Analysis of Contemporary Accounting Issues: BHP Billiton & Woolworths

VerifiedAdded on 2020/03/04

|14

|2875

|168

Report

AI Summary

This report provides a critical analysis of the 2016 annual reports of BHP Billiton and Woolworths, evaluating their compliance with the conceptual framework and relevant Australian Accounting Standards Board (AASB) standards. The analysis focuses on key financial statement components, including Property, Plant, and Equipment (PPE), inventories, asset impairment, and contingent liabilities. The report compares the companies' accounting policies with the expected standards, highlighting any discrepancies. Additionally, it discusses the role of prudence in the conceptual framework, its compatibility with neutrality, and its potential implications for corporate reporting. The report also draws a comparison of disclosures in the annual reports of the two companies. The conclusion summarizes the findings, emphasizing the adherence of both companies to accounting standards and the significance of prudence in ensuring accurate and relevant financial information for stakeholders. The report is a valuable resource for understanding contemporary accounting practices and the application of accounting standards in real-world scenarios.

Contemporary Issues in Accounting

BHP Billiton & Woolworths

Student ID:

[Pick the date]

BHP Billiton & Woolworths

Student ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary

The given report has the aim of critically analysing the latest annual reports of BHP Billiton

and Woolworths in order to determine if the various accounting policies utilised in the

representation of the financial statements tend to comply with the conceptual framework and

also the appropriate AASB standards or not. In this endeavour, the focus is essentially on

highlighting few pivotal components of the financial statements and compares the actual

policy with the expected policy. Further, the role and introduction of prudence in the

conceptual framework has been highlighted coupled with the inherent incompatibility with

neutrality and the likely implications of prudence on corporate reporting. Also, a comparison

has been drawn of the disclosures in the annual reports of the given companies.

1

Executive Summary

The given report has the aim of critically analysing the latest annual reports of BHP Billiton

and Woolworths in order to determine if the various accounting policies utilised in the

representation of the financial statements tend to comply with the conceptual framework and

also the appropriate AASB standards or not. In this endeavour, the focus is essentially on

highlighting few pivotal components of the financial statements and compares the actual

policy with the expected policy. Further, the role and introduction of prudence in the

conceptual framework has been highlighted coupled with the inherent incompatibility with

neutrality and the likely implications of prudence on corporate reporting. Also, a comparison

has been drawn of the disclosures in the annual reports of the given companies.

1

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Compliance with conceptual framework...................................................................................3

BHP Billiton...........................................................................................................................3

Woolworths............................................................................................................................7

Role of Prudence........................................................................................................................9

Comparison of disclosures.......................................................................................................10

Conclusion................................................................................................................................11

References................................................................................................................................11

2

Table of Contents

Introduction................................................................................................................................3

Compliance with conceptual framework...................................................................................3

BHP Billiton...........................................................................................................................3

Woolworths............................................................................................................................7

Role of Prudence........................................................................................................................9

Comparison of disclosures.......................................................................................................10

Conclusion................................................................................................................................11

References................................................................................................................................11

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

Conceptual framework is a useful tool which to ensure that corporate reporting for various

organisations is not only at par but at the same time relevant for the users. The underlying

aim of deploying conceptual framework is to make sure that the accounting norms applied by

the firms are driven by the same uniform rules while maintaining the relevance of disclosures

for various stakeholders particularly shareholders. Another utility of conceptual framework is

that it results in accounting standards harmonisation which makes comparison between

companies based in different geographies possible as the financial statements are driven by

the same underlying rules (Melville, 2013). In the Australian context, the conceptual

framework given by the IASB (International Accounting Standards Board) is represented in

the applicable accounting standards that have been given by AASB or Australian Accounting

Standards Board. This ensures that the results of the Australian listed entities can be

compared with their counterparts elsewhere especially where conceptual framework is the

same and hence attracts foreign investors (Deegan, 2014).

In wake of the above context, the underlying report aims to critically analyse the FY2016

annual report for the two public listed companies namely BHP Billiton and Woolworths in

order to opine on whether the accounting standards deployed deploys the conceptual

framework or not. Additionally, the scope of the report also includes a comparison of the

nature of disclosures visible for the two selected companies. Besides, the addition of

prudence and subsequent modification of the conceptual framework and the potential

implications for parity in corporate reporting has also been discussed.

