................................3

1. Attributes to useful information.........................................................................................3

2. Useful information has different characteristics which are stated as below:.....................4

3. An example of useful information in the context of Fabrik Clothing Ltd..........................5

TASK 2............................................................................................................................................5

1. Threats to the revenue processing cycle.............................................................................5

The differences between unintentional and intentional acts...................................................5

2. Identification of threats that Fabrik Clothing Ltd face.......................................................6

3. Explanation of why threats are damaging the operation of Fabrik Clothing Ltd...............7

TASK 3............................................................................................................................................8

1. Threats to existing information system and potential prevention methods........................8

Defining COSO cube..............................................................................................................8

2. Identification of weaknesses in Fabrik Clothing Ltd.’s existing internal control environment

................................................................................................................................................9

3. Explanation of identifying them as weaknesses and their impact on the business............9

Conclusion.....................................................................................................................................10

REFERENCES..............................................................................................................................11

Introduction

Accounting information system is a framework or structure which used by business

organisation for multiple purposes associated with data and information such as data collecting,

storing, manipulating, processing etc. (Cañibano, 2018). This report aims to provide different

attributes of useful information that are necessary for running a business like Fabrik Clothing

Ltd. which is a UK based company established in 2015 by Susan Stimmer. To successfully run a

business, there should be proper management of data and information. In this report, different

threats to the revenue processing cycle, the threat to the existing information system and

potential prevention methods are explained. In the end, a complete VAT return pivot table is also

developed along with final sheet of VAT returns.

TASK 1

1. Attributes to useful information

Data:

Data is referred as raw, unorganised facts that needs to be processed into meaningful

information which is easily understandable and then utilised (De Mauro, Greco and Grimaldi,

2015). It can be something simple and seemingly random and useless until it is organised. It can

be any character, text, word or number which, if not put into correct context then it creates little

or nothing meaning to its evaluators. For example, when students get admission in a college, they

fill admission form. This form contains raw facts (data of student) like name, father’s name,

address of student, obtained marks, photo graph etc. This raw but diverse facts is an example of

data.

Information:

Information is referred as data formatted and processed in a manner that allows it to be

understood and utilised by human beings in some significant way (Janich, 2018). It is well-

organised, well-processed, structured and presented in a context so that it can be used for a

practical purpose and not only for theoretical purposes. The end users utilise this ‘meaningful

data’ which is known as ‘information’ for effective decision making. For example, if a manager

is told that company’s net profit has been decreased in the past month, manager may use this

information as a reason to cut financial spending for the next month. Another example, the

Accounting information system is a framework or structure which used by business

organisation for multiple purposes associated with data and information such as data collecting,

storing, manipulating, processing etc. (Cañibano, 2018). This report aims to provide different

attributes of useful information that are necessary for running a business like Fabrik Clothing

Ltd. which is a UK based company established in 2015 by Susan Stimmer. To successfully run a

business, there should be proper management of data and information. In this report, different

threats to the revenue processing cycle, the threat to the existing information system and

potential prevention methods are explained. In the end, a complete VAT return pivot table is also

developed along with final sheet of VAT returns.

TASK 1

1. Attributes to useful information

Data:

Data is referred as raw, unorganised facts that needs to be processed into meaningful

information which is easily understandable and then utilised (De Mauro, Greco and Grimaldi,

2015). It can be something simple and seemingly random and useless until it is organised. It can

be any character, text, word or number which, if not put into correct context then it creates little

or nothing meaning to its evaluators. For example, when students get admission in a college, they

fill admission form. This form contains raw facts (data of student) like name, father’s name,

address of student, obtained marks, photo graph etc. This raw but diverse facts is an example of

data.

Information:

Information is referred as data formatted and processed in a manner that allows it to be

understood and utilised by human beings in some significant way (Janich, 2018). It is well-

organised, well-processed, structured and presented in a context so that it can be used for a

practical purpose and not only for theoretical purposes. The end users utilise this ‘meaningful

data’ which is known as ‘information’ for effective decision making. For example, if a manager

is told that company’s net profit has been decreased in the past month, manager may use this

information as a reason to cut financial spending for the next month. Another example, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

average score of a class or of the entire school is information that can be derived from the data

contained in student forms.

