Holmes Institute HA2042: Adam & Co Internal Control System Case Study

VerifiedAdded on 2022/11/14

|15

|2819

|50

Case Study

AI Summary

This case study examines the internal control system of Adam & Co, a Perth-based wholesaler. The analysis covers the company's purchase, cash disbursement, and payroll systems, including detailed flowcharts for each. The report identifies weaknesses within these systems, such as the lack of a dedicated purchase department, issues in the cash disbursement process (like missing pre-numbered cheques), and data manipulation in the payroll system. The study highlights the risks associated with these weaknesses, such as overstocking, potential fraud, and employee dissatisfaction. The assignment aims to provide a comprehensive understanding of the internal control system and its impact on the company's operations and financial stability.

Running head: INTERNAL CONTROL SYSTEM

Internal Control System

Name of the Student

Name of the University

Author note

Internal Control System

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

INTERNAL CONTROL SYSTEM

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Purchase system.........................................................................................................................3

Cash disbursement system.........................................................................................................5

Payroll system............................................................................................................................6

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

INTERNAL CONTROL SYSTEM

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Purchase system.........................................................................................................................3

Cash disbursement system.........................................................................................................5

Payroll system............................................................................................................................6

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

2

INTERNAL CONTROL SYSTEM

Executive summary

The aim of the report is to give brief explanation of the flowchart of the purchase, cash

disbursement and payroll system of the company. The report further explains the weakness

that the company has in the flow of the expenditure cycle. In conclusion the weakness of the

internal control system and the risks due to such weakness has been explained in brief.

INTERNAL CONTROL SYSTEM

Executive summary

The aim of the report is to give brief explanation of the flowchart of the purchase, cash

disbursement and payroll system of the company. The report further explains the weakness

that the company has in the flow of the expenditure cycle. In conclusion the weakness of the

internal control system and the risks due to such weakness has been explained in brief.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

INTERNAL CONTROL SYSTEM

Introduction

The report contains a brief impression of the internal control system of Adam and co a

Perth grounded wholesaler of supplies. Adam & co bases its inventories from manufacturers

in china, Thailand and the accounting system of the company is centralized for which it

become easy for the company to maintain a control system in order to control the affairs of

the company effectively. The company used an effective expenditure cycle procedure by

which it is possible for the organization to monitor all the business transactions and

implement a cost control method so that all the optimal usage of the resources is possible.

The entire expenditure cycle is arranged in such a way that it is possible for Adam & co to

reduce the cost and increase the profitability.

Discussion

The entire expenditure cycle of the company is classified in to three system the

purchase system, a cash disbursement system and the payroll system. The internal control

system of the company is well planned and the strategy of Adam & co is to maintain a steady

growth rate through the application of the efficiency of its expenditure cycle. The entire flow

of the expenditure of the company is explained below

Purchase system

Purchase is the first step from which the activity of the business starts. The company

give emphasis on the purchase of the best quality product from the market in order to ensure

customer satisfaction. Purchase is the most important part of the business activity as all the

activity of the business is directly related with the quality and quantity of the raw materials

purchased to produce the specific product that the organization desires to produce and sell in

the market. So, Adam & co take all necessary steps to ensure that the process of purchasing

INTERNAL CONTROL SYSTEM

Introduction

The report contains a brief impression of the internal control system of Adam and co a

Perth grounded wholesaler of supplies. Adam & co bases its inventories from manufacturers

in china, Thailand and the accounting system of the company is centralized for which it

become easy for the company to maintain a control system in order to control the affairs of

the company effectively. The company used an effective expenditure cycle procedure by

which it is possible for the organization to monitor all the business transactions and

implement a cost control method so that all the optimal usage of the resources is possible.

The entire expenditure cycle is arranged in such a way that it is possible for Adam & co to

reduce the cost and increase the profitability.