Compliance with conceptual framework

As outlined above, for the sake of this task, the selected companies are BHP Billiton

(Mining) and Woolworths (Organised Retail – Supermarkets). The critical analysis of the

corporate reporting in relation to the various applicable aspects of the corporate reporting is

outlined below.

BHP Billiton

The critical aspects worth discussing are highlighted above along with relevant extract from

the annual report.

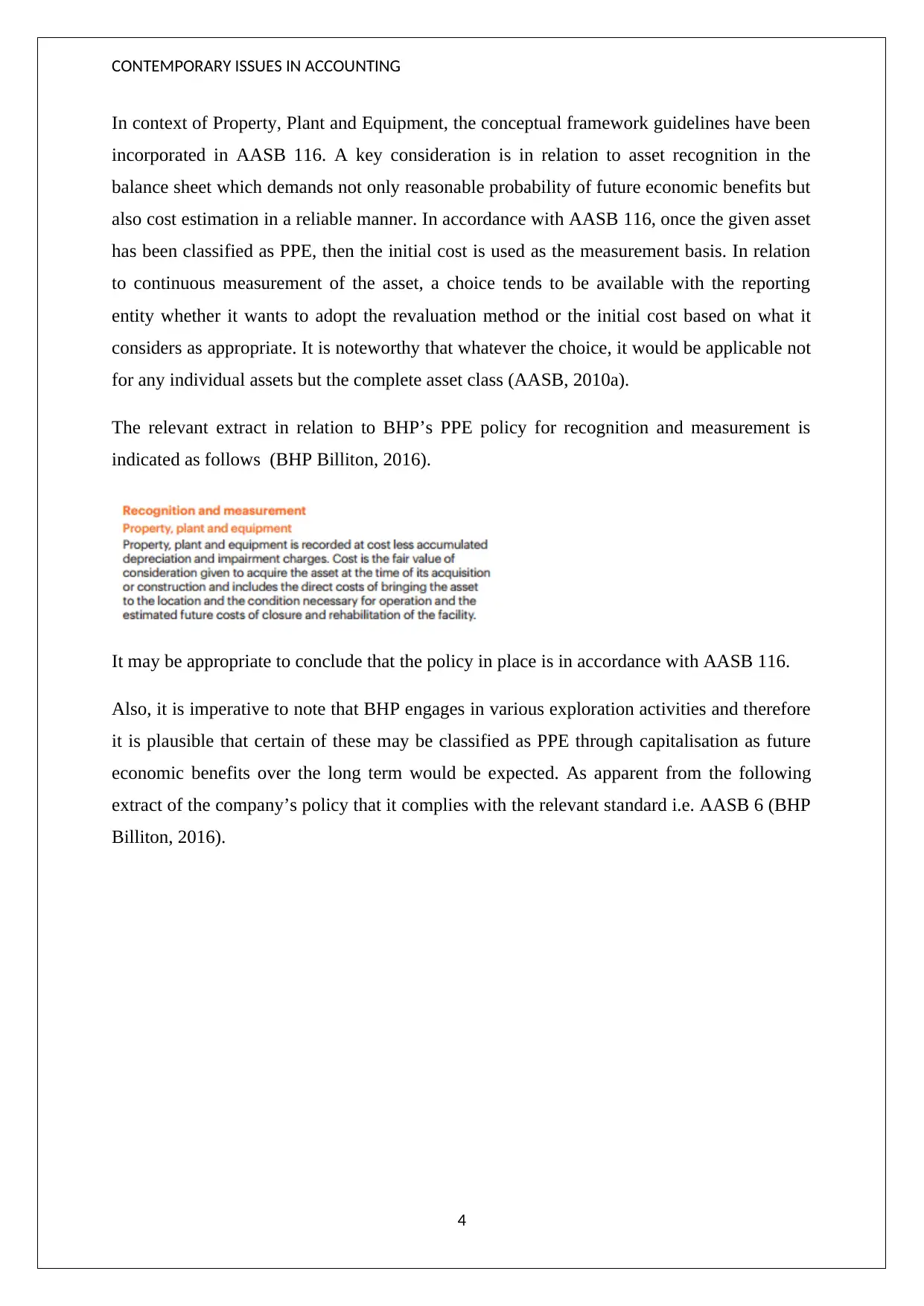

PPE (Property, plant & Equipment) – ( Relevant Standard - AASB 116)

