Holmes Institute HA2042 Accounting Information Systems Case Study

VerifiedAdded on 2022/11/29

|16

|2699

|79

Case Study

AI Summary

This assignment is a case study focusing on accounting information systems (AIS). It begins with an executive summary outlining the purpose of the assessment: to analyze the internal control processes of Adam & Co., identify weaknesses, and suggest improvements. The introduction defines AIS, its functions (data collection, information provision, and control), and its components, including source documents, input/output devices, processing and storage devices, and the people involved. The paper then explores key principles of AIS, such as cost-effectiveness, usefulness, and flexibility. The core of the case study involves system flowcharts for purchase, cash disbursement, and payroll systems. Each flowchart illustrates the steps and roles within these processes. Finally, the study concludes by summarizing the findings and emphasizing the importance of a robust internal control system to prevent operational issues within the company. The assignment is designed to provide a comprehensive understanding of AIS and its practical application within a business context.

Running head: ACCOUNTING INFORMATION SYSTEM

Accounting information system

Name of the student:

Name of the university:

Authors note:

Accounting information system

Name of the student:

Name of the university:

Authors note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING INFORMATION SYSTEM

Executive summary:

Inspection of the internal control process of Adam and Co.’s business and also recognition of

the feebleness, which can affect the operations of the company is the primary purpose of the

assessment. The inspection will be consisting of the flowchart that will be showing the three

variant ways related to cash payments that are made by the business and also identifies the

different roles played by the clerks and senior executives in the entire process. The issues

which are present in the manner of working of the business and even the ways of improving

will be shown in the discussion.

ACCOUNTING INFORMATION SYSTEM

Executive summary:

Inspection of the internal control process of Adam and Co.’s business and also recognition of

the feebleness, which can affect the operations of the company is the primary purpose of the

assessment. The inspection will be consisting of the flowchart that will be showing the three

variant ways related to cash payments that are made by the business and also identifies the

different roles played by the clerks and senior executives in the entire process. The issues

which are present in the manner of working of the business and even the ways of improving

will be shown in the discussion.

2

ACCOUNTING INFORMATION SYSTEM

Table of Contents

Introduction:...............................................................................................................................3

System flowchart of purchase system:.......................................................................................6

System flowchart of cash disbursements system:......................................................................6

System flowchart of payroll system:..........................................................................................6

Conclusion:................................................................................................................................6

References:.................................................................................................................................6

ACCOUNTING INFORMATION SYSTEM

Table of Contents

Introduction:...............................................................................................................................3

System flowchart of purchase system:.......................................................................................6

System flowchart of cash disbursements system:......................................................................6

System flowchart of payroll system:..........................................................................................6

Conclusion:................................................................................................................................6

References:.................................................................................................................................6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING INFORMATION SYSTEM

Introduction:

It is a systematic process for collecting data, converting them into information and

then passing that information to the ultimate users. The actual purpose is to collect, store and

process all the financial and accounting data, which is used by the managers or any other

willing parties to make any decision regarding business. It can be done through using human

resources, but in today generation computerized system is often used for an accounting

information system (Galliers and Leidner 2014).

Functions of accounting information system:

There are 3 basis functions of accounting system:

The main functions of an Accounting information system are that it is very efficient

and effective collection and storage of data concerning the organization financial

motive. It also records the transactions in the journals to ledgers account. It is the

process of getting the transaction data from the source document.

The 2nd function of an accounting information system is to provide information

which is useful for making decisions, which include making managerial reports and

financial statements.

The 3rd functions of an accounting information system are to confirm that the

controls are in place so that it can precisely record and process data.

Parts of accounting information system:

Securities measures are taken under consideration to protect the data. There is an

internal control to protect data.

The people who uses the AIS system includes accountable, managers and

business analysis.

All the data relating to AIS goes in an accounting information system.

ACCOUNTING INFORMATION SYSTEM

Introduction:

It is a systematic process for collecting data, converting them into information and

then passing that information to the ultimate users. The actual purpose is to collect, store and

process all the financial and accounting data, which is used by the managers or any other

willing parties to make any decision regarding business. It can be done through using human

resources, but in today generation computerized system is often used for an accounting

information system (Galliers and Leidner 2014).

Functions of accounting information system:

There are 3 basis functions of accounting system:

The main functions of an Accounting information system are that it is very efficient

and effective collection and storage of data concerning the organization financial

motive. It also records the transactions in the journals to ledgers account. It is the

process of getting the transaction data from the source document.

The 2nd function of an accounting information system is to provide information

which is useful for making decisions, which include making managerial reports and

financial statements.

The 3rd functions of an accounting information system are to confirm that the

controls are in place so that it can precisely record and process data.

Parts of accounting information system:

Securities measures are taken under consideration to protect the data. There is an

internal control to protect data.

The people who uses the AIS system includes accountable, managers and

business analysis.

