Accounting Info Systems MP121: Luxurious Firm Case Study S2 2018

VerifiedAdded on 2023/06/03

|10

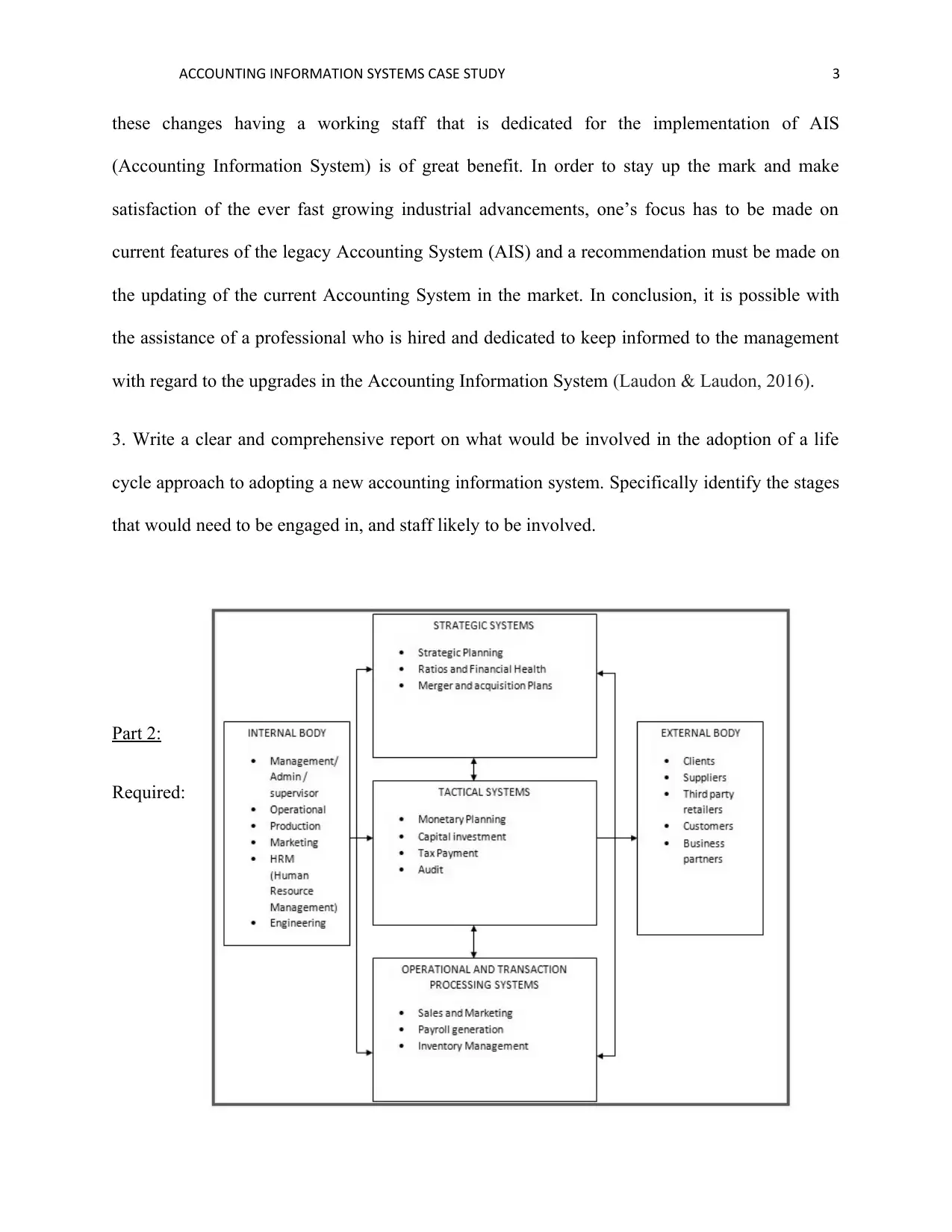

|2110

|500

Case Study

AI Summary

This case study solution analyzes the accounting information systems of Luxurious Firm, addressing issues raised by the CEO regarding the inadequacy of the current system. Part 1 outlines the roles of the management team, particularly the accounting manager, in developing a new AIS, emphasizes the importance of user involvement in the analysis and implementation phases, and details the life cycle approach to adopting a new AIS. Part 2 identifies weaknesses in the firm's expenditure cycle procedures, such as lack of cross-checking, absence of a formal inventory control system, and potential for fraudulent disbursements, along with suggested solutions. Part 3 identifies five examples of improper segregation of duties within the revenue cycle, explaining the potential risks associated with each. The solution provides actionable recommendations for improving the accounting information systems and internal controls at Luxurious Firm. Desklib offers this solution and many more solved assignments for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.