Strategic Information Systems: Management Accounting Analysis

VerifiedAdded on 2021/01/03

|15

|4454

|241

Report

AI Summary

This report delves into the realm of strategic information systems, focusing on management accounting techniques and their applications. It begins with an introduction to management accounting, its essential requirements, and the differences between financial and management accounting. The report then explores various management accounting reporting methods, including cost reports, budgetary reports, and performance reports. A key section of the report focuses on cost calculation and income statement preparation, comparing and contrasting absorption costing and marginal costing methods. Through detailed calculations and interpretations, the report demonstrates how these costing techniques impact profit and loss statements. Furthermore, the report analyzes the advantages and disadvantages of different planning tools related to budgetary control and examines the effectiveness of businesses in solving financial problems through budgetary control. The report concludes with a summary of the key findings and a list of references.

Strategic information systems

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

P1 management accounting and its essential requirements of different types of management

accounting system.......................................................................................................................1

P2 Different methods of management accounting reporting......................................................4

TASK 2............................................................................................................................................5

P3 calculation of costs and preparation of income statements....................................................5

P4 advantages and disadvantages of various planning tools of budgetary control.....................8

Effectiveness of business in solving financial problems through budgetary controlling..........10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

P1 management accounting and its essential requirements of different types of management

accounting system.......................................................................................................................1

P2 Different methods of management accounting reporting......................................................4

TASK 2............................................................................................................................................5

P3 calculation of costs and preparation of income statements....................................................5

P4 advantages and disadvantages of various planning tools of budgetary control.....................8

Effectiveness of business in solving financial problems through budgetary controlling..........10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting system is a branch of management which helps the business in

enhancing capabilities of organisation regarding enhancement of financial position of the

business. It can be defined as application of knowledge and skills of professionals in order to

formulate policies, and strategies in order to perform planning and control activities efficiently

and effectively as well. The present study gives description regarding various methods and

essential requirements of different types of management accounting system. It also shows proper

calculation of cost and preparation of income statement using different techniques. The report

describes advantages and disadvantages of various planning tools of budgetary control used by

Nero ltd. Along with adaption of various management accounting system with a view to respond

to financial problems of business.

Task 1

P1 management accounting and its essential requirements of different types of management

accounting system

Management accounting:

Management accounting is an accounting techniques which provides important

information to management as to develop effective plans and strategies of the business in order

to enhance organization's capacity and financial position (Höglund, 2016).

Management accounting can also be termed as cost accounting, which performs its

activities to analyse the total cost of business in order to prepare financial reports and help the

management in making plans and budgets regarding financial activities of the business.

Management accounting system:

Management accounting system can be defined as method and technique of formulating

planning and controlling system in order to maximize profit and efficiency of the business

through evaluation of business's past performance and comparing it with its present performance.

Management accounting system is a major part of organisation as it influences the

financial position of the business and also helps in enhancing profitability. It helps the

organisation in planning related to cash and investment, budgeting, and provides professional

advice to the business related to financial activities of the business.

Difference between financial and management accounting

1

Management accounting system is a branch of management which helps the business in

enhancing capabilities of organisation regarding enhancement of financial position of the

business. It can be defined as application of knowledge and skills of professionals in order to

formulate policies, and strategies in order to perform planning and control activities efficiently

and effectively as well. The present study gives description regarding various methods and

essential requirements of different types of management accounting system. It also shows proper

calculation of cost and preparation of income statement using different techniques. The report

describes advantages and disadvantages of various planning tools of budgetary control used by

Nero ltd. Along with adaption of various management accounting system with a view to respond

to financial problems of business.

Task 1

P1 management accounting and its essential requirements of different types of management

accounting system

Management accounting:

Management accounting is an accounting techniques which provides important

information to management as to develop effective plans and strategies of the business in order

to enhance organization's capacity and financial position (Höglund, 2016).

Management accounting can also be termed as cost accounting, which performs its

activities to analyse the total cost of business in order to prepare financial reports and help the

management in making plans and budgets regarding financial activities of the business.

Management accounting system:

Management accounting system can be defined as method and technique of formulating

planning and controlling system in order to maximize profit and efficiency of the business

through evaluation of business's past performance and comparing it with its present performance.

Management accounting system is a major part of organisation as it influences the

financial position of the business and also helps in enhancing profitability. It helps the

organisation in planning related to cash and investment, budgeting, and provides professional

advice to the business related to financial activities of the business.

Difference between financial and management accounting

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Basis Financial accounting Management accounting

Meaning Financial accounting refers to a system to

prepare financial statements of business

for external parties of company (Smith,

2017).

Management accounting is a

system to provide information

to the management and help

them in developing more

effective plans for

organisation.

Aim Providing information to external users of

company about financial position of

business like, customers, creditors, etc.

To provide relevant

information to managers to

help them in taking effective

decisions.

Users Both internal and external parties can use

it.

It can be used by management

of business only.

Essential requirements of different management techniques:

Cost accounting system: cost accounting is a system of management through which it

analyses approximate cost of manufacturing goods. It provides specific tools to

management like standard costing, budgetary control, marginal costing etc. which are

applied by managers as to have better control over the cost of business.

Benefits:

▪ It helps managers in inventory management, analysis of profitability of business,

identifying cost efficiency of organisation, etc.

▪ Through cost accounting techniques, managers enable to predict organisation's

total production cost as to enhance the efficiency of the business and increase its

profitability.

▪ Cost accounting predicts cost of organisation which is being compared by the

management with the actual cost of to determine the performance and efficiency

of the business.

2

Meaning Financial accounting refers to a system to

prepare financial statements of business

for external parties of company (Smith,

2017).

Management accounting is a

system to provide information

to the management and help

them in developing more

effective plans for

organisation.

