Finance Assignment: Bank Reconciliation, Inventory, and Adjustments

VerifiedAdded on 2020/10/23

|4

|369

|74

Homework Assignment

AI Summary

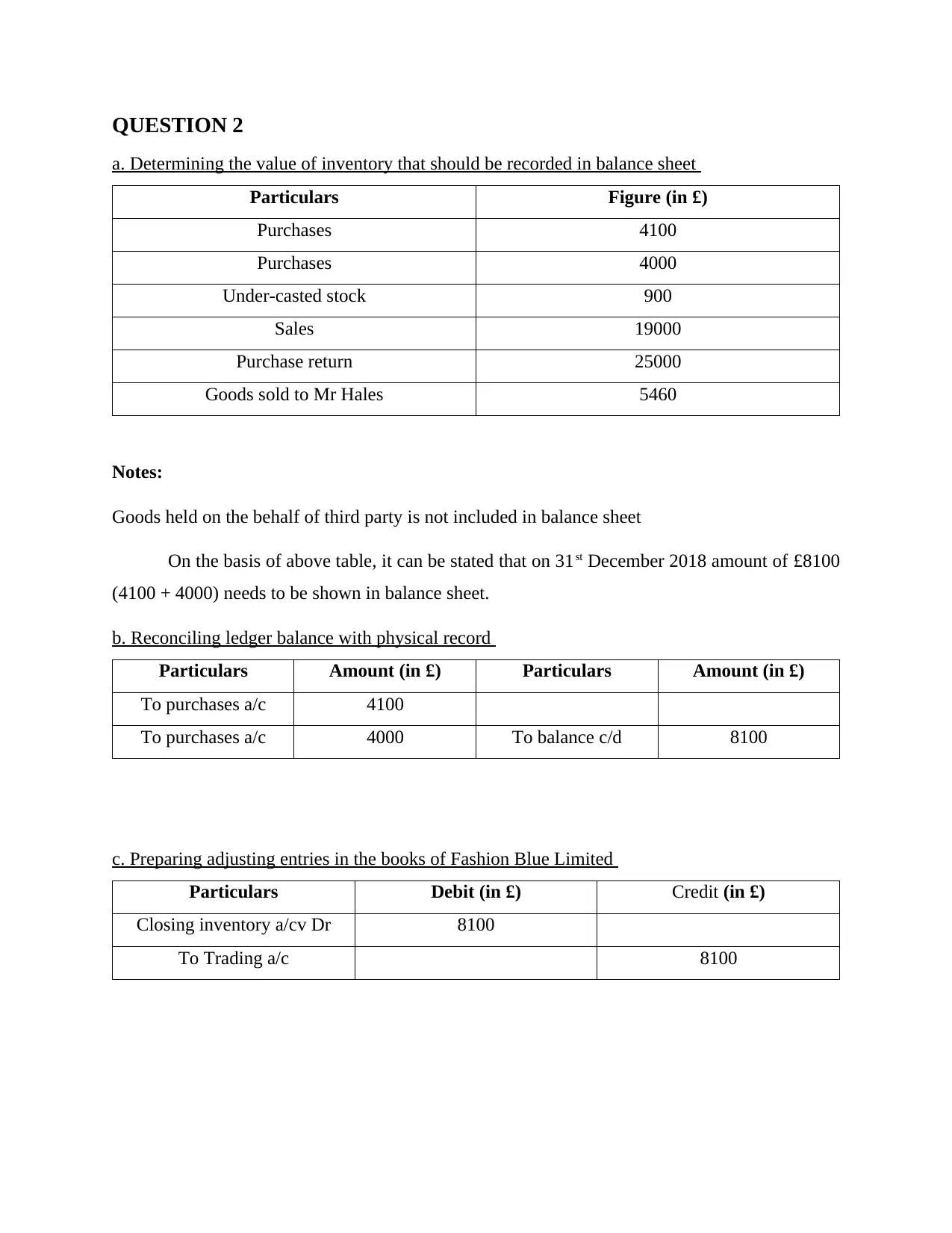

This assignment solution addresses two key areas of financial accounting: bank reconciliation and inventory valuation. The solution begins by detailing the preparation of a bank reconciliation statement, including the adjustment of a bank book, and determining the final bank balance. The second part of the solution focuses on inventory, determining the value of inventory to be recorded in the balance sheet, reconciling ledger balances with physical records, and preparing the necessary adjusting entries in the books of Fashion Blue Limited. Specifically, it calculates the inventory value based on purchases, sales, and purchase returns, and provides the journal entry for closing inventory. The assignment provides a clear understanding of these core accounting principles.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.