All the data relating to AIS goes in an accounting information system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING INFORMATION SYSTEM

Software consists of a computer programmer which are used for data processing.

All the hardware which are used to operate the accounting information system are

included in information technology infrastructure.

Data are collected, stored, redeem and processed through procedures and

instructions.

Components of accounting information system:

An accounting information system generates a bedrock of five basic principles. It

teaches both principles of control as well as relevance. It also exercises upon flexibility,

compatibility and lust benefits proposition. By doing so, it fulfils the law of GAAP (generally

accepted accounting principle). This system also has more five eccentric components

(Rikhardsson 2017).

Source document:

It is one of the components of an accounting system; it is that document which

contains all the records relating to business transaction. They are the writer proof of commercial

activities. For examples of these documents are purchase orders, invoice and receipts. It is

created at the end of the business transaction they serve as an indicator of business activity and

keeps a detailed record of the sales. Source of the document can be of different mature like

tangible or digital.

Devices to capture input data:

It is one of the significant components of this system. Input devices are used to

maintain the transaction information so that it can be used for accounting purpose. By using

appropriate means, they capture data precisely and allow for its storage (Rikhardsson 2017). It is

often used by the employees; they give aid to enter this information into an accounting

information system. Example of input devices is keyboarded, touchpads and bar code scanners.

ACCOUNTING INFORMATION SYSTEM

Software consists of a computer programmer which are used for data processing.

All the hardware which are used to operate the accounting information system are

included in information technology infrastructure.

Data are collected, stored, redeem and processed through procedures and

instructions.

Components of accounting information system:

An accounting information system generates a bedrock of five basic principles. It

teaches both principles of control as well as relevance. It also exercises upon flexibility,

compatibility and lust benefits proposition. By doing so, it fulfils the law of GAAP (generally

accepted accounting principle). This system also has more five eccentric components

(Rikhardsson 2017).

Source document:

It is one of the components of an accounting system; it is that document which

contains all the records relating to business transaction. They are the writer proof of commercial

activities. For examples of these documents are purchase orders, invoice and receipts. It is

created at the end of the business transaction they serve as an indicator of business activity and

keeps a detailed record of the sales. Source of the document can be of different mature like

tangible or digital.

Devices to capture input data:

It is one of the significant components of this system. Input devices are used to

maintain the transaction information so that it can be used for accounting purpose. By using

appropriate means, they capture data precisely and allow for its storage (Rikhardsson 2017). It is

often used by the employees; they give aid to enter this information into an accounting

information system. Example of input devices is keyboarded, touchpads and bar code scanners.

5

ACCOUNTING INFORMATION SYSTEM

Processes device for information:

It is usually linked to the input devices. It receives raw data from them, processes it

and then inserts it in digital storage file such as ledger, journals. Examples of processing devices

are software and digital tools. Their last objective is to translate accounting data into information

which can be utilized by the decision-makers. New process out is able to process colossal

accounting information in seconds (Schaltegger and Burritt 2017).

Storage devices for information:

It is used to preserve the ledgers and reports that are developed from the processed

accounting date. Traditionally, file cabinet was used as storage devices, but now an accounting

information system is based on a computerized system. Due to which all the storage is

performed in the hard disk, flash drives, memory card and cloud infrastructure is stored in such a

manner so that it can support shared access.

Some principles of accounting information system:

Cost effectiveness:

The accounting information system should be economical and practical. It must

outweigh the information cost. It accounting information system is cost-effective, it can provide

the desired result, and it is flexible, and it will help much in achieving the goals of a person or

the organization as a whole(Neogy 2014.).

Useful output/ necessity:

The accounting information system must be able to provide the necessary output or

result. All the practical information must be such that can be easily comprehend, relevant,

reliable, timely and accurate. The designer of the information system will always take into

consideration the necessity and knowledge of accounting information users.

ACCOUNTING INFORMATION SYSTEM

Processes device for information:

It is usually linked to the input devices. It receives raw data from them, processes it

and then inserts it in digital storage file such as ledger, journals. Examples of processing devices

are software and digital tools. Their last objective is to translate accounting data into information

which can be utilized by the decision-makers. New process out is able to process colossal

accounting information in seconds (Schaltegger and Burritt 2017).

Storage devices for information:

It is used to preserve the ledgers and reports that are developed from the processed

accounting date. Traditionally, file cabinet was used as storage devices, but now an accounting

information system is based on a computerized system. Due to which all the storage is

performed in the hard disk, flash drives, memory card and cloud infrastructure is stored in such a

manner so that it can support shared access.

Some principles of accounting information system:

Cost effectiveness:

The accounting information system should be economical and practical. It must

outweigh the information cost. It accounting information system is cost-effective, it can provide

the desired result, and it is flexible, and it will help much in achieving the goals of a person or

the organization as a whole(Neogy 2014.).