3

Introduction

Conceptual framework is a useful tool which to ensure that corporate reporting for various

organisations is not only at par but at the same time relevant for the users. The underlying

aim of deploying conceptual framework is to make sure that the accounting norms applied by

the firms are driven by the same uniform rules while maintaining the relevance of disclosures

for various stakeholders particularly shareholders. Another utility of conceptual framework is

that it results in accounting standards harmonisation which makes comparison between

companies based in different geographies possible as the financial statements are driven by

the same underlying rules (Melville, 2013). In the Australian context, the conceptual

framework given by the IASB (International Accounting Standards Board) is represented in

the applicable accounting standards that have been given by AASB or Australian Accounting

Standards Board. This ensures that the results of the Australian listed entities can be

compared with their counterparts elsewhere especially where conceptual framework is the

same and hence attracts foreign investors (Deegan, 2014).

In wake of the above context, the underlying report aims to critically analyse the FY2016

annual report for the two public listed companies namely BHP Billiton and Woolworths in

order to opine on whether the accounting standards deployed deploys the conceptual

framework or not. Additionally, the scope of the report also includes a comparison of the

nature of disclosures visible for the two selected companies. Besides, the addition of

prudence and subsequent modification of the conceptual framework and the potential

implications for parity in corporate reporting has also been discussed.

Compliance with conceptual framework

As outlined above, for the sake of this task, the selected companies are BHP Billiton

(Mining) and Woolworths (Organised Retail – Supermarkets). The critical analysis of the

corporate reporting in relation to the various applicable aspects of the corporate reporting is

outlined below.

BHP Billiton

The critical aspects worth discussing are highlighted above along with relevant extract from

the annual report.

PPE (Property, plant & Equipment) – ( Relevant Standard - AASB 116)

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ISSUES IN ACCOUNTING

In context of Property, Plant and Equipment, the conceptual framework guidelines have been

incorporated in AASB 116. A key consideration is in relation to asset recognition in the

balance sheet which demands not only reasonable probability of future economic benefits but

also cost estimation in a reliable manner. In accordance with AASB 116, once the given asset

has been classified as PPE, then the initial cost is used as the measurement basis. In relation

to continuous measurement of the asset, a choice tends to be available with the reporting

entity whether it wants to adopt the revaluation method or the initial cost based on what it

considers as appropriate. It is noteworthy that whatever the choice, it would be applicable not

for any individual assets but the complete asset class (AASB, 2010a).

The relevant extract in relation to BHP’s PPE policy for recognition and measurement is

indicated as follows (BHP Billiton, 2016).

It may be appropriate to conclude that the policy in place is in accordance with AASB 116.