2. Useful information has different characteristics which are stated as below:

Useful information creates value and contains appropriate level of briefing. It is

communicated in stimulated time and is relevant for its purpose; complete enough for the

problem resolution, reliable and even targeted to the right person. Few attributes of useful

information are described below:

Reliability:

This attribute deals with the truth of information or the objectivity with which information is

presented. According to this feature, information should be gathered from a valid and trusted

source so that evaluator can be relied upon it and can evidently prove it to be correct.

For example, Accounting information is reliable if users can depend on it to represent the

economic conditions or events that it proposes to represent. In the given case, information in

financial statements must be complete, free from errors and without bias so that information

provided to Susan, (the director) should not be incomplete due to any errors. Susan should be

able to have a high degree of confidence in the information presented by her from Rachel,

Caroline and David. She should be given a total picture of the weekly and monthly reporting

business as far as possible. It is desirable that all information required for decision making is

made available to her, but it should also be reliable so that overall profitability and productivity

of the organisation can be improved.

Relevance:

This refers to the attribute which shows that how helpful the information (in this case

financial information) is for financial decision-making processes. To be relevant, accounting

information must be capable of making a difference in a decision by helping users to form

predictions about the outcomes for future events and adequately analyse past and present events.

It is information’s ability to make a difference that makes it relevant to a decision. In Fabrik

Clothing Ltd, the report or information given by her store manager and account assistant must be

able to help Susan foresee the likely financial performance and the changes in the financial

position expected. Susan should be able to know the results of the investment and the

transactions that took place and she should be able to tell whether the results of the operation

match her expectations.

contained in student forms.

2. Useful information has different characteristics which are stated as below:

Useful information creates value and contains appropriate level of briefing. It is

communicated in stimulated time and is relevant for its purpose; complete enough for the

problem resolution, reliable and even targeted to the right person. Few attributes of useful

information are described below:

Reliability:

This attribute deals with the truth of information or the objectivity with which information is

presented. According to this feature, information should be gathered from a valid and trusted

source so that evaluator can be relied upon it and can evidently prove it to be correct.

For example, Accounting information is reliable if users can depend on it to represent the

economic conditions or events that it proposes to represent. In the given case, information in

financial statements must be complete, free from errors and without bias so that information

provided to Susan, (the director) should not be incomplete due to any errors. Susan should be

able to have a high degree of confidence in the information presented by her from Rachel,

Caroline and David. She should be given a total picture of the weekly and monthly reporting

business as far as possible. It is desirable that all information required for decision making is

made available to her, but it should also be reliable so that overall profitability and productivity

of the organisation can be improved.

Relevance:

This refers to the attribute which shows that how helpful the information (in this case

financial information) is for financial decision-making processes. To be relevant, accounting

information must be capable of making a difference in a decision by helping users to form

predictions about the outcomes for future events and adequately analyse past and present events.

It is information’s ability to make a difference that makes it relevant to a decision. In Fabrik

Clothing Ltd, the report or information given by her store manager and account assistant must be

able to help Susan foresee the likely financial performance and the changes in the financial

position expected. Susan should be able to know the results of the investment and the

transactions that took place and she should be able to tell whether the results of the operation

match her expectations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accuracy:

Good information should always be accurate and specific in nature. Effective decision

making relies upon accurate information. It should not have any arithmetical and grammatical

errors. In Fabrik Clothing Ltd., accuracy of financial information should be the key because it

will allow the business to predict what the future profit may be and how they could save money.

Any financial information that is given to Susan must be valid and accurate, there should be no

mistakes or errors made. Information that comes directly in written form from the company is

likely to be more reliable than it comes from indirect sources (transferred from various

intermediate mediums) or verbally which can be later retracted. The reason for this is that if

information is inaccurate, it can lead to the wrong decisions being made. Precise information

should be given to Susan, so that it will help her in making business decision easier (Penuel and

et.al., 2018).

3. An example of useful information in the context of Fabrik Clothing Ltd

The useful information that Fabrik clothing Ltd needs is an accurate data which is not

available to Susan. For example, the annual turnover of the company is £10000. But the

collection of turnovers shown to Susan is of £8000. The company is under-stating its revenue at

£2000 which is not favourable for the company.

Therefore, it can be said that the collection of data that comes to Susan is not accurate. Apart

from the above issues, the company is also facing an issue of information which is not available

to her on time (Hazen and et. al., 2018). The timeliness of information is necessary for the

successful implementation of a business. Late information not only becomes worthless but also

increases loss to the organisation. Data received by Susan through her store managers and

accounting assistant is evident to be inaccurate. But then also, that information is useful for

Susan as by concerning that only she can make decision related to her business. Even the

problems and causes for inaccurate information can be only derived with that information only.