Aim Providing information to external users of

company about financial position of

business like, customers, creditors, etc.

To provide relevant

information to managers to

help them in taking effective

decisions.

Users Both internal and external parties can use

it.

It can be used by management

of business only.

Essential requirements of different management techniques:

Cost accounting system: cost accounting is a system of management through which it

analyses approximate cost of manufacturing goods. It provides specific tools to

management like standard costing, budgetary control, marginal costing etc. which are

applied by managers as to have better control over the cost of business.

Benefits:

▪ It helps managers in inventory management, analysis of profitability of business,

identifying cost efficiency of organisation, etc.

▪ Through cost accounting techniques, managers enable to predict organisation's

total production cost as to enhance the efficiency of the business and increase its

profitability.

▪ Cost accounting predicts cost of organisation which is being compared by the

management with the actual cost of to determine the performance and efficiency

of the business.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

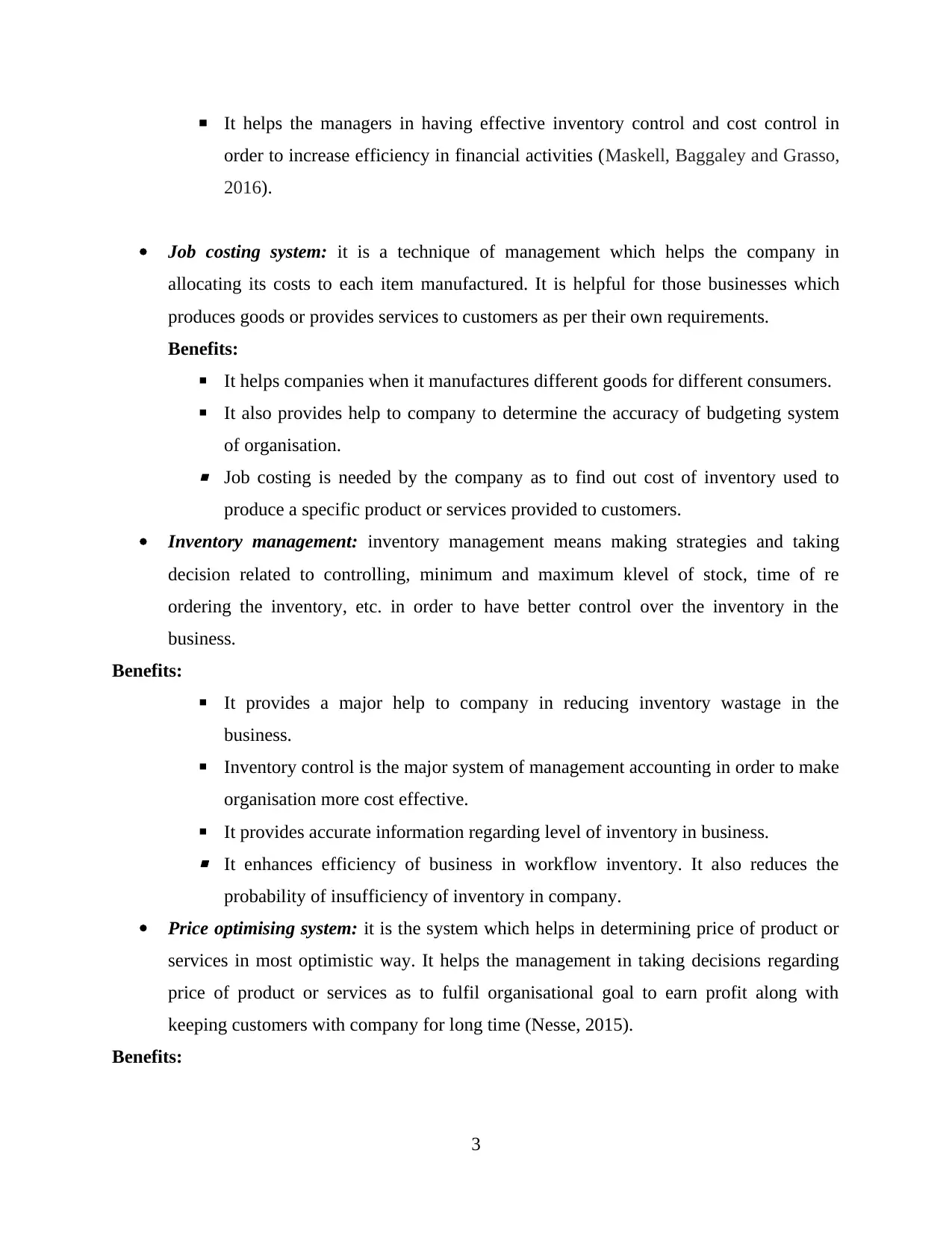

▪ It helps the managers in having effective inventory control and cost control in

order to increase efficiency in financial activities (Maskell, Baggaley and Grasso,

2016).

Job costing system: it is a technique of management which helps the company in

allocating its costs to each item manufactured. It is helpful for those businesses which

produces goods or provides services to customers as per their own requirements.

Benefits:

▪ It helps companies when it manufactures different goods for different consumers.

▪ It also provides help to company to determine the accuracy of budgeting system

of organisation.

▪ Job costing is needed by the company as to find out cost of inventory used to

produce a specific product or services provided to customers.

Inventory management: inventory management means making strategies and taking

decision related to controlling, minimum and maximum klevel of stock, time of re

ordering the inventory, etc. in order to have better control over the inventory in the

business.

Benefits:

▪ It provides a major help to company in reducing inventory wastage in the

business.

▪ Inventory control is the major system of management accounting in order to make

organisation more cost effective.

▪ It provides accurate information regarding level of inventory in business.

▪ It enhances efficiency of business in workflow inventory. It also reduces the

probability of insufficiency of inventory in company.

