HA2042 T2 2019 Case Study: Accounting Information Systems at Adam & Co

VerifiedAdded on 2022/11/17

|15

|3054

|409

Case Study

AI Summary

This case study analyzes the accounting information systems of Adam & Co., focusing on purchases, cash disbursements, and payroll processes. It examines flowcharts for each system, identifying weaknesses such as inadequate segregation of duties, manual processes susceptible to errors, and lack of physical internal controls. The report highlights potential risks, including fraud, misallocation of funds, and data manipulation. It also discusses the limitations of the company's payroll system, emphasizing the need for improved timekeeping methods and automated processes. The analysis underscores the importance of robust internal controls and suggests improvements to mitigate risks and enhance efficiency within the company's financial operations. The report is intended for the management of Adam & Co to highlight vulnerable areas of the company's accounting system that may need attention.

ACCOUNTING INFORMATION SYSTEMS 1

Processes, risks and internal controls

Student’s name

Course

Instructor’s name

Institutional affiliation

City and state

Date

Processes, risks and internal controls

Student’s name

Course

Instructor’s name

Institutional affiliation

City and state

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING INFORMATION SYSTEMS 2

Table of Contents

Executive summary.........................................................................................................................3

Introduction......................................................................................................................................3

The purchases flowchart system......................................................................................................4

Purchase flowchart weaknesses.......................................................................................................5

Cash disbursement flow chart..........................................................................................................6

The potential risk associated with the company cash disbursement system...................................7

Payroll system flow chart................................................................................................................9

The weaknesses of the Adam and company payroll system..........................................................10

Other internal control weakness of the within the company.........................................................10

Conclusion.....................................................................................................................................11

Table of Contents

Executive summary.........................................................................................................................3

Introduction......................................................................................................................................3

The purchases flowchart system......................................................................................................4

Purchase flowchart weaknesses.......................................................................................................5

Cash disbursement flow chart..........................................................................................................6

The potential risk associated with the company cash disbursement system...................................7

Payroll system flow chart................................................................................................................9

The weaknesses of the Adam and company payroll system..........................................................10

Other internal control weakness of the within the company.........................................................10

Conclusion.....................................................................................................................................11

ACCOUNTING INFORMATION SYSTEMS 3

Executive summary

The information provided in this short report is an assessment of the accounting

information systems, regarding the risks, internal controls, weaknesses together with the different

information flow charts. The report is specifically addressed to the management of Adam and

company. The report is therefore in an to attempt to identify the possible vulnerable areas that

are present to the company that may require attention. The report covers the point of interest in

about four aspects of the accounting system information of the company. These include the

purchases system, cash disbursements, payroll and description of the internal control weaknesses

and risks associated with such weaknesses.

Introduction

Globally, there is an increasing rate of demand for efficiency effectiveness of preparing,

recording and presentation of financial data within the organizations. It is due to such demands

that business has come with a series of internal control measures to achieve such an objective.

These control measures are classified into several ways depending on the organizational goals

and objectives. For such reasons, accounting information systems have been part of the changing

trends in ensuring efficiency and effectiveness. An accounting information system can, therefore,

be defined as an internal control tool or structure that a business entity puts in place to ensure

that all financial activities are carried out most appropriately. This system involves components

such as the purchases control system, the payroll and cash disbursement system as further

discussed below:

Executive summary

The information provided in this short report is an assessment of the accounting

information systems, regarding the risks, internal controls, weaknesses together with the different

information flow charts. The report is specifically addressed to the management of Adam and

company. The report is therefore in an to attempt to identify the possible vulnerable areas that

are present to the company that may require attention. The report covers the point of interest in

about four aspects of the accounting system information of the company. These include the

purchases system, cash disbursements, payroll and description of the internal control weaknesses

and risks associated with such weaknesses.

Introduction

Globally, there is an increasing rate of demand for efficiency effectiveness of preparing,

recording and presentation of financial data within the organizations. It is due to such demands

that business has come with a series of internal control measures to achieve such an objective.

These control measures are classified into several ways depending on the organizational goals

and objectives. For such reasons, accounting information systems have been part of the changing

trends in ensuring efficiency and effectiveness. An accounting information system can, therefore,

be defined as an internal control tool or structure that a business entity puts in place to ensure

that all financial activities are carried out most appropriately. This system involves components

such as the purchases control system, the payroll and cash disbursement system as further

discussed below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING INFORMATION SYSTEMS 4