Discussion

The entire expenditure cycle of the company is classified in to three system the

purchase system, a cash disbursement system and the payroll system. The internal control

system of the company is well planned and the strategy of Adam & co is to maintain a steady

growth rate through the application of the efficiency of its expenditure cycle. The entire flow

of the expenditure of the company is explained below

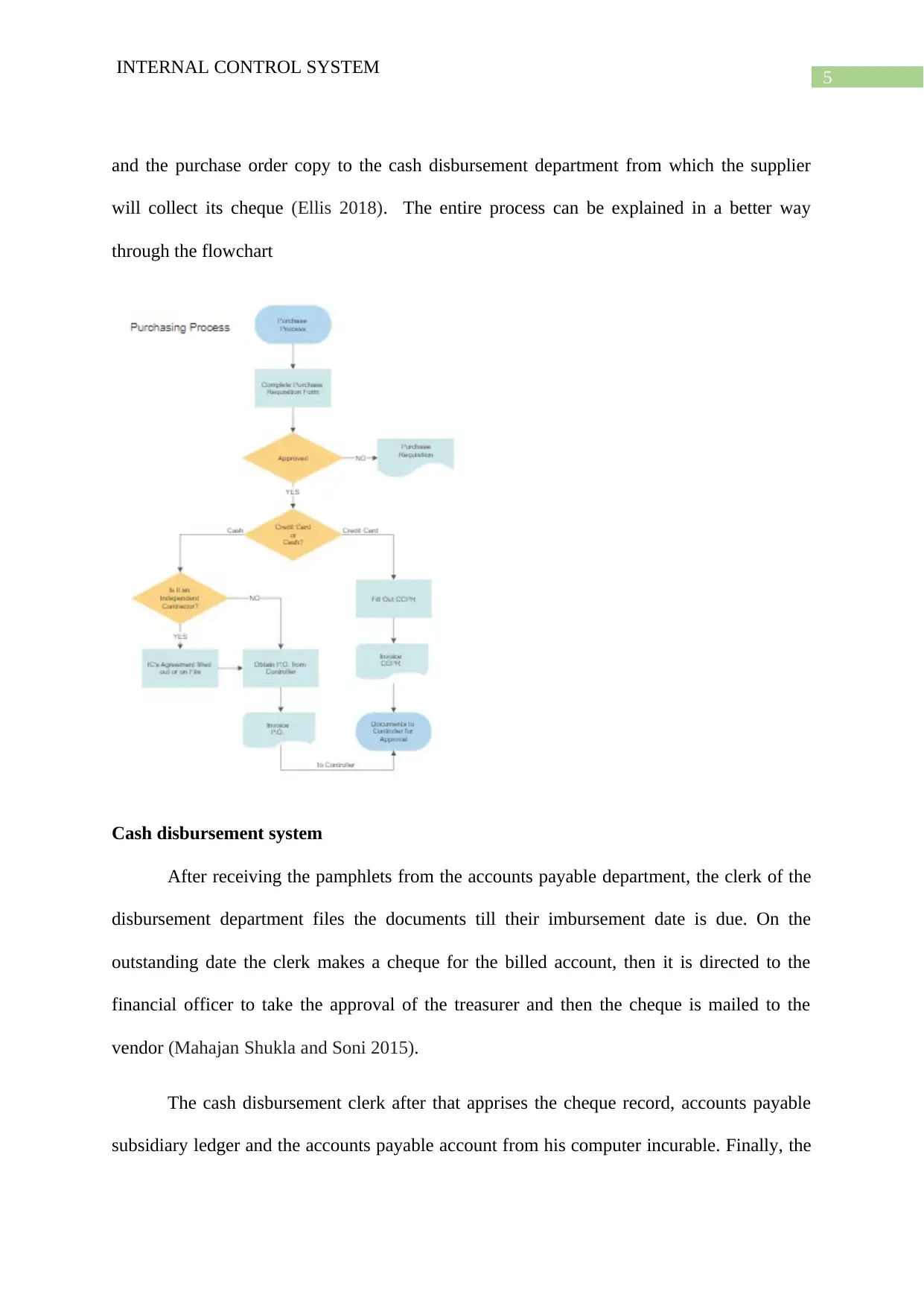

Purchase system

Purchase is the first step from which the activity of the business starts. The company

give emphasis on the purchase of the best quality product from the market in order to ensure

customer satisfaction. Purchase is the most important part of the business activity as all the

activity of the business is directly related with the quality and quantity of the raw materials

purchased to produce the specific product that the organization desires to produce and sell in

the market. So, Adam & co take all necessary steps to ensure that the process of purchasing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

