Adam & Co.: Accounting Information Systems Case Study Analysis

VerifiedAdded on 2022/11/02

|14

|2554

|342

Case Study

AI Summary

This case study analyzes the accounting information systems (AIS) of Adam & Co., a wholesaler of industrial supplies. The assessment focuses on the purchase system, cash disbursement system, and payroll system, evaluating their efficiency and internal controls. The analysis identifies weaknesses in each system, such as the lack of coordination in the purchase system, risks in the cash disbursement process, and vulnerabilities in the payroll system due to employee self-reporting and inadequate review processes. The study concludes by recommending improvements, including enhanced communication between departments, progressive filing of documents, segregation of duties, and increased oversight to strengthen internal controls, thereby improving the overall expenditures cycle and reducing the risk of errors and fraud within the organization. The case study emphasizes the importance of a robust AIS for achieving organizational objectives.

Running head: ACCOUNTING INFORMATION SYSTEM

Accounting Information System

Name of the Student:

Name of the University:

Authors Note:

Accounting Information System

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING INFORMATION SYSTEM

Executive summary:

The systems and processes used within an organization determine the efficiency and

effectiveness of operations of such organization. It is important to institute strong and effective

internal controls to improve the quality of different systems and processes within the

organization. A brief look at the purchase system, cash disbursement system and payroll system

of Adam & Co. will enable the readers to understand the important elements needed to make

these systems efficient and effective to enable an organization to achieve its goals and objectives.

The weaknesses in internal controls the cash disbursement, purchase and payroll systems in

Adam &Co have been mentioned in the document below.

ACCOUNTING INFORMATION SYSTEM

Executive summary:

The systems and processes used within an organization determine the efficiency and

effectiveness of operations of such organization. It is important to institute strong and effective

internal controls to improve the quality of different systems and processes within the

organization. A brief look at the purchase system, cash disbursement system and payroll system

of Adam & Co. will enable the readers to understand the important elements needed to make

these systems efficient and effective to enable an organization to achieve its goals and objectives.

The weaknesses in internal controls the cash disbursement, purchase and payroll systems in

Adam &Co have been mentioned in the document below.

2

ACCOUNTING INFORMATION SYSTEM

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Systems:...........................................................................................................................................3

Evaluation of purchase system:...................................................................................................3

Risks and internal control evaluation of purchasing system:......................................................5

Evaluation of cash disbursement system:....................................................................................5

Risks and internal control evaluation of disbursement system:...................................................6

Evaluation of payroll system:......................................................................................................7

Risks and internal control evaluation of payroll system:.............................................................8

Conclusion:......................................................................................................................................9

Recommendations:..........................................................................................................................9

References:....................................................................................................................................13

ACCOUNTING INFORMATION SYSTEM

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Systems:...........................................................................................................................................3

Evaluation of purchase system:...................................................................................................3

Risks and internal control evaluation of purchasing system:......................................................5

Evaluation of cash disbursement system:....................................................................................5

Risks and internal control evaluation of disbursement system:...................................................6

Evaluation of payroll system:......................................................................................................7

Risks and internal control evaluation of payroll system:.............................................................8

Conclusion:......................................................................................................................................9

Recommendations:..........................................................................................................................9

References:....................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING INFORMATION SYSTEM

Introduction:

An organization generally establishes a standard system within the organization to ensure that

the purchases and other expenditures are incurred efficiently to achieve the organizational

objectives. Optimum utilization of resources is closely related with expenditures incurred by an

organization. Thus, it is important to give necessary emphasis on creating a standard and

efficient expenditures cycle in the workplace to minimize the expenditures by reducing wastages

and other loopholes within the organization. A closer look at the purchase system and

expenditures cycle used in Adam & Co. will enable us to comment on the efficiency or lack of it

in the purchase system and expenditures cycle.

Systems:

It is clear from the facts provided in the case study that Adam &co. is a wholesaler of industrial

supplies and it collects its inventories from different parts of the globe. The manufacturers are

from China, Thailand and Vietnam that supply the inventories to the company. Thus, Adam &

Co. imports inventories from these countries hence, the assessment and evaluation of the

purchase systems and expenditures cycles must be carried out keeping in mind the requirements

of the company to import (Uka, 2018).

