Accounting Information Systems Case Study: Adam & Co Analysis (HA2042)

VerifiedAdded on 2023/01/03

|15

|3194

|69

Case Study

AI Summary

This case study examines the accounting information systems (AIS) of Adam & Co, a wholesaler, focusing on its purchasing, cash disbursement, and payroll systems. The study begins with an executive summary outlining the company's operations and the structure of its AIS, including networked terminals. It then delves into the system flowcharts of the purchasing, cash disbursement, and payroll systems. Furthermore, the analysis identifies and describes weaknesses in the internal controls of each system, evaluating the associated risks, such as understatement or overstatement of needs, improper controls, and security issues. The assignment provides a detailed overview of the systems, their functions, and the potential vulnerabilities within Adam & Co's financial processes, concluding with a summary of the key findings and recommendations.

Running head: ACCOUNTING INFORMATION SYSTEMS

Accounting Information Systems

(Adam & Co)

Name of the student:

Name of the university:

Author Note

Accounting Information Systems

(Adam & Co)

Name of the student:

Name of the university:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING INFORMATION SYSTEMS

Executive summary

Adam & Co is a wholesaler of the industrial suppliers based in Perth. The business has been

sourcing their inventories from various manufacturers in Vietnam Thailand and China. They have

the centralized accounting systems having the networked terminals located at varies locations. On

the other hand, the accounting information system is the framework used by organizations for

making collections, storages, controlling, processing, retrieving and then report the economic

information. In this study, the system flowchart to purchase systems of cash disbursement and

payroll systems of the business are analyzed. Apart from this, the internal control’s weaknesses for

the systems are the challenges related to this are evaluated in the study.

Executive summary

Adam & Co is a wholesaler of the industrial suppliers based in Perth. The business has been

sourcing their inventories from various manufacturers in Vietnam Thailand and China. They have

the centralized accounting systems having the networked terminals located at varies locations. On

the other hand, the accounting information system is the framework used by organizations for

making collections, storages, controlling, processing, retrieving and then report the economic

information. In this study, the system flowchart to purchase systems of cash disbursement and

payroll systems of the business are analyzed. Apart from this, the internal control’s weaknesses for

the systems are the challenges related to this are evaluated in the study.

2ACCOUNTING INFORMATION SYSTEMS

Table of Contents

Introduction:..........................................................................................................................................3

The situation of the accounting information system regarding operating practices and organizational

structure:................................................................................................................................................3

Various kinds of accounting information systems:...............................................................................5

Purchasing system:............................................................................................................................5

Cash disbursements systems:.............................................................................................................6

Payroll system:...................................................................................................................................9

Describing the weakness of internal control in every system and the risks related to the weaknesses

identified:.............................................................................................................................................11

Conclusion:..........................................................................................................................................12

References:..........................................................................................................................................13

Table of Contents

Introduction:..........................................................................................................................................3

The situation of the accounting information system regarding operating practices and organizational

structure:................................................................................................................................................3

Various kinds of accounting information systems:...............................................................................5

Purchasing system:............................................................................................................................5

Cash disbursements systems:.............................................................................................................6

Payroll system:...................................................................................................................................9

Describing the weakness of internal control in every system and the risks related to the weaknesses

identified:.............................................................................................................................................11

Conclusion:..........................................................................................................................................12

References:..........................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING INFORMATION SYSTEMS

Introduction:

The AIS or Accounting Information System is the structure that business utilizes for

collecting, storing, managing, processing, retrieving and reporting its financial information. Hence, it

can be utilized by the accountants, business, consultants, managers, auditors, tax agencies and chief

financial officers CFOs. The following study demonstrates, the system flowchart of purchasing, cash

disbursement systems and payroll systems of Adam & Co. Further, the weakness of internal control

in every systems and risk related to the identified weakness is analyzed here.

The situation of the accounting information system regarding operating practices

and organizational structure:

The AIS or Accounting Information System assimilates the practice and study of accounting.

