Accounting Information Systems Case Study: Adam & Co Analysis

VerifiedAdded on 2022/12/27

|16

|3242

|63

Case Study

AI Summary

This case study examines the accounting information systems of Adam & Co, a wholesaler based in Perth, focusing on its purchases, cash disbursements, and payroll systems. The analysis identifies internal control weaknesses within each system, including issues like overstocking, lack of order tracking, and inadequate supplier selection in the purchases system; improper controls, accountability issues, and adaptation problems in the cash disbursement system; and data entry errors, processing division, and insufficient audits in the payroll system. The report assesses the associated risks, such as fraud, errors, and operational inefficiencies, and provides system flowcharts for each area. The study emphasizes the importance of maintaining robust internal controls to mitigate risks and ensure the reliability of financial reporting and operational effectiveness. The study aims to provide a comprehensive analysis of accounting information systems and their importance in business operations.

ACCOUNTING FOR INFORMATION SYSTEM

Accounting for Information System

Name of the Student

Student Number

Author Note

Accounting for Information System

Name of the Student

Student Number

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING FOR INFORMATION SYSTEM

EXECUTIVE SUMMARY

Adam & Co is the wholesaler of the industrial supplies based in Perth. Its inventory is sourced

from the manufacturers in Vietnam, Thailand and China. This company comprises of a central

accounting system containing the networked terminal at various locations. There are various

procedures of expenditure cycle of this company comprising of the purchases system, cash

disbursements system and the payroll system. The weaknesses of the internal control for each of

the three systems that is purchases system, cash disbursement system as well as the payroll

system has been evaluated. The risks associated along with all the identified weaknesses of the

internal control has also been discussed along with flow charts for each of the systems. The

internal control should always be maintained in all of these systems.

ACCOUNTING FOR INFORMATION SYSTEM

EXECUTIVE SUMMARY

Adam & Co is the wholesaler of the industrial supplies based in Perth. Its inventory is sourced

from the manufacturers in Vietnam, Thailand and China. This company comprises of a central

accounting system containing the networked terminal at various locations. There are various

procedures of expenditure cycle of this company comprising of the purchases system, cash

disbursements system and the payroll system. The weaknesses of the internal control for each of

the three systems that is purchases system, cash disbursement system as well as the payroll

system has been evaluated. The risks associated along with all the identified weaknesses of the

internal control has also been discussed along with flow charts for each of the systems. The

internal control should always be maintained in all of these systems.

2

ACCOUNTING FOR INFORMATION SYSTEM

Table of Contents

Introduction......................................................................................................................................3

Body.................................................................................................................................................3

Purchases System.........................................................................................................................4

Risks associated with the purchases system................................................................................6

Cash Disbursements Systems......................................................................................................7

Internal control weaknesses in the cash disbursements system.................................................10

Risks associated with the cash disbursements system...............................................................10

Payroll System...........................................................................................................................11

Internal control weaknesses in the payroll system....................................................................13

Risks associated with the payroll system...................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

ACCOUNTING FOR INFORMATION SYSTEM

Table of Contents

Introduction......................................................................................................................................3

Body.................................................................................................................................................3

Purchases System.........................................................................................................................4

Risks associated with the purchases system................................................................................6

Cash Disbursements Systems......................................................................................................7

Internal control weaknesses in the cash disbursements system.................................................10

Risks associated with the cash disbursements system...............................................................10

Payroll System...........................................................................................................................11

Internal control weaknesses in the payroll system....................................................................13

Risks associated with the payroll system...................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING FOR INFORMATION SYSTEM

Introduction

Adam & Co is the wholesaler of the industrial supplies based in Perth. Its inventory is

sourced from the manufacturers in Vietnam, Thailand and China. This company comprises of a

central accounting system containing the networked terminal at various locations (Huang et al.

2019). There are various procedures of expenditure cycle of this company comprising of the

purchases system, cash disbursements system and the payroll system. The report aims to discuss

the weakness related to the internal control of each of the mentioned systems in related to this

company. This report also focuses on detecting the possible risks that is associated with the

weakness that has been identified for each of the mentioned systems (Sagala et al. 2016). The

processes as well as risks attached to the internal controls will also be evaluated in this report.