INTERNAL CONTROL SYSTEM

the raw materials does not have any loopholes for which the supply process of the company

does not have to suffer. The process of the purchase starts with the checking of the inventory

subsidiary ledger which is done by the purchasing clerk on a regular basis on the early

morning when the goods arrived. if the clerk finds the quantity of any specific item is too low

in that case the clerk immediately chooses a seller from the wholesaler file and makes a

digital purchase order. The clerk prints hard copies from which one copy is sent to the

respective wholesaler and another copy is marched in the purchase section. A ordinal

purchase order record is attached to the purchase order file (Swanson Swanson and Lindsay

2017).

In the next step of the purchase process the control system starts after the goods

arrived in the receiving department. Here the receiving clerk receive the goods after

inspecting all the goods against the details that are mentioned in the digital purchase order

and the packing slip. After the verification process the clerk then create two hard copies of

the receiving reports. One of which is attached with the goods and send to the inventory

warehouse, in the warehouse the clerks defers the goods and update the inventory ledger

which is kept in the computer terminal of the receiving department. The receiving report is

then filed by the clerk and kept in the respective department. The other copy of the receiving

report is sent to the accounts payable department, where the clerk of the accounts payable

department files until the invoice of the supplier is received by the company. At the time of

receiving the invoice the accountant pulls the receiving report from the temporary file, the

accountant then prints a hard copy of the digital purchase order, and reconcile the three

documents. The clerk updates the accounts payable subsidiary ledger, the accounts payable

control account and the inventory control account in the general ledger form the terminal of

the receiving department. At the final stage the clerk sends the invoice to the receiving report

INTERNAL CONTROL SYSTEM

the raw materials does not have any loopholes for which the supply process of the company

does not have to suffer. The process of the purchase starts with the checking of the inventory

subsidiary ledger which is done by the purchasing clerk on a regular basis on the early

morning when the goods arrived. if the clerk finds the quantity of any specific item is too low

in that case the clerk immediately chooses a seller from the wholesaler file and makes a

digital purchase order. The clerk prints hard copies from which one copy is sent to the

respective wholesaler and another copy is marched in the purchase section. A ordinal

purchase order record is attached to the purchase order file (Swanson Swanson and Lindsay

2017).

In the next step of the purchase process the control system starts after the goods

arrived in the receiving department. Here the receiving clerk receive the goods after

inspecting all the goods against the details that are mentioned in the digital purchase order

and the packing slip. After the verification process the clerk then create two hard copies of

the receiving reports. One of which is attached with the goods and send to the inventory

warehouse, in the warehouse the clerks defers the goods and update the inventory ledger

which is kept in the computer terminal of the receiving department. The receiving report is

then filed by the clerk and kept in the respective department. The other copy of the receiving

report is sent to the accounts payable department, where the clerk of the accounts payable

department files until the invoice of the supplier is received by the company. At the time of

receiving the invoice the accountant pulls the receiving report from the temporary file, the

accountant then prints a hard copy of the digital purchase order, and reconcile the three

documents. The clerk updates the accounts payable subsidiary ledger, the accounts payable

control account and the inventory control account in the general ledger form the terminal of

the receiving department. At the final stage the clerk sends the invoice to the receiving report

