ACC539 Report: Analysis of Accounting Information Systems and Controls

VerifiedAdded on 2023/01/18

|15

|2300

|83

Report

AI Summary

This report presents a comprehensive analysis of accounting information systems, focusing on two case studies: Oriental Traders and Chipps. Part A of the report documents the acquisition-to-payment system of Oriental Traders through a flowchart, detailing the process from purchase requisition to payment. Part B examines the internal control weaknesses within Chipps, assessing associated risks and proposing control measures to mitigate these weaknesses. The report identifies weaknesses such as approval process inefficiencies, communication issues, poor record-keeping, lack of segregation in purchasing and receiving processes, and escalating consumption patterns. It provides detailed impacts of these weaknesses and suggests specific controls, including the implementation of ERP systems, formation of inspection committees, and improved record-keeping. The report concludes with recommendations for both companies, emphasizing the importance of automated systems and robust internal controls to prevent fraud and improve efficiency.

1

Running Head: ACCOUNTING INFORMATION SYSTEMS

Accounting information systems

Student’s name

Affiliate institution

Date

Running Head: ACCOUNTING INFORMATION SYSTEMS

Accounting information systems

Student’s name

Affiliate institution

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

ACCOUNTING INFORMATION SYSTEMS

To: Oriental Traders

From: System Analyst

Topic: The Acquisition To Payment System Of Oriental Traders

Date: 10th May 2019

ACCOUNTING INFORMATION SYSTEMS

To: Oriental Traders

From: System Analyst

Topic: The Acquisition To Payment System Of Oriental Traders

Date: 10th May 2019

3

ACCOUNTING INFORMATION SYSTEMS

Part A

Executive summary

The purpose of this report was to analyze and develop a word flowchart that indicates the

type of purchasing process in Oriental Traders. The report also aimed at the identification of

internal control weakness in the expenditure of the company. The report also aimed at providing

the risks which are associated with the related weakness in Oriental Traders Company. The

report concludes by giving a recommendation of the available control to mitigate the indentified

Oriental Traders internal control weaknesses. This report also aims at providing a clear

illustrated purchase process of Oriental Traders.

ACCOUNTING INFORMATION SYSTEMS

Part A

Executive summary

The purpose of this report was to analyze and develop a word flowchart that indicates the

type of purchasing process in Oriental Traders. The report also aimed at the identification of

internal control weakness in the expenditure of the company. The report also aimed at providing

the risks which are associated with the related weakness in Oriental Traders Company. The

report concludes by giving a recommendation of the available control to mitigate the indentified

Oriental Traders internal control weaknesses. This report also aims at providing a clear

illustrated purchase process of Oriental Traders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