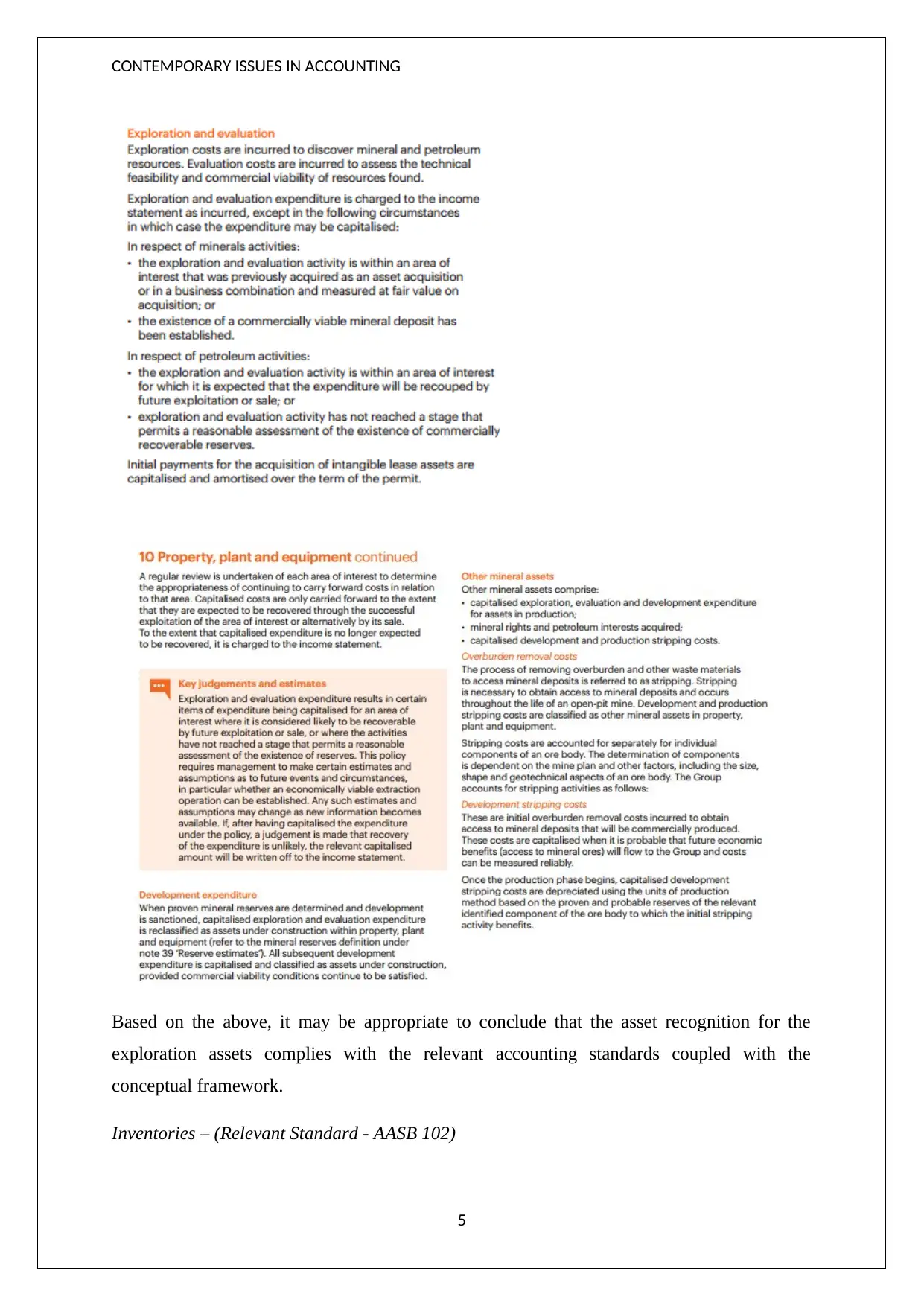

Also, it is imperative to note that BHP engages in various exploration activities and therefore

it is plausible that certain of these may be classified as PPE through capitalisation as future

economic benefits over the long term would be expected. As apparent from the following

extract of the company’s policy that it complies with the relevant standard i.e. AASB 6 (BHP

Billiton, 2016).

4

In context of Property, Plant and Equipment, the conceptual framework guidelines have been

incorporated in AASB 116. A key consideration is in relation to asset recognition in the

balance sheet which demands not only reasonable probability of future economic benefits but

also cost estimation in a reliable manner. In accordance with AASB 116, once the given asset

has been classified as PPE, then the initial cost is used as the measurement basis. In relation

to continuous measurement of the asset, a choice tends to be available with the reporting

entity whether it wants to adopt the revaluation method or the initial cost based on what it

considers as appropriate. It is noteworthy that whatever the choice, it would be applicable not

for any individual assets but the complete asset class (AASB, 2010a).

The relevant extract in relation to BHP’s PPE policy for recognition and measurement is

indicated as follows (BHP Billiton, 2016).

It may be appropriate to conclude that the policy in place is in accordance with AASB 116.