5

INTERNAL CONTROL SYSTEM

and the purchase order copy to the cash disbursement department from which the supplier

will collect its cheque (Ellis 2018). The entire process can be explained in a better way

through the flowchart

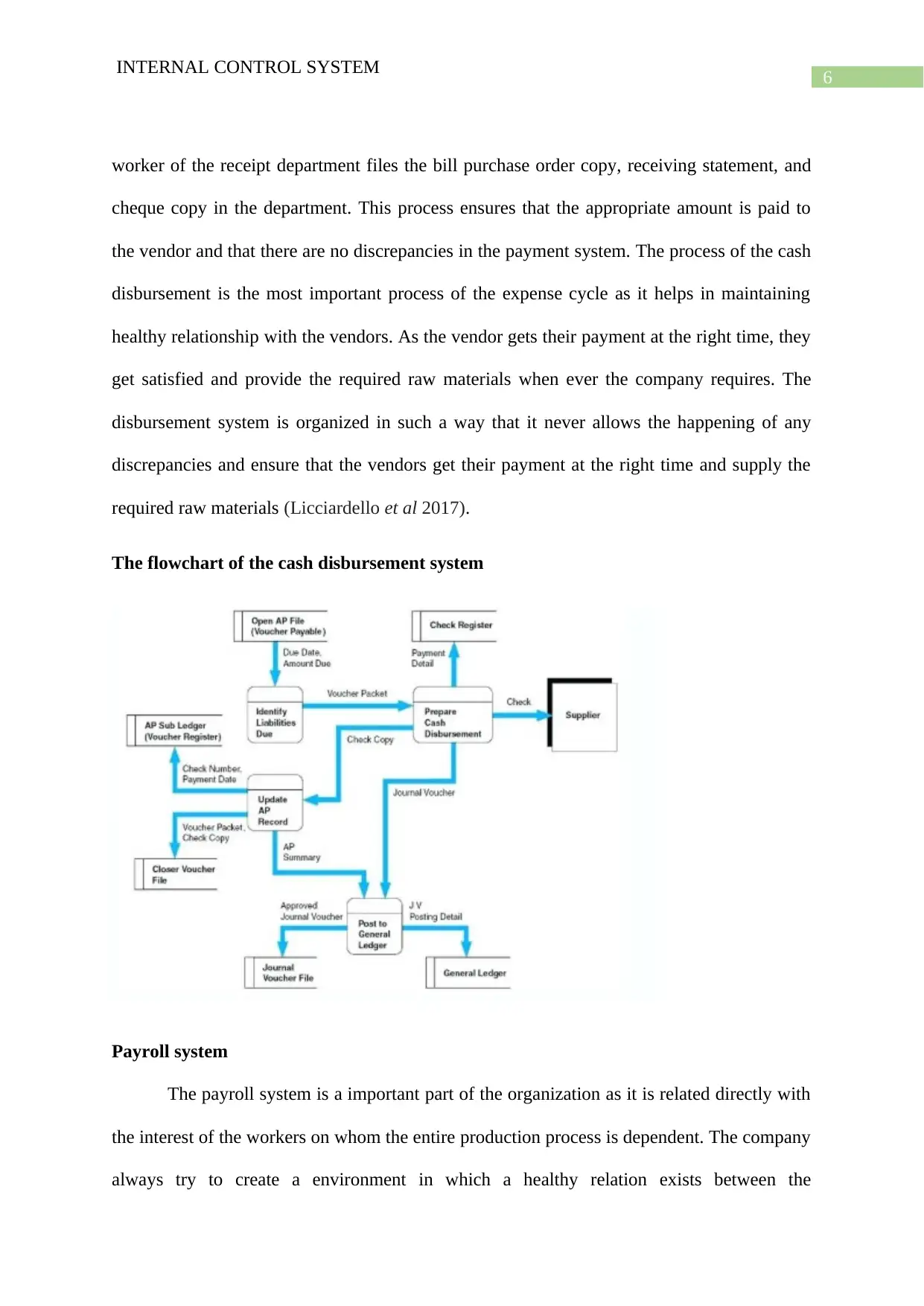

Cash disbursement system

After receiving the pamphlets from the accounts payable department, the clerk of the

disbursement department files the documents till their imbursement date is due. On the

outstanding date the clerk makes a cheque for the billed account, then it is directed to the

financial officer to take the approval of the treasurer and then the cheque is mailed to the

vendor (Mahajan Shukla and Soni 2015).