Body

In terms of auditing as well as accounting, the term internal control is a method for

satisfying the goals or the achievements of the objectives and aims of the organization in terms

of operational efficiency and effectiveness, its compliance with the laws, certain rules, policies,

regulations and a financial reporting that must be reliable in nature. Everything regarding the risk

control to the organizations is included in the internal control (Zakaria et al. 2016). The internal

control plays a role in the form of channel through which all the resources of an organization are

monitored, measured as well as directed. An essential part is played by it in prevention and

detection of frauds along with the protection of the resources of the organization (Apple 2017).

The resources might be both intangible like intellectual property in the form of trademarks,

reputation to name a few and physical like properties and machineries of the organization.

Purchases System

A purchases system is an essential part involved in the accounting system and is a

method for buying the services as well as the products surrounding the purchases from the

requisition and the order of the purchase through the receipt of the product along with the

payment. This type of systems forms a key constituent for managing the inventory in an effective

way (Appelbaum et al. 2017). In the inventory management is where the existing stocks are

monitored and the companies are assisted in determining what goods should be purchased, when

ACCOUNTING FOR INFORMATION SYSTEM

Introduction

Adam & Co is the wholesaler of the industrial supplies based in Perth. Its inventory is

sourced from the manufacturers in Vietnam, Thailand and China. This company comprises of a

central accounting system containing the networked terminal at various locations (Huang et al.

2019). There are various procedures of expenditure cycle of this company comprising of the

purchases system, cash disbursements system and the payroll system. The report aims to discuss

the weakness related to the internal control of each of the mentioned systems in related to this

company. This report also focuses on detecting the possible risks that is associated with the

weakness that has been identified for each of the mentioned systems (Sagala et al. 2016). The

processes as well as risks attached to the internal controls will also be evaluated in this report.

Body

In terms of auditing as well as accounting, the term internal control is a method for

satisfying the goals or the achievements of the objectives and aims of the organization in terms

of operational efficiency and effectiveness, its compliance with the laws, certain rules, policies,

regulations and a financial reporting that must be reliable in nature. Everything regarding the risk

control to the organizations is included in the internal control (Zakaria et al. 2016). The internal

control plays a role in the form of channel through which all the resources of an organization are

monitored, measured as well as directed. An essential part is played by it in prevention and

detection of frauds along with the protection of the resources of the organization (Apple 2017).

The resources might be both intangible like intellectual property in the form of trademarks,

reputation to name a few and physical like properties and machineries of the organization.

Purchases System

A purchases system is an essential part involved in the accounting system and is a

method for buying the services as well as the products surrounding the purchases from the

requisition and the order of the purchase through the receipt of the product along with the

payment. This type of systems forms a key constituent for managing the inventory in an effective

way (Appelbaum et al. 2017). In the inventory management is where the existing stocks are

monitored and the companies are assisted in determining what goods should be purchased, when

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING FOR INFORMATION SYSTEM

the goods should be purchased and how much goods should be purchased (Morris et al. 2016).

The purchases systems might be dependent on the models that are related to economic order

quantity. In addition to this, a very important role is played by the purchases systems for

controlling the cash outflows of the organizations. It also helps in ensuring that the necessary as

well as much needed purchases are made and that at justifiable costs (Shin et al. 2017). The

weakness present in the internal control of the purchases system has been mentioned further.