Evaluation of purchase system:

The very process of purchase is initiated by the purchasing clerk after he check the inventory

subsidiary ledger at the computer terminal. Only after it is found that any particular item in the

inventory is extremely low that the purchasing clerk prepares a digital purchase order. Only two

copies of such order is prepared with one sent to the vendor who is also selected by the

purchasing clerk and the other copy of the order is filed with the inventory department.

ACCOUNTING INFORMATION SYSTEM

Introduction:

An organization generally establishes a standard system within the organization to ensure that

the purchases and other expenditures are incurred efficiently to achieve the organizational

objectives. Optimum utilization of resources is closely related with expenditures incurred by an

organization. Thus, it is important to give necessary emphasis on creating a standard and

efficient expenditures cycle in the workplace to minimize the expenditures by reducing wastages

and other loopholes within the organization. A closer look at the purchase system and

expenditures cycle used in Adam & Co. will enable us to comment on the efficiency or lack of it

in the purchase system and expenditures cycle.

Systems:

It is clear from the facts provided in the case study that Adam &co. is a wholesaler of industrial

supplies and it collects its inventories from different parts of the globe. The manufacturers are

from China, Thailand and Vietnam that supply the inventories to the company. Thus, Adam &

Co. imports inventories from these countries hence, the assessment and evaluation of the

purchase systems and expenditures cycles must be carried out keeping in mind the requirements

of the company to import (Uka, 2018).

Evaluation of purchase system:

The very process of purchase is initiated by the purchasing clerk after he check the inventory

subsidiary ledger at the computer terminal. Only after it is found that any particular item in the

inventory is extremely low that the purchasing clerk prepares a digital purchase order. Only two

copies of such order is prepared with one sent to the vendor who is also selected by the

purchasing clerk and the other copy of the order is filed with the inventory department.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING INFORMATION SYSTEM