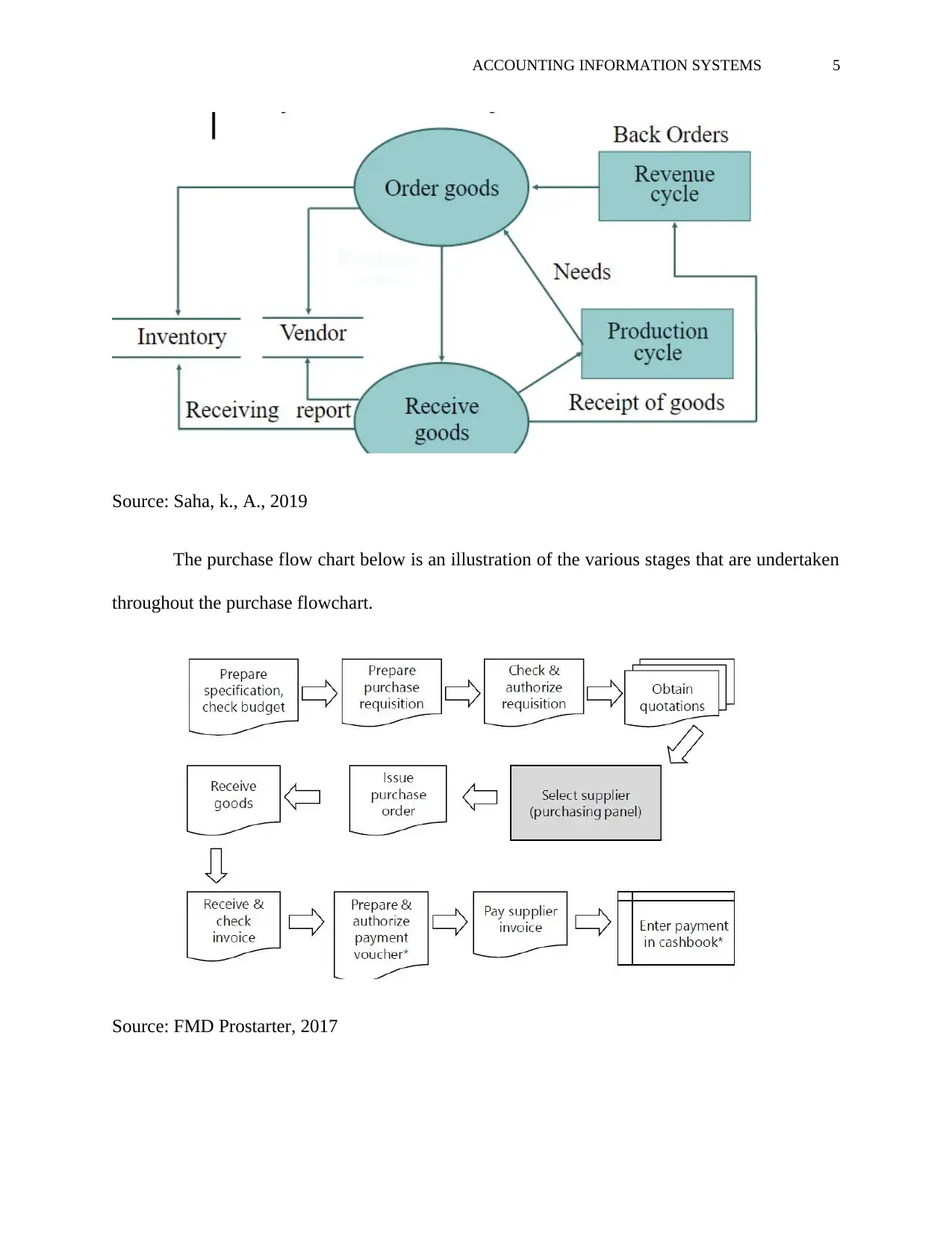

The purchases flowchart system

The purchase flow chart refers to the various steps and stages that a company undertakes

when procuring or purchasing materials, stock or inventories that are used to carry out daily

operations of the business. The purchase flow chart system is a cycle of events that are carried

out by different personnel or individuals (Mitrenfinch, 2019). Additionally, the purchase

flowchart system is carried in about nine stages or processes. The very first step in the system is

need recognition and the last stage, therefore, needs satisfaction. When the need arises in the

organization or department, a requisition note is prepared which then has to be authorized. The

next step is obtaining quotations. From the quotations stage a suitable supplier is then selected

which s followed by issuing a purchase order and delivery is made. When goods are delivered,

inspection is carried out to verify the specifications. If all the items are in good condition,

payment is authorized to the supplier and the last stage is recording the purchase in the books of

accounts. This cycle expenditure cycle takes place on a continuous process.