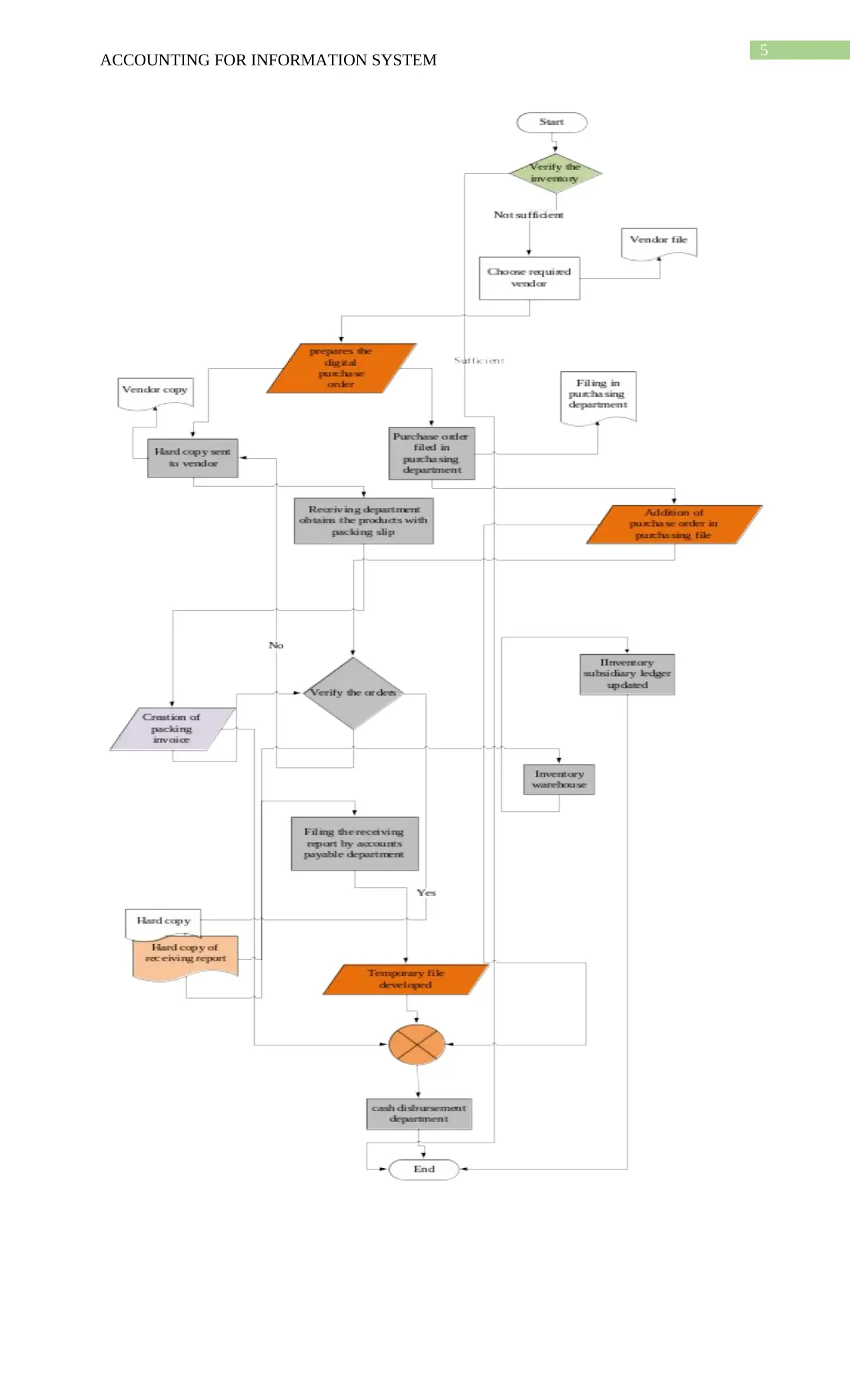

The system flowchart for purchases system:

ACCOUNTING FOR INFORMATION SYSTEM

the goods should be purchased and how much goods should be purchased (Morris et al. 2016).

The purchases systems might be dependent on the models that are related to economic order

quantity. In addition to this, a very important role is played by the purchases systems for

controlling the cash outflows of the organizations. It also helps in ensuring that the necessary as

well as much needed purchases are made and that at justifiable costs (Shin et al. 2017). The

weakness present in the internal control of the purchases system has been mentioned further.

The system flowchart for purchases system:

5

ACCOUNTING FOR INFORMATION SYSTEM

ACCOUNTING FOR INFORMATION SYSTEM

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING FOR INFORMATION SYSTEM

Internal control weaknesses in the purchases system

The internal control weakness in the purchases system are as follows:

The internal control systems present in the purchases system are it is not checked with the

stock with respect to the requisition of the purchases by the individuals who are

accountable for the purchases system which might lead to overstock (Shareef et al. 2016).

The order sequence as well as the orders that are cancelled are not accounted which

might lead to the misplacement of the orders along with no occurrence of the transaction

for the purchases.

The selection of the suppliers takes place on the basis of the reputation of the suppliers

instead of the other essential factors like the terms provided by the supplier, duration of

the delivery of the suppliers along with the prices of the materials supplied by them.

Various incoming goods like the assets that are fixed are never cleared through the

receiving department or the goods inwards.

The good inwards manager only has the right to approve any sort of discrepancy occurred

between the delivery docket and the order (Kelly et al. 2016). Except the goods inward

manager, nobody has the right or is authorized for approving the occurred discrepancies

if the manager is absent.