TASK 2

1. Threats to the revenue processing cycle

The differences between unintentional and intentional acts.

Following are the differences between intentional and unintentional acts.

Basis of Comparison Unintentional Acts Intentional Acts

Good information should always be accurate and specific in nature. Effective decision

making relies upon accurate information. It should not have any arithmetical and grammatical

errors. In Fabrik Clothing Ltd., accuracy of financial information should be the key because it

will allow the business to predict what the future profit may be and how they could save money.

Any financial information that is given to Susan must be valid and accurate, there should be no

mistakes or errors made. Information that comes directly in written form from the company is

likely to be more reliable than it comes from indirect sources (transferred from various

intermediate mediums) or verbally which can be later retracted. The reason for this is that if

information is inaccurate, it can lead to the wrong decisions being made. Precise information

should be given to Susan, so that it will help her in making business decision easier (Penuel and

et.al., 2018).

3. An example of useful information in the context of Fabrik Clothing Ltd

The useful information that Fabrik clothing Ltd needs is an accurate data which is not

available to Susan. For example, the annual turnover of the company is £10000. But the

collection of turnovers shown to Susan is of £8000. The company is under-stating its revenue at

£2000 which is not favourable for the company.

Therefore, it can be said that the collection of data that comes to Susan is not accurate. Apart

from the above issues, the company is also facing an issue of information which is not available

to her on time (Hazen and et. al., 2018). The timeliness of information is necessary for the

successful implementation of a business. Late information not only becomes worthless but also

increases loss to the organisation. Data received by Susan through her store managers and

accounting assistant is evident to be inaccurate. But then also, that information is useful for

Susan as by concerning that only she can make decision related to her business. Even the

problems and causes for inaccurate information can be only derived with that information only.

TASK 2

1. Threats to the revenue processing cycle

The differences between unintentional and intentional acts.

Following are the differences between intentional and unintentional acts.

Basis of Comparison Unintentional Acts Intentional Acts

Definition These are the acts

which are carried out

unintentionally. Hence,

one cannot be held

accountable for

indulging in such acts.

In these acts one is

liable to all its

activities done as they

are carried out with an

intention, both positive

and negative.

Types of Acts Negligence

Occupier's liability

Vicarious Liability

Strict Liability

Commercial

Negligence

Assault and Battery

False Imprisonment

Defamation

Trespass

Nuisance

Liability Under this, the liability

will not remain with

the doer as it is

unintentional.

The liability of act is

fully dependent on the

doer as the task is done

intentionally.