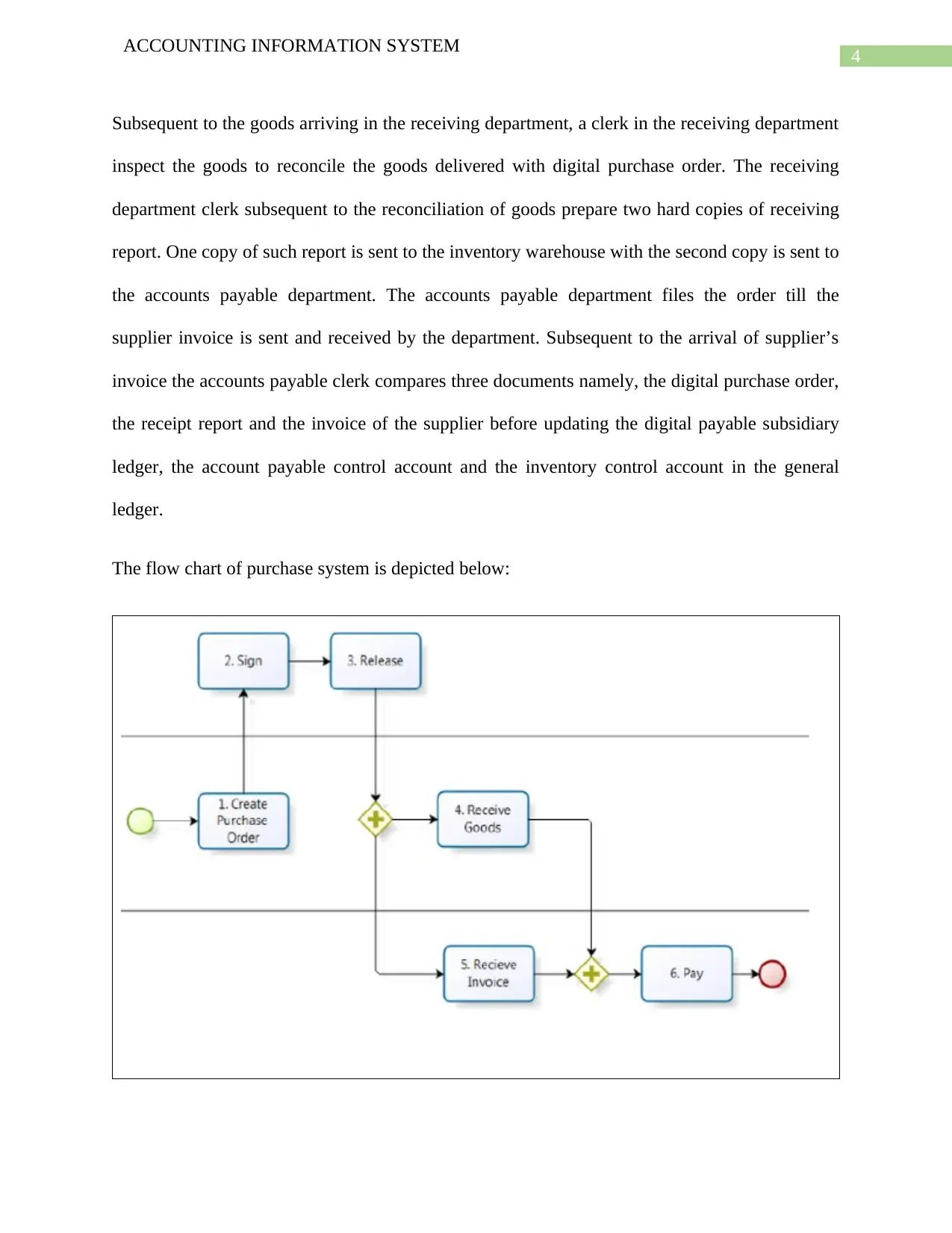

Subsequent to the goods arriving in the receiving department, a clerk in the receiving department

inspect the goods to reconcile the goods delivered with digital purchase order. The receiving

department clerk subsequent to the reconciliation of goods prepare two hard copies of receiving

report. One copy of such report is sent to the inventory warehouse with the second copy is sent to

the accounts payable department. The accounts payable department files the order till the

supplier invoice is sent and received by the department. Subsequent to the arrival of supplier’s

invoice the accounts payable clerk compares three documents namely, the digital purchase order,

the receipt report and the invoice of the supplier before updating the digital payable subsidiary

ledger, the account payable control account and the inventory control account in the general

ledger.

The flow chart of purchase system is depicted below:

ACCOUNTING INFORMATION SYSTEM

Subsequent to the goods arriving in the receiving department, a clerk in the receiving department

inspect the goods to reconcile the goods delivered with digital purchase order. The receiving

department clerk subsequent to the reconciliation of goods prepare two hard copies of receiving

report. One copy of such report is sent to the inventory warehouse with the second copy is sent to

the accounts payable department. The accounts payable department files the order till the

supplier invoice is sent and received by the department. Subsequent to the arrival of supplier’s

invoice the accounts payable clerk compares three documents namely, the digital purchase order,

the receipt report and the invoice of the supplier before updating the digital payable subsidiary

ledger, the account payable control account and the inventory control account in the general

ledger.

The flow chart of purchase system is depicted below:

5

ACCOUNTING INFORMATION SYSTEM

Risks and internal control evaluation of purchasing system:

The above evaluation of the purchasing system shows that there are certain weaknesses in the

system as well as in accounting for purchases. Firstly, the purchasing clerk has the power to

place an order of any item that it too low in the inventory all by himself. Thus, instead of

coordinated efforts from purchasing and inventory clerk the purchase order is placed by the

purchasing clerk on his own. In addition the purchasing clerk is also responsible to choose the

suitable vendor from the file to place the purchasing order. Thus, the risk of placing excessive or

lower quantity of orders by the clerk as there is no coordination and communication between

inventory, sales and purchase departments (pamungkas, 2016).

Further the process of accounting of purchases including posting in accounts payable ledger is

also not completely accurate as the accounts payable clerk is expected to reconcile three different

documents before updating the accounts payable subsidiary ledger. Reconciling the digital

purchase order, receipt report and supplier’s invoice before updating the accounts payable ledger

is asking too much from an accounts payable clerk. As a result the possibility of mistake in

updating the accounts payable subsidiary ledger is quite significant. Lack of controls in the

purchasing system including the accounting system in recording the purchases in the books of

accounts is obvious from the evaluation of the purchasing system.

Evaluation of cash disbursement system:

The cash disbursement clerk files the documents he receives from accounts payable department

till the due date of payment. On the due a check is prepared by the clerk for the due amount

which is sent to the treasury for signing and subsequent disbursement to the vendor. The treasury

after signing the check disburse it to the supplier. After the disbursement of the check the

receiving clerk files all the document.