The purchases systems should be checked on a regular basis for the reduction of the risks of

the occurrence of the frauds or certain errors in the process of transactions (Loishyn et al. 2019).

The various risks associated with the identified weaknesses in the purchases system are

mentioned below.

Risks associated with the purchases system

The risks associated with the above identified weaknesses of the internal control in the

purchases system are as follows:

Irregular check- up of the stocks lead to overstock and can hamper the quality as

well as the delivery of the tasks.

The order sequence as well as cancelled orders are not accounted and leads to the

misplacements of all the orders.

The selected suppliers with no reputation can harm the quality of the goods and

can commit frauds.

ACCOUNTING FOR INFORMATION SYSTEM

Internal control weaknesses in the purchases system

The internal control weakness in the purchases system are as follows:

The internal control systems present in the purchases system are it is not checked with the

stock with respect to the requisition of the purchases by the individuals who are

accountable for the purchases system which might lead to overstock (Shareef et al. 2016).

The order sequence as well as the orders that are cancelled are not accounted which

might lead to the misplacement of the orders along with no occurrence of the transaction

for the purchases.

The selection of the suppliers takes place on the basis of the reputation of the suppliers

instead of the other essential factors like the terms provided by the supplier, duration of

the delivery of the suppliers along with the prices of the materials supplied by them.

Various incoming goods like the assets that are fixed are never cleared through the

receiving department or the goods inwards.

The good inwards manager only has the right to approve any sort of discrepancy occurred

between the delivery docket and the order (Kelly et al. 2016). Except the goods inward

manager, nobody has the right or is authorized for approving the occurred discrepancies

if the manager is absent.

The purchases systems should be checked on a regular basis for the reduction of the risks of

the occurrence of the frauds or certain errors in the process of transactions (Loishyn et al. 2019).

The various risks associated with the identified weaknesses in the purchases system are

mentioned below.

Risks associated with the purchases system

The risks associated with the above identified weaknesses of the internal control in the

purchases system are as follows:

Irregular check- up of the stocks lead to overstock and can hamper the quality as

well as the delivery of the tasks.

The order sequence as well as cancelled orders are not accounted and leads to the

misplacements of all the orders.

The selected suppliers with no reputation can harm the quality of the goods and

can commit frauds.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING FOR INFORMATION SYSTEM

The fixed assets are not cleared by the receiving department and this might result

in the overstock.

The right to approve the discrepancy is given to only one person and if that person

is absent, then nobody will be able

Cash Disbursements Systems

A cash disbursement system is simply termed as the paid cash outflow in exchange of the

provision of the services as well as goods. A cash disbursement system can be utilized for

refunding a customer that in turn is recorded in the form of a sales reduction. The other form of

the cash disbursement system is the dividend payment which is again recorded in the form of a

corporate equity reduction (Sari 2017). The process of cash disbursement can be executed with a

single check, coins or bills or with the electronic funds transfer. The scenario here can be like

any payment is made in the form of a check, a delay of some days will occur before the

withdrawal of the funds from the checking account of the organization because of the severe

impacts of the processing float as well as the mail float (Oro et al. 2016). The cash

disbursements are generally done by the means of the accounts payable system. The other

method by which the funds can also be disbursed is by the means of petty cash or the payroll

system that will be discussed next. In simple words, the system of the cash disbursement can be

described in terms of the money payment or the outflow of cash for settling up of the various

obligations like the expenses of operating, interests regarding the loan payments along with the

accounts receivable for carrying out the activities related to the business for a certain amount of

time (Sari 2018). It is executed through the plastic money, checks, cash, electronic funds transfer

as well as warrants.

In other words the cash disbursement is the delivery of the funds from the other funds or

bank accounts (Griffin et al. 2017). This is a payment which is done by the company in the form

of equivalents of cash or actual cash during a fixed amount of time like yearly, quarterly or even

in three months.