Expenditure cycle

1. Placing orders of the goods, services and or supplies

2. Receiving the items ordered

3. Making payment for the items.

The purchases flowchart system

The purchase flow chart refers to the various steps and stages that a company undertakes

when procuring or purchasing materials, stock or inventories that are used to carry out daily

operations of the business. The purchase flow chart system is a cycle of events that are carried

out by different personnel or individuals (Mitrenfinch, 2019). Additionally, the purchase

flowchart system is carried in about nine stages or processes. The very first step in the system is

need recognition and the last stage, therefore, needs satisfaction. When the need arises in the

organization or department, a requisition note is prepared which then has to be authorized. The

next step is obtaining quotations. From the quotations stage a suitable supplier is then selected

which s followed by issuing a purchase order and delivery is made. When goods are delivered,

inspection is carried out to verify the specifications. If all the items are in good condition,

payment is authorized to the supplier and the last stage is recording the purchase in the books of

accounts. This cycle expenditure cycle takes place on a continuous process.

Expenditure cycle

1. Placing orders of the goods, services and or supplies

2. Receiving the items ordered

3. Making payment for the items.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING INFORMATION SYSTEMS 5

Source: Saha, k., A., 2019

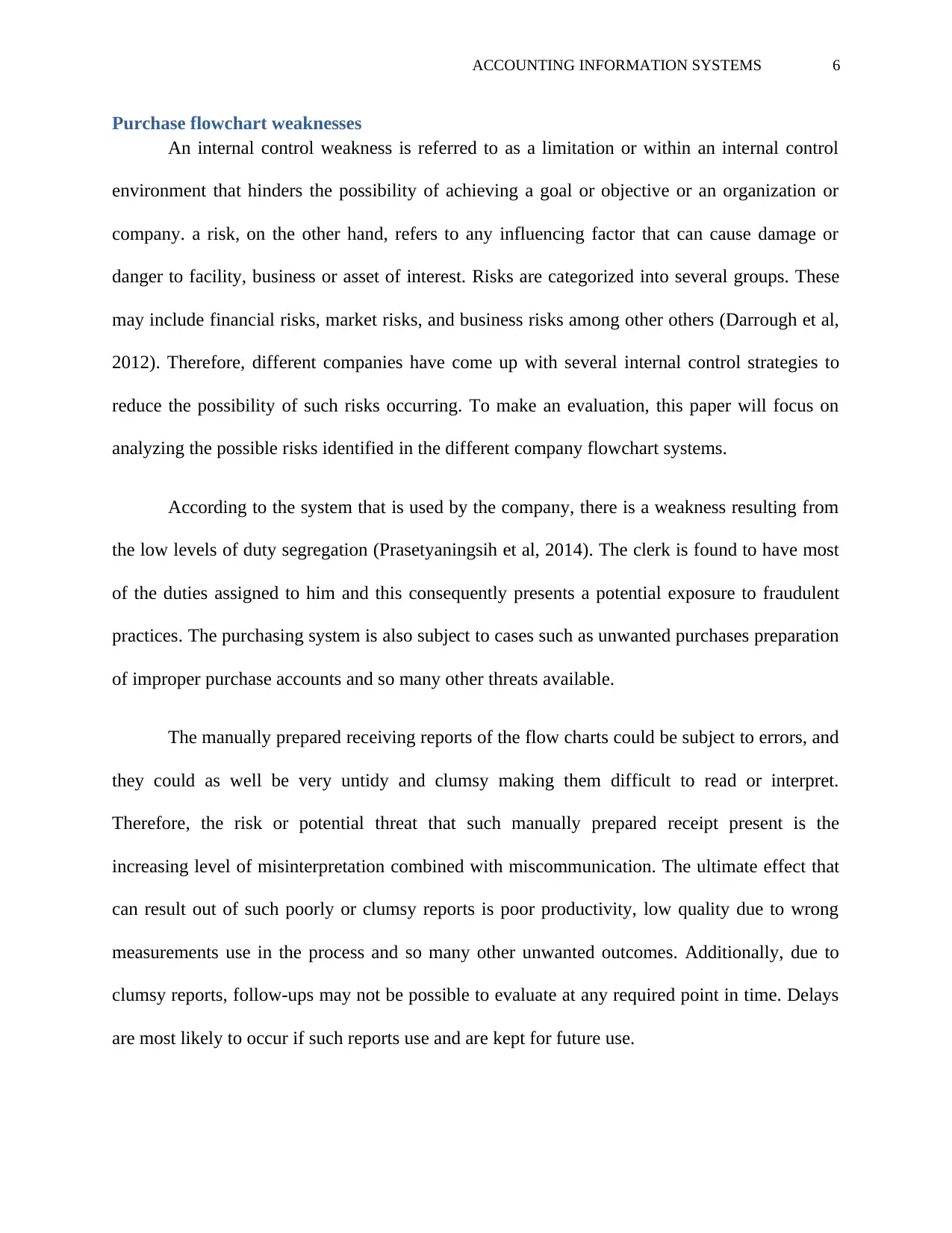

The purchase flow chart below is an illustration of the various stages that are undertaken

throughout the purchase flowchart.