ACCOUNTING INFORMATION SYSTEMS

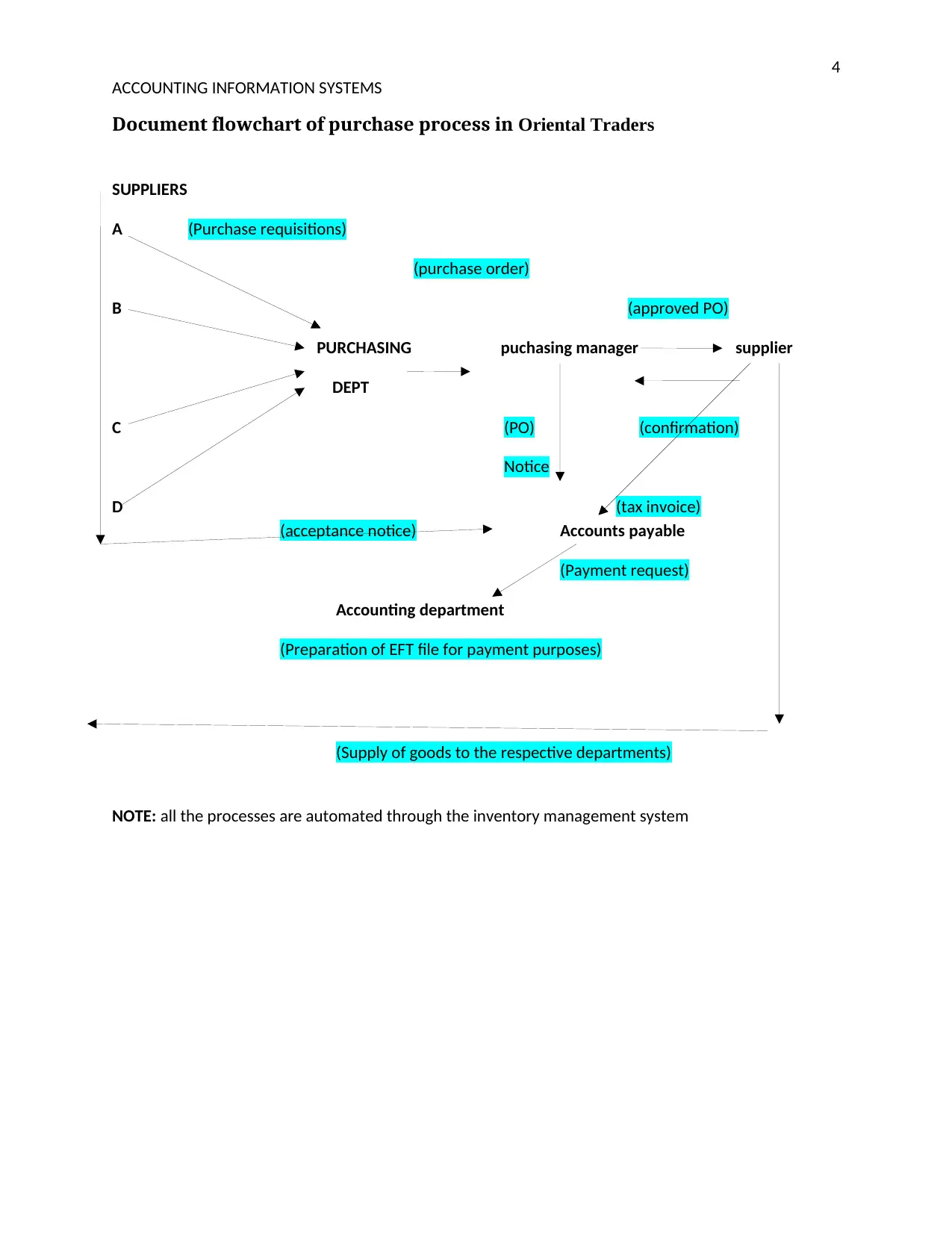

Document flowchart of purchase process in Oriental Traders

SUPPLIERS

A (Purchase requisitions)

(purchase order)

B (approved PO)

PURCHASING puchasing manager supplier

DEPT

C (PO) (confirmation)

Notice

D (tax invoice)

(acceptance notice) Accounts payable

(Payment request)

Accounting department

(Preparation of EFT file for payment purposes)

(Supply of goods to the respective departments)

NOTE: all the processes are automated through the inventory management system

ACCOUNTING INFORMATION SYSTEMS

Document flowchart of purchase process in Oriental Traders

SUPPLIERS

A (Purchase requisitions)

(purchase order)

B (approved PO)

PURCHASING puchasing manager supplier

DEPT

C (PO) (confirmation)

Notice

D (tax invoice)

(acceptance notice) Accounts payable

(Payment request)

Accounting department

(Preparation of EFT file for payment purposes)

(Supply of goods to the respective departments)

NOTE: all the processes are automated through the inventory management system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

ACCOUNTING INFORMATION SYSTEMS

To: Chipps

From: Chipps Accountant

Topic: Internal Control Weaknesses, Risks And Control Measures

Date: 10th May 2019

ACCOUNTING INFORMATION SYSTEMS

To: Chipps

From: Chipps Accountant

Topic: Internal Control Weaknesses, Risks And Control Measures

Date: 10th May 2019

6

ACCOUNTING INFORMATION SYSTEMS

Part B

Executive summary

This report aims at the examination of internal control weaknesses which are found in Chipps

Company. Te report also aims at the assessment of all the risks which are associated with the various

indentified internal control weaknesses. Moreover, the report aims at the provision f the available

control proce4dures which can be followed in order to mitigate the indentified in Chipps. The report

finally concludes with a recommendation for Chipps Company.