Price optimising system: it is the system which helps in determining price of product or

services in most optimistic way. It helps the management in taking decisions regarding

price of product or services as to fulfil organisational goal to earn profit along with

keeping customers with company for long time (Nesse, 2015).

Benefits:

3

order to increase efficiency in financial activities (Maskell, Baggaley and Grasso,

2016).

Job costing system: it is a technique of management which helps the company in

allocating its costs to each item manufactured. It is helpful for those businesses which

produces goods or provides services to customers as per their own requirements.

Benefits:

▪ It helps companies when it manufactures different goods for different consumers.

▪ It also provides help to company to determine the accuracy of budgeting system

of organisation.

▪ Job costing is needed by the company as to find out cost of inventory used to

produce a specific product or services provided to customers.

Inventory management: inventory management means making strategies and taking

decision related to controlling, minimum and maximum klevel of stock, time of re

ordering the inventory, etc. in order to have better control over the inventory in the

business.

Benefits:

▪ It provides a major help to company in reducing inventory wastage in the

business.

▪ Inventory control is the major system of management accounting in order to make

organisation more cost effective.

▪ It provides accurate information regarding level of inventory in business.

▪ It enhances efficiency of business in workflow inventory. It also reduces the

probability of insufficiency of inventory in company.

Price optimising system: it is the system which helps in determining price of product or

services in most optimistic way. It helps the management in taking decisions regarding

price of product or services as to fulfil organisational goal to earn profit along with

keeping customers with company for long time (Nesse, 2015).

Benefits:

3

▪ It provides the best way to achieve organisational goal of earning profit by

deciding the best price of the product.

▪ It also provides alternatives through which company can enhance price of product

along with making the business operations more cost effective with a view to

enhance its profitability and market share in the competitive market.

P2 Different methods of management accounting reporting

Management of financial accounting provides relevant information to managers to

provide them help in effective decisions making as to enhance the financial position of business

and increase their profitability. Information provided by financial accounting managers need to

be reliable as non reliable information may result in increasing probability of gaining failure by

the business.

Management accounting system provides information to the internal management of the

business on the basis of which managers develop their strategies and financial planning with a

view to enhance the capability of the business organisation. In case, it provides wrong

information to manager, it will result in reducing efficiency of business and reduction of

profitability and financial position as well.

The report to be provided to management need to be undersrandable by them so that they

can properly use the reports and take appropriate decsions for the business organisation. In this

order an understandable report can contribute in enhancing the efficiency and profitability along

with its financial growth.

Methods of management accounting reporting:

Cost reports: managers of company calculates cost of goods manufactured or service

rendered to customers. The report is prepared with help of assembling various costs like

material, labour, overheads, etc. all costs of product or services are included in this report

for calculating total cost of product or services in order to determine their selling price.

Budgetary reports: this report shows estimated cost of production of business. It helps

managers in deciding various financial activities and determining requirement of finance

in the business. It also provides sources of revenues and expenses to the managers in

order to achieve its organisational goals.

4

deciding the best price of the product.

▪ It also provides alternatives through which company can enhance price of product

along with making the business operations more cost effective with a view to

enhance its profitability and market share in the competitive market.

P2 Different methods of management accounting reporting

Management of financial accounting provides relevant information to managers to

provide them help in effective decisions making as to enhance the financial position of business

and increase their profitability. Information provided by financial accounting managers need to

be reliable as non reliable information may result in increasing probability of gaining failure by

the business.

Management accounting system provides information to the internal management of the

business on the basis of which managers develop their strategies and financial planning with a

view to enhance the capability of the business organisation. In case, it provides wrong

information to manager, it will result in reducing efficiency of business and reduction of

profitability and financial position as well.

The report to be provided to management need to be undersrandable by them so that they

can properly use the reports and take appropriate decsions for the business organisation. In this

order an understandable report can contribute in enhancing the efficiency and profitability along

with its financial growth.

Methods of management accounting reporting:

Cost reports: managers of company calculates cost of goods manufactured or service

rendered to customers. The report is prepared with help of assembling various costs like

material, labour, overheads, etc. all costs of product or services are included in this report

for calculating total cost of product or services in order to determine their selling price.

Budgetary reports: this report shows estimated cost of production of business. It helps

managers in deciding various financial activities and determining requirement of finance

in the business. It also provides sources of revenues and expenses to the managers in

order to achieve its organisational goals.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Performance report: it is being prepared by comparing actual cost and actual revenue

earned with budgeted cost and revenue in order to identify the efficiency of business. It

helps the managers in taking better control over the efficiency of business.