Source: FMD Prostarter, 2017

Source: Saha, k., A., 2019

The purchase flow chart below is an illustration of the various stages that are undertaken

throughout the purchase flowchart.

Source: FMD Prostarter, 2017

ACCOUNTING INFORMATION SYSTEMS 6

Purchase flowchart weaknesses

An internal control weakness is referred to as a limitation or within an internal control

environment that hinders the possibility of achieving a goal or objective or an organization or

company. a risk, on the other hand, refers to any influencing factor that can cause damage or

danger to facility, business or asset of interest. Risks are categorized into several groups. These

may include financial risks, market risks, and business risks among other others (Darrough et al,

2012). Therefore, different companies have come up with several internal control strategies to

reduce the possibility of such risks occurring. To make an evaluation, this paper will focus on

analyzing the possible risks identified in the different company flowchart systems.

According to the system that is used by the company, there is a weakness resulting from

the low levels of duty segregation (Prasetyaningsih et al, 2014). The clerk is found to have most

of the duties assigned to him and this consequently presents a potential exposure to fraudulent

practices. The purchasing system is also subject to cases such as unwanted purchases preparation

of improper purchase accounts and so many other threats available.

The manually prepared receiving reports of the flow charts could be subject to errors, and

they could as well be very untidy and clumsy making them difficult to read or interpret.

Therefore, the risk or potential threat that such manually prepared receipt present is the

increasing level of misinterpretation combined with miscommunication. The ultimate effect that

can result out of such poorly or clumsy reports is poor productivity, low quality due to wrong

measurements use in the process and so many other unwanted outcomes. Additionally, due to

clumsy reports, follow-ups may not be possible to evaluate at any required point in time. Delays

are most likely to occur if such reports use and are kept for future use.

Purchase flowchart weaknesses

An internal control weakness is referred to as a limitation or within an internal control

environment that hinders the possibility of achieving a goal or objective or an organization or

company. a risk, on the other hand, refers to any influencing factor that can cause damage or

danger to facility, business or asset of interest. Risks are categorized into several groups. These

may include financial risks, market risks, and business risks among other others (Darrough et al,

2012). Therefore, different companies have come up with several internal control strategies to

reduce the possibility of such risks occurring. To make an evaluation, this paper will focus on

analyzing the possible risks identified in the different company flowchart systems.

According to the system that is used by the company, there is a weakness resulting from

the low levels of duty segregation (Prasetyaningsih et al, 2014). The clerk is found to have most

of the duties assigned to him and this consequently presents a potential exposure to fraudulent

practices. The purchasing system is also subject to cases such as unwanted purchases preparation

of improper purchase accounts and so many other threats available.

The manually prepared receiving reports of the flow charts could be subject to errors, and

they could as well be very untidy and clumsy making them difficult to read or interpret.

Therefore, the risk or potential threat that such manually prepared receipt present is the

increasing level of misinterpretation combined with miscommunication. The ultimate effect that

can result out of such poorly or clumsy reports is poor productivity, low quality due to wrong

measurements use in the process and so many other unwanted outcomes. Additionally, due to

clumsy reports, follow-ups may not be possible to evaluate at any required point in time. Delays

are most likely to occur if such reports use and are kept for future use.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING INFORMATION SYSTEMS 7

According to the effective and efficient internal control environment requires that duties

of the organization should be separated. This implies that no single individual or person has the

liberty or mandate to carry out all activities as one (Crouthamel, 2013). However, at Adam and

company, this is rather the opposite. From the information that is provided, that purchasing clerk

is the only person who can determine how much stock should be purchased, which vendor

should supply and it is still the same person who determines when to purchase. All such duties

are not in line with the requirements of an effective internal control system. Consequently, the

company stands to be significantly exposed to threats and risks resulting from fraud, poor quality

material purchases, and so many other risks that are associated with low levels of duty

distribution.