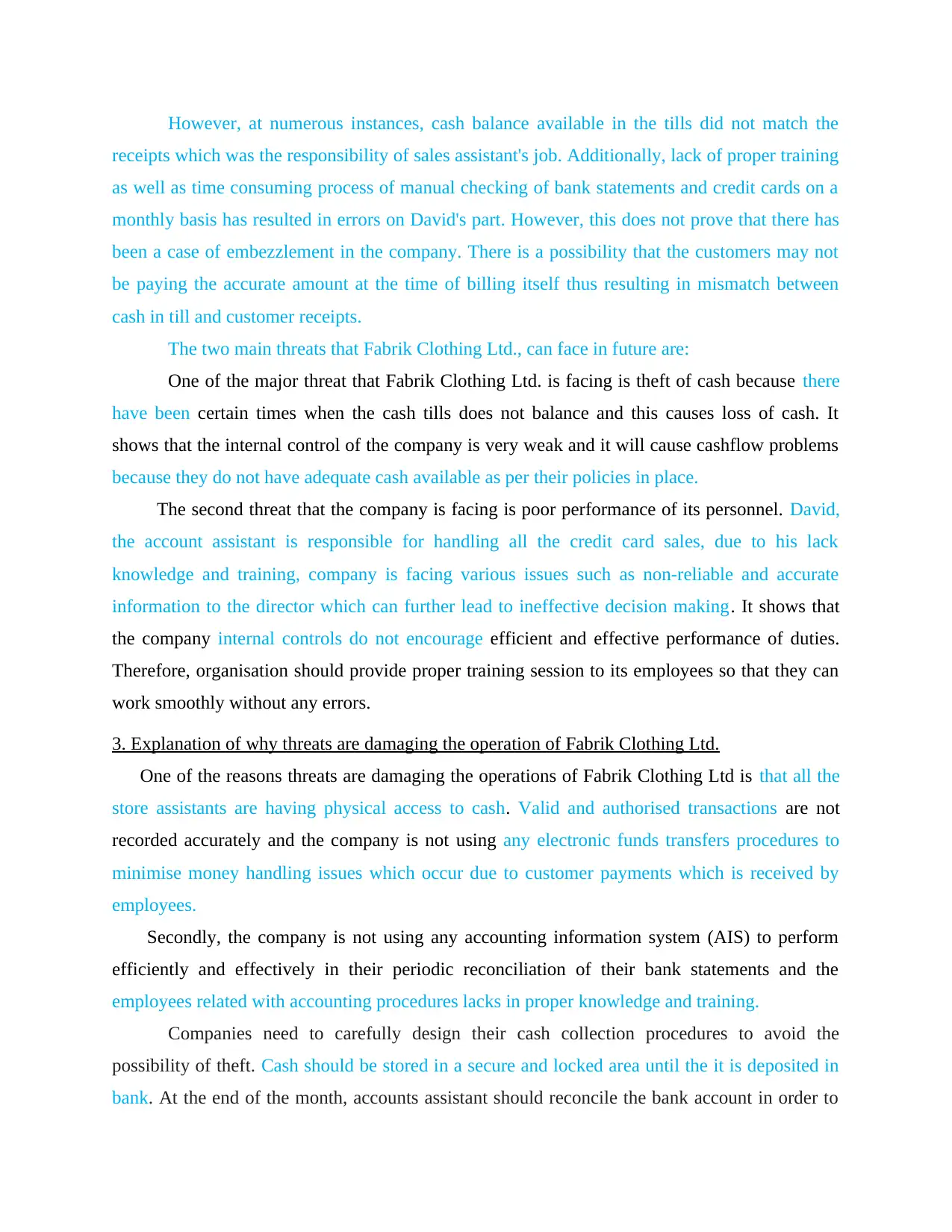

2. Identification of threats that Fabrik Clothing Ltd face

A revenue cycle refers to a set of recurring activities associated with selling products and

services to the customers and collecting cash in return in form of revenue generated (Wells and

Bravender, 2016). Fabrik Clothing Ltd.'s revenue cycle includes two main sources viz. Cash and

Credit Card. As mentioned in the case scenario, Susan receives a weekly report on sales and

expenses from Store Managers of both Watford and St. Albans Branches. Apart from this, she

also gets a month-wise income and expenses statement from her accounts assistant, David.

Before receiving these reports, the cash sales are updated by sales assistants of each branch as

and when they are made on a daily basis. This requires the assistants to balance the cash in till

with cash receipts at the end of their shifts every day. On the other hand, Credit Card Sales are

checked by David by comparing bank statements to card receipts at the end of each month.

However, Susan is not contented with this process.

which are carried out

unintentionally. Hence,

one cannot be held

accountable for

indulging in such acts.

In these acts one is

liable to all its

activities done as they

are carried out with an

intention, both positive

and negative.

Types of Acts Negligence

Occupier's liability

Vicarious Liability

Strict Liability

Commercial

Negligence

Assault and Battery

False Imprisonment

Defamation

Trespass

Nuisance

Liability Under this, the liability

will not remain with

the doer as it is

unintentional.

The liability of act is

fully dependent on the

doer as the task is done

intentionally.

2. Identification of threats that Fabrik Clothing Ltd face

A revenue cycle refers to a set of recurring activities associated with selling products and

services to the customers and collecting cash in return in form of revenue generated (Wells and

Bravender, 2016). Fabrik Clothing Ltd.'s revenue cycle includes two main sources viz. Cash and

Credit Card. As mentioned in the case scenario, Susan receives a weekly report on sales and

expenses from Store Managers of both Watford and St. Albans Branches. Apart from this, she

also gets a month-wise income and expenses statement from her accounts assistant, David.

Before receiving these reports, the cash sales are updated by sales assistants of each branch as

and when they are made on a daily basis. This requires the assistants to balance the cash in till

with cash receipts at the end of their shifts every day. On the other hand, Credit Card Sales are

checked by David by comparing bank statements to card receipts at the end of each month.