Also, it is imperative to note that BHP engages in various exploration activities and therefore

it is plausible that certain of these may be classified as PPE through capitalisation as future

economic benefits over the long term would be expected. As apparent from the following

extract of the company’s policy that it complies with the relevant standard i.e. AASB 6 (BHP

Billiton, 2016).

4

CONTEMPORARY ISSUES IN ACCOUNTING

Based on the above, it may be appropriate to conclude that the asset recognition for the

exploration assets complies with the relevant accounting standards coupled with the

conceptual framework.

Inventories – (Relevant Standard - AASB 102)

5

Based on the above, it may be appropriate to conclude that the asset recognition for the

exploration assets complies with the relevant accounting standards coupled with the

conceptual framework.

Inventories – (Relevant Standard - AASB 102)

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ISSUES IN ACCOUNTING

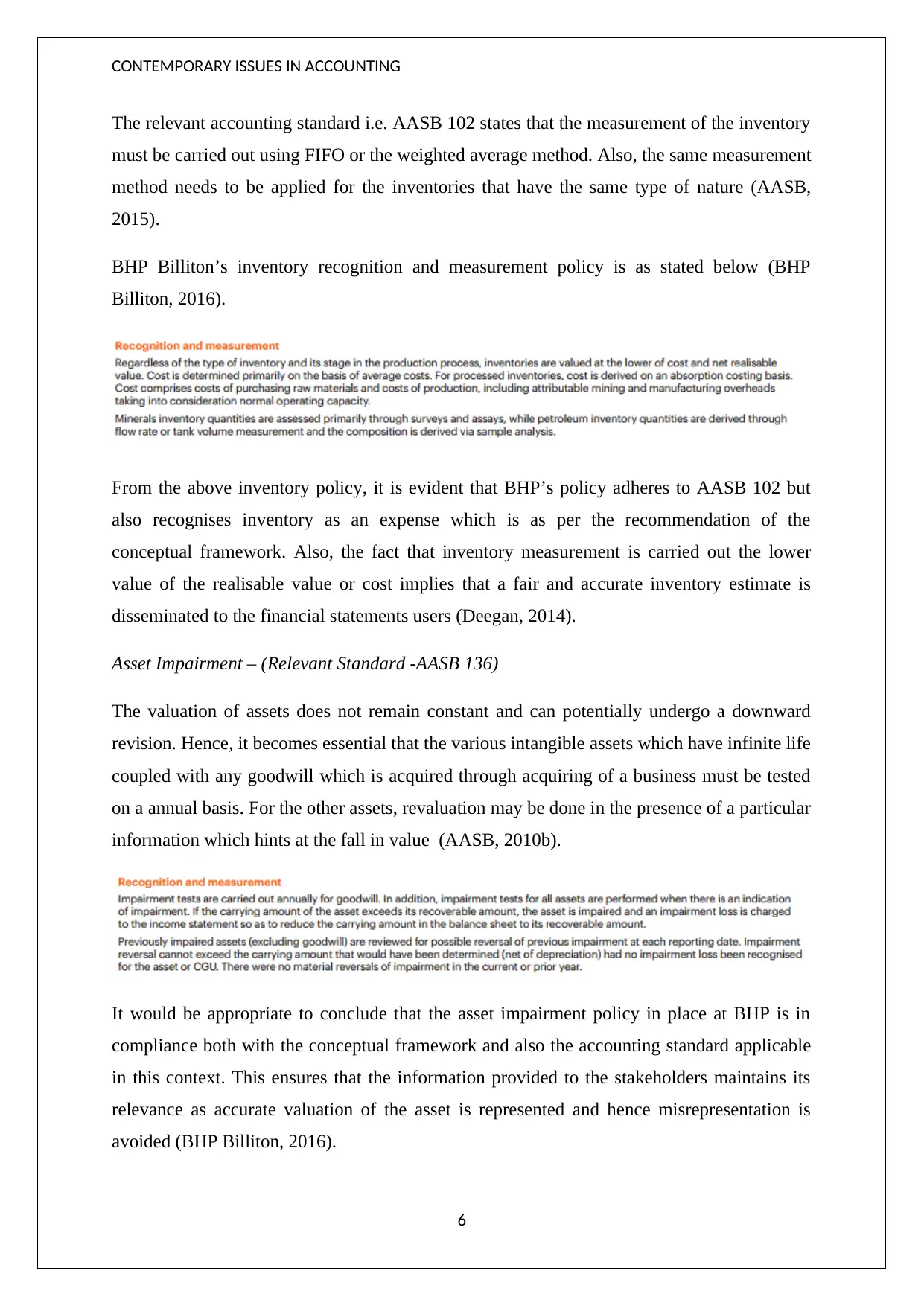

The relevant accounting standard i.e. AASB 102 states that the measurement of the inventory