TASK 2

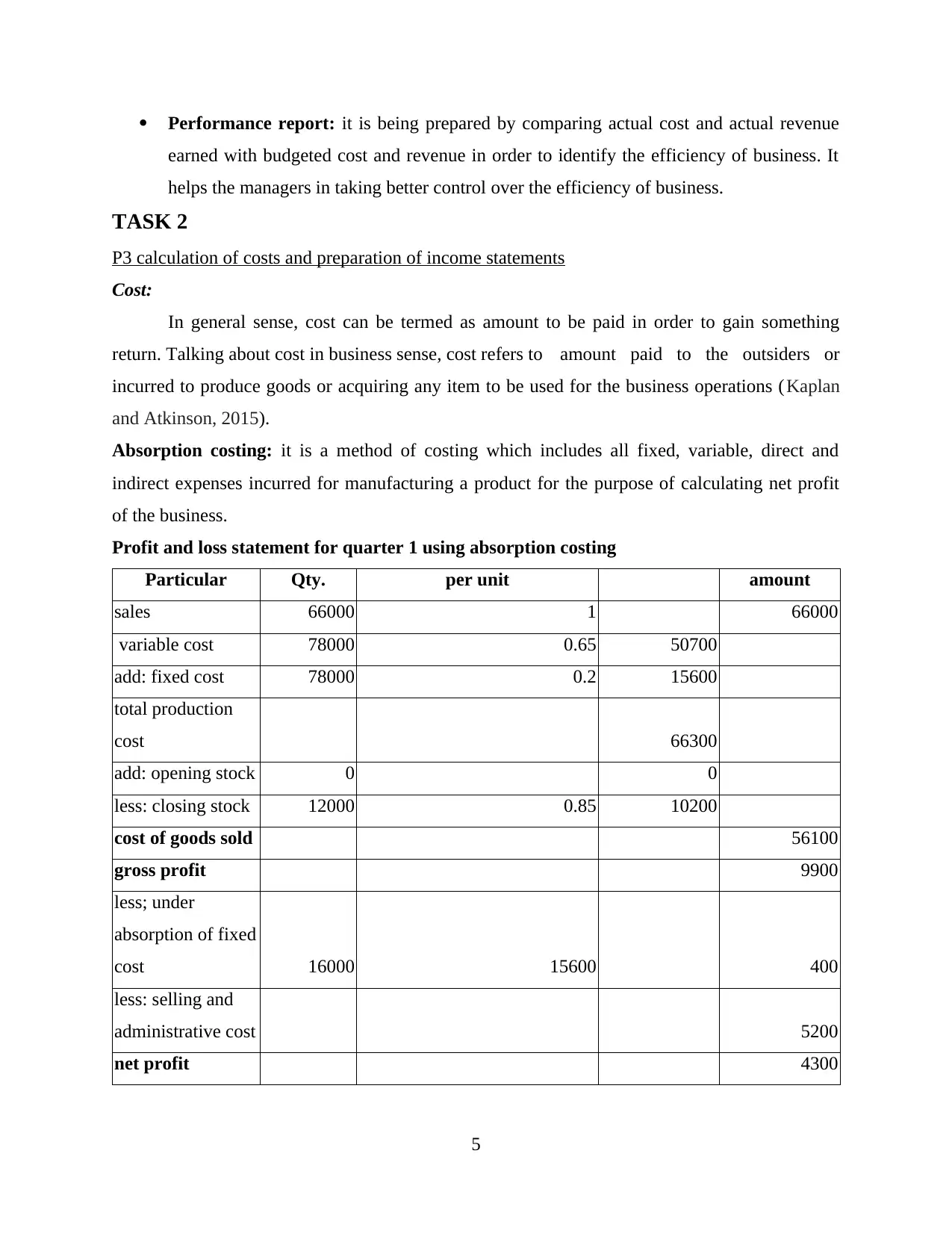

P3 calculation of costs and preparation of income statements

Cost:

In general sense, cost can be termed as amount to be paid in order to gain something

return. Talking about cost in business sense, cost refers to amount paid to the outsiders or

incurred to produce goods or acquiring any item to be used for the business operations (Kaplan

and Atkinson, 2015).

Absorption costing: it is a method of costing which includes all fixed, variable, direct and

indirect expenses incurred for manufacturing a product for the purpose of calculating net profit

of the business.

Profit and loss statement for quarter 1 using absorption costing

Particular Qty. per unit amount

sales 66000 1 66000

variable cost 78000 0.65 50700

add: fixed cost 78000 0.2 15600

total production

cost 66300

add: opening stock 0 0

less: closing stock 12000 0.85 10200

cost of goods sold 56100

gross profit 9900

less; under

absorption of fixed

cost 16000 15600 400

less: selling and

administrative cost 5200

net profit 4300

5

earned with budgeted cost and revenue in order to identify the efficiency of business. It

helps the managers in taking better control over the efficiency of business.

TASK 2

P3 calculation of costs and preparation of income statements

Cost:

In general sense, cost can be termed as amount to be paid in order to gain something

return. Talking about cost in business sense, cost refers to amount paid to the outsiders or

incurred to produce goods or acquiring any item to be used for the business operations (Kaplan

and Atkinson, 2015).

Absorption costing: it is a method of costing which includes all fixed, variable, direct and

indirect expenses incurred for manufacturing a product for the purpose of calculating net profit

of the business.