However, Susan is not contented with this process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

However, at numerous instances, cash balance available in the tills did not match the

receipts which was the responsibility of sales assistant's job. Additionally, lack of proper training

as well as time consuming process of manual checking of bank statements and credit cards on a

monthly basis has resulted in errors on David's part. However, this does not prove that there has

been a case of embezzlement in the company. There is a possibility that the customers may not

be paying the accurate amount at the time of billing itself thus resulting in mismatch between

cash in till and customer receipts.

The two main threats that Fabrik Clothing Ltd., can face in future are:

One of the major threat that Fabrik Clothing Ltd. is facing is theft of cash because there

have been certain times when the cash tills does not balance and this causes loss of cash. It

shows that the internal control of the company is very weak and it will cause cashflow problems

because they do not have adequate cash available as per their policies in place.

The second threat that the company is facing is poor performance of its personnel. David,

the account assistant is responsible for handling all the credit card sales, due to his lack

knowledge and training, company is facing various issues such as non-reliable and accurate

information to the director which can further lead to ineffective decision making. It shows that

the company internal controls do not encourage efficient and effective performance of duties.

Therefore, organisation should provide proper training session to its employees so that they can

work smoothly without any errors.

3. Explanation of why threats are damaging the operation of Fabrik Clothing Ltd.

One of the reasons threats are damaging the operations of Fabrik Clothing Ltd is that all the

store assistants are having physical access to cash. Valid and authorised transactions are not

recorded accurately and the company is not using any electronic funds transfers procedures to

minimise money handling issues which occur due to customer payments which is received by

employees.

Secondly, the company is not using any accounting information system (AIS) to perform

efficiently and effectively in their periodic reconciliation of their bank statements and the

employees related with accounting procedures lacks in proper knowledge and training.

Companies need to carefully design their cash collection procedures to avoid the

possibility of theft. Cash should be stored in a secure and locked area until the it is deposited in

bank. At the end of the month, accounts assistant should reconcile the bank account in order to

receipts which was the responsibility of sales assistant's job. Additionally, lack of proper training

as well as time consuming process of manual checking of bank statements and credit cards on a

monthly basis has resulted in errors on David's part. However, this does not prove that there has

been a case of embezzlement in the company. There is a possibility that the customers may not

be paying the accurate amount at the time of billing itself thus resulting in mismatch between

cash in till and customer receipts.

The two main threats that Fabrik Clothing Ltd., can face in future are:

One of the major threat that Fabrik Clothing Ltd. is facing is theft of cash because there

have been certain times when the cash tills does not balance and this causes loss of cash. It

shows that the internal control of the company is very weak and it will cause cashflow problems

because they do not have adequate cash available as per their policies in place.

The second threat that the company is facing is poor performance of its personnel. David,

the account assistant is responsible for handling all the credit card sales, due to his lack

knowledge and training, company is facing various issues such as non-reliable and accurate

information to the director which can further lead to ineffective decision making. It shows that

the company internal controls do not encourage efficient and effective performance of duties.

Therefore, organisation should provide proper training session to its employees so that they can

work smoothly without any errors.

3. Explanation of why threats are damaging the operation of Fabrik Clothing Ltd.

One of the reasons threats are damaging the operations of Fabrik Clothing Ltd is that all the

store assistants are having physical access to cash. Valid and authorised transactions are not

recorded accurately and the company is not using any electronic funds transfers procedures to

minimise money handling issues which occur due to customer payments which is received by

employees.

Secondly, the company is not using any accounting information system (AIS) to perform

efficiently and effectively in their periodic reconciliation of their bank statements and the

employees related with accounting procedures lacks in proper knowledge and training.

Companies need to carefully design their cash collection procedures to avoid the

possibility of theft. Cash should be stored in a secure and locked area until the it is deposited in

bank. At the end of the month, accounts assistant should reconcile the bank account in order to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ensure the accuracy of all deposits. Cash receipts should be processed more quickly in order to

improve cash flow situation of the organization. Reports and performance measures should be

timelier and enhance management’s ability to monitor and improve efficiency and effectiveness

of organization’s financial procedures.