This is done with the monitoring, implementation and designing of any information system. This

type of system includes the application of the resources of current information technology towards

conventional accounting controls. This also involves the processes of providing the users with the

financial information needed for managing the business. Further, the system is the component of the

system of the entity’s management information. The current technological abilities allow a range of

probable designs for the AIS (Schaltegger and Burritt 2017). However, the primary structure of the

system has been continuing to involve the three elements of input, output and processing. Next, the

input devices are commonly related to the AIS and involve the personal machines or the

workstations that run applications. It scans the different devices related to the overall standardized

data entry along with electronic communication devices. This is regarding EDI or Electronic Data

Interchange along with the innovation of e-commerce or electronic commerce (Libby 2017).

Moreover, the basic process is gained through the systems that range from individual PC to the huge

Introduction:

The AIS or Accounting Information System is the structure that business utilizes for

collecting, storing, managing, processing, retrieving and reporting its financial information. Hence, it

can be utilized by the accountants, business, consultants, managers, auditors, tax agencies and chief

financial officers CFOs. The following study demonstrates, the system flowchart of purchasing, cash

disbursement systems and payroll systems of Adam & Co. Further, the weakness of internal control

in every systems and risk related to the identified weakness is analyzed here.

The situation of the accounting information system regarding operating practices

and organizational structure:

The AIS or Accounting Information System assimilates the practice and study of accounting.

This is done with the monitoring, implementation and designing of any information system. This

type of system includes the application of the resources of current information technology towards

conventional accounting controls. This also involves the processes of providing the users with the

financial information needed for managing the business. Further, the system is the component of the

system of the entity’s management information. The current technological abilities allow a range of

probable designs for the AIS (Schaltegger and Burritt 2017). However, the primary structure of the

system has been continuing to involve the three elements of input, output and processing. Next, the

input devices are commonly related to the AIS and involve the personal machines or the

workstations that run applications. It scans the different devices related to the overall standardized

data entry along with electronic communication devices. This is regarding EDI or Electronic Data

Interchange along with the innovation of e-commerce or electronic commerce (Libby 2017).

Moreover, the basic process is gained through the systems that range from individual PC to the huge

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING INFORMATION SYSTEMS

scale enterprise servers. Nevertheless, conceptually, the underpinning model of processing has been

the accounting system of double-entry that has been found out various centuries before. Lastly, the

out devices utilized involves the nonimpact printers, impacts and displays along with electronic

communication devices relate to e-commerce and EDI. Further, the content of the output has been

encompassing all kinds of economic report.

Under organizational context the MIS or management information systems are the systems of

interactive human or machine supporting the decision making for the users under in and out of

conventional organizational limits. The systems are utilized for supporting the regular operational

tasks, resent and further tactical decisions along with the entire strategic pathway (Maskell,

Baggaley and Grasso 2017). Besides, the MIS is created of various important applications that

involve human resource systems and financial information. The financial information application is

at the core of AIS in real-life practice. Here, the different modules implemented commonly involves

the budgeting, projects, assets, inventories, billing, receivables, purchasing or procurements,

payables and common ledger. Again, human resource applications are the other important element of

present-day information systems. Commonly that are commonly integrated to the AIS involves the

labor reporting, time, payroll, pension administration, benefits administration and human resources

(Collier 2015).

Thus AIS is able to cover the different types of business functions originating from the

system of transaction processing systems of accounting transactions to the developed process system

and planning of financial management. The financial report begins with operational levels of

business. Here, the transaction processing system is able to capture the vital events of business-like

common selling, purchasing and production activities. Here transactions or events are summarized

and classified for making decisions internally and for the financial reporting externally (Diatmika,

scale enterprise servers. Nevertheless, conceptually, the underpinning model of processing has been

the accounting system of double-entry that has been found out various centuries before. Lastly, the

out devices utilized involves the nonimpact printers, impacts and displays along with electronic

communication devices relate to e-commerce and EDI. Further, the content of the output has been

encompassing all kinds of economic report.