ACCOUNTING INFORMATION SYSTEM

Risks and internal control evaluation of purchasing system:

The above evaluation of the purchasing system shows that there are certain weaknesses in the

system as well as in accounting for purchases. Firstly, the purchasing clerk has the power to

place an order of any item that it too low in the inventory all by himself. Thus, instead of

coordinated efforts from purchasing and inventory clerk the purchase order is placed by the

purchasing clerk on his own. In addition the purchasing clerk is also responsible to choose the

suitable vendor from the file to place the purchasing order. Thus, the risk of placing excessive or

lower quantity of orders by the clerk as there is no coordination and communication between

inventory, sales and purchase departments (pamungkas, 2016).

Further the process of accounting of purchases including posting in accounts payable ledger is

also not completely accurate as the accounts payable clerk is expected to reconcile three different

documents before updating the accounts payable subsidiary ledger. Reconciling the digital

purchase order, receipt report and supplier’s invoice before updating the accounts payable ledger

is asking too much from an accounts payable clerk. As a result the possibility of mistake in

updating the accounts payable subsidiary ledger is quite significant. Lack of controls in the

purchasing system including the accounting system in recording the purchases in the books of

accounts is obvious from the evaluation of the purchasing system.

Evaluation of cash disbursement system:

The cash disbursement clerk files the documents he receives from accounts payable department

till the due date of payment. On the due a check is prepared by the clerk for the due amount

which is sent to the treasury for signing and subsequent disbursement to the vendor. The treasury

after signing the check disburse it to the supplier. After the disbursement of the check the

receiving clerk files all the document.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING INFORMATION SYSTEM