Useful output/ necessity:

The accounting information system must be able to provide the necessary output or

result. All the practical information must be such that can be easily comprehend, relevant,

reliable, timely and accurate. The designer of the information system will always take into

consideration the necessity and knowledge of accounting information users.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING INFORMATION SYSTEM

Flexibility:

In an accounting information system, there should be flexibility in changing any

information needed by different users. It should be as flexible as to meet the change in market

demand (Daoud and Triki 2013).

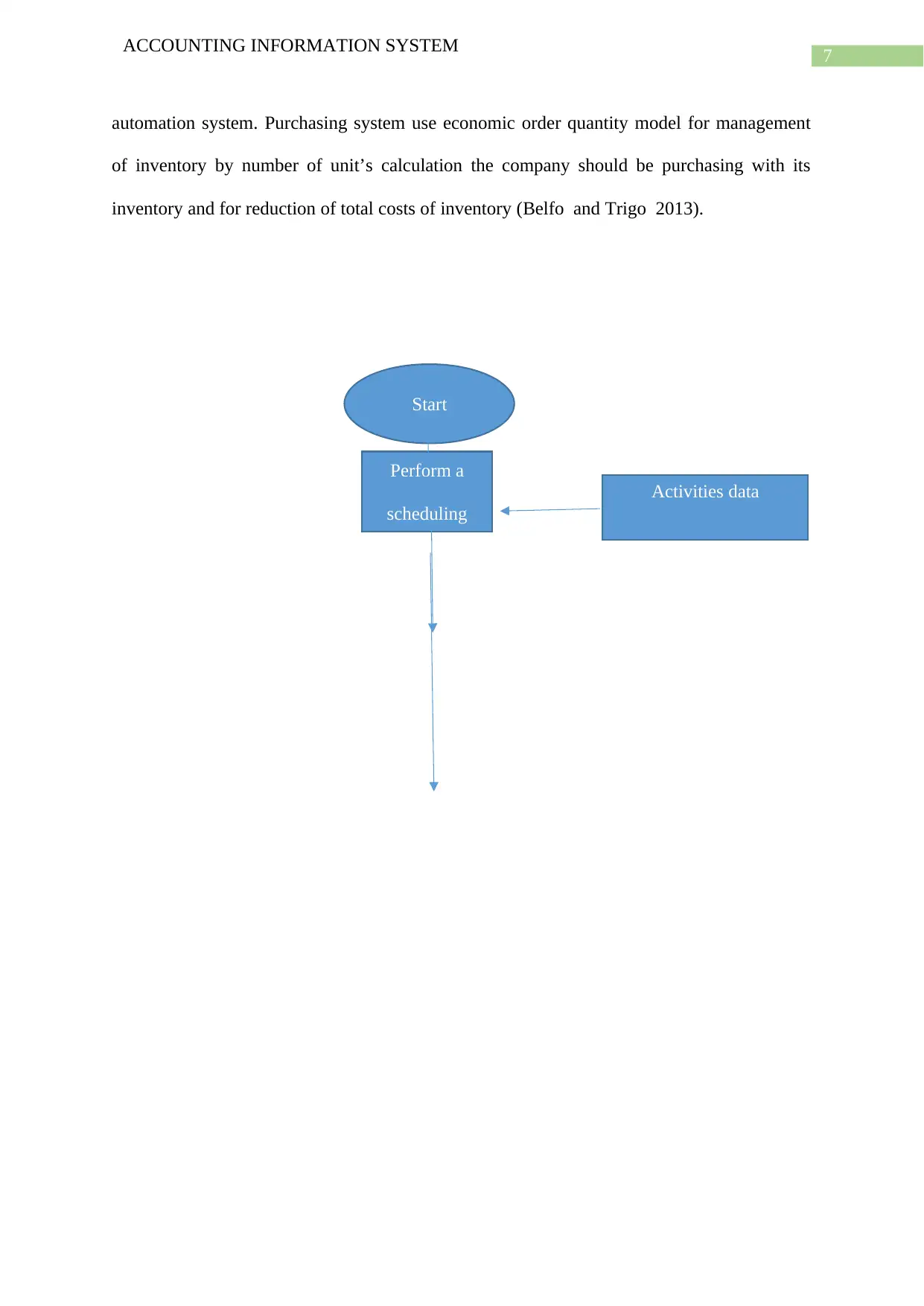

System flowchart of purchase system:

It refers to the process of purchasing products as well as services including purchase

of reacquisition as well as order of purchase with the help of receipt of product and also its

payment. Key component of inventory management is purchase system where the monitor

present stock and leads the companies for buying and how much to buy. Purchasing system

can be on the basis if economic order quantity. It can also be said that purchasing system

helps to control cash outflow of company where they can ensure only essential purchases can

be made and which are made at reasonable prices. Purchasing process by purchasing system

are very efficient to help the companies for cost reduction. Purchasing system in the form of

computerized can reduce the administrative costs of the companies, reduce length of cycle of

purchase as well as reduction in human error in reducing shortages. Purchasing system can

simplify tracking system of order and makes it very simple for managing purchase of budgets

by creation of reports related to expenditure. Purchasing system also plays an important role

for cash outflows control. It ensures that purchases in the form of necessity are made at the

reasonable prices. Use of outputs through production planning system are made by purchase

systems. Outputs include amount of inputs required for the process of production. Purchasing

system includes the purchase process with the help of receipt of product as well as payment.