Profit and loss statement for quarter 1 using absorption costing

Particular Qty. per unit amount

sales 66000 1 66000

variable cost 78000 0.65 50700

add: fixed cost 78000 0.2 15600

total production

cost 66300

add: opening stock 0 0

less: closing stock 12000 0.85 10200

cost of goods sold 56100

gross profit 9900

less; under

absorption of fixed

cost 16000 15600 400

less: selling and

administrative cost 5200

net profit 4300

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

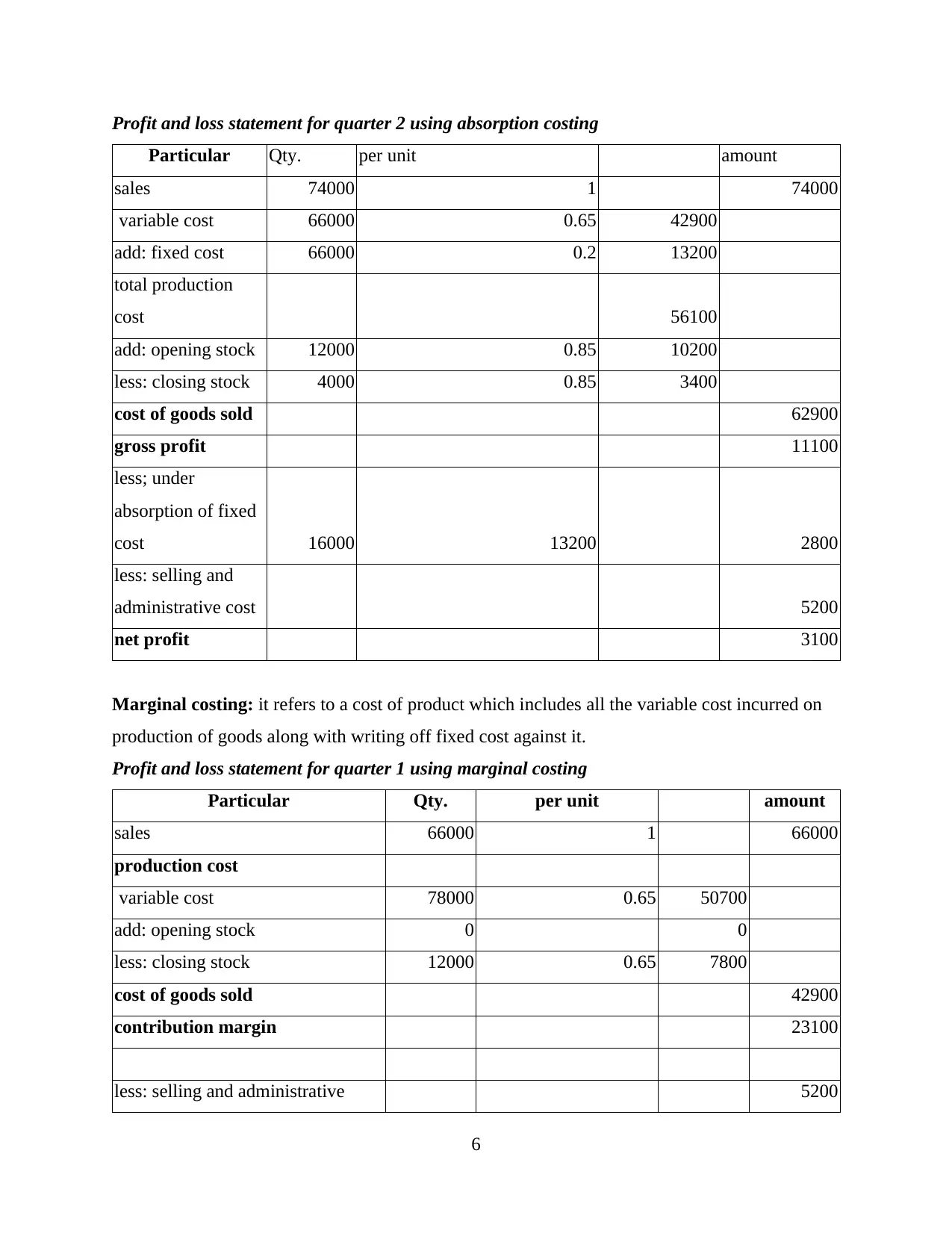

Profit and loss statement for quarter 2 using absorption costing

Particular Qty. per unit amount

sales 74000 1 74000

variable cost 66000 0.65 42900

add: fixed cost 66000 0.2 13200

total production

cost 56100

add: opening stock 12000 0.85 10200

less: closing stock 4000 0.85 3400

cost of goods sold 62900

gross profit 11100

less; under

absorption of fixed

cost 16000 13200 2800

less: selling and

administrative cost 5200

net profit 3100

Marginal costing: it refers to a cost of product which includes all the variable cost incurred on

production of goods along with writing off fixed cost against it.

Profit and loss statement for quarter 1 using marginal costing

Particular Qty. per unit amount

sales 66000 1 66000

production cost

variable cost 78000 0.65 50700

add: opening stock 0 0

less: closing stock 12000 0.65 7800

cost of goods sold 42900

contribution margin 23100

less: selling and administrative 5200

6

Particular Qty. per unit amount

sales 74000 1 74000

variable cost 66000 0.65 42900

add: fixed cost 66000 0.2 13200

total production

cost 56100

add: opening stock 12000 0.85 10200

less: closing stock 4000 0.85 3400

cost of goods sold 62900

gross profit 11100

less; under

absorption of fixed

cost 16000 13200 2800

less: selling and

administrative cost 5200

net profit 3100

Marginal costing: it refers to a cost of product which includes all the variable cost incurred on

production of goods along with writing off fixed cost against it.

Profit and loss statement for quarter 1 using marginal costing

Particular Qty. per unit amount

sales 66000 1 66000

production cost

variable cost 78000 0.65 50700

add: opening stock 0 0

less: closing stock 12000 0.65 7800

cost of goods sold 42900

contribution margin 23100

less: selling and administrative 5200

6

overheads

less: fixed manufacturing expenses 16000

net profit 1900

Profit and loss statement for quarter 2 using marginal costing

Particular Qty. per unit amount

sales 74000 1 74000

production cost

variable cost 66000 0.65 42900

add: opening stock 12000 0.65 7800

less: closing stock 4000 0.65 2600

cost of goods sold 48100

contribution margin 25900

less: selling and

administrative

overheads 5200

less: fixed

manufacturing

expenses 16000

net profit 4700

Interpretation:

Both techniques are useful for the business in order to calculate cost of production. From

the above calculation it can be interpret that net profit calculated from absorption costing comes

less than marginal costing. It happens because while calculating net profit from marginal costing,

under or over absorption costs are not included.

Cost volume profit:

Cost volume profit is a method used in cost accounting which determines the variation of

cost at different level of business operations. Its helps the business in determining break even

point in order to determine different sales volume and decide price of product or services

7

less: fixed manufacturing expenses 16000

net profit 1900

Profit and loss statement for quarter 2 using marginal costing

Particular Qty. per unit amount

sales 74000 1 74000

production cost

variable cost 66000 0.65 42900

add: opening stock 12000 0.65 7800

less: closing stock 4000 0.65 2600

cost of goods sold 48100

contribution margin 25900

less: selling and

administrative

overheads 5200

less: fixed

manufacturing

expenses 16000

net profit 4700

Interpretation:

Both techniques are useful for the business in order to calculate cost of production. From

the above calculation it can be interpret that net profit calculated from absorption costing comes

less than marginal costing. It happens because while calculating net profit from marginal costing,

under or over absorption costs are not included.