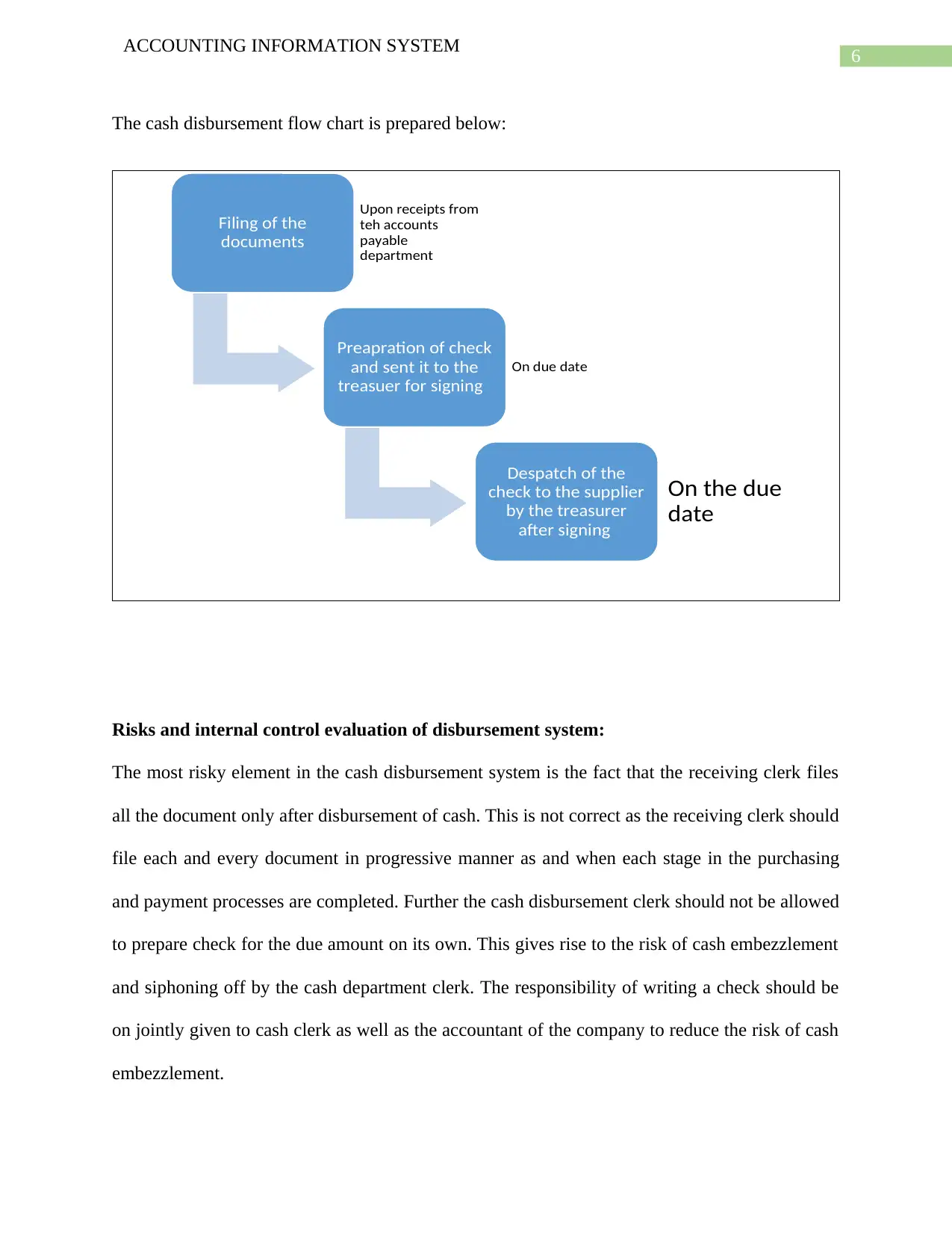

The cash disbursement flow chart is prepared below:

Risks and internal control evaluation of disbursement system:

The most risky element in the cash disbursement system is the fact that the receiving clerk files

all the document only after disbursement of cash. This is not correct as the receiving clerk should

file each and every document in progressive manner as and when each stage in the purchasing

and payment processes are completed. Further the cash disbursement clerk should not be allowed

to prepare check for the due amount on its own. This gives rise to the risk of cash embezzlement

and siphoning off by the cash department clerk. The responsibility of writing a check should be

on jointly given to cash clerk as well as the accountant of the company to reduce the risk of cash

embezzlement.

Filing of the

documents

Upon receipts from

teh accounts

payable

department

Preapration of check

and sent it to the

treasuer for signing

On due date

Despatch of the

check to the supplier

by the treasurer

after signing

On the due

date

ACCOUNTING INFORMATION SYSTEM

The cash disbursement flow chart is prepared below:

Risks and internal control evaluation of disbursement system:

The most risky element in the cash disbursement system is the fact that the receiving clerk files

all the document only after disbursement of cash. This is not correct as the receiving clerk should

file each and every document in progressive manner as and when each stage in the purchasing

and payment processes are completed. Further the cash disbursement clerk should not be allowed

to prepare check for the due amount on its own. This gives rise to the risk of cash embezzlement

and siphoning off by the cash department clerk. The responsibility of writing a check should be

on jointly given to cash clerk as well as the accountant of the company to reduce the risk of cash

embezzlement.