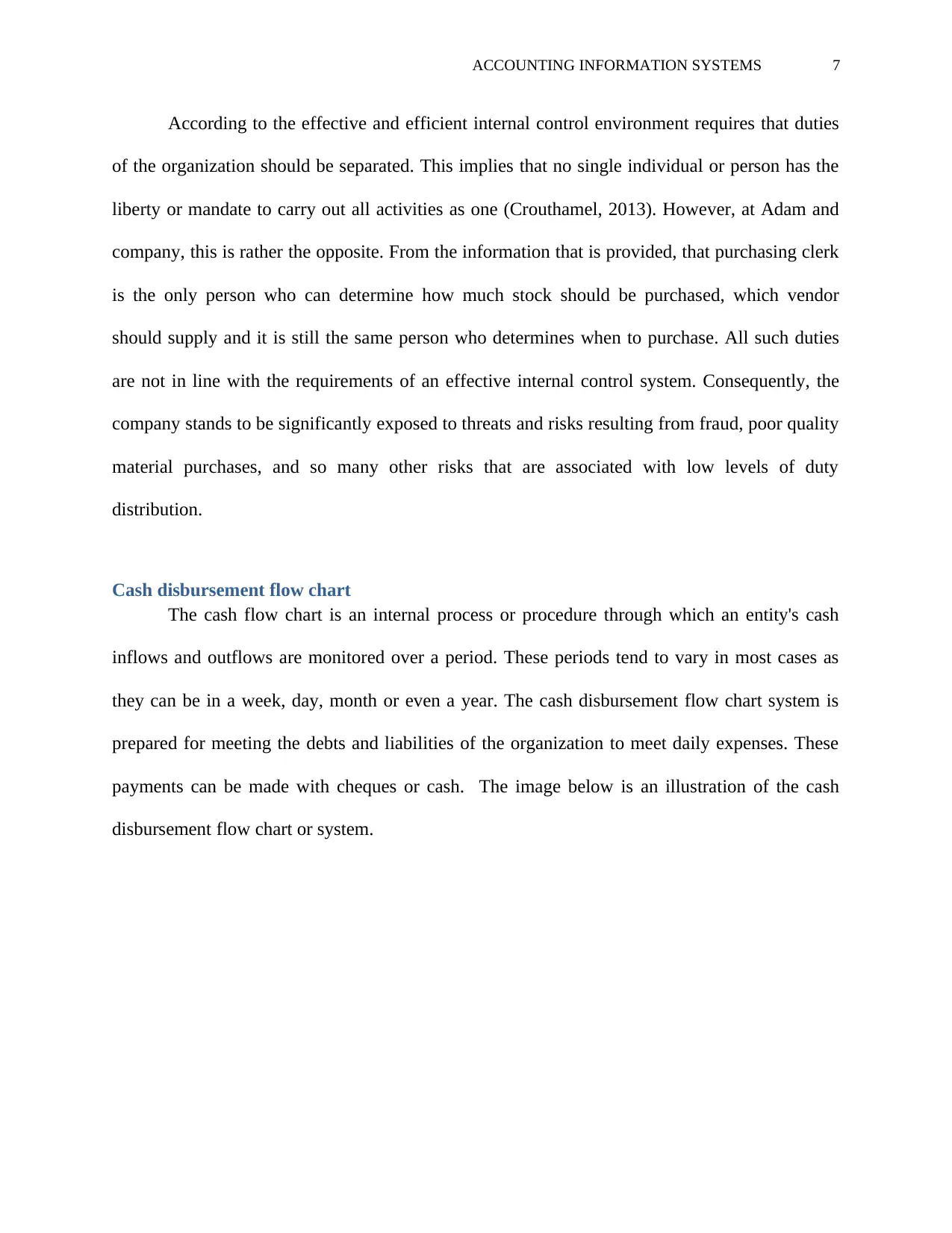

Cash disbursement flow chart

The cash flow chart is an internal process or procedure through which an entity's cash

inflows and outflows are monitored over a period. These periods tend to vary in most cases as

they can be in a week, day, month or even a year. The cash disbursement flow chart system is

prepared for meeting the debts and liabilities of the organization to meet daily expenses. These

payments can be made with cheques or cash. The image below is an illustration of the cash

disbursement flow chart or system.

According to the effective and efficient internal control environment requires that duties

of the organization should be separated. This implies that no single individual or person has the

liberty or mandate to carry out all activities as one (Crouthamel, 2013). However, at Adam and

company, this is rather the opposite. From the information that is provided, that purchasing clerk

is the only person who can determine how much stock should be purchased, which vendor

should supply and it is still the same person who determines when to purchase. All such duties

are not in line with the requirements of an effective internal control system. Consequently, the

company stands to be significantly exposed to threats and risks resulting from fraud, poor quality

material purchases, and so many other risks that are associated with low levels of duty

distribution.

Cash disbursement flow chart

The cash flow chart is an internal process or procedure through which an entity's cash

inflows and outflows are monitored over a period. These periods tend to vary in most cases as

they can be in a week, day, month or even a year. The cash disbursement flow chart system is

prepared for meeting the debts and liabilities of the organization to meet daily expenses. These

payments can be made with cheques or cash. The image below is an illustration of the cash

disbursement flow chart or system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING INFORMATION SYSTEMS 8

Source: vishekbatra, 2019

The potential risk associated with the company cash disbursement system

An entity that has all its cash and funds managed by individuals is at high risk of losing financial

resources and perhaps is the management of the cash resource. At times the financial manager is

limited by various unethical practices such as theft, fraud and misallocation of funds, therefore,

having the individuals controlling the cash accounts of the company such as Adam Company is a

threat to company funds (Beasley, 2019). The internal control system of the company s still very

inadequate since it is only the clerk and the treasurers who have access to most of the company

accounts such as the purchases ad cash disbursements system. This is however not ideal because

it gives these individual the liberty to carry out activities without any supervision. The system of

the company does not have provision for any periodic reconciliation of the different accounts.