Efficiency is maintained well by purchase system required for purchases and those are

effected with prices that are reasonable. Augmentation of purchase system is there through

ACCOUNTING INFORMATION SYSTEM

Flexibility:

In an accounting information system, there should be flexibility in changing any

information needed by different users. It should be as flexible as to meet the change in market

demand (Daoud and Triki 2013).

System flowchart of purchase system:

It refers to the process of purchasing products as well as services including purchase

of reacquisition as well as order of purchase with the help of receipt of product and also its

payment. Key component of inventory management is purchase system where the monitor

present stock and leads the companies for buying and how much to buy. Purchasing system

can be on the basis if economic order quantity. It can also be said that purchasing system

helps to control cash outflow of company where they can ensure only essential purchases can

be made and which are made at reasonable prices. Purchasing process by purchasing system

are very efficient to help the companies for cost reduction. Purchasing system in the form of

computerized can reduce the administrative costs of the companies, reduce length of cycle of

purchase as well as reduction in human error in reducing shortages. Purchasing system can

simplify tracking system of order and makes it very simple for managing purchase of budgets

by creation of reports related to expenditure. Purchasing system also plays an important role

for cash outflows control. It ensures that purchases in the form of necessity are made at the

reasonable prices. Use of outputs through production planning system are made by purchase

systems. Outputs include amount of inputs required for the process of production. Purchasing

system includes the purchase process with the help of receipt of product as well as payment.

Efficiency is maintained well by purchase system required for purchases and those are

effected with prices that are reasonable. Augmentation of purchase system is there through

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING INFORMATION SYSTEM

automation system. Purchasing system use economic order quantity model for management

of inventory by number of unit’s calculation the company should be purchasing with its

inventory and for reduction of total costs of inventory (Belfo and Trigo 2013).

Start

Perform a

scheduling

Activities data

ACCOUNTING INFORMATION SYSTEM

automation system. Purchasing system use economic order quantity model for management

of inventory by number of unit’s calculation the company should be purchasing with its

inventory and for reduction of total costs of inventory (Belfo and Trigo 2013).

Start

Perform a

scheduling

Activities data

8

ACCOUNTING INFORMATION SYSTEM

No

yes

Figure 1: Flow chart of Purchasing System.