Filing of the

documents

Upon receipts from

teh accounts

payable

department

Preapration of check

and sent it to the

treasuer for signing

On due date

Despatch of the

check to the supplier

by the treasurer

after signing

On the due

date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING INFORMATION SYSTEM

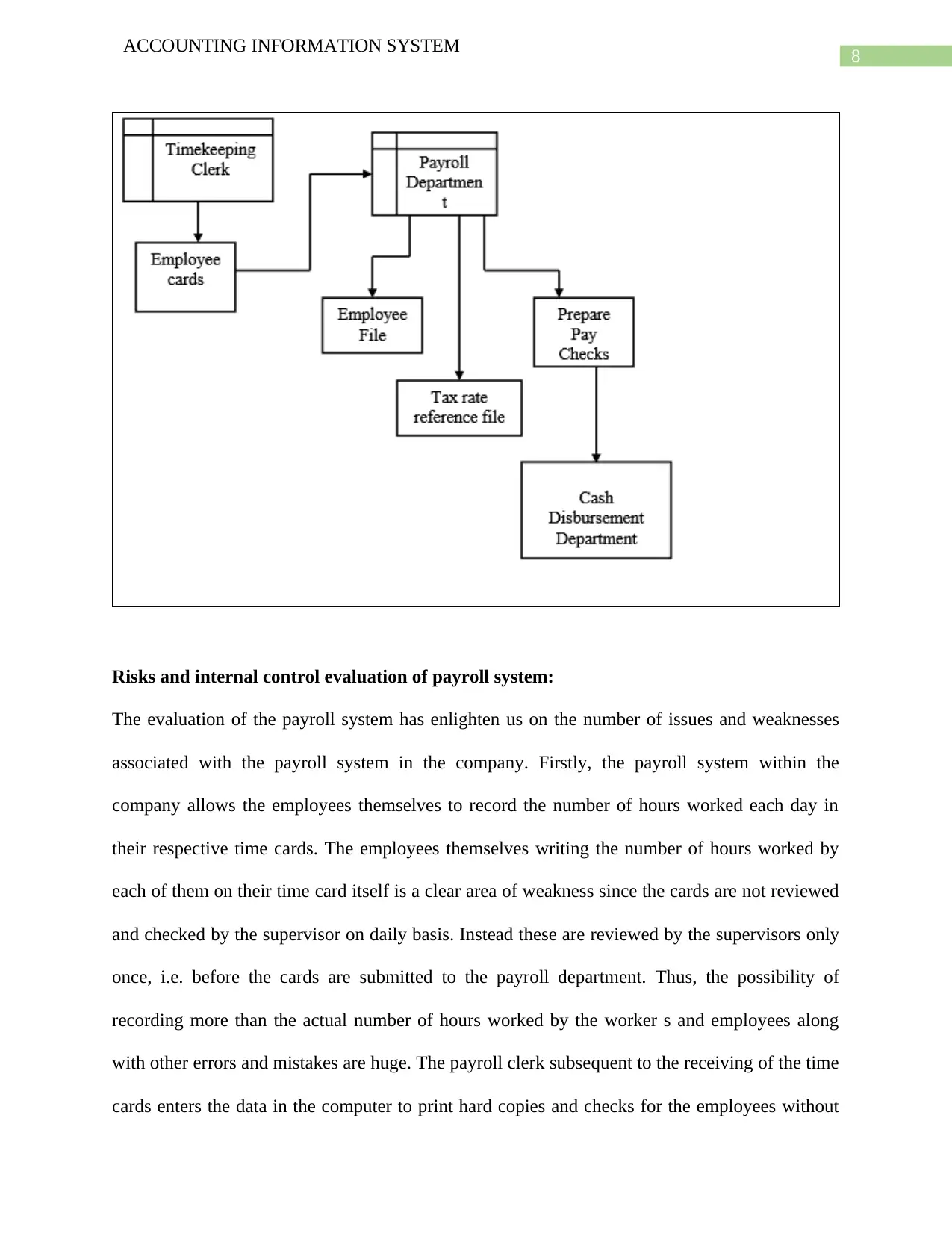

Evaluation of payroll system:

The employees of the company themselves record the number of hours worked on time card each

day. The records are reviewed by the supervisor before submitting the records to the payroll

department. The records are submitted to the payroll department at the end of each week thus,

the supervisor only review the hours recorded by the employees once in a week while these are

submitted to the payroll department. Subsequent to this the payroll clerk inputs the time card data

and takes necessary hardcopies of the register, time card and check copies. The time cards are

filed in the payroll department by the clerk and checks are distributed to the respective

supervisors to be issued to the employees accordingly. The supervisors then distribute the checks

to the respective employees. The accounts payable department receives one copy of the payroll

register subsequent to the disbursement of checks to the employees. The accounts payable clerk

prepares the disbursement vouchers manually after reviewing the payroll register. The payment

is recorded in general ledger subsequent to the writing of entire payroll check to deposit in

imprest accounts at the bank. The general ledger clerk updates the ledger once he receives the

voucher and payroll register (Mamaeva, 2017).

The payroll system is depicted in the flow chart below:

ACCOUNTING INFORMATION SYSTEM

Evaluation of payroll system:

The employees of the company themselves record the number of hours worked on time card each

day. The records are reviewed by the supervisor before submitting the records to the payroll

department. The records are submitted to the payroll department at the end of each week thus,

the supervisor only review the hours recorded by the employees once in a week while these are

submitted to the payroll department. Subsequent to this the payroll clerk inputs the time card data

and takes necessary hardcopies of the register, time card and check copies. The time cards are

filed in the payroll department by the clerk and checks are distributed to the respective

supervisors to be issued to the employees accordingly. The supervisors then distribute the checks

to the respective employees. The accounts payable department receives one copy of the payroll

register subsequent to the disbursement of checks to the employees. The accounts payable clerk

prepares the disbursement vouchers manually after reviewing the payroll register. The payment

is recorded in general ledger subsequent to the writing of entire payroll check to deposit in

imprest accounts at the bank. The general ledger clerk updates the ledger once he receives the

voucher and payroll register (Mamaeva, 2017).