must be carried out using FIFO or the weighted average method. Also, the same measurement

method needs to be applied for the inventories that have the same type of nature (AASB,

2015).

BHP Billiton’s inventory recognition and measurement policy is as stated below (BHP

Billiton, 2016).

From the above inventory policy, it is evident that BHP’s policy adheres to AASB 102 but

also recognises inventory as an expense which is as per the recommendation of the

conceptual framework. Also, the fact that inventory measurement is carried out the lower

value of the realisable value or cost implies that a fair and accurate inventory estimate is

disseminated to the financial statements users (Deegan, 2014).

Asset Impairment – (Relevant Standard -AASB 136)

The valuation of assets does not remain constant and can potentially undergo a downward

revision. Hence, it becomes essential that the various intangible assets which have infinite life

coupled with any goodwill which is acquired through acquiring of a business must be tested

on a annual basis. For the other assets, revaluation may be done in the presence of a particular

information which hints at the fall in value (AASB, 2010b).

It would be appropriate to conclude that the asset impairment policy in place at BHP is in

compliance both with the conceptual framework and also the accounting standard applicable

in this context. This ensures that the information provided to the stakeholders maintains its

relevance as accurate valuation of the asset is represented and hence misrepresentation is

avoided (BHP Billiton, 2016).

6

The relevant accounting standard i.e. AASB 102 states that the measurement of the inventory

must be carried out using FIFO or the weighted average method. Also, the same measurement

method needs to be applied for the inventories that have the same type of nature (AASB,

2015).

BHP Billiton’s inventory recognition and measurement policy is as stated below (BHP

Billiton, 2016).

From the above inventory policy, it is evident that BHP’s policy adheres to AASB 102 but

also recognises inventory as an expense which is as per the recommendation of the

conceptual framework. Also, the fact that inventory measurement is carried out the lower

value of the realisable value or cost implies that a fair and accurate inventory estimate is

disseminated to the financial statements users (Deegan, 2014).

Asset Impairment – (Relevant Standard -AASB 136)

The valuation of assets does not remain constant and can potentially undergo a downward

revision. Hence, it becomes essential that the various intangible assets which have infinite life

coupled with any goodwill which is acquired through acquiring of a business must be tested

on a annual basis. For the other assets, revaluation may be done in the presence of a particular

information which hints at the fall in value (AASB, 2010b).

It would be appropriate to conclude that the asset impairment policy in place at BHP is in

compliance both with the conceptual framework and also the accounting standard applicable

in this context. This ensures that the information provided to the stakeholders maintains its

relevance as accurate valuation of the asset is represented and hence misrepresentation is

avoided (BHP Billiton, 2016).