The cash disbursement clerk after that apprises the cheque record, accounts payable

subsidiary ledger and the accounts payable account from his computer incurable. Finally, the

INTERNAL CONTROL SYSTEM

and the purchase order copy to the cash disbursement department from which the supplier

will collect its cheque (Ellis 2018). The entire process can be explained in a better way

through the flowchart

Cash disbursement system

After receiving the pamphlets from the accounts payable department, the clerk of the

disbursement department files the documents till their imbursement date is due. On the

outstanding date the clerk makes a cheque for the billed account, then it is directed to the

financial officer to take the approval of the treasurer and then the cheque is mailed to the

vendor (Mahajan Shukla and Soni 2015).

The cash disbursement clerk after that apprises the cheque record, accounts payable

subsidiary ledger and the accounts payable account from his computer incurable. Finally, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

INTERNAL CONTROL SYSTEM

worker of the receipt department files the bill purchase order copy, receiving statement, and

cheque copy in the department. This process ensures that the appropriate amount is paid to

the vendor and that there are no discrepancies in the payment system. The process of the cash

disbursement is the most important process of the expense cycle as it helps in maintaining

healthy relationship with the vendors. As the vendor gets their payment at the right time, they

get satisfied and provide the required raw materials when ever the company requires. The

disbursement system is organized in such a way that it never allows the happening of any

discrepancies and ensure that the vendors get their payment at the right time and supply the

required raw materials (Licciardello et al 2017).