Under organizational context the MIS or management information systems are the systems of

interactive human or machine supporting the decision making for the users under in and out of

conventional organizational limits. The systems are utilized for supporting the regular operational

tasks, resent and further tactical decisions along with the entire strategic pathway (Maskell,

Baggaley and Grasso 2017). Besides, the MIS is created of various important applications that

involve human resource systems and financial information. The financial information application is

at the core of AIS in real-life practice. Here, the different modules implemented commonly involves

the budgeting, projects, assets, inventories, billing, receivables, purchasing or procurements,

payables and common ledger. Again, human resource applications are the other important element of

present-day information systems. Commonly that are commonly integrated to the AIS involves the

labor reporting, time, payroll, pension administration, benefits administration and human resources

(Collier 2015).

Thus AIS is able to cover the different types of business functions originating from the

system of transaction processing systems of accounting transactions to the developed process system

and planning of financial management. The financial report begins with operational levels of

business. Here, the transaction processing system is able to capture the vital events of business-like

common selling, purchasing and production activities. Here transactions or events are summarized

and classified for making decisions internally and for the financial reporting externally (Diatmika,

5ACCOUNTING INFORMATION SYSTEMS

Irianto and Baridwan 2016). Next, the cost accounting systems like ABC or activity-based costing

are basically utilized or the environments of manufacturing. However, rousingly that are

implemented to service companies like insurance agencies, real estate firms and banks. It permits the

business sin tracking the expenses related to the production of goods and the service performances.

Lastly, the management accounting systems like master budgets are been utilized for facilitating the

control, monitoring and planning at organizational level. This type of systems permits every

managerial level to gain access for prompting the statistical and reporting analysis (Alewine, Allport

and Shen 2016). Here, the systems are utilized for collection of data in considering alternative

scenarios. This is to determine the optimal response among the various hypothetical scenarios.

Various kinds of accounting information systems:

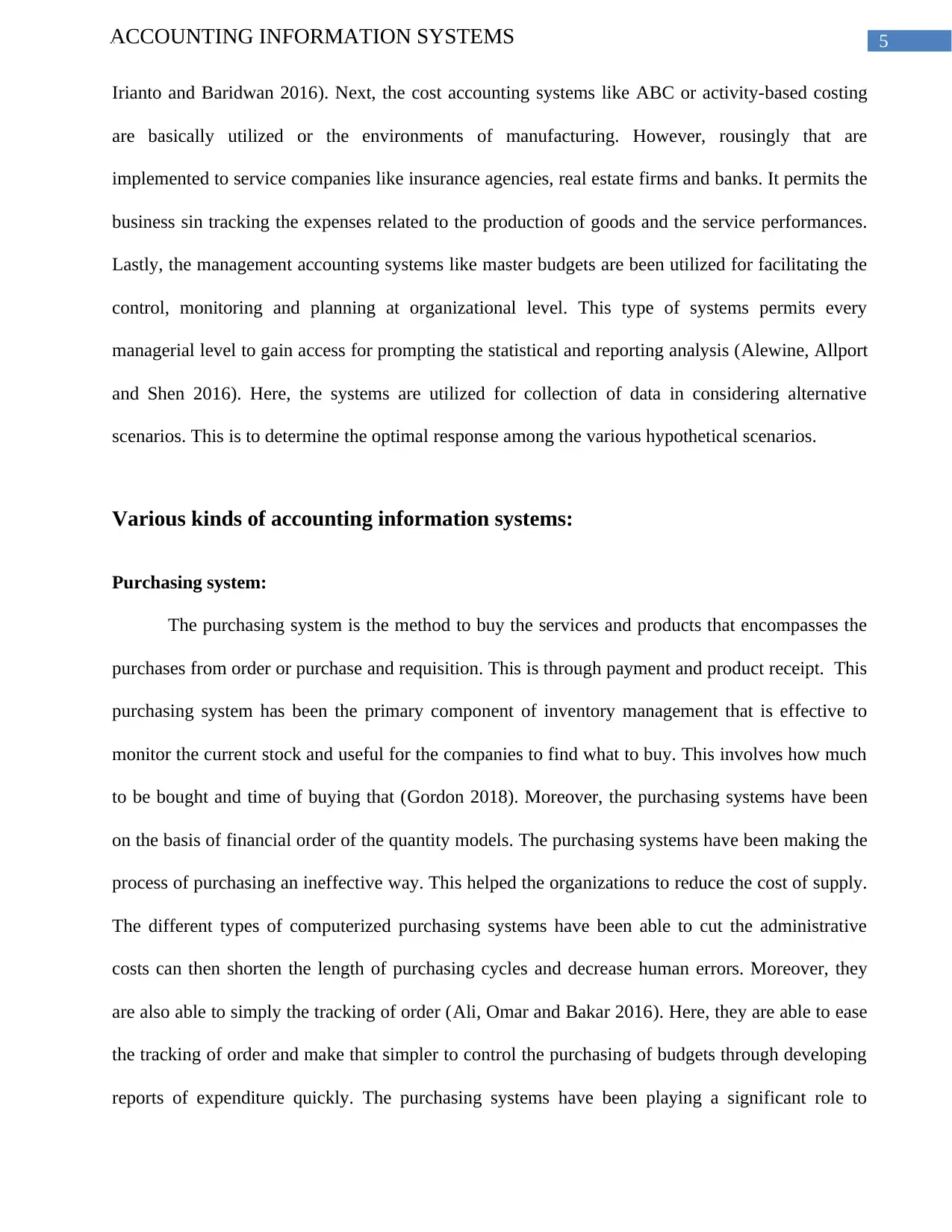

Purchasing system:

The purchasing system is the method to buy the services and products that encompasses the

purchases from order or purchase and requisition. This is through payment and product receipt. This

purchasing system has been the primary component of inventory management that is effective to

monitor the current stock and useful for the companies to find what to buy. This involves how much

to be bought and time of buying that (Gordon 2018). Moreover, the purchasing systems have been

on the basis of financial order of the quantity models. The purchasing systems have been making the

process of purchasing an ineffective way. This helped the organizations to reduce the cost of supply.

The different types of computerized purchasing systems have been able to cut the administrative

costs can then shorten the length of purchasing cycles and decrease human errors. Moreover, they

are also able to simply the tracking of order (Ali, Omar and Bakar 2016). Here, they are able to ease

the tracking of order and make that simpler to control the purchasing of budgets through developing

reports of expenditure quickly. The purchasing systems have been playing a significant role to

Irianto and Baridwan 2016). Next, the cost accounting systems like ABC or activity-based costing

are basically utilized or the environments of manufacturing. However, rousingly that are

implemented to service companies like insurance agencies, real estate firms and banks. It permits the

business sin tracking the expenses related to the production of goods and the service performances.

Lastly, the management accounting systems like master budgets are been utilized for facilitating the

control, monitoring and planning at organizational level. This type of systems permits every

managerial level to gain access for prompting the statistical and reporting analysis (Alewine, Allport

and Shen 2016). Here, the systems are utilized for collection of data in considering alternative

scenarios. This is to determine the optimal response among the various hypothetical scenarios.

Various kinds of accounting information systems:

Purchasing system:

The purchasing system is the method to buy the services and products that encompasses the

purchases from order or purchase and requisition. This is through payment and product receipt. This

purchasing system has been the primary component of inventory management that is effective to

monitor the current stock and useful for the companies to find what to buy. This involves how much

to be bought and time of buying that (Gordon 2018). Moreover, the purchasing systems have been

on the basis of financial order of the quantity models. The purchasing systems have been making the

process of purchasing an ineffective way. This helped the organizations to reduce the cost of supply.

The different types of computerized purchasing systems have been able to cut the administrative

costs can then shorten the length of purchasing cycles and decrease human errors. Moreover, they

are also able to simply the tracking of order (Ali, Omar and Bakar 2016). Here, they are able to ease

the tracking of order and make that simpler to control the purchasing of budgets through developing

reports of expenditure quickly. The purchasing systems have been playing a significant role to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING INFORMATION SYSTEMS

control the cash outflows of the company. It can assure the just needed purchases are to be done and

they are done at prices at reasonable level. Moreover, the systems of purchasing are able to utilize

the outcomes from the systems of product planning. Besides, the outcomes involve the amounts of

inputs in the process of productions.