This combined with the manual handling of the cash resources further weakens the internal

control within the organization.

Source: vishekbatra, 2019

The potential risk associated with the company cash disbursement system

An entity that has all its cash and funds managed by individuals is at high risk of losing financial

resources and perhaps is the management of the cash resource. At times the financial manager is

limited by various unethical practices such as theft, fraud and misallocation of funds, therefore,

having the individuals controlling the cash accounts of the company such as Adam Company is a

threat to company funds (Beasley, 2019). The internal control system of the company s still very

inadequate since it is only the clerk and the treasurers who have access to most of the company

accounts such as the purchases ad cash disbursements system. This is however not ideal because

it gives these individual the liberty to carry out activities without any supervision. The system of

the company does not have provision for any periodic reconciliation of the different accounts.

This combined with the manual handling of the cash resources further weakens the internal

control within the organization.

ACCOUNTING INFORMATION SYSTEMS 9

The cash disbursement system is that is used at Adam and company is highly manual. Although

this type of system has its associated advantages, it is critically under potential and significant

threats. For instance, at the company receipts of payment are manually stored and kept within

the company premises (Indico, 2015). The risk of such an accounting system is that critical

information is extensively subjected to manipulation, loss through fire outbreaks and any other

damage. If such important records are lost in a fire outbreak, the company could suffer

significant financial losses.

The other alternative risk that is present to the company is related to the significance of errors in

financial data entry. Because the systems of the company are operated manually, the possibility

of recording wrong amounts and failure to follow the double-entry principles of accounting are

high. Humans make mistake daily and having an accounting system that solely depends on

human knowledge could lead to significant losses (Bowers, 2017).

Since the company does not have any person to review or approve the cash transaction and

movements, this as well presents an internal control weakness. Reviews on activities such as

purchase orders payroll systems need to be carried out to ensure that all the transactions are

genuine and material necessary (Salin et al, 2018). On the contrary, however, the Adam and

company limited do not have such personnel in place to assess and evaluate or eve authorize the

different transactions that are carried conducted throughout the business. This weakness in the

company system presents a likelihood of paying to incur improper charges on purchases, making

payments for items that have not been delivered to business and so many other consequences of

the sort.

The cash disbursement system is that is used at Adam and company is highly manual. Although

this type of system has its associated advantages, it is critically under potential and significant

threats. For instance, at the company receipts of payment are manually stored and kept within

the company premises (Indico, 2015). The risk of such an accounting system is that critical

information is extensively subjected to manipulation, loss through fire outbreaks and any other

damage. If such important records are lost in a fire outbreak, the company could suffer

significant financial losses.

The other alternative risk that is present to the company is related to the significance of errors in

financial data entry. Because the systems of the company are operated manually, the possibility

of recording wrong amounts and failure to follow the double-entry principles of accounting are

high. Humans make mistake daily and having an accounting system that solely depends on

human knowledge could lead to significant losses (Bowers, 2017).

Since the company does not have any person to review or approve the cash transaction and

movements, this as well presents an internal control weakness. Reviews on activities such as

purchase orders payroll systems need to be carried out to ensure that all the transactions are

genuine and material necessary (Salin et al, 2018). On the contrary, however, the Adam and

company limited do not have such personnel in place to assess and evaluate or eve authorize the

different transactions that are carried conducted throughout the business. This weakness in the

company system presents a likelihood of paying to incur improper charges on purchases, making

payments for items that have not been delivered to business and so many other consequences of

the sort.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING INFORMATION SYSTEMS 10