The flowchart of the cash disbursement system

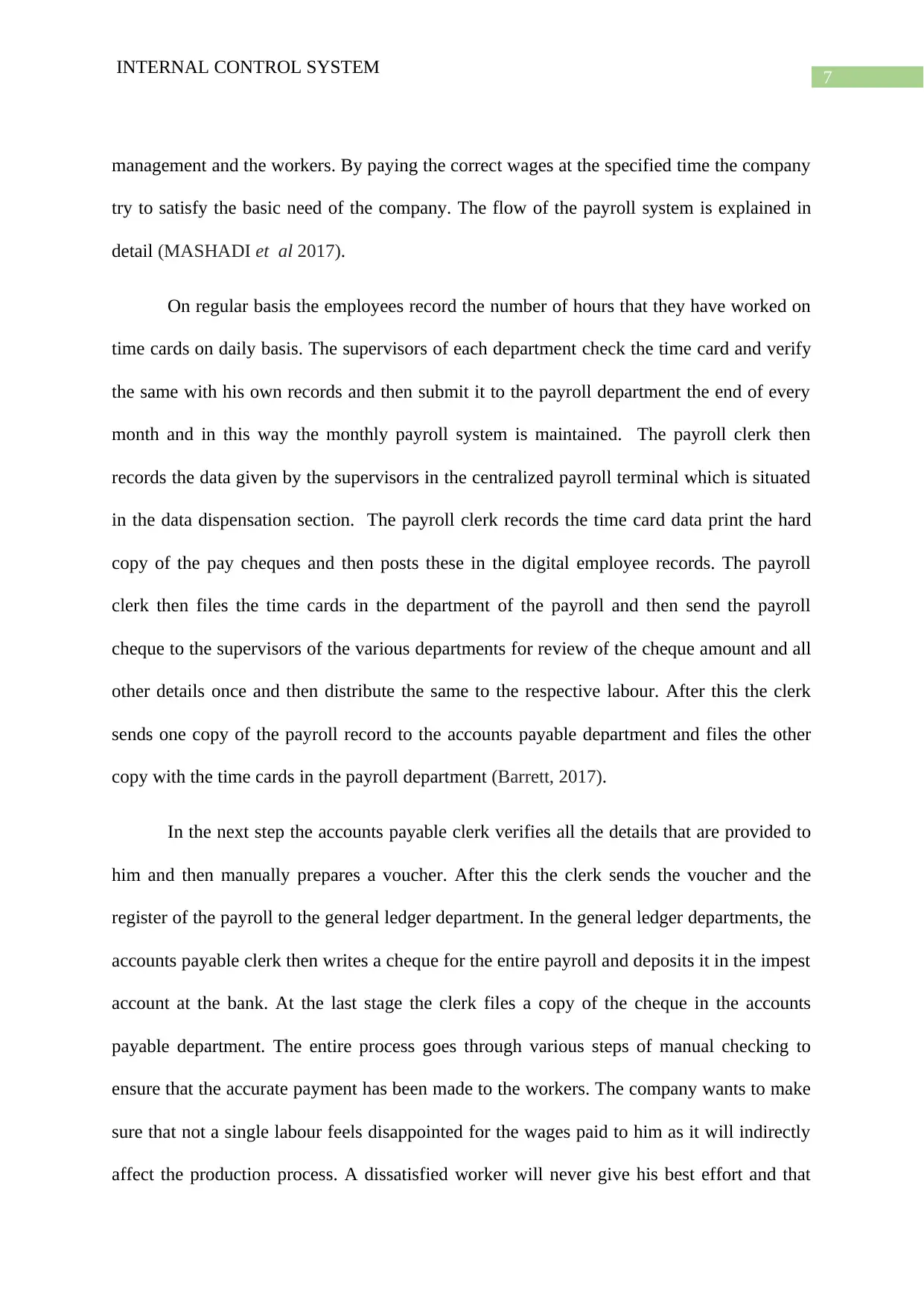

Payroll system

The payroll system is a important part of the organization as it is related directly with

the interest of the workers on whom the entire production process is dependent. The company

always try to create a environment in which a healthy relation exists between the

INTERNAL CONTROL SYSTEM

worker of the receipt department files the bill purchase order copy, receiving statement, and

cheque copy in the department. This process ensures that the appropriate amount is paid to

the vendor and that there are no discrepancies in the payment system. The process of the cash

disbursement is the most important process of the expense cycle as it helps in maintaining

healthy relationship with the vendors. As the vendor gets their payment at the right time, they

get satisfied and provide the required raw materials when ever the company requires. The

disbursement system is organized in such a way that it never allows the happening of any

discrepancies and ensure that the vendors get their payment at the right time and supply the

required raw materials (Licciardello et al 2017).

The flowchart of the cash disbursement system

Payroll system

The payroll system is a important part of the organization as it is related directly with

the interest of the workers on whom the entire production process is dependent. The company

always try to create a environment in which a healthy relation exists between the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

INTERNAL CONTROL SYSTEM

management and the workers. By paying the correct wages at the specified time the company

try to satisfy the basic need of the company. The flow of the payroll system is explained in

detail (MASHADI et al 2017).

On regular basis the employees record the number of hours that they have worked on

time cards on daily basis. The supervisors of each department check the time card and verify

the same with his own records and then submit it to the payroll department the end of every

month and in this way the monthly payroll system is maintained. The payroll clerk then

records the data given by the supervisors in the centralized payroll terminal which is situated

in the data dispensation section. The payroll clerk records the time card data print the hard

copy of the pay cheques and then posts these in the digital employee records. The payroll

clerk then files the time cards in the department of the payroll and then send the payroll

cheque to the supervisors of the various departments for review of the cheque amount and all

other details once and then distribute the same to the respective labour. After this the clerk

sends one copy of the payroll record to the accounts payable department and files the other

copy with the time cards in the payroll department (Barrett, 2017).

In the next step the accounts payable clerk verifies all the details that are provided to

him and then manually prepares a voucher. After this the clerk sends the voucher and the

register of the payroll to the general ledger department. In the general ledger departments, the

accounts payable clerk then writes a cheque for the entire payroll and deposits it in the impest

account at the bank. At the last stage the clerk files a copy of the cheque in the accounts

payable department. The entire process goes through various steps of manual checking to

ensure that the accurate payment has been made to the workers. The company wants to make

sure that not a single labour feels disappointed for the wages paid to him as it will indirectly

affect the production process. A dissatisfied worker will never give his best effort and that

INTERNAL CONTROL SYSTEM

management and the workers. By paying the correct wages at the specified time the company

try to satisfy the basic need of the company. The flow of the payroll system is explained in

detail (MASHADI et al 2017).