Figure 1: “System flowchart of purchases system for Adam & Co”

(Source: Created by Author)

control the cash outflows of the company. It can assure the just needed purchases are to be done and

they are done at prices at reasonable level. Moreover, the systems of purchasing are able to utilize

the outcomes from the systems of product planning. Besides, the outcomes involve the amounts of

inputs in the process of productions.

Figure 1: “System flowchart of purchases system for Adam & Co”

(Source: Created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING INFORMATION SYSTEMS

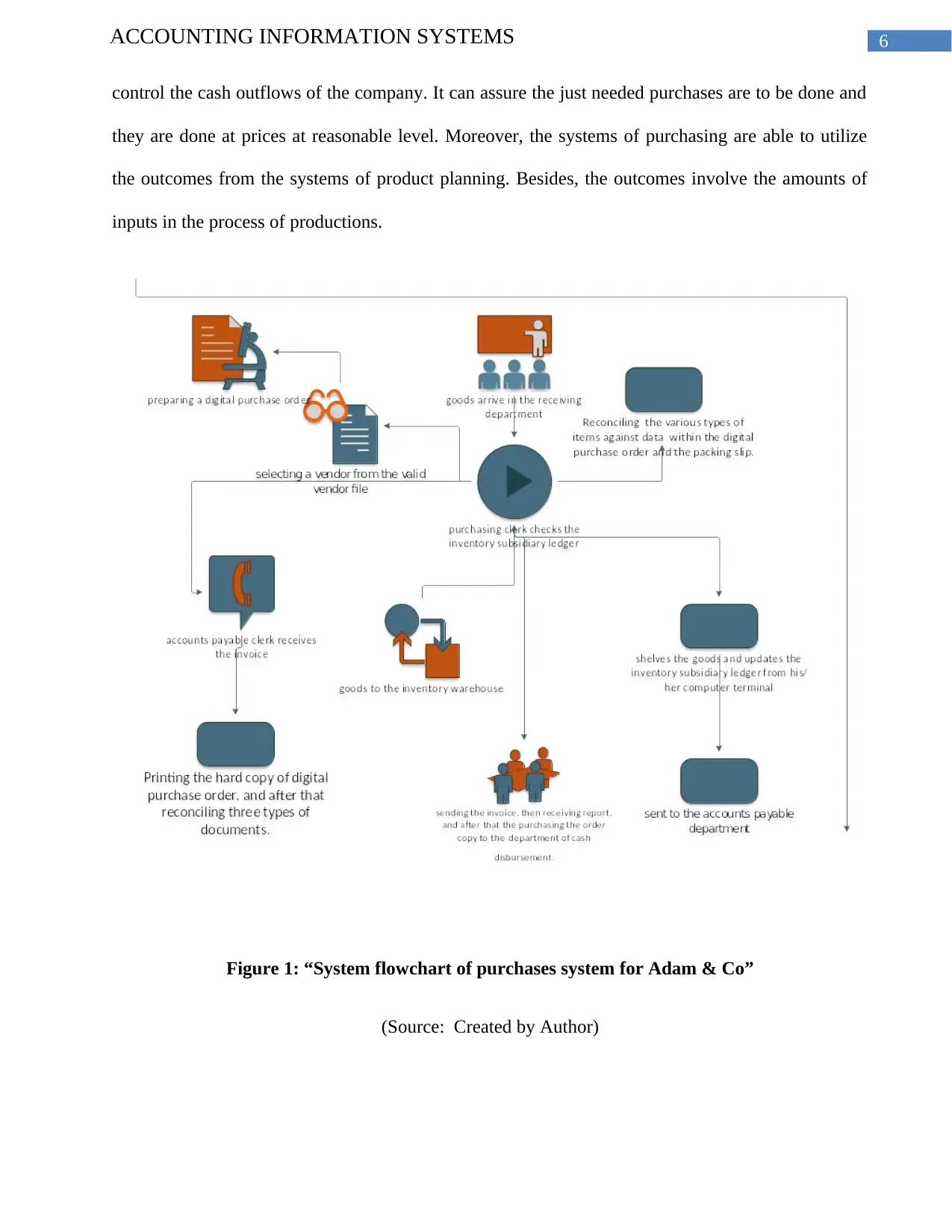

Cash disbursements systems:

Adam & Co requires the cash disbursement system such that it can securely and efficiently

control the business‘s cash payment system. It is seen that there are necessities of the system of cash

disbursement. This securely and effectively handles their cash payments. Here, their accounts

payable has been nearly connected to cash disbursements. This is to be recorded over the financial

records of Adam & Co. Here, the presence of the effective internal controls are vital under cash

disbursements and is helpful to assure that cash gets aid for legitimate type of transactions. Here, the

function of the A/P has been in charge to approve payments on the vendor of the company and the

transaction of creditor (Taiwo 2016). Moreover, A/P has been approving the transactions for just the

payment while supporting the documentation present on the transaction. The reason is that a/p can

match the needed paperwork for approval of transaction. Hence, it is preferable that it never records

the real payments to creditor and vendor for preventing the paying of invalid and fraudulent

transactions (Cleary 2017). Further, maximum of the cash disbursements have invoice payments.

Here, for instance as the inventory is been bought, the transaction should be consisting of the invoice

apart from the order of purchase and evidence of merchandise receipt. This is prior the payment for

the transaction is made. Regarding this service, the invoice must be referring to the contract detailing

the agreement of job between various parties. The missing of documentation is able sign the

unfinished transaction like non-delivery of services and products and fraudulent tasks.

Cash disbursements systems:

Adam & Co requires the cash disbursement system such that it can securely and efficiently

control the business‘s cash payment system. It is seen that there are necessities of the system of cash

disbursement. This securely and effectively handles their cash payments. Here, their accounts

payable has been nearly connected to cash disbursements. This is to be recorded over the financial

records of Adam & Co. Here, the presence of the effective internal controls are vital under cash

disbursements and is helpful to assure that cash gets aid for legitimate type of transactions. Here, the

function of the A/P has been in charge to approve payments on the vendor of the company and the

transaction of creditor (Taiwo 2016). Moreover, A/P has been approving the transactions for just the

payment while supporting the documentation present on the transaction. The reason is that a/p can

match the needed paperwork for approval of transaction. Hence, it is preferable that it never records

the real payments to creditor and vendor for preventing the paying of invalid and fraudulent

transactions (Cleary 2017). Further, maximum of the cash disbursements have invoice payments.

Here, for instance as the inventory is been bought, the transaction should be consisting of the invoice

apart from the order of purchase and evidence of merchandise receipt. This is prior the payment for

the transaction is made. Regarding this service, the invoice must be referring to the contract detailing

the agreement of job between various parties. The missing of documentation is able sign the

unfinished transaction like non-delivery of services and products and fraudulent tasks.

8ACCOUNTING INFORMATION SYSTEMS

Figure 2: “System flowchart of cash disbursements system for Adam & Co”

(Source: Created by Author)

Figure 2: “System flowchart of cash disbursements system for Adam & Co”

(Source: Created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING INFORMATION SYSTEMS