Cost volume profit:

Cost volume profit is a method used in cost accounting which determines the variation of

cost at different level of business operations. Its helps the business in determining break even

point in order to determine different sales volume and decide price of product or services

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

provided by the company to its customers. In this order, management can develop the best

strategies for the business with the view to achieve organisations' profitability goals.

Flexible budgeting:

Flexible budget provides information regarding cost that need to be incurred by the

business at different level. It also provides data relates to the budgeted output that can be gained

at a certain level. It is a budget which considers possible outputs along wuth cash to be incurred

at different level of production (Ortea and Gallardo, 2015). With the help of flexible budget,

managers can identify the optimistic level of production at which company can gain maximum

level of profit with minimum cost incurred. In this order management can make the company

more cost effective.

Cost variance:

Variance refers to difference between actual and budget. Therefore, cost variance refers

to difference between estimated cost and actual cost incurred by the business in producing goods

or rendering services. It is a part of standard costing which is a method of cost accounting. It

enables the management in determining the actual performance of the business. In case, cost

incurred by the company comes less than budgeted cost, it shows favourable result to

management and if actual incurred cost is more than budgeted one, it provides negative result to

management.

Cost allocation:

Cost allocation refers to a process of costing which helps management in identifying and

assigning cost at different level of management. It is used in preparing financial reports of the

company in order to allocate cost among different departments of business to determine actual

cost incur reed by the department. In this order mangers can detemine efficiency of each

department of the business and take appropriate decision for each determine as to enhance their

capacity along with increasing probability of the business as a whole (Ossimitz, Wieder and

Chapman, 2016).

Standard costing:

Standard costing helps the management in determining the actual performance of the

business operations. As it provides various formulae to compare actual cost incured with the

budgeted cost of operations.

Role of costing in setting price:

8

strategies for the business with the view to achieve organisations' profitability goals.

Flexible budgeting:

Flexible budget provides information regarding cost that need to be incurred by the

business at different level. It also provides data relates to the budgeted output that can be gained

at a certain level. It is a budget which considers possible outputs along wuth cash to be incurred

at different level of production (Ortea and Gallardo, 2015). With the help of flexible budget,

managers can identify the optimistic level of production at which company can gain maximum

level of profit with minimum cost incurred. In this order management can make the company

more cost effective.

Cost variance:

Variance refers to difference between actual and budget. Therefore, cost variance refers

to difference between estimated cost and actual cost incurred by the business in producing goods

or rendering services. It is a part of standard costing which is a method of cost accounting. It

enables the management in determining the actual performance of the business. In case, cost

incurred by the company comes less than budgeted cost, it shows favourable result to

management and if actual incurred cost is more than budgeted one, it provides negative result to

management.

Cost allocation:

Cost allocation refers to a process of costing which helps management in identifying and

assigning cost at different level of management. It is used in preparing financial reports of the

company in order to allocate cost among different departments of business to determine actual

cost incur reed by the department. In this order mangers can detemine efficiency of each

department of the business and take appropriate decision for each determine as to enhance their

capacity along with increasing probability of the business as a whole (Ossimitz, Wieder and

Chapman, 2016).

Standard costing:

Standard costing helps the management in determining the actual performance of the

business operations. As it provides various formulae to compare actual cost incured with the

budgeted cost of operations.

Role of costing in setting price:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Costing is a system of business which helps the organisation in determining cost incurred

to produce goods or render services to customers. It also provides some techniques through

which company can predict its future cost taking into consideration the levbel of efficiency of the

business.

Costing also provides help to management to set the price of goods or services as under:

Costing provides different techniques to allocate the total cost incurred by business in

each department as per their operations. Through which it can allocate4 the cost incure on

each product.

Costing helps the managers in determining organisations' break even point. Through

which company can add appropriate profit in order to gain profit as per organisation's

goal and set the optimistic price of product.