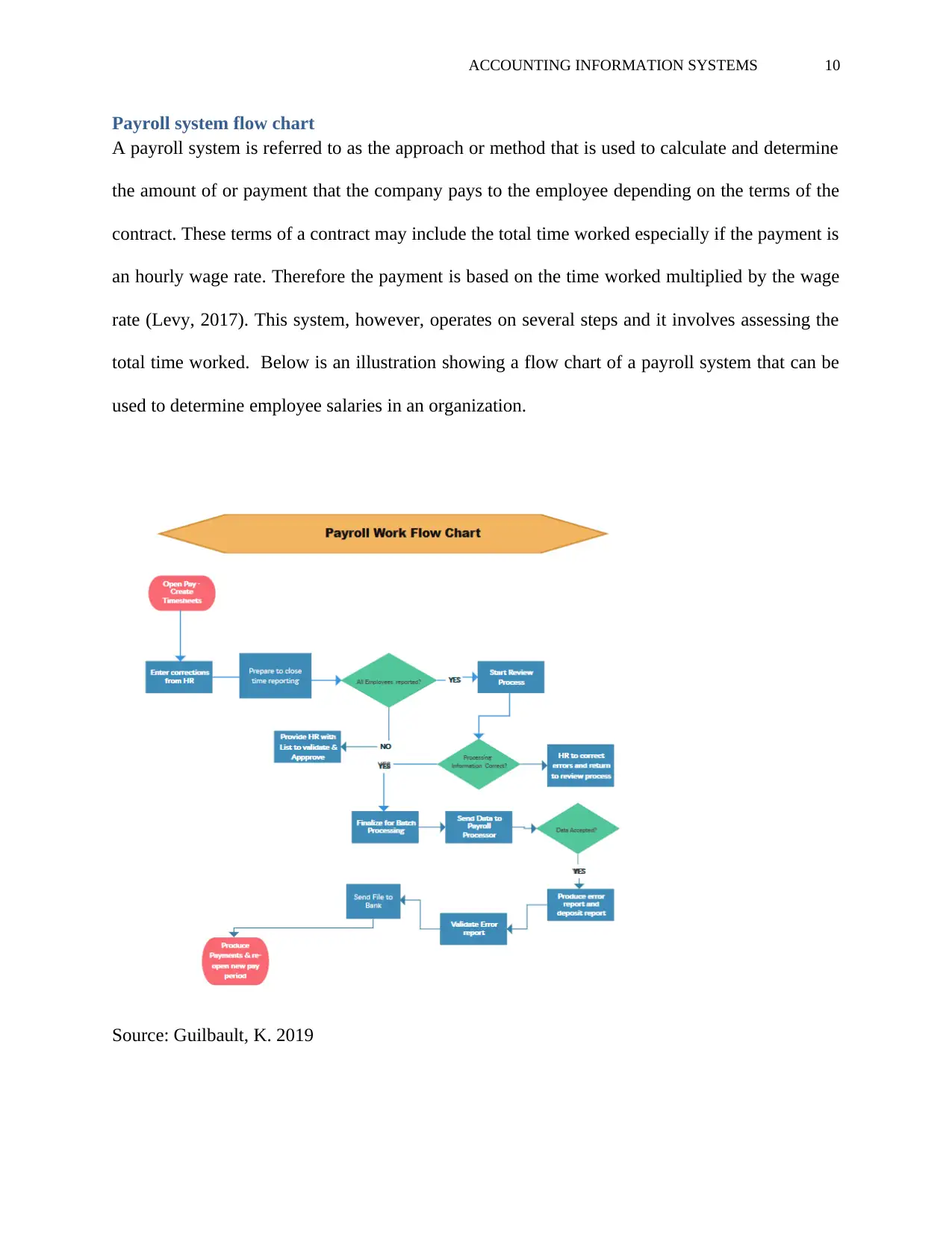

Payroll system flow chart

A payroll system is referred to as the approach or method that is used to calculate and determine

the amount of or payment that the company pays to the employee depending on the terms of the

contract. These terms of a contract may include the total time worked especially if the payment is

an hourly wage rate. Therefore the payment is based on the time worked multiplied by the wage

rate (Levy, 2017). This system, however, operates on several steps and it involves assessing the

total time worked. Below is an illustration showing a flow chart of a payroll system that can be

used to determine employee salaries in an organization.

Source: Guilbault, K. 2019

Payroll system flow chart

A payroll system is referred to as the approach or method that is used to calculate and determine

the amount of or payment that the company pays to the employee depending on the terms of the

contract. These terms of a contract may include the total time worked especially if the payment is

an hourly wage rate. Therefore the payment is based on the time worked multiplied by the wage

rate (Levy, 2017). This system, however, operates on several steps and it involves assessing the

total time worked. Below is an illustration showing a flow chart of a payroll system that can be

used to determine employee salaries in an organization.

Source: Guilbault, K. 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING INFORMATION SYSTEMS 11

The weaknesses of the Adam and company payroll system

The traditional process of analyzing and assessing the total time worked by employees has been

challenged by the increasing rate of inefficiency for the past periods. Therefore is due to such

limitations associated with the traditional methods such time cards that have created the need for

more sophisticated techniques and equipment to keep roper records concerning the time worked

by an individual (Nashwan,2018). However, the payroll system at Adam and company is still

under significant threats (Lai et al, 2017). The traditional time cards that are fully operated by

manual standards are highly exposed to manipulation. There is a huge and significant potential of

exposure because of the different personnel can easily and freely alter the reporting time and

consequently, this means that management will have pay wages for hours that are not worked for

(Al-Sharairi et al, 2018).