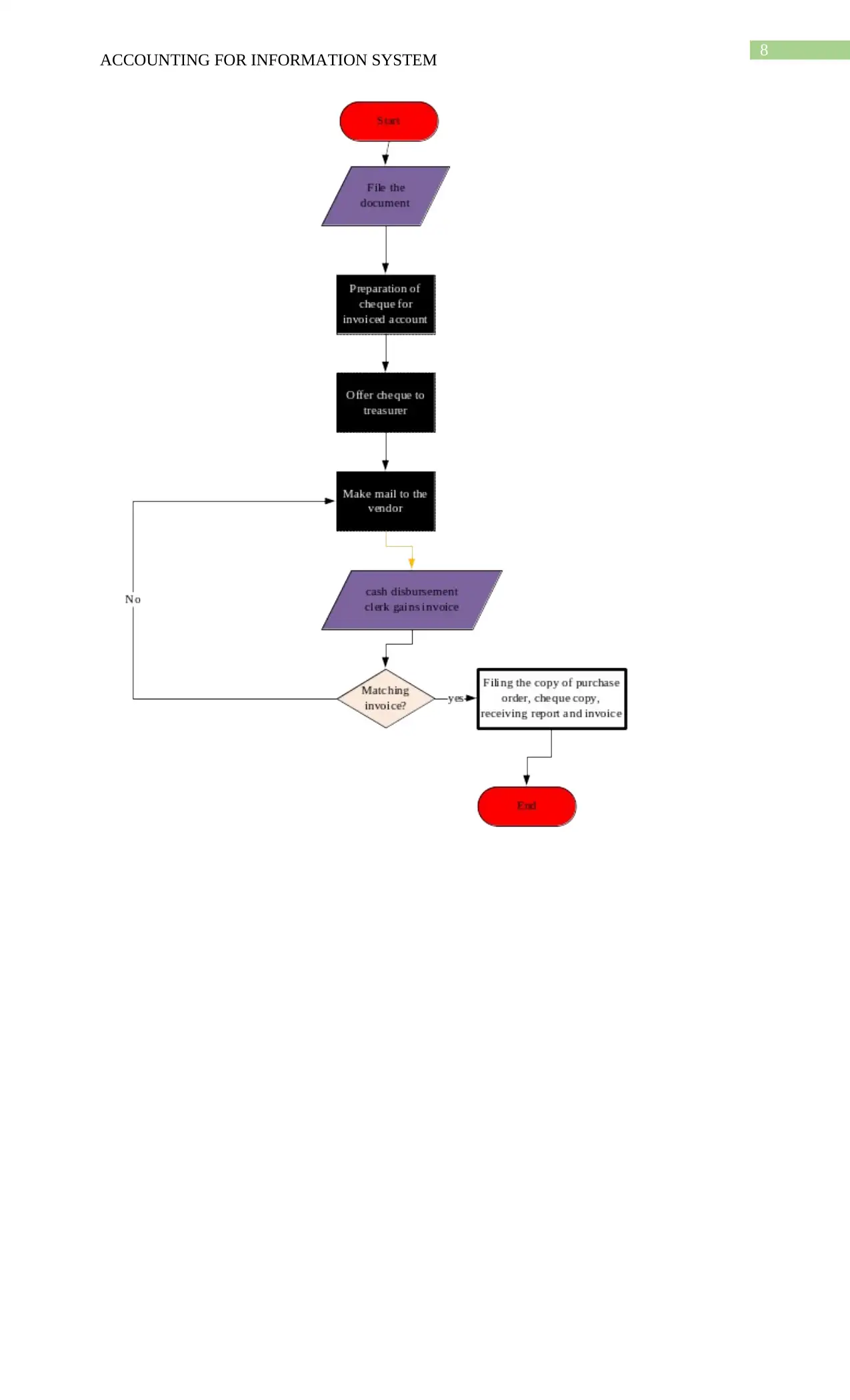

The system flowchart of cash disbursement system :

ACCOUNTING FOR INFORMATION SYSTEM

The fixed assets are not cleared by the receiving department and this might result

in the overstock.

The right to approve the discrepancy is given to only one person and if that person

is absent, then nobody will be able

Cash Disbursements Systems

A cash disbursement system is simply termed as the paid cash outflow in exchange of the

provision of the services as well as goods. A cash disbursement system can be utilized for

refunding a customer that in turn is recorded in the form of a sales reduction. The other form of

the cash disbursement system is the dividend payment which is again recorded in the form of a

corporate equity reduction (Sari 2017). The process of cash disbursement can be executed with a

single check, coins or bills or with the electronic funds transfer. The scenario here can be like

any payment is made in the form of a check, a delay of some days will occur before the

withdrawal of the funds from the checking account of the organization because of the severe

impacts of the processing float as well as the mail float (Oro et al. 2016). The cash

disbursements are generally done by the means of the accounts payable system. The other

method by which the funds can also be disbursed is by the means of petty cash or the payroll

system that will be discussed next. In simple words, the system of the cash disbursement can be

described in terms of the money payment or the outflow of cash for settling up of the various

obligations like the expenses of operating, interests regarding the loan payments along with the

accounts receivable for carrying out the activities related to the business for a certain amount of

time (Sari 2018). It is executed through the plastic money, checks, cash, electronic funds transfer

as well as warrants.