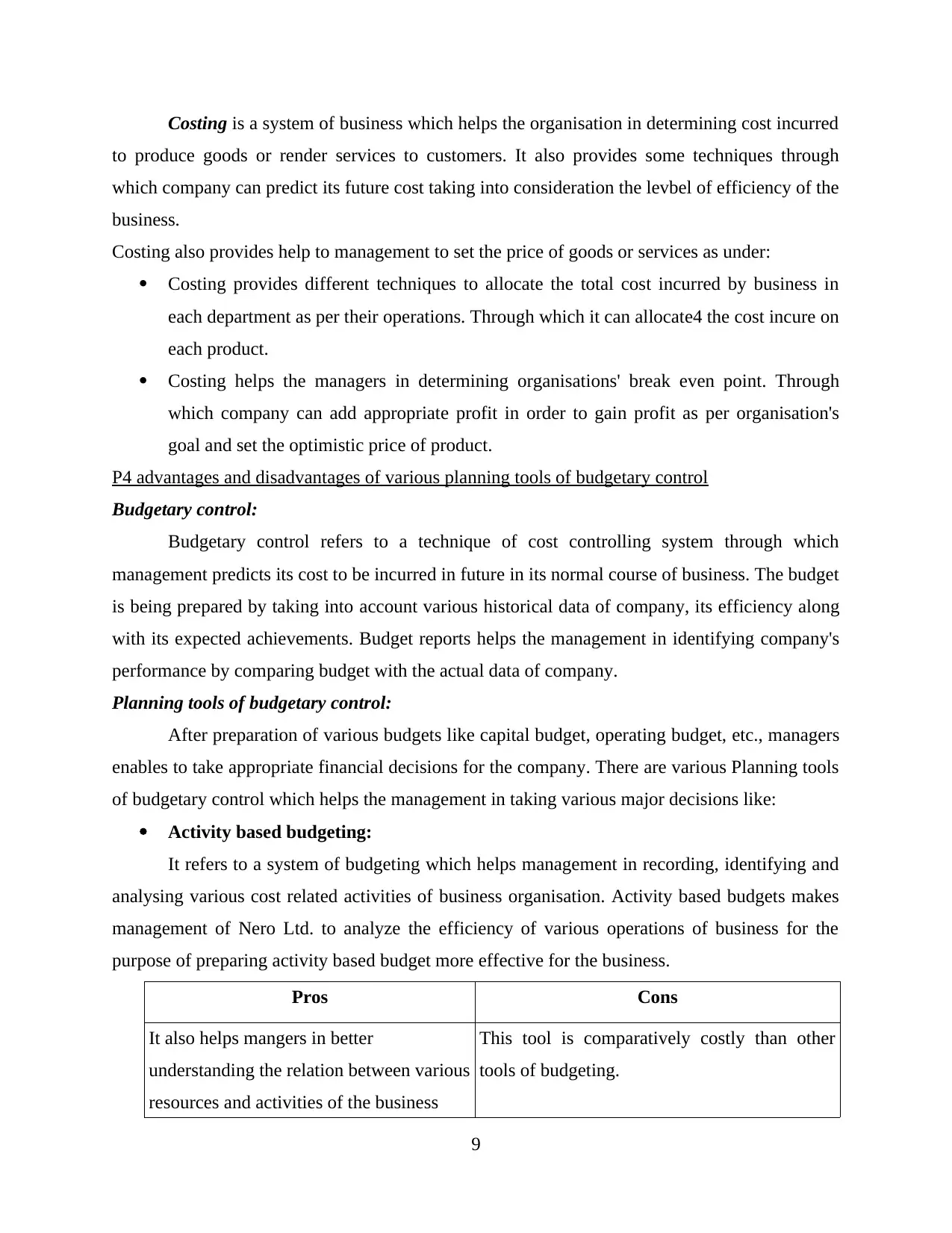

P4 advantages and disadvantages of various planning tools of budgetary control

Budgetary control:

Budgetary control refers to a technique of cost controlling system through which

management predicts its cost to be incurred in future in its normal course of business. The budget

is being prepared by taking into account various historical data of company, its efficiency along

with its expected achievements. Budget reports helps the management in identifying company's

performance by comparing budget with the actual data of company.

Planning tools of budgetary control:

After preparation of various budgets like capital budget, operating budget, etc., managers

enables to take appropriate financial decisions for the company. There are various Planning tools

of budgetary control which helps the management in taking various major decisions like:

Activity based budgeting:

It refers to a system of budgeting which helps management in recording, identifying and

analysing various cost related activities of business organisation. Activity based budgets makes

management of Nero Ltd. to analyze the efficiency of various operations of business for the

purpose of preparing activity based budget more effective for the business.

Pros Cons

It also helps mangers in better

understanding the relation between various

resources and activities of the business

This tool is comparatively costly than other

tools of budgeting.

9

to produce goods or render services to customers. It also provides some techniques through

which company can predict its future cost taking into consideration the levbel of efficiency of the

business.

Costing also provides help to management to set the price of goods or services as under:

Costing provides different techniques to allocate the total cost incurred by business in

each department as per their operations. Through which it can allocate4 the cost incure on

each product.

Costing helps the managers in determining organisations' break even point. Through

which company can add appropriate profit in order to gain profit as per organisation's

goal and set the optimistic price of product.

P4 advantages and disadvantages of various planning tools of budgetary control

Budgetary control:

Budgetary control refers to a technique of cost controlling system through which

management predicts its cost to be incurred in future in its normal course of business. The budget

is being prepared by taking into account various historical data of company, its efficiency along

with its expected achievements. Budget reports helps the management in identifying company's

performance by comparing budget with the actual data of company.

Planning tools of budgetary control:

After preparation of various budgets like capital budget, operating budget, etc., managers

enables to take appropriate financial decisions for the company. There are various Planning tools

of budgetary control which helps the management in taking various major decisions like:

Activity based budgeting:

It refers to a system of budgeting which helps management in recording, identifying and

analysing various cost related activities of business organisation. Activity based budgets makes

management of Nero Ltd. to analyze the efficiency of various operations of business for the

purpose of preparing activity based budget more effective for the business.

Pros Cons

It also helps mangers in better

understanding the relation between various

resources and activities of the business

This tool is comparatively costly than other

tools of budgeting.

9

operations.

This tool helps mangers in effectively

move in context of [planning, taking

decisions, measurement of performance,

evaluation of organisation's performance,

etc.

Activity based budgeting requires more

resources as to having additional assumptions

which can provide more opportunities for

inaccuracies in budgeting.

Cash budget:

Cash budget is an estimation of company's future position regarding cash. Nero Ltd. Can

prepare cash budget by predicting various future sources of cash generation, sources of cash

outflows along with their purposes for a specific period of time. As the flow of cash is quite

uncertain, Manager's of Nero ltd. Can Prepare monthly cash budget for the company in order to

reduce uncertainty in the forecasting organization's position (What is a Cash Budget?, 2019.).