The payroll system is depicted in the flow chart below:

8

ACCOUNTING INFORMATION SYSTEM

Risks and internal control evaluation of payroll system:

The evaluation of the payroll system has enlighten us on the number of issues and weaknesses

associated with the payroll system in the company. Firstly, the payroll system within the

company allows the employees themselves to record the number of hours worked each day in

their respective time cards. The employees themselves writing the number of hours worked by

each of them on their time card itself is a clear area of weakness since the cards are not reviewed

and checked by the supervisor on daily basis. Instead these are reviewed by the supervisors only

once, i.e. before the cards are submitted to the payroll department. Thus, the possibility of

recording more than the actual number of hours worked by the worker s and employees along

with other errors and mistakes are huge. The payroll clerk subsequent to the receiving of the time

cards enters the data in the computer to print hard copies and checks for the employees without

ACCOUNTING INFORMATION SYSTEM

Risks and internal control evaluation of payroll system:

The evaluation of the payroll system has enlighten us on the number of issues and weaknesses

associated with the payroll system in the company. Firstly, the payroll system within the

company allows the employees themselves to record the number of hours worked each day in

their respective time cards. The employees themselves writing the number of hours worked by

each of them on their time card itself is a clear area of weakness since the cards are not reviewed

and checked by the supervisor on daily basis. Instead these are reviewed by the supervisors only

once, i.e. before the cards are submitted to the payroll department. Thus, the possibility of

recording more than the actual number of hours worked by the worker s and employees along

with other errors and mistakes are huge. The payroll clerk subsequent to the receiving of the time

cards enters the data in the computer to print hard copies and checks for the employees without

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING INFORMATION SYSTEM

reviewing the time cards and their authenticity. Thus, the internal controls within the company in

handling the payroll payment is definitely very weak.

The accounts payable clerk gets the payroll register and other documents from the payroll clerk

which is neither reviewed nor verified properly. As accounts payable clerk subsequently send the

payroll register and time cards to the general ledger clerk for recording and the general ledger

does the same without conducting any further verification.

Thus, the entire process of payroll payment and accounting contains number of areas that make

the entire process of payment as well as recording of payroll related expenditures vulnerable to

the risk of error, mistakes and fraud. Thus, necessary steps should be taken by the management

to strengthen the weaker areas within the payroll and other expenditures section to improve the

overall expenditures cycle of the company (Gitman, Forrester and Forrester, 2018).

Conclusion:

Considering the discussion on the payroll cycles and systems including the accounting system to

record these transactions in the books of accounts of the company it is clear that all of the

systems and expenditure cycles mentioned in the document have one or more weaknesses which

have to be dealt with effectively by the management to improve the overall expenditures cycles

and accounting of these expenditures.

Recommendations:

As already mentioned that each and every single system mentioned in the document, i.e.

purchase system, cash disbursement system and payroll system lacks necessary controls and

sophistication require to make these systems water tight in terms of scope of exploiting risk and

threats associated to these systems. In order to deal with the weaknesses in these systems to

ACCOUNTING INFORMATION SYSTEM

reviewing the time cards and their authenticity. Thus, the internal controls within the company in

handling the payroll payment is definitely very weak.

The accounts payable clerk gets the payroll register and other documents from the payroll clerk

which is neither reviewed nor verified properly. As accounts payable clerk subsequently send the

payroll register and time cards to the general ledger clerk for recording and the general ledger

does the same without conducting any further verification.

Thus, the entire process of payroll payment and accounting contains number of areas that make

the entire process of payment as well as recording of payroll related expenditures vulnerable to

the risk of error, mistakes and fraud. Thus, necessary steps should be taken by the management

to strengthen the weaker areas within the payroll and other expenditures section to improve the

overall expenditures cycle of the company (Gitman, Forrester and Forrester, 2018).

Conclusion:

Considering the discussion on the payroll cycles and systems including the accounting system to

record these transactions in the books of accounts of the company it is clear that all of the

systems and expenditure cycles mentioned in the document have one or more weaknesses which

have to be dealt with effectively by the management to improve the overall expenditures cycles

and accounting of these expenditures.