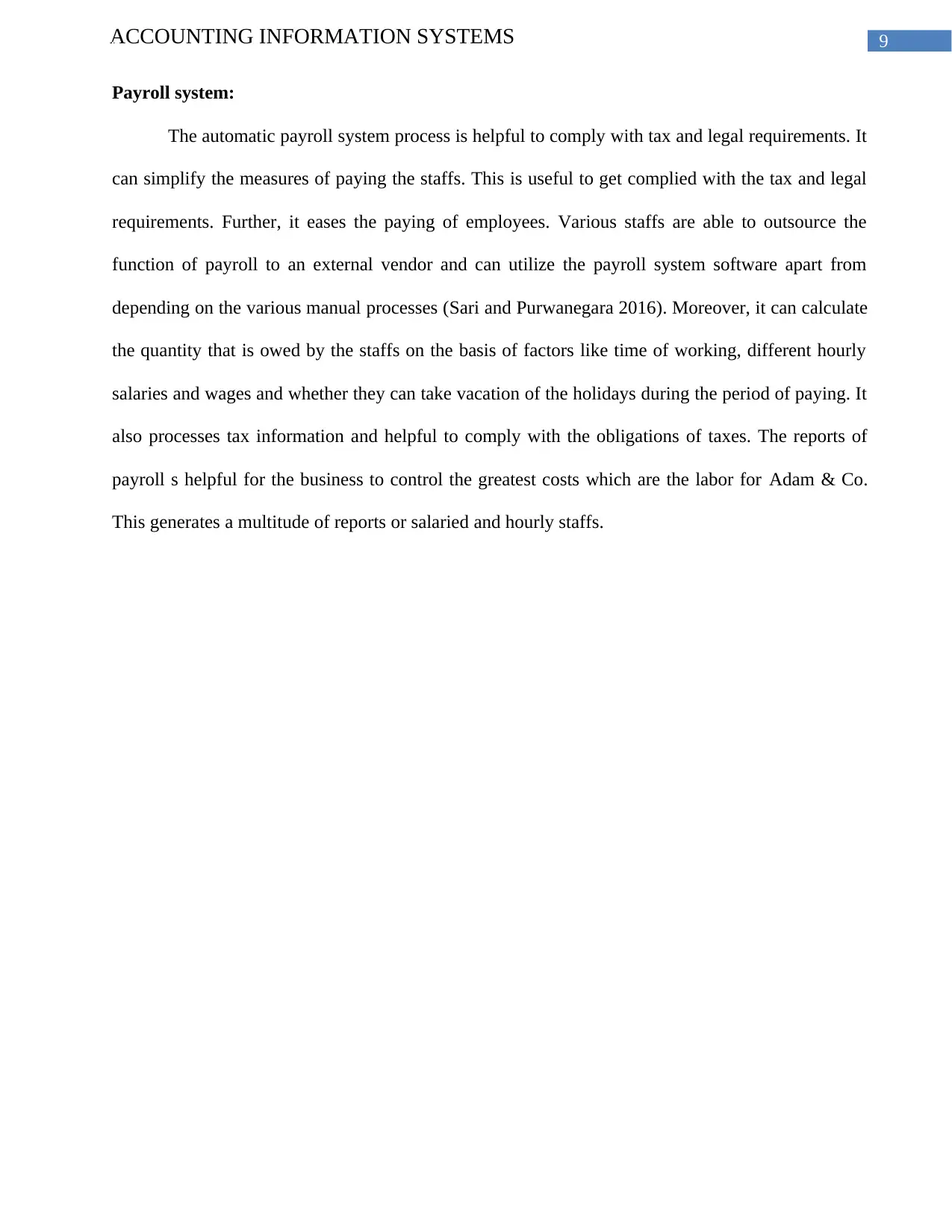

Payroll system:

The automatic payroll system process is helpful to comply with tax and legal requirements. It

can simplify the measures of paying the staffs. This is useful to get complied with the tax and legal

requirements. Further, it eases the paying of employees. Various staffs are able to outsource the

function of payroll to an external vendor and can utilize the payroll system software apart from

depending on the various manual processes (Sari and Purwanegara 2016). Moreover, it can calculate

the quantity that is owed by the staffs on the basis of factors like time of working, different hourly

salaries and wages and whether they can take vacation of the holidays during the period of paying. It

also processes tax information and helpful to comply with the obligations of taxes. The reports of

payroll s helpful for the business to control the greatest costs which are the labor for Adam & Co.

This generates a multitude of reports or salaried and hourly staffs.