On regular basis the employees record the number of hours that they have worked on

time cards on daily basis. The supervisors of each department check the time card and verify

the same with his own records and then submit it to the payroll department the end of every

month and in this way the monthly payroll system is maintained. The payroll clerk then

records the data given by the supervisors in the centralized payroll terminal which is situated

in the data dispensation section. The payroll clerk records the time card data print the hard

copy of the pay cheques and then posts these in the digital employee records. The payroll

clerk then files the time cards in the department of the payroll and then send the payroll

cheque to the supervisors of the various departments for review of the cheque amount and all

other details once and then distribute the same to the respective labour. After this the clerk

sends one copy of the payroll record to the accounts payable department and files the other

copy with the time cards in the payroll department (Barrett, 2017).

In the next step the accounts payable clerk verifies all the details that are provided to

him and then manually prepares a voucher. After this the clerk sends the voucher and the

register of the payroll to the general ledger department. In the general ledger departments, the

accounts payable clerk then writes a cheque for the entire payroll and deposits it in the impest

account at the bank. At the last stage the clerk files a copy of the cheque in the accounts

payable department. The entire process goes through various steps of manual checking to

ensure that the accurate payment has been made to the workers. The company wants to make

sure that not a single labour feels disappointed for the wages paid to him as it will indirectly

affect the production process. A dissatisfied worker will never give his best effort and that

8

INTERNAL CONTROL SYSTEM

will affect the progress of the company. So in view of this kind of problems may arise if the

payment to the workers are paid properly the company has adopted a systematic method of

the payroll system which enables the company to keep the workers happy and also saves

resources for the company (Collins et al 2016).

Flowchart of the payroll system

The weakness in each system

Purchase system

It has been observed that there is no specific purchase department in the organization

and only one clerk is appointed to look after the process of the purchase. The orders are

placed after the verification of the clerk which means that the company does not maintain any

system before placing a order. The products are received and kept with out following any

method of inventory that is either the products are stored as per first in first out basis or last in

INTERNAL CONTROL SYSTEM

will affect the progress of the company. So in view of this kind of problems may arise if the

payment to the workers are paid properly the company has adopted a systematic method of

the payroll system which enables the company to keep the workers happy and also saves

resources for the company (Collins et al 2016).

Flowchart of the payroll system

The weakness in each system

Purchase system

It has been observed that there is no specific purchase department in the organization

and only one clerk is appointed to look after the process of the purchase. The orders are

placed after the verification of the clerk which means that the company does not maintain any

system before placing a order. The products are received and kept with out following any

method of inventory that is either the products are stored as per first in first out basis or last in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

INTERNAL CONTROL SYSTEM

last out basis. The company also does not have any predefined vendor management system so

there is no specification that from which vendor how much order has been placed (Taha and

AbdulRazzaq 2019). Some of the major issues of the purchase system are stated below

Not self-sufficiently verified with inventory in contradiction of the procurement

demand that can consequence to overstock.

There is no proper system of the numbering of the orders counting the invalid orders

that can consequence to inappropriate order and no acquisition deal occurs.

Proper selection process of the suppliers are not followed and the company used to

select the vendors based on their past performance and not on the basis of prices and

terms and delivery time.

All inward possessions that includes fixed assets are not cleared by a goods inwards

receipt section.

Any inconsistency among instruction and distribution tag only accepted by properties

inward manager. There is no additional person to give approval in the nonappearance

of the administrator.

No autonomous verification on the acquiring in contradiction of the order.

No monitoring of comparison among receipt of accounts and the examination reports

which might consequence to no assurance that all substances conventional are in good

ailment or not.

Acquiring officer trusts on individual information and there is no certifiable self-

governing price list to guarantee that the contractor’s price list to confirm traders’

price are precise. Recording of values could be lower or exaggerated.