ACCOUNTING INFORMATION SYSTEMS

Part B

Executive summary

This report aims at the examination of internal control weaknesses which are found in Chipps

Company. Te report also aims at the assessment of all the risks which are associated with the various

indentified internal control weaknesses. Moreover, the report aims at the provision f the available

control proce4dures which can be followed in order to mitigate the indentified in Chipps. The report

finally concludes with a recommendation for Chipps Company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

ACCOUNTING INFORMATION SYSTEMS

Table of Contents

Part A...........................................................................................................................................................4

Executive summary..................................................................................................................................4

Document flowchart of purchase process in Oriental Traders................................................................5

Part B...........................................................................................................................................................6

Executive summary..................................................................................................................................6

1.0 Internal control weakness......................................................................................................................8

1.2 Impact of the weakness..........................................................................................................................8

1.3 Control to mitigate the weakness...........................................................................................................8

1.1 Approval process...............................................................................................................................8

1.2 communication procedure................................................................................................................8

1.3 Poor recordkeeping for....................................................................................................................10

intake, uses, requests, projected needs................................................................................................10

1.4 No segregation in purchasing receiving processes..........................................................................11

1.5 Escalating consumption pattern not detected nor reviewed...........................................................12

1.2.1 Impact of approval process internal control weakness..............................................................5

1.2.1 Impact of poor communication internal control weakness........................................................5

1.3.1 risks of poor record...................................................................................................................10

keeping..............................................................................................................................................10

1.4.1 Internal confusion.....................................................................................................................11

1.5.1 Lack of clear records.................................................................................................................12

1.2.2 Approval process internal control weakness control..................................................................5

1.2.2 mitigation of poor communication procedure as.......................................................................5

1.2.3 Formation of inspection and receiving committee.....................................................................9

1.3.2 control of poor record keeping.................................................................................................10

1.4.2 Introduction of a receiving department and officers................................................................11

1.5.2 Frequent reporting...................................................................................................................12

Conclusion.................................................................................................................................................13

others.......................................................................................................................................................13

Recommendations.....................................................................................................................................13

ACCOUNTING INFORMATION SYSTEMS

Table of Contents

Part A...........................................................................................................................................................4

Executive summary..................................................................................................................................4

Document flowchart of purchase process in Oriental Traders................................................................5

Part B...........................................................................................................................................................6

Executive summary..................................................................................................................................6

1.0 Internal control weakness......................................................................................................................8

1.2 Impact of the weakness..........................................................................................................................8

1.3 Control to mitigate the weakness...........................................................................................................8

1.1 Approval process...............................................................................................................................8

1.2 communication procedure................................................................................................................8

1.3 Poor recordkeeping for....................................................................................................................10

intake, uses, requests, projected needs................................................................................................10

1.4 No segregation in purchasing receiving processes..........................................................................11

1.5 Escalating consumption pattern not detected nor reviewed...........................................................12

1.2.1 Impact of approval process internal control weakness..............................................................5

1.2.1 Impact of poor communication internal control weakness........................................................5

1.3.1 risks of poor record...................................................................................................................10

keeping..............................................................................................................................................10

1.4.1 Internal confusion.....................................................................................................................11

1.5.1 Lack of clear records.................................................................................................................12

1.2.2 Approval process internal control weakness control..................................................................5

1.2.2 mitigation of poor communication procedure as.......................................................................5

1.2.3 Formation of inspection and receiving committee.....................................................................9

1.3.2 control of poor record keeping.................................................................................................10

1.4.2 Introduction of a receiving department and officers................................................................11

1.5.2 Frequent reporting...................................................................................................................12

Conclusion.................................................................................................................................................13

others.......................................................................................................................................................13

Recommendations.....................................................................................................................................13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

ACCOUNTING INFORMATION SYSTEMS

References.............................................................................................................................................15

ACCOUNTING INFORMATION SYSTEMS

References.............................................................................................................................................15