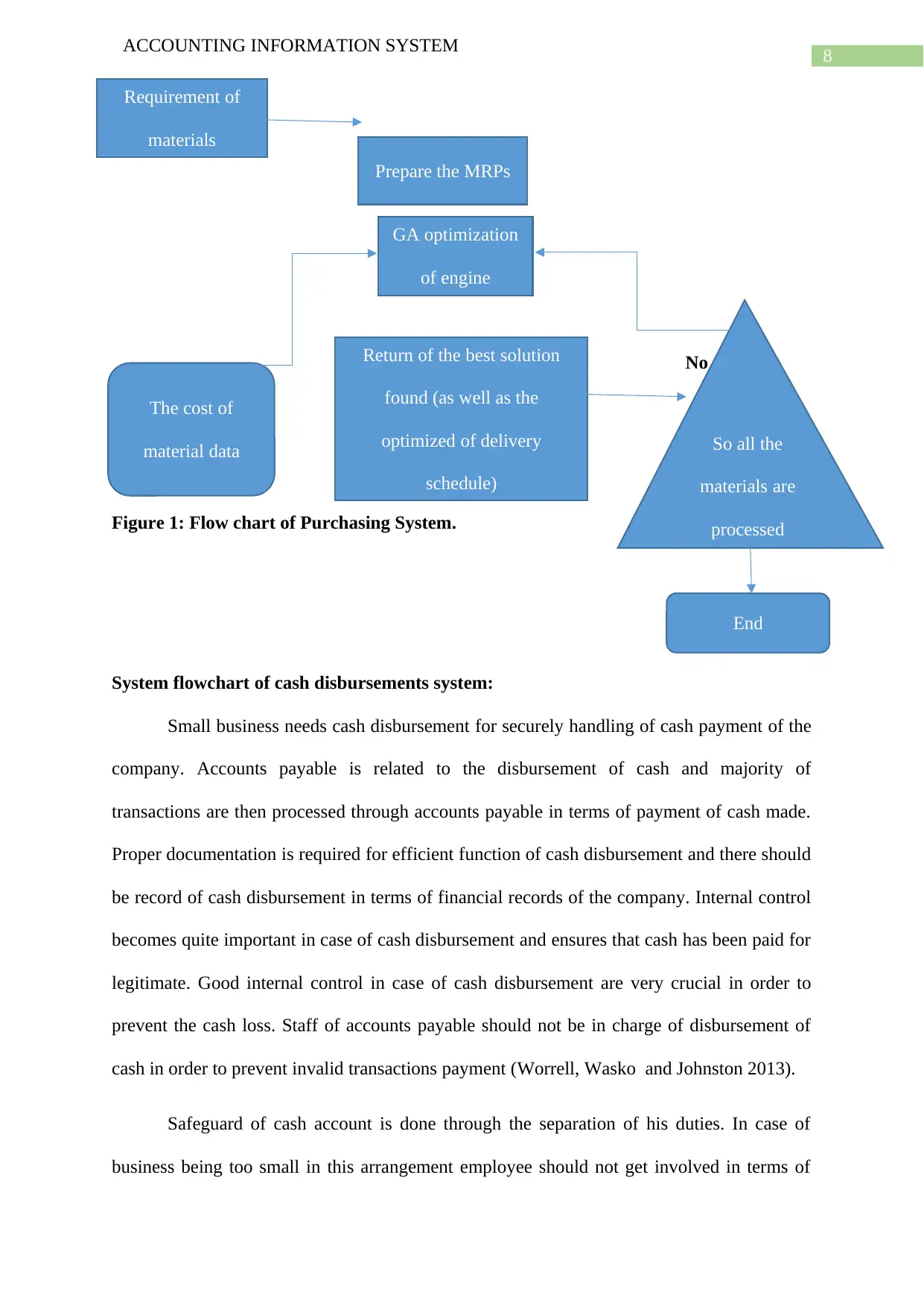

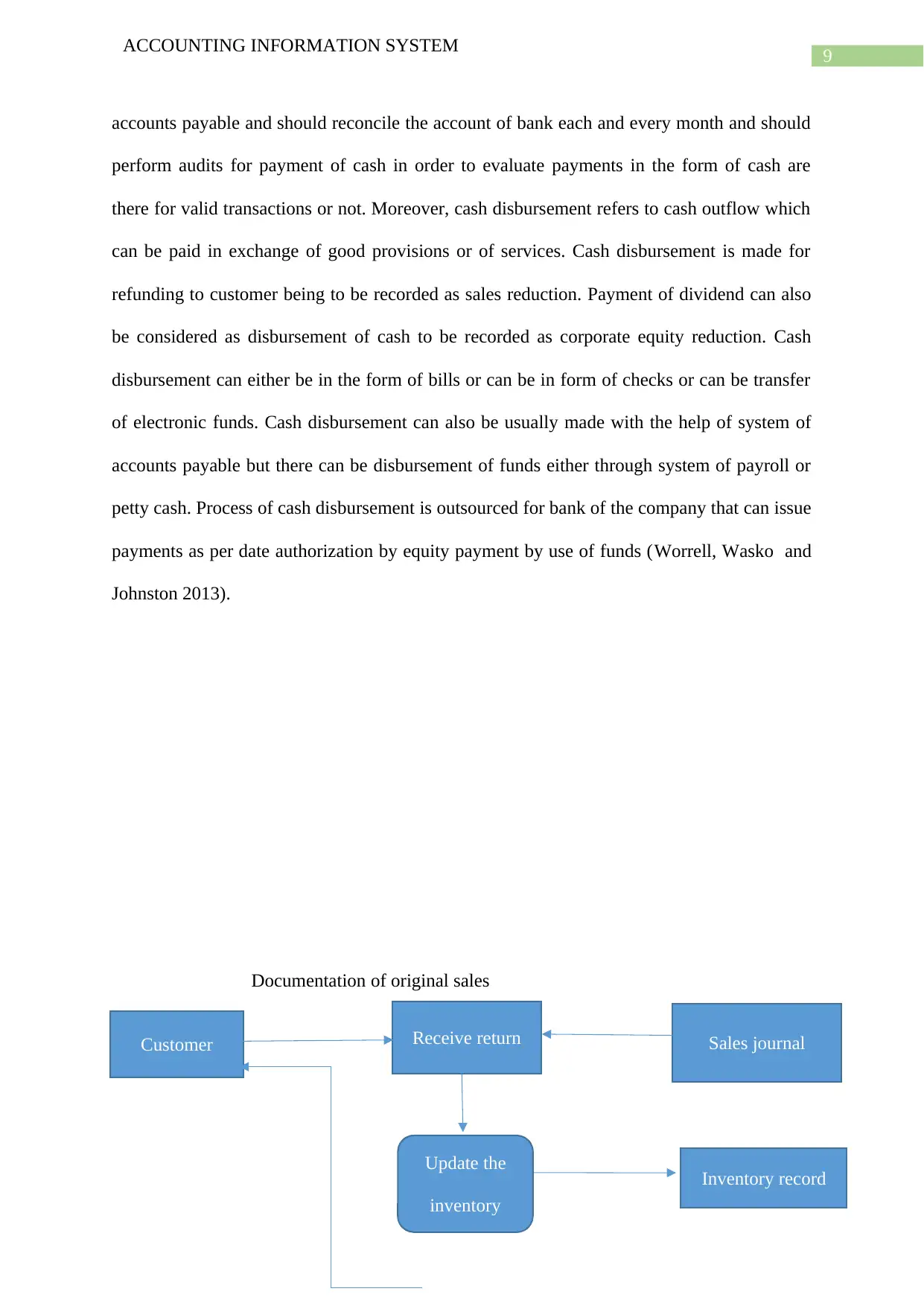

System flowchart of cash disbursements system:

Small business needs cash disbursement for securely handling of cash payment of the

company. Accounts payable is related to the disbursement of cash and majority of

transactions are then processed through accounts payable in terms of payment of cash made.

Proper documentation is required for efficient function of cash disbursement and there should

be record of cash disbursement in terms of financial records of the company. Internal control

becomes quite important in case of cash disbursement and ensures that cash has been paid for

legitimate. Good internal control in case of cash disbursement are very crucial in order to

prevent the cash loss. Staff of accounts payable should not be in charge of disbursement of

cash in order to prevent invalid transactions payment (Worrell, Wasko and Johnston 2013).

Safeguard of cash account is done through the separation of his duties. In case of

business being too small in this arrangement employee should not get involved in terms of

Prepare the MRPs

GA optimization

of engine

Return of the best solution

found (as well as the

optimized of delivery

schedule)

Requirement of

materials

The cost of

material data So all the

materials are

processed

End

ACCOUNTING INFORMATION SYSTEM

No

yes

Figure 1: Flow chart of Purchasing System.

System flowchart of cash disbursements system:

Small business needs cash disbursement for securely handling of cash payment of the

company. Accounts payable is related to the disbursement of cash and majority of

transactions are then processed through accounts payable in terms of payment of cash made.

Proper documentation is required for efficient function of cash disbursement and there should

be record of cash disbursement in terms of financial records of the company. Internal control

becomes quite important in case of cash disbursement and ensures that cash has been paid for

legitimate. Good internal control in case of cash disbursement are very crucial in order to

prevent the cash loss. Staff of accounts payable should not be in charge of disbursement of

cash in order to prevent invalid transactions payment (Worrell, Wasko and Johnston 2013).

Safeguard of cash account is done through the separation of his duties. In case of

business being too small in this arrangement employee should not get involved in terms of

Prepare the MRPs