In other words the cash disbursement is the delivery of the funds from the other funds or

bank accounts (Griffin et al. 2017). This is a payment which is done by the company in the form

of equivalents of cash or actual cash during a fixed amount of time like yearly, quarterly or even

in three months.

The system flowchart of cash disbursement system :

8

ACCOUNTING FOR INFORMATION SYSTEM

ACCOUNTING FOR INFORMATION SYSTEM

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING FOR INFORMATION SYSTEM

Internal control weaknesses in the cash disbursements system

Improper internal controls forms one of the reason behind the weaknesses in the internal

control of the cash disbursement system.

Next is the missing of the controls as well as certain circumstances

Accountability refers to a major internal weakness in the internal control of cash

disbursement system.

The continuous issues related to adaptation also forms a major weakness.

Risks associated with the cash disbursements system

The risks associated with the cash disbursement system are as follows:

The decisions taken regarding the internal controls are not always appropriate (Rodgers

et al. 2015). The controls can be questionable in some areas which might lead to the

various concerns related to security that might lead to inappropriate delays in funding as

well as consumes a lot of time.

Some of the essential controls might be skipped if the internal controls will not be

regulated by the authorities outside like a business might face a loss regarding a new

program due to incomplete creation of rules because of certain problems like this.

The secured internal controls are referred by accountability along with the capabilities of

avoiding the misuse as well misconduct of the internal control of the cash disbursement

system.

In context of the adaptation issues, the internal controls might not be able to change very

quickly as well as easily by leaving certain organizations that are in turn lagging behind

and it tries and aims for meeting the modern and advanced requirements with the

strategies that have become outdated.

Payroll System

A payroll system is responsible for calculating the total amount that are owed to the

employees by the organization. This is executed on the basis of certain factors like the duration

of their work in the organization, their salaries or wages per hour and also on the basis of the

vacation leave or holiday time taken by them at the time of their payment period (Rozzani et al.

2016). The gross pay is adjusted by the system by the process of subtracting as well as

calculating the taxes along with other amount that are withheld regarding the taxes related to

ACCOUNTING FOR INFORMATION SYSTEM

Internal control weaknesses in the cash disbursements system

Improper internal controls forms one of the reason behind the weaknesses in the internal

control of the cash disbursement system.

Next is the missing of the controls as well as certain circumstances

Accountability refers to a major internal weakness in the internal control of cash

disbursement system.

The continuous issues related to adaptation also forms a major weakness.

Risks associated with the cash disbursements system

The risks associated with the cash disbursement system are as follows:

The decisions taken regarding the internal controls are not always appropriate (Rodgers

et al. 2015). The controls can be questionable in some areas which might lead to the

various concerns related to security that might lead to inappropriate delays in funding as

well as consumes a lot of time.

Some of the essential controls might be skipped if the internal controls will not be

regulated by the authorities outside like a business might face a loss regarding a new

program due to incomplete creation of rules because of certain problems like this.

The secured internal controls are referred by accountability along with the capabilities of

avoiding the misuse as well misconduct of the internal control of the cash disbursement

system.

In context of the adaptation issues, the internal controls might not be able to change very

quickly as well as easily by leaving certain organizations that are in turn lagging behind

and it tries and aims for meeting the modern and advanced requirements with the

strategies that have become outdated.

Payroll System

A payroll system is responsible for calculating the total amount that are owed to the

employees by the organization. This is executed on the basis of certain factors like the duration

of their work in the organization, their salaries or wages per hour and also on the basis of the

vacation leave or holiday time taken by them at the time of their payment period (Rozzani et al.

2016). The gross pay is adjusted by the system by the process of subtracting as well as

calculating the taxes along with other amount that are withheld regarding the taxes related to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING FOR INFORMATION SYSTEM

payroll like the social security taxes, state income taxes, medical care taxes and federal income

taxes if they are applicable and are needed.

