Accounting for Business: Ratio Analysis and Investment Decisions

VerifiedAdded on 2023/06/04

|10

|1738

|251

Report

AI Summary

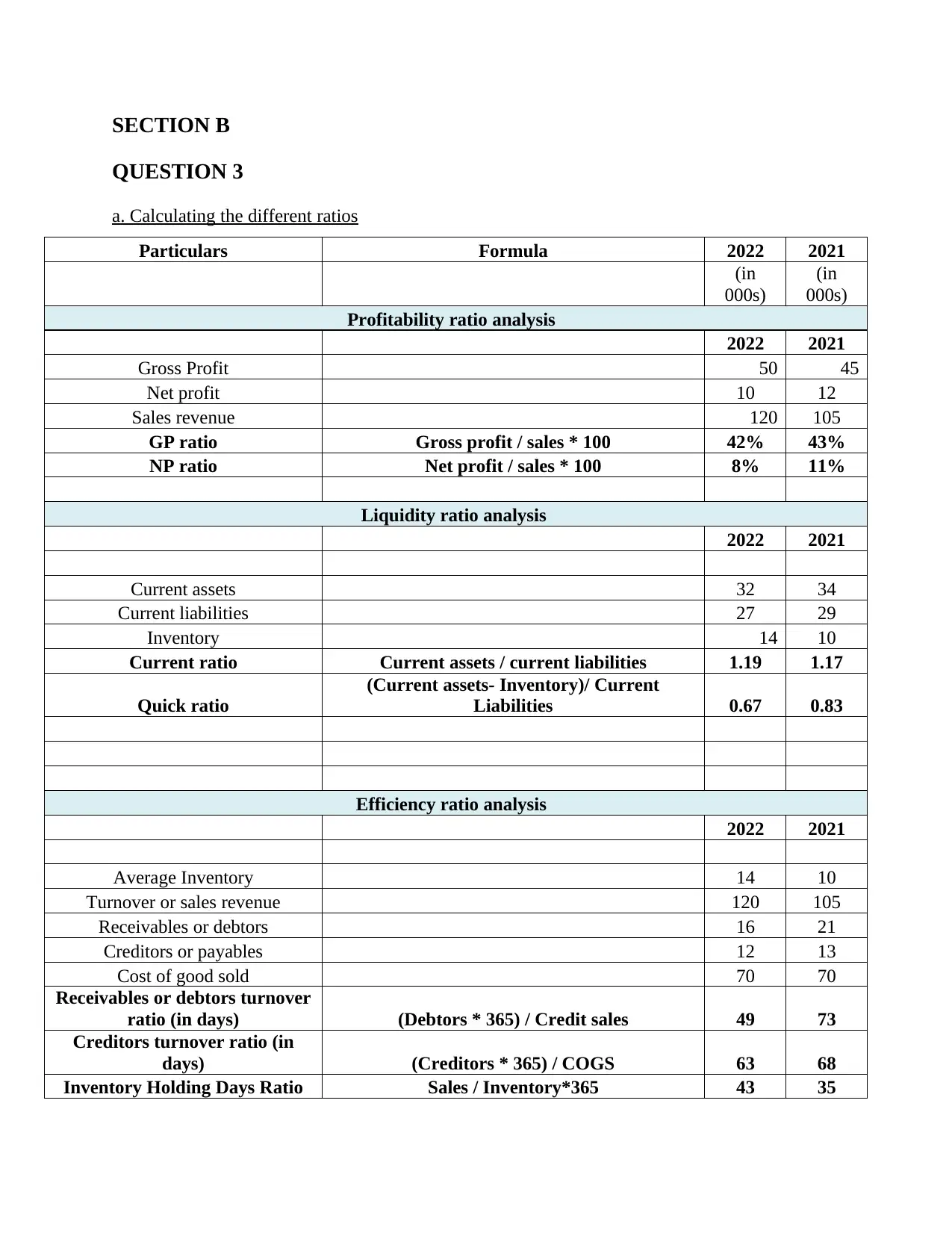

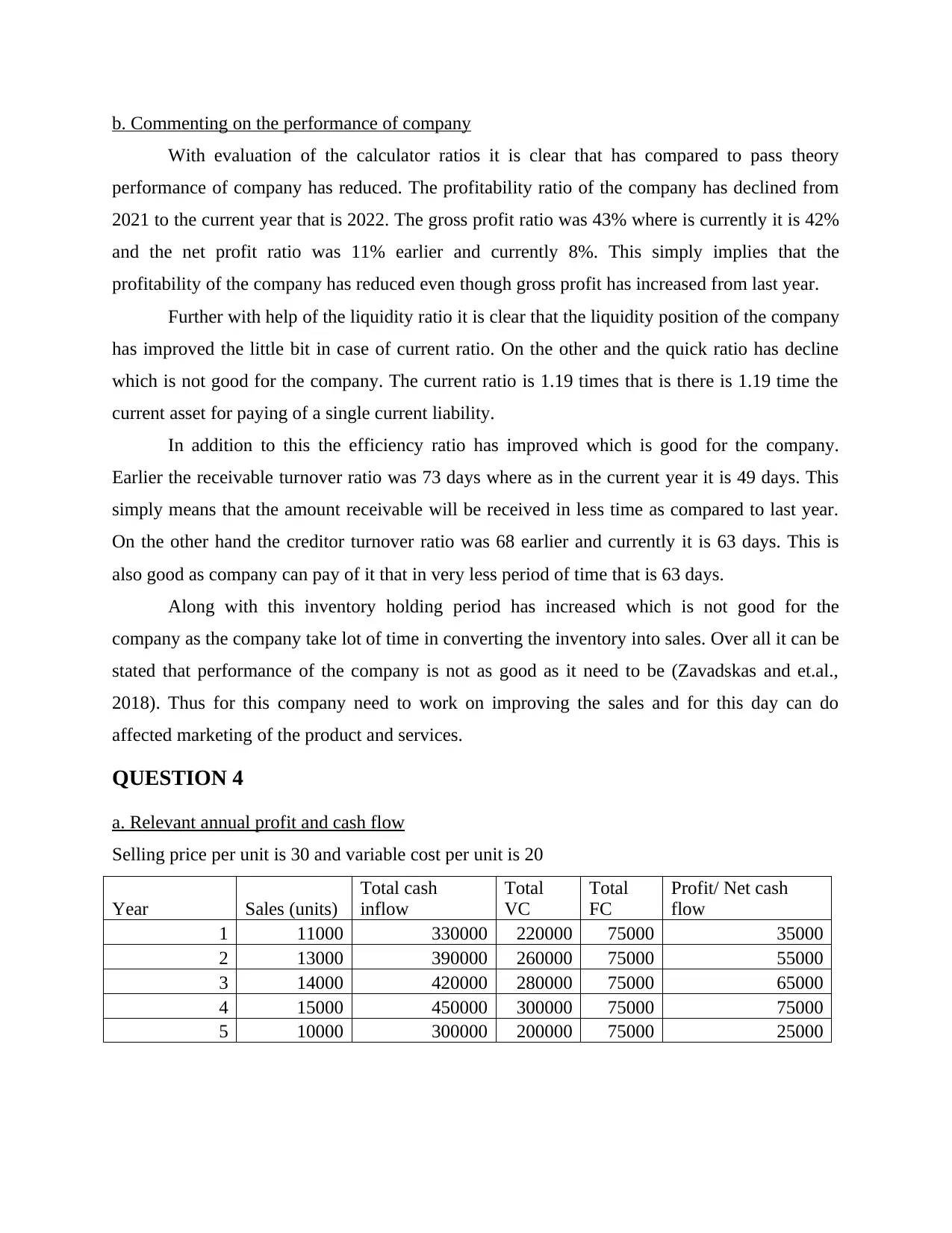

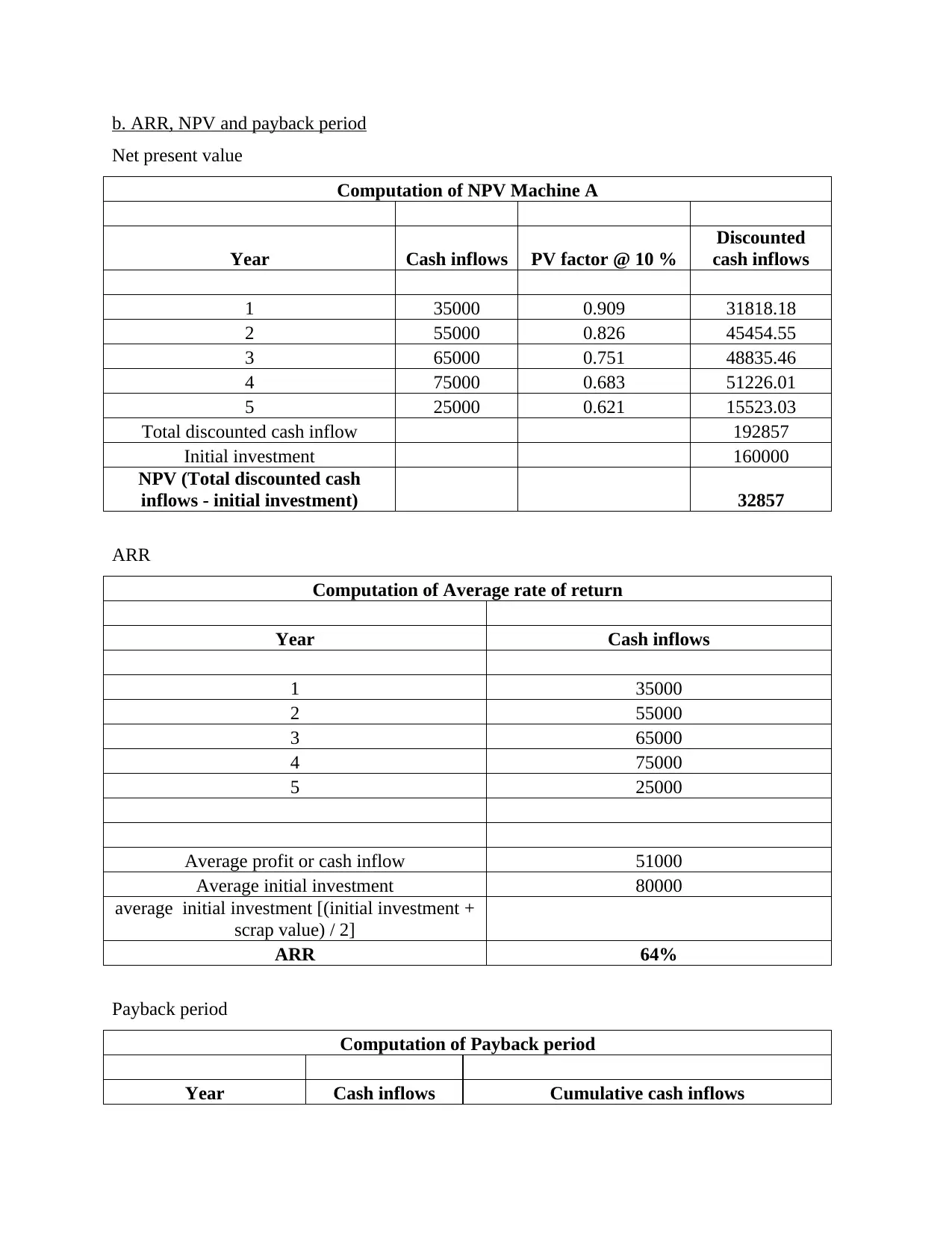

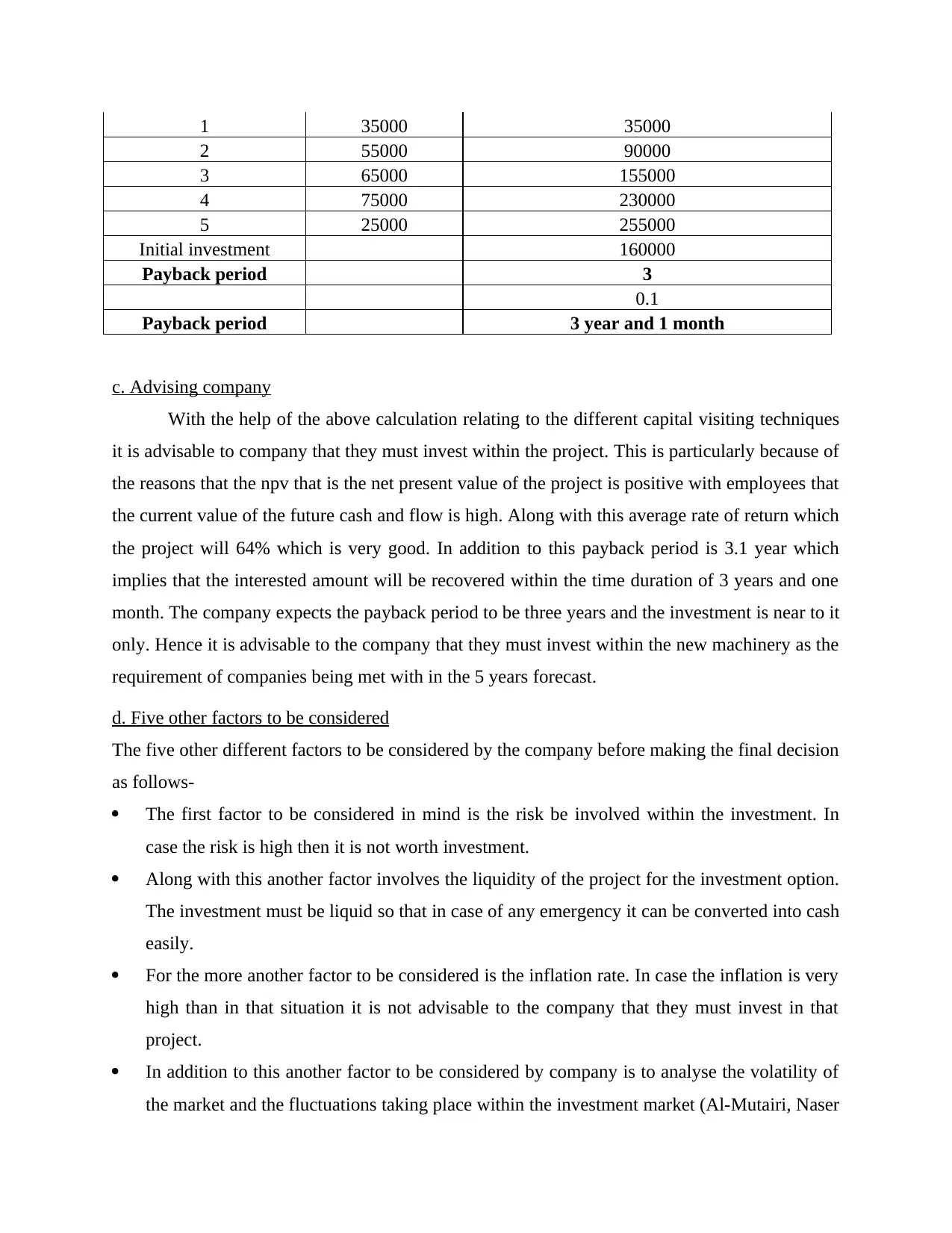

This accounting report meticulously analyzes financial statements, including the income statement and the statement of financial position, to assess a company's performance. The report delves into profitability, liquidity, and efficiency ratios, comparing the company's performance over two years. It evaluates investment decisions using techniques such as ARR, NPV, and payback period, offering recommendations on whether the company should invest in a new machine. Furthermore, it identifies crucial factors for investment decisions, such as risk, liquidity, and market volatility, and explains the advantages of the internal rate of return (IRR). The report provides a comprehensive overview of financial analysis and investment strategies, making it a valuable resource for students studying accounting and finance. This report is available on Desklib, a platform offering AI-based study tools to help students excel.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.