TASK 3

1. Threats to existing information system and potential prevention methods

Defining COSO cube

COSO is the Committee of Sponsoring Organisations which was established in 1985 to

sponsor the National Commission on Fraudulent Financial Reporting. COSO cube helps us to

look at the whole organisations’ enterprise risk management model (Sari and et.al., 2018). It's

internal control framework is presented as a cube which have five components mentioned below:

The control environment:

It represents the culture of internal controls at an organisation. An organisation could have a

culture of discipline and compliance or a culture of lax policies and procedures. This culture

often begins with the actions of executive management. The elements that make up the internal

environment include such things as an entity's ethical values, competence and development of

personnel, management's operating style and how it assigns authority and responsibility. As part

of this internal environment, a company will establish its philosophy of risk management,

determine its risk appetite and will integrate Enterprise Risk Reporting.

Risk Assessment:

It is a process used to identify, assess and manage risks to the achievement of an entity’s

objectives.

Control Activities:

These activities are actions performed under the direction of management as directed by

an entity’s policies and procedures to mitigate the risks to the achievement of the entity’s

objectives.

Information and Communication:

This component is the distribution of information needed to perform control activities and

to understand internal control responsibilities to personnel internal and external to the entity.

improve cash flow situation of the organization. Reports and performance measures should be

timelier and enhance management’s ability to monitor and improve efficiency and effectiveness

of organization’s financial procedures.

TASK 3

1. Threats to existing information system and potential prevention methods

Defining COSO cube

COSO is the Committee of Sponsoring Organisations which was established in 1985 to

sponsor the National Commission on Fraudulent Financial Reporting. COSO cube helps us to

look at the whole organisations’ enterprise risk management model (Sari and et.al., 2018). It's

internal control framework is presented as a cube which have five components mentioned below:

The control environment:

It represents the culture of internal controls at an organisation. An organisation could have a

culture of discipline and compliance or a culture of lax policies and procedures. This culture

often begins with the actions of executive management. The elements that make up the internal

environment include such things as an entity's ethical values, competence and development of

personnel, management's operating style and how it assigns authority and responsibility. As part

of this internal environment, a company will establish its philosophy of risk management,

determine its risk appetite and will integrate Enterprise Risk Reporting.

Risk Assessment:

It is a process used to identify, assess and manage risks to the achievement of an entity’s

objectives.

Control Activities:

These activities are actions performed under the direction of management as directed by

an entity’s policies and procedures to mitigate the risks to the achievement of the entity’s

objectives.

Information and Communication:

This component is the distribution of information needed to perform control activities and

to understand internal control responsibilities to personnel internal and external to the entity.

Monitoring Activities:

These activities are ongoing evaluations of the implementation and operation of the five

components of internal audit.

2. Identification of weaknesses in Fabrik Clothing Ltd.’s existing internal control environment

Lack of training, information and communication:

In Fabrik Clothing Ltd., employees should be provided with ongoing training, support and

mentoring on a regular basis, so that they can use their knowledge and skills necessary to

accomplish tasks that define the individual’s job. There should be adequate induction procedures

for new employees, so that they can carry out their assigned responsibilities effectively and

efficiently soon after being engaged by the company. Finally, keeping current policies and

procedures available to their employees and communicate other critical information in a timely

manner.

Control Activities:

Susan has ultimate responsibility and ownership of the internal control system. She sets

the tone at the top that affects the integrity and ethics and other factors that create the positive

control environment needed for the internal control system to thrive. Aside from setting, the

tone at the top, much of the day‐to‐day operation of the control system is delegated to other

senior managers in the company, under the leadership of the CEO. This shows that the

environment of company is a culture of lax policies and procedures. The organisation has to

improve this procedure as soon as possible to ensure proper controlling of organisational

activities.

3. Explanation of identifying them as weaknesses and their impact on the business

In this case, the new appointed employee feels frustrated and annoying while asking for the

return policy of company. He felt that he does not have adequate knowledge, skills and training

to perform his role. This will impact badly onto the business because when employee starts to

think themselves as non-important for the organisation they start to switch to other available

options of employment which is harmful for the company. The founder of company Susan is

reluctant to start the investigation against the stealing of till from the funds. This shows that the

company is not serious about any fraud in it. This also inculcate lax policies and procedures in

the organisation. If this weakness is not diagnosed properly by investigation, the person who did

fraud will get motivated to do even bigger frauds. This results into the loss of business.

These activities are ongoing evaluations of the implementation and operation of the five

components of internal audit.