No suitable indication on bill to specify numerous interior checks have been achieved.

INTERNAL CONTROL SYSTEM

last out basis. The company also does not have any predefined vendor management system so

there is no specification that from which vendor how much order has been placed (Taha and

AbdulRazzaq 2019). Some of the major issues of the purchase system are stated below

Not self-sufficiently verified with inventory in contradiction of the procurement

demand that can consequence to overstock.

There is no proper system of the numbering of the orders counting the invalid orders

that can consequence to inappropriate order and no acquisition deal occurs.

Proper selection process of the suppliers are not followed and the company used to

select the vendors based on their past performance and not on the basis of prices and

terms and delivery time.

All inward possessions that includes fixed assets are not cleared by a goods inwards

receipt section.

Any inconsistency among instruction and distribution tag only accepted by properties

inward manager. There is no additional person to give approval in the nonappearance

of the administrator.

No autonomous verification on the acquiring in contradiction of the order.

No monitoring of comparison among receipt of accounts and the examination reports

which might consequence to no assurance that all substances conventional are in good

ailment or not.

Acquiring officer trusts on individual information and there is no certifiable self-

governing price list to guarantee that the contractor’s price list to confirm traders’

price are precise. Recording of values could be lower or exaggerated.

No suitable indication on bill to specify numerous interior checks have been achieved.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

INTERNAL CONTROL SYSTEM

Weakness in the cash disbursement system

No pre numbered cheques

Proper maintenance of cheques is not done which might leads to the manipulation of

the cheques

Duty is not segregated properly for which confusion arise between the staffs regarding

their responsibility.

Weakness of the payroll system

The major weakness that are identified in the payroll system are stated below

Data collection

The time card is recorded manually by the employees this led to the manipulation of

the data that are recorded in the time card. The process of data collection system is wrongly

done by the organization.

Separation of the duty

The duty of the payroll system should be divided among various staffs so that they

can do their job professionally and that will ensure that all the data are correct and that there

is no scope of embezzlement.

Data security

Security controls are meant for the protection of the confidential information of the

employees. The company still maintains hard copy information cheque stamping process

which will led to the occurrence of the theft of information money or equipment.

INTERNAL CONTROL SYSTEM

Weakness in the cash disbursement system

No pre numbered cheques

Proper maintenance of cheques is not done which might leads to the manipulation of

the cheques

Duty is not segregated properly for which confusion arise between the staffs regarding

their responsibility.

Weakness of the payroll system

The major weakness that are identified in the payroll system are stated below

Data collection

The time card is recorded manually by the employees this led to the manipulation of

the data that are recorded in the time card. The process of data collection system is wrongly

done by the organization.

Separation of the duty

The duty of the payroll system should be divided among various staffs so that they

can do their job professionally and that will ensure that all the data are correct and that there

is no scope of embezzlement.

Data security

Security controls are meant for the protection of the confidential information of the

employees. The company still maintains hard copy information cheque stamping process

which will led to the occurrence of the theft of information money or equipment.

11

INTERNAL CONTROL SYSTEM

Conclusion

From the above discussion it can be concluded that the Adam & co has tried to

impose a strong system of purchase , cash disbursement, and payroll to ensure that the

company does not face the problem of the manipulation data and that all the flow of the entire

expenditure cycle moves in a smooth way and that will ensure the sustainable growth of the

company. Though from the analysis it can be observed that there is some weakness in the

internal control system that will lead to the occurrence of the manipulation of data and will

lead to the obstruction of the production process.

INTERNAL CONTROL SYSTEM

Conclusion

From the above discussion it can be concluded that the Adam & co has tried to

impose a strong system of purchase , cash disbursement, and payroll to ensure that the

company does not face the problem of the manipulation data and that all the flow of the entire

expenditure cycle moves in a smooth way and that will ensure the sustainable growth of the

company. Though from the analysis it can be observed that there is some weakness in the

internal control system that will lead to the occurrence of the manipulation of data and will

lead to the obstruction of the production process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.