Recommendations:

As already mentioned that each and every single system mentioned in the document, i.e.

purchase system, cash disbursement system and payroll system lacks necessary controls and

sophistication require to make these systems water tight in terms of scope of exploiting risk and

threats associated to these systems. In order to deal with the weaknesses in these systems to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING INFORMATION SYSTEM

strengthen and improve these systems and their effectiveness the following recommendations

should be followed.

Purchase system:

Increase amount of coordination and communication between purchasing department and other

departments:

There must be proper communication and coordination between purchase, sales, inventory and

other departments to ensure that the purchase system is following the standard procedures to

make sure that the purchase orders are correctly placed and these are properly recorded in the

books of accounts. Giving the responsibility on purchasing clerk himself to place purchase

orders as well as selection of suitable vendors is not correct in the purchasing system

(Generational Analysis in Educational Organizations, 2018).

The purchasing clerk should in consultation with inventory department clerk shall place purchase

orders:

The purchasing orders shall be placed by the purchasing clerk in consultation with the inventory

clerk instead of placing such orders all by himself.

More than two copies of purchase orders shall be created:

More than two copies of purchasing orders shall be created to dispatch these copies to the

different departments within the company to improve the process of reconciliation and review of

the orders sent by the suppliers.

Cash disbursement system:

ACCOUNTING INFORMATION SYSTEM

strengthen and improve these systems and their effectiveness the following recommendations

should be followed.

Purchase system:

Increase amount of coordination and communication between purchasing department and other

departments:

There must be proper communication and coordination between purchase, sales, inventory and

other departments to ensure that the purchase system is following the standard procedures to

make sure that the purchase orders are correctly placed and these are properly recorded in the

books of accounts. Giving the responsibility on purchasing clerk himself to place purchase

orders as well as selection of suitable vendors is not correct in the purchasing system

(Generational Analysis in Educational Organizations, 2018).

The purchasing clerk should in consultation with inventory department clerk shall place purchase

orders:

The purchasing orders shall be placed by the purchasing clerk in consultation with the inventory

clerk instead of placing such orders all by himself.

More than two copies of purchase orders shall be created:

More than two copies of purchasing orders shall be created to dispatch these copies to the

different departments within the company to improve the process of reconciliation and review of

the orders sent by the suppliers.

Cash disbursement system:

11

ACCOUNTING INFORMATION SYSTEM

The cash disbursement system shall be improved by taking the following recommendatory steps:

The progressive filing of document should be encouraged:

The receiving clerk should be encouraged to file the documents in a progressive manner, i.e. he

should immediately the documents subsequent to the receipt of the document (Cade and McVay,

2018).

Segregation of duties:

The preparation of check and recording of the payment entries in the books of accounts should

be done by two separate persons in the company. This will reduce the risk of cash embezzlement

and misuse.

Payroll system:

The payroll system is honestly full of weaknesses and it is important for the management to take

necessary steps to improve the payroll system in the future.

The time card should be maintained and written by supervisors:

Number of hours worked by the employees are written in the time cards by the employees

themselves thus, the chances of mistake and errors in recording the number of hours worked in

the time cards is extremely high (Buzzard, 2016).

Regular review of the time cards by the supervisors:

Instead of weekly review by the supervisors it is recommended that they review the time cards

regularly and make necessary changes in the time cards if any mistakes and errors are identified.

ACCOUNTING INFORMATION SYSTEM

The cash disbursement system shall be improved by taking the following recommendatory steps:

The progressive filing of document should be encouraged:

The receiving clerk should be encouraged to file the documents in a progressive manner, i.e. he

should immediately the documents subsequent to the receipt of the document (Cade and McVay,

2018).

Segregation of duties:

The preparation of check and recording of the payment entries in the books of accounts should

be done by two separate persons in the company. This will reduce the risk of cash embezzlement

and misuse.

Payroll system:

The payroll system is honestly full of weaknesses and it is important for the management to take

necessary steps to improve the payroll system in the future.

The time card should be maintained and written by supervisors:

Number of hours worked by the employees are written in the time cards by the employees

themselves thus, the chances of mistake and errors in recording the number of hours worked in

the time cards is extremely high (Buzzard, 2016).

Regular review of the time cards by the supervisors:

Instead of weekly review by the supervisors it is recommended that they review the time cards

regularly and make necessary changes in the time cards if any mistakes and errors are identified.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.