9

ACCOUNTING INFORMATION SYSTEMS

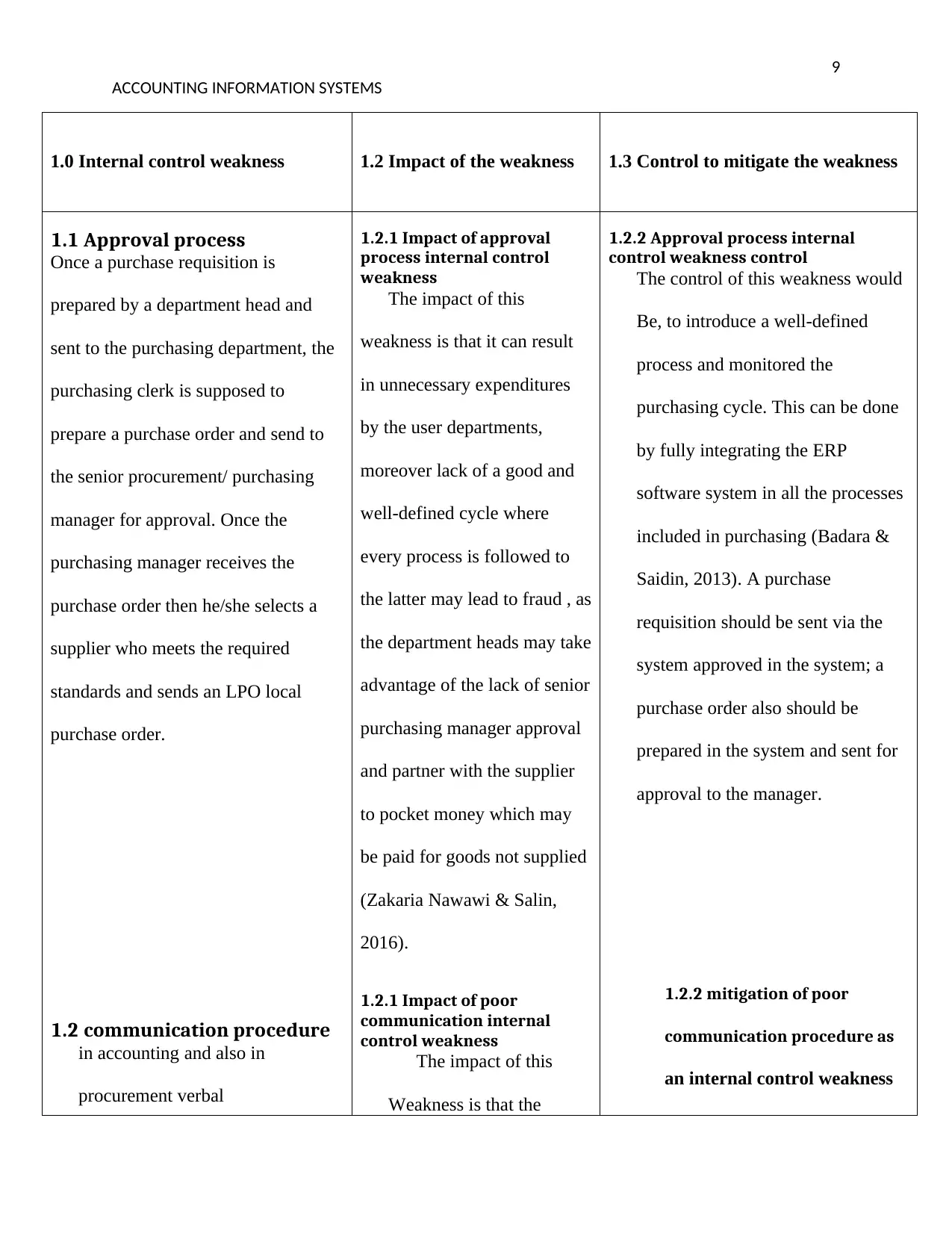

1.0 Internal control weakness 1.2 Impact of the weakness 1.3 Control to mitigate the weakness

1.1 Approval process

Once a purchase requisition is

prepared by a department head and

sent to the purchasing department, the

purchasing clerk is supposed to

prepare a purchase order and send to

the senior procurement/ purchasing

manager for approval. Once the

purchasing manager receives the

purchase order then he/she selects a

supplier who meets the required

standards and sends an LPO local

purchase order.

1.2 communication procedure

in accounting and also in

procurement verbal

1.2.1 Impact of approval

process internal control

weakness

The impact of this

weakness is that it can result

in unnecessary expenditures

by the user departments,

moreover lack of a good and

well-defined cycle where

every process is followed to

the latter may lead to fraud , as

the department heads may take

advantage of the lack of senior

purchasing manager approval

and partner with the supplier

to pocket money which may

be paid for goods not supplied

(Zakaria Nawawi & Salin,

2016).

1.2.1 Impact of poor

communication internal

control weakness

The impact of this

Weakness is that the

1.2.2 Approval process internal

control weakness control

The control of this weakness would

Be, to introduce a well-defined

process and monitored the

purchasing cycle. This can be done

by fully integrating the ERP

software system in all the processes

included in purchasing (Badara &

Saidin, 2013). A purchase

requisition should be sent via the

system approved in the system; a

purchase order also should be

prepared in the system and sent for

approval to the manager.