Payroll system:

The automatic payroll system process is helpful to comply with tax and legal requirements. It

can simplify the measures of paying the staffs. This is useful to get complied with the tax and legal

requirements. Further, it eases the paying of employees. Various staffs are able to outsource the

function of payroll to an external vendor and can utilize the payroll system software apart from

depending on the various manual processes (Sari and Purwanegara 2016). Moreover, it can calculate

the quantity that is owed by the staffs on the basis of factors like time of working, different hourly

salaries and wages and whether they can take vacation of the holidays during the period of paying. It

also processes tax information and helpful to comply with the obligations of taxes. The reports of

payroll s helpful for the business to control the greatest costs which are the labor for Adam & Co.

This generates a multitude of reports or salaried and hourly staffs.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING INFORMATION SYSTEMS

Figure 3: “System flowchart of payroll system for Adam & Co”

(Source: Created by Author)

Figure 3: “System flowchart of payroll system for Adam & Co”

(Source: Created by Author)

11ACCOUNTING INFORMATION SYSTEMS

Describing the weakness of internal control in every system and the risks related

to the weaknesses identified:

For purchasing system they can face the concern about the understatement of need. For the

weakness is purchasing of improper service or product, wastage of money, necessity did not satisfy.

Then there is the overstatement of need. It can lead to poor competition and higher expense. Then,

there is the misinterpretation of user needs. They are fully unacceptable purchasing, time lost, rise in

cost and probable downtime (Feeney and Pierce 2016). Further, there is insufficient funding. This

can give rise of delay to make the purchase, extra expenses for the re-tender. Further, there is the

impractical timeframe. This has improper reactions from the tenders, decrease in competition and

not meeting the delivery schedule. Lastly, there are the issues of probity. This involves the rise in

procurement expenses, misuse of the resources, the most appropriate products are never gained and

unethical conducts.

For Cash disbursements systems there are improper controls. Here, the internal controls are

decided and created on the business. However, this is not always suitable and the controls can be too

lax in some sectors that might result in security concerns. Further, there can be missing controls with

particular circumstances. As the internal controls are never been regulated from the external

authority there are scopes that some of the controls needed are skipped (Arabmazar Yazdi et al.

2017). For instance, Adam & Co may have detailed controls for the cash disbursements for the

common business projects. Nevertheless, they are at a loss as the disbursements for the grant

program is considered. The accountability indicates to security of internal controls and capability of

withstanding misuse and misconduct. Further, the security measures are able to alter the channels

through which cash is able to move. However, the internal controls are able to alter very fast. This

Describing the weakness of internal control in every system and the risks related

to the weaknesses identified:

For purchasing system they can face the concern about the understatement of need. For the

weakness is purchasing of improper service or product, wastage of money, necessity did not satisfy.

Then there is the overstatement of need. It can lead to poor competition and higher expense. Then,

there is the misinterpretation of user needs. They are fully unacceptable purchasing, time lost, rise in

cost and probable downtime (Feeney and Pierce 2016). Further, there is insufficient funding. This

can give rise of delay to make the purchase, extra expenses for the re-tender. Further, there is the

impractical timeframe. This has improper reactions from the tenders, decrease in competition and

not meeting the delivery schedule. Lastly, there are the issues of probity. This involves the rise in

procurement expenses, misuse of the resources, the most appropriate products are never gained and

unethical conducts.

For Cash disbursements systems there are improper controls. Here, the internal controls are

decided and created on the business. However, this is not always suitable and the controls can be too

lax in some sectors that might result in security concerns. Further, there can be missing controls with

particular circumstances. As the internal controls are never been regulated from the external

authority there are scopes that some of the controls needed are skipped (Arabmazar Yazdi et al.

2017). For instance, Adam & Co may have detailed controls for the cash disbursements for the

common business projects. Nevertheless, they are at a loss as the disbursements for the grant

program is considered. The accountability indicates to security of internal controls and capability of

withstanding misuse and misconduct. Further, the security measures are able to alter the channels

through which cash is able to move. However, the internal controls are able to alter very fast. This

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.