2. Identification of weaknesses in Fabrik Clothing Ltd.’s existing internal control environment

Lack of training, information and communication:

In Fabrik Clothing Ltd., employees should be provided with ongoing training, support and

mentoring on a regular basis, so that they can use their knowledge and skills necessary to

accomplish tasks that define the individual’s job. There should be adequate induction procedures

for new employees, so that they can carry out their assigned responsibilities effectively and

efficiently soon after being engaged by the company. Finally, keeping current policies and

procedures available to their employees and communicate other critical information in a timely

manner.

Control Activities:

Susan has ultimate responsibility and ownership of the internal control system. She sets

the tone at the top that affects the integrity and ethics and other factors that create the positive

control environment needed for the internal control system to thrive. Aside from setting, the

tone at the top, much of the day‐to‐day operation of the control system is delegated to other

senior managers in the company, under the leadership of the CEO. This shows that the

environment of company is a culture of lax policies and procedures. The organisation has to

improve this procedure as soon as possible to ensure proper controlling of organisational

activities.

3. Explanation of identifying them as weaknesses and their impact on the business

In this case, the new appointed employee feels frustrated and annoying while asking for the

return policy of company. He felt that he does not have adequate knowledge, skills and training

to perform his role. This will impact badly onto the business because when employee starts to

think themselves as non-important for the organisation they start to switch to other available

options of employment which is harmful for the company. The founder of company Susan is

reluctant to start the investigation against the stealing of till from the funds. This shows that the

company is not serious about any fraud in it. This also inculcate lax policies and procedures in

the organisation. If this weakness is not diagnosed properly by investigation, the person who did

fraud will get motivated to do even bigger frauds. This results into the loss of business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

From the above report, it can be concluded that data and information are the two different

aspects. The useful characteristics of information helps to identify the accurate and complete

information. In case of Fabrik Clothing Ltd., the fraud of company is still not investigated by

Susan as they felt it is wasting of money. The threats which influence the company are unbalance

of cash till, lack of training to the employees etc. COSO tube is also helpful in this report to

identify and resolve the issues related with the company. It is also observed that various

weakness such as lack of training influences this company.

From the above report, it can be concluded that data and information are the two different

aspects. The useful characteristics of information helps to identify the accurate and complete

information. In case of Fabrik Clothing Ltd., the fraud of company is still not investigated by

Susan as they felt it is wasting of money. The threats which influence the company are unbalance

of cash till, lack of training to the employees etc. COSO tube is also helpful in this report to

identify and resolve the issues related with the company. It is also observed that various

weakness such as lack of training influences this company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Cañibano, L., 2018. Accounting and intangibles. Revista de Contabilidad-Spanish Accounting

Review, 21(1). pp.1-6.

De Mauro, A., Greco, M. and Grimaldi, M., 2015, February. What is big data? A consensual

definition and a review of key research topics. In AIP conference proceedings (Vol. 1644.

No. 1. pp. 97-104). AIP.

Janich, P., 2018. What Is Information? (Vol. 55). U of Minnesota Press.

Penuel, W. R., and et.al., 2018. What research district leaders find useful. Educational

Policy, 32(4). pp.540-568.

Wells, S. T. and Bravender, R., 2016. Improving employee engagement in the revenue

cycle. Healthcare Financial Management, 70(10). pp.36-39.

Sari, R., and et.al., 2018. October. COSO Framework for Warehouse Management Internal

Control Evaluation: Enabling Smart Warehouse Systems. In 2018 International

Conference on ICT for Smart Society (ICISS) (pp. 1-5). IEEE.

Books and Journals

Cañibano, L., 2018. Accounting and intangibles. Revista de Contabilidad-Spanish Accounting

Review, 21(1). pp.1-6.

De Mauro, A., Greco, M. and Grimaldi, M., 2015, February. What is big data? A consensual

definition and a review of key research topics. In AIP conference proceedings (Vol. 1644.

No. 1. pp. 97-104). AIP.

Janich, P., 2018. What Is Information? (Vol. 55). U of Minnesota Press.

Penuel, W. R., and et.al., 2018. What research district leaders find useful. Educational

Policy, 32(4). pp.540-568.

Wells, S. T. and Bravender, R., 2016. Improving employee engagement in the revenue

cycle. Healthcare Financial Management, 70(10). pp.36-39.

Sari, R., and et.al., 2018. October. COSO Framework for Warehouse Management Internal

Control Evaluation: Enabling Smart Warehouse Systems. In 2018 International

Conference on ICT for Smart Society (ICISS) (pp. 1-5). IEEE.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.