GA optimization

of engine

Return of the best solution

found (as well as the

optimized of delivery

schedule)

Requirement of

materials

The cost of

material data So all the

materials are

processed

End

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING INFORMATION SYSTEM

accounts payable and should reconcile the account of bank each and every month and should

perform audits for payment of cash in order to evaluate payments in the form of cash are

there for valid transactions or not. Moreover, cash disbursement refers to cash outflow which

can be paid in exchange of good provisions or of services. Cash disbursement is made for

refunding to customer being to be recorded as sales reduction. Payment of dividend can also

be considered as disbursement of cash to be recorded as corporate equity reduction. Cash

disbursement can either be in the form of bills or can be in form of checks or can be transfer

of electronic funds. Cash disbursement can also be usually made with the help of system of

accounts payable but there can be disbursement of funds either through system of payroll or

petty cash. Process of cash disbursement is outsourced for bank of the company that can issue

payments as per date authorization by equity payment by use of funds (Worrell, Wasko and

Johnston 2013).

Documentation of original sales

Receive return Sales journalCustomer

Update the

inventory

Inventory record

ACCOUNTING INFORMATION SYSTEM

accounts payable and should reconcile the account of bank each and every month and should

perform audits for payment of cash in order to evaluate payments in the form of cash are

there for valid transactions or not. Moreover, cash disbursement refers to cash outflow which

can be paid in exchange of good provisions or of services. Cash disbursement is made for

refunding to customer being to be recorded as sales reduction. Payment of dividend can also

be considered as disbursement of cash to be recorded as corporate equity reduction. Cash

disbursement can either be in the form of bills or can be in form of checks or can be transfer

of electronic funds. Cash disbursement can also be usually made with the help of system of

accounts payable but there can be disbursement of funds either through system of payroll or

petty cash. Process of cash disbursement is outsourced for bank of the company that can issue

payments as per date authorization by equity payment by use of funds (Worrell, Wasko and

Johnston 2013).