Secondly, the system of that is used at Adam and company is very manual and it involves

numerous procedures to accomplish (Akwas-sekyi and Gene, 2016). The challenge or weakness

width such a system is that it is very time consuming and delays are very inevitable. Transactions

tend to take a lot of time to process thereby resulting in time wastage a scenario that leads to

inefficiency and reduced productivity (Agbenyo et al, 2018). For instance, employees may often

get themselves waiting for very long periods just to register their arrival or departure from work.

Other internal control weakness of the within the company

Adam and company limited does not in any way reflect the presence of physical internal controls

in the system (Monisola and Rekiat, 2016). This is adversely among the weak points of the

company that need to be addressed with huge interest and seriousness. Without the physical

controls to guard and protect the company assets and purchases, there is a high likelihood that

The weaknesses of the Adam and company payroll system

The traditional process of analyzing and assessing the total time worked by employees has been

challenged by the increasing rate of inefficiency for the past periods. Therefore is due to such

limitations associated with the traditional methods such time cards that have created the need for

more sophisticated techniques and equipment to keep roper records concerning the time worked

by an individual (Nashwan,2018). However, the payroll system at Adam and company is still

under significant threats (Lai et al, 2017). The traditional time cards that are fully operated by

manual standards are highly exposed to manipulation. There is a huge and significant potential of

exposure because of the different personnel can easily and freely alter the reporting time and

consequently, this means that management will have pay wages for hours that are not worked for

(Al-Sharairi et al, 2018).

Secondly, the system of that is used at Adam and company is very manual and it involves

numerous procedures to accomplish (Akwas-sekyi and Gene, 2016). The challenge or weakness

width such a system is that it is very time consuming and delays are very inevitable. Transactions

tend to take a lot of time to process thereby resulting in time wastage a scenario that leads to

inefficiency and reduced productivity (Agbenyo et al, 2018). For instance, employees may often

get themselves waiting for very long periods just to register their arrival or departure from work.

Other internal control weakness of the within the company

Adam and company limited does not in any way reflect the presence of physical internal controls

in the system (Monisola and Rekiat, 2016). This is adversely among the weak points of the

company that need to be addressed with huge interest and seriousness. Without the physical

controls to guard and protect the company assets and purchases, there is a high likelihood that

ACCOUNTING INFORMATION SYSTEMS 12

losses are very inevitable. Such losses could arise out of thefts of company stock and other fixed

assets that are valuable to the entity.

Almost all of the systems of the company are operated on a manual basis. Starting for the hard

receipt payments, the clock cards, payment vouchers and so on are stored in the form of hard

copies. Such as system of operating requires large amounts of space to keep and such documents

in the long run (Mahadeen et al, 2016). Not only does this particular system subject important

information to threats such as theft but it also makes it hard to make corrections where necessary

if an error has been made in a transaction.

Conclusion

Conclusively, an effective and efficient internal control system is a vital requirement that each

and very active firm or business entity should possess. The level of profitability of performance

within any business organization or company is to some extent dependent upon efficiency and

effectiveness that results from activities such as resource utilization. The current and present

market trends that have introduced new technologies of management and internal controls that

are a more efficient and highly effective call for immediate organizational changes. Adam and

company limited should, therefore, revise the type of internal controls that are more efficient.

Systems such as the current manual systems of purchases flow chart, the time cards of used for

recording time worked are have over the years been phased out and they cannot sufficiently

facilitate effective operations.

losses are very inevitable. Such losses could arise out of thefts of company stock and other fixed

assets that are valuable to the entity.

Almost all of the systems of the company are operated on a manual basis. Starting for the hard

receipt payments, the clock cards, payment vouchers and so on are stored in the form of hard

copies. Such as system of operating requires large amounts of space to keep and such documents

in the long run (Mahadeen et al, 2016). Not only does this particular system subject important

information to threats such as theft but it also makes it hard to make corrections where necessary

if an error has been made in a transaction.

Conclusion

Conclusively, an effective and efficient internal control system is a vital requirement that each

and very active firm or business entity should possess. The level of profitability of performance

within any business organization or company is to some extent dependent upon efficiency and

effectiveness that results from activities such as resource utilization. The current and present

market trends that have introduced new technologies of management and internal controls that

are a more efficient and highly effective call for immediate organizational changes. Adam and

company limited should, therefore, revise the type of internal controls that are more efficient.

Systems such as the current manual systems of purchases flow chart, the time cards of used for

recording time worked are have over the years been phased out and they cannot sufficiently

facilitate effective operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.