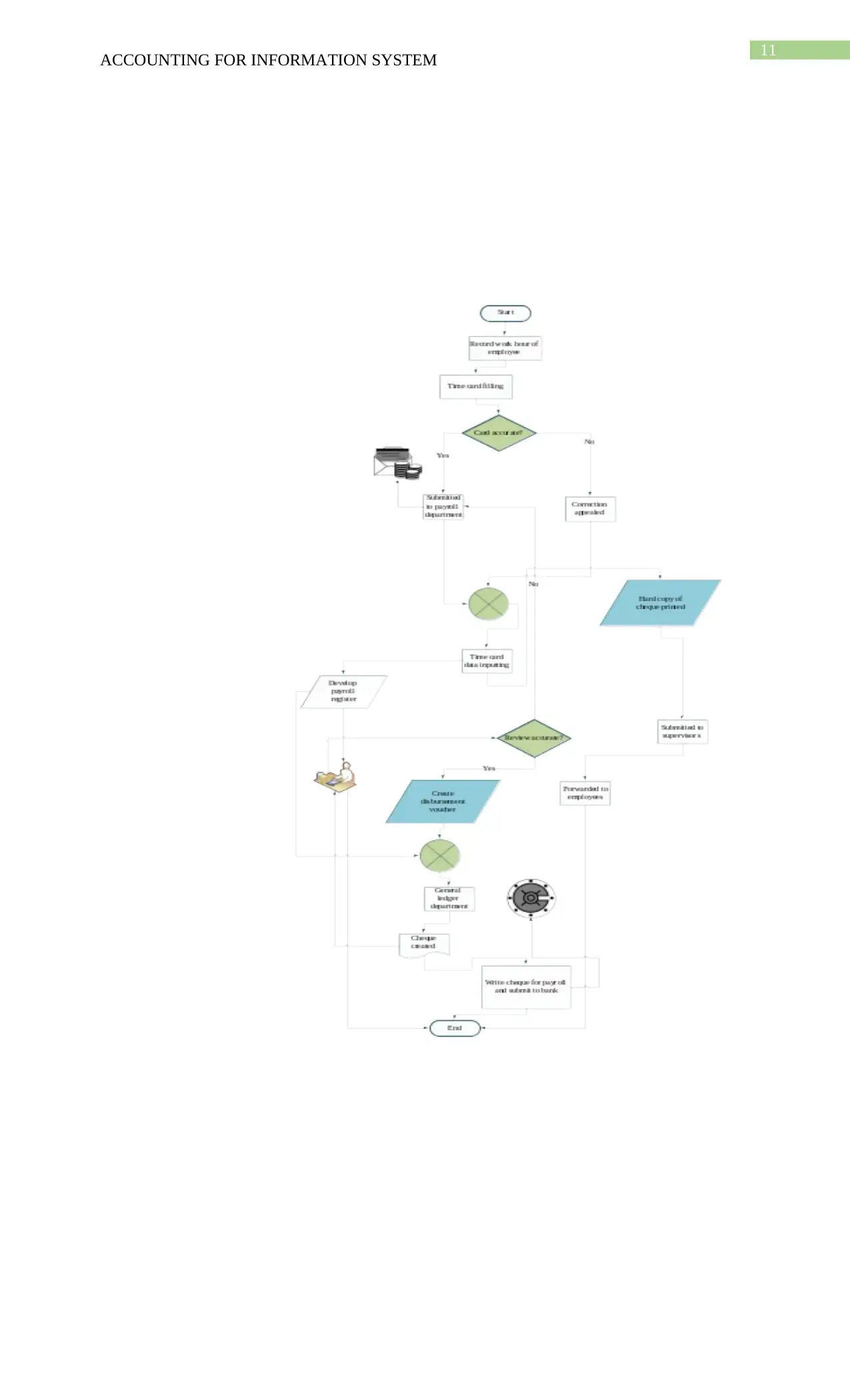

The system flowchart for payroll system

ACCOUNTING FOR INFORMATION SYSTEM

payroll like the social security taxes, state income taxes, medical care taxes and federal income

taxes if they are applicable and are needed.

The system flowchart for payroll system

11

ACCOUNTING FOR INFORMATION SYSTEM

ACCOUNTING FOR INFORMATION SYSTEM

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.