Documentation of original sales

Receive return Sales journalCustomer

Update the

inventory

Inventory record

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING INFORMATION SYSTEM

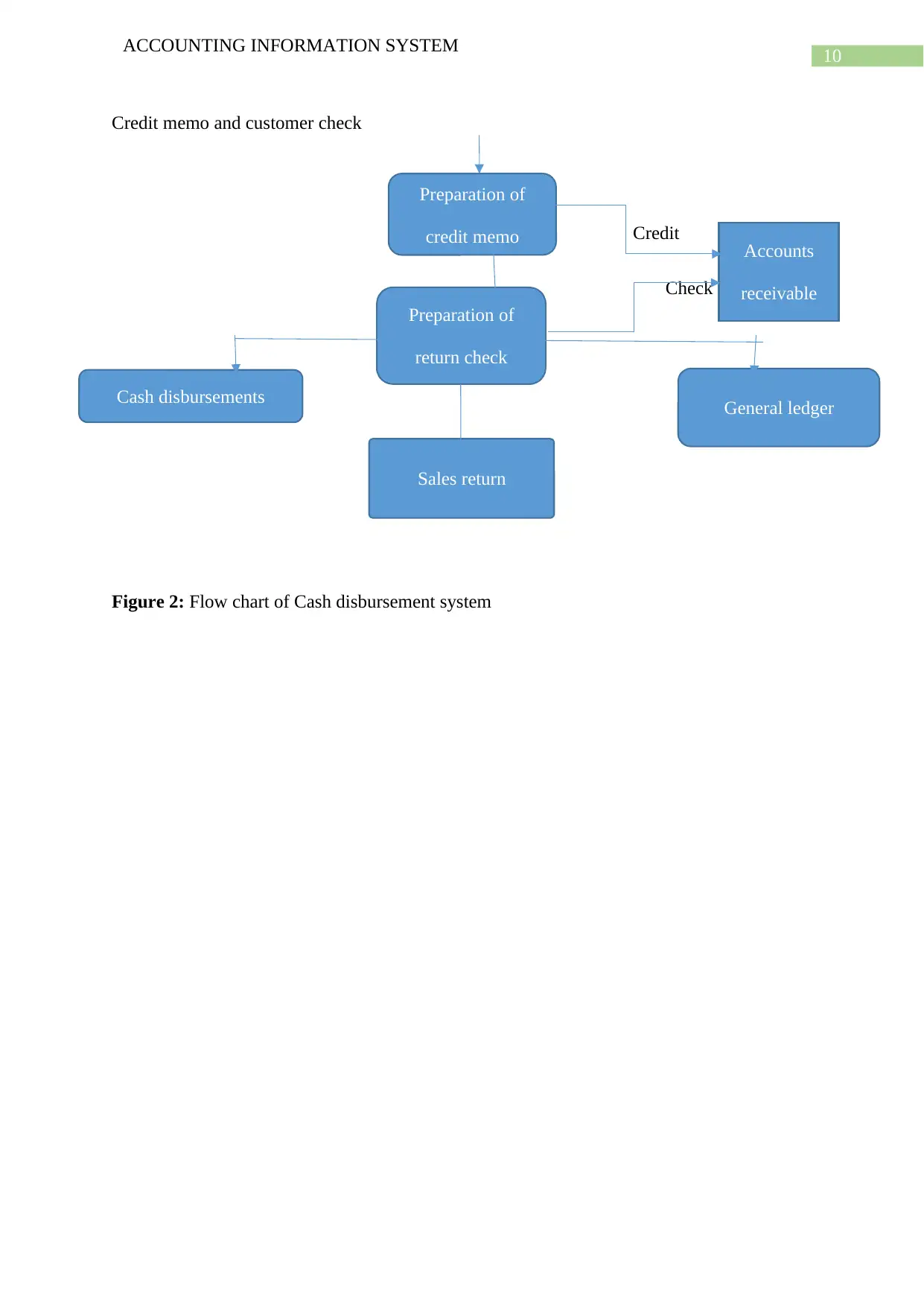

Credit memo and customer check

Credit

Check

Figure 2: Flow chart of Cash disbursement system

Preparation of

credit memo

Preparation of

return check

Cash disbursements

Sales return

General ledger

Accounts

receivable

ACCOUNTING INFORMATION SYSTEM

Credit memo and customer check

Credit

Check

Figure 2: Flow chart of Cash disbursement system

Preparation of

credit memo

Preparation of

return check

Cash disbursements

Sales return

General ledger

Accounts

receivable

11

ACCOUNTING INFORMATION SYSTEM

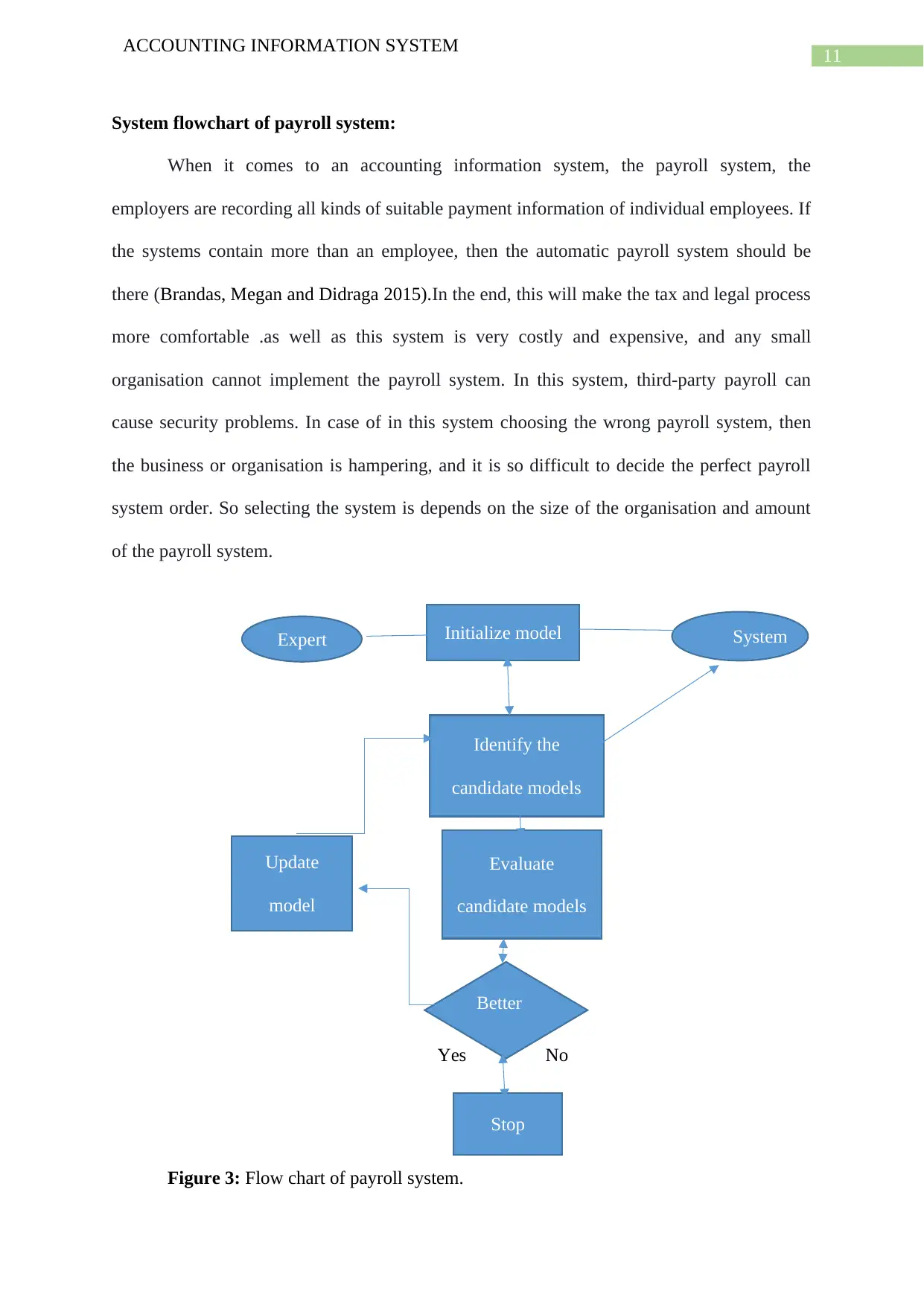

System flowchart of payroll system:

When it comes to an accounting information system, the payroll system, the

employers are recording all kinds of suitable payment information of individual employees. If

the systems contain more than an employee, then the automatic payroll system should be

there (Brandas, Megan and Didraga 2015).In the end, this will make the tax and legal process

more comfortable .as well as this system is very costly and expensive, and any small

organisation cannot implement the payroll system. In this system, third-party payroll can

cause security problems. In case of in this system choosing the wrong payroll system, then

the business or organisation is hampering, and it is so difficult to decide the perfect payroll

system order. So selecting the system is depends on the size of the organisation and amount

of the payroll system.

Yes No

Figure 3: Flow chart of payroll system.

Initialize model

Identify the

candidate models

Evaluate

candidate models

Better

candida

Stop

Update

model

Expert System

ACCOUNTING INFORMATION SYSTEM

System flowchart of payroll system:

When it comes to an accounting information system, the payroll system, the

employers are recording all kinds of suitable payment information of individual employees. If

the systems contain more than an employee, then the automatic payroll system should be

there (Brandas, Megan and Didraga 2015).In the end, this will make the tax and legal process

more comfortable .as well as this system is very costly and expensive, and any small

organisation cannot implement the payroll system. In this system, third-party payroll can

cause security problems. In case of in this system choosing the wrong payroll system, then

the business or organisation is hampering, and it is so difficult to decide the perfect payroll

system order. So selecting the system is depends on the size of the organisation and amount

of the payroll system.

Yes No

Figure 3: Flow chart of payroll system.

Initialize model

Identify the

candidate models

Evaluate

candidate models

Better

candida

Stop

Update

model

Expert System

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.