1.2.2 mitigation of poor

communication procedure as

an internal control weakness

ACCOUNTING INFORMATION SYSTEMS

1.0 Internal control weakness 1.2 Impact of the weakness 1.3 Control to mitigate the weakness

1.1 Approval process

Once a purchase requisition is

prepared by a department head and

sent to the purchasing department, the

purchasing clerk is supposed to

prepare a purchase order and send to

the senior procurement/ purchasing

manager for approval. Once the

purchasing manager receives the

purchase order then he/she selects a

supplier who meets the required

standards and sends an LPO local

purchase order.

1.2 communication procedure

in accounting and also in

procurement verbal

1.2.1 Impact of approval

process internal control

weakness

The impact of this

weakness is that it can result

in unnecessary expenditures

by the user departments,

moreover lack of a good and

well-defined cycle where

every process is followed to

the latter may lead to fraud , as

the department heads may take

advantage of the lack of senior

purchasing manager approval

and partner with the supplier

to pocket money which may

be paid for goods not supplied

(Zakaria Nawawi & Salin,

2016).

1.2.1 Impact of poor

communication internal

control weakness

The impact of this

Weakness is that the

1.2.2 Approval process internal

control weakness control

The control of this weakness would

Be, to introduce a well-defined

process and monitored the

purchasing cycle. This can be done

by fully integrating the ERP

software system in all the processes

included in purchasing (Badara &

Saidin, 2013). A purchase

requisition should be sent via the

system approved in the system; a

purchase order also should be

prepared in the system and sent for

approval to the manager.

1.2.2 mitigation of poor

communication procedure as

an internal control weakness

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

ACCOUNTING INFORMATION SYSTEMS

communication is not a

professional way to conduct a

purchase. Chipps has not embraced

a professional way of conducting

purchases as the purchasing clerk

uses a phone to discuss a price

quote. In accounting, the price

quote should be sent as a request

for quotation to several selected

suppliers who have been listed for

the product and service required.

Once the suppliers through a

segment in the ERP system replies

to that request an analysis should

be conducted and the best supplier

and not the lowest bidder should

be sent a local purchase order

requesting the supplier to make

deliveries. Moreover, verbal

communication in Chipps from the

user department to the purchasing

clerk noticing them that the goods

had been received is also not a

company can suffer from

excess expenditure and

payment of non-supplied

goods. Hence may end up

suffering losses.

The control for this internal

control weakness would be, the

installation and fully embracement

of the ERP system to automate

every step from requisition to

payment.

1.2.3 Formation of inspection and

receiving committee

The second control would be the

formation of inspection and

receiving committee which will be

used to countercheck the goods

received against the local purchase

order which was given out (Badara

& Saidin, 2013).

ACCOUNTING INFORMATION SYSTEMS

communication is not a

professional way to conduct a

purchase. Chipps has not embraced

a professional way of conducting

purchases as the purchasing clerk

uses a phone to discuss a price

quote. In accounting, the price

quote should be sent as a request

for quotation to several selected

suppliers who have been listed for

the product and service required.

Once the suppliers through a

segment in the ERP system replies

to that request an analysis should

be conducted and the best supplier

and not the lowest bidder should

be sent a local purchase order

requesting the supplier to make

deliveries. Moreover, verbal

communication in Chipps from the

user department to the purchasing

clerk noticing them that the goods

had been received is also not a

company can suffer from

excess expenditure and

payment of non-supplied

goods. Hence may end up

suffering losses.

The control for this internal

control weakness would be, the

installation and fully embracement

of the ERP system to automate

every step from requisition to

payment.

1.2.3 Formation of inspection and

receiving committee

The second control would be the

formation of inspection and

receiving committee which will be

used to countercheck the goods

received against the local purchase

order which was given out (Badara

& Saidin, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

ACCOUNTING INFORMATION SYSTEMS

professional way to report as it can

attract greediness to corrupt if

receiving inspection does not

involve individuals from several

departments to act as witnesses.

1.3 Poor recordkeeping for

intake, uses, requests,

projected needs

This weakness can be easily be traced

from the purchasing process of chipps,

a purchasing clerk uses a phone call to

request for a quotation. In an

organized company the request for a

quotation should be automated and

where a previous order was given the

past price quotation has used the

inquiry by the clerk shows that the

company lacks a well-defined

recordkeeping rule. More so, the

verbal notification of goods received

indicates that the company did not

make use of goods received a note and

other important records such as issue

notice and goods returned notice.