Following are the pros and cons of cash budget:

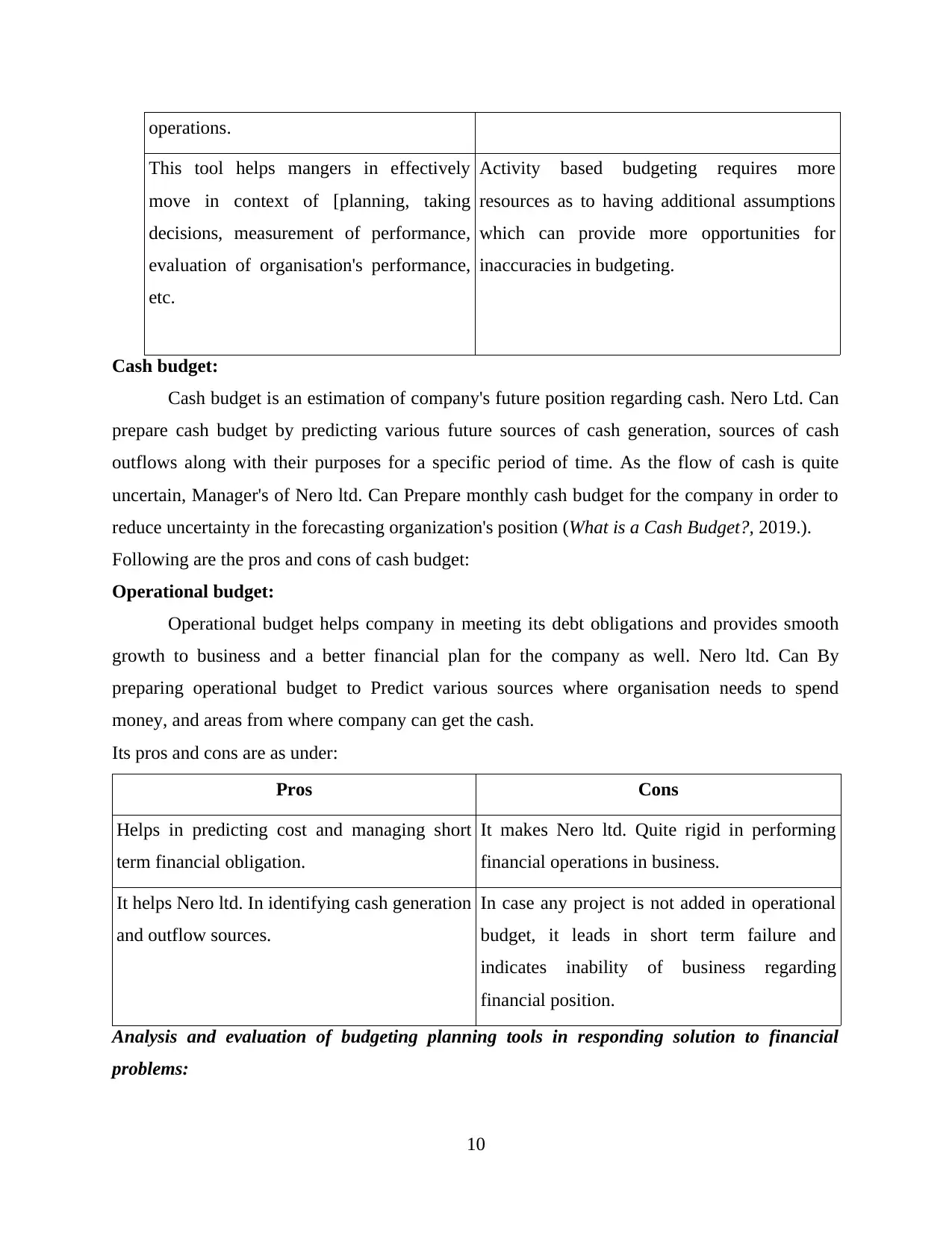

Operational budget:

Operational budget helps company in meeting its debt obligations and provides smooth

growth to business and a better financial plan for the company as well. Nero ltd. Can By

preparing operational budget to Predict various sources where organisation needs to spend

money, and areas from where company can get the cash.

Its pros and cons are as under:

Pros Cons

Helps in predicting cost and managing short

term financial obligation.

It makes Nero ltd. Quite rigid in performing

financial operations in business.

It helps Nero ltd. In identifying cash generation

and outflow sources.

In case any project is not added in operational

budget, it leads in short term failure and

indicates inability of business regarding

financial position.

Analysis and evaluation of budgeting planning tools in responding solution to financial

problems:

10

This tool helps mangers in effectively

move in context of [planning, taking

decisions, measurement of performance,

evaluation of organisation's performance,

etc.

Activity based budgeting requires more

resources as to having additional assumptions

which can provide more opportunities for

inaccuracies in budgeting.

Cash budget:

Cash budget is an estimation of company's future position regarding cash. Nero Ltd. Can

prepare cash budget by predicting various future sources of cash generation, sources of cash

outflows along with their purposes for a specific period of time. As the flow of cash is quite

uncertain, Manager's of Nero ltd. Can Prepare monthly cash budget for the company in order to

reduce uncertainty in the forecasting organization's position (What is a Cash Budget?, 2019.).

Following are the pros and cons of cash budget:

Operational budget:

Operational budget helps company in meeting its debt obligations and provides smooth

growth to business and a better financial plan for the company as well. Nero ltd. Can By

preparing operational budget to Predict various sources where organisation needs to spend

money, and areas from where company can get the cash.

Its pros and cons are as under:

Pros Cons

Helps in predicting cost and managing short

term financial obligation.

It makes Nero ltd. Quite rigid in performing

financial operations in business.

It helps Nero ltd. In identifying cash generation

and outflow sources.

In case any project is not added in operational

budget, it leads in short term failure and

indicates inability of business regarding

financial position.

Analysis and evaluation of budgeting planning tools in responding solution to financial

problems:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.