1.3.1 risks of poor record

keeping

The impact of this

The departmental heads can

make use of the verbal

communication to lie to the

purchasing clerk that goods

have been received while In

reality nothing has been

supplied.

Lack of future reference

Another risk is that due

to lack of proper

documentation fraud cases are

not easy to be traced or even

be audited.

Purchasing fraud

Finally, the company will

incur expenses for goods and

services which were not

1.3.2 control of poor record keeping

The control to this will be the

implication of an online system for

record keeping. This can be achieved

through installation of a database

software which will be used as the

company achieve where ever

documents will be backed up for easy

retrieval during inspection or audit

purposes (Nicolăescu, 2013).

ACCOUNTING INFORMATION SYSTEMS

professional way to report as it can

attract greediness to corrupt if

receiving inspection does not

involve individuals from several

departments to act as witnesses.

1.3 Poor recordkeeping for

intake, uses, requests,

projected needs

This weakness can be easily be traced

from the purchasing process of chipps,

a purchasing clerk uses a phone call to

request for a quotation. In an

organized company the request for a

quotation should be automated and

where a previous order was given the

past price quotation has used the

inquiry by the clerk shows that the

company lacks a well-defined

recordkeeping rule. More so, the

verbal notification of goods received

indicates that the company did not

make use of goods received a note and

other important records such as issue

notice and goods returned notice.

1.3.1 risks of poor record

keeping

The impact of this

The departmental heads can

make use of the verbal

communication to lie to the

purchasing clerk that goods

have been received while In

reality nothing has been

supplied.

Lack of future reference

Another risk is that due

to lack of proper

documentation fraud cases are

not easy to be traced or even

be audited.

Purchasing fraud

Finally, the company will

incur expenses for goods and

services which were not

1.3.2 control of poor record keeping

The control to this will be the

implication of an online system for

record keeping. This can be achieved

through installation of a database

software which will be used as the

company achieve where ever

documents will be backed up for easy

retrieval during inspection or audit

purposes (Nicolăescu, 2013).

12

ACCOUNTING INFORMATION SYSTEMS

1.4 No segregation in

purchasing receiving processes

This can be easily been traced in

Chippy as the requester department is

the receiver and hence the company

lacked a very critical department

which receives and issues goods to the

department upon need. The store is a

very critical department which has to

be integrated in each business for

proper segregation of purchasing and

receiving activities. In cases where

their is a store verbal communication

is killed and goods received notes as

well as well documented goods issue

note are prepared to ensure efficiency

in the operation of the company.

supplied hence incurring loss

through an increase in the

operational cost as compared

to the revenue generated.

1.4.1 Internal confusion

Lack of a well segregated

activities will lead to

confusion whereby even the

limitation of products use is

not regulated. Hence the

company will be suffering

from wasteful use or

unnecessary disposals which

have not matured (Dorotinsky

& Floyd, 2014). As it is

always known departments

will always be requesting for

more and more every day but

if a regulatory department

exists cases of fraud will

decrease hence saving the

companies expenses.

1.4.2 Introduction of a receiving

department and officers

The control to this weakness will

be the introduction of a receiving

officer who will be mandated to control

the request and usage of goods in the

company.

Improved recording

Another remedy would be proper

recording of department expenditure

monthly reporting.

ACCOUNTING INFORMATION SYSTEMS

1.4 No segregation in

purchasing receiving processes

This can be easily been traced in

Chippy as the requester department is

the receiver and hence the company

lacked a very critical department

which receives and issues goods to the

department upon need. The store is a

very critical department which has to

be integrated in each business for

proper segregation of purchasing and

receiving activities. In cases where

their is a store verbal communication

is killed and goods received notes as

well as well documented goods issue

note are prepared to ensure efficiency

in the operation of the company.

supplied hence incurring loss

through an increase in the

operational cost as compared

to the revenue generated.

1.4.1 Internal confusion

Lack of a well segregated

activities will lead to

confusion whereby even the

limitation of products use is

not regulated. Hence the

company will be suffering

from wasteful use or

unnecessary disposals which

have not matured (Dorotinsky

& Floyd, 2014). As it is

always known departments

will always be requesting for

more and more every day but

if a regulatory department

exists cases of fraud will

decrease hence saving the

companies expenses.

1.4.2 Introduction of a receiving

department and officers

The control to this weakness will

be the introduction of a receiving

officer who will be mandated to control

the request and usage of goods in the

company.

Improved recording

Another remedy would be proper

recording of department expenditure

monthly reporting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.