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ISSUES IN ACCOUNTING

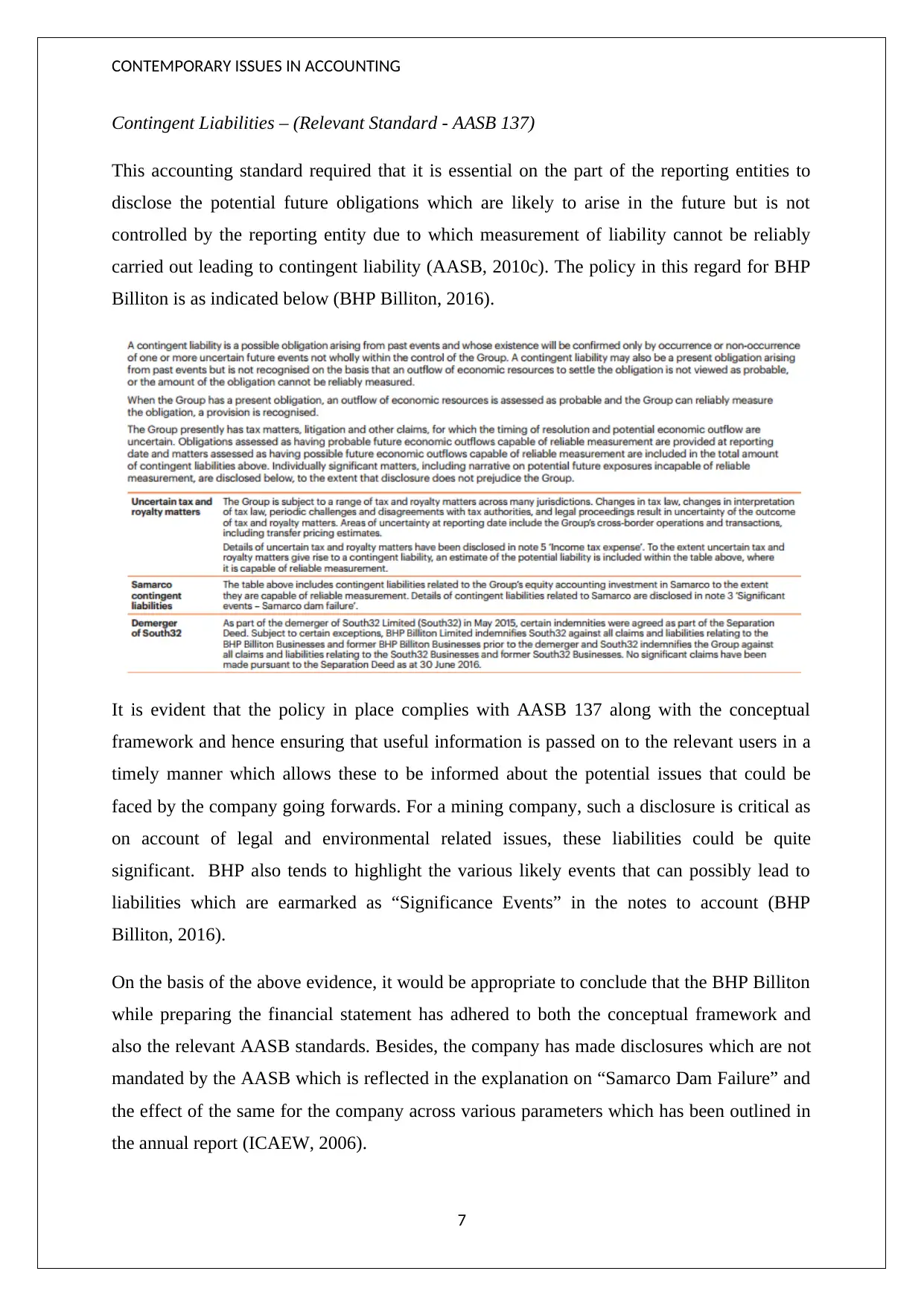

Contingent Liabilities – (Relevant Standard - AASB 137)

This accounting standard required that it is essential on the part of the reporting entities to

disclose the potential future obligations which are likely to arise in the future but is not

controlled by the reporting entity due to which measurement of liability cannot be reliably

carried out leading to contingent liability (AASB, 2010c). The policy in this regard for BHP

Billiton is as indicated below (BHP Billiton, 2016).

It is evident that the policy in place complies with AASB 137 along with the conceptual

framework and hence ensuring that useful information is passed on to the relevant users in a

timely manner which allows these to be informed about the potential issues that could be

faced by the company going forwards. For a mining company, such a disclosure is critical as

on account of legal and environmental related issues, these liabilities could be quite

significant. BHP also tends to highlight the various likely events that can possibly lead to

liabilities which are earmarked as “Significance Events” in the notes to account (BHP

Billiton, 2016).

On the basis of the above evidence, it would be appropriate to conclude that the BHP Billiton

while preparing the financial statement has adhered to both the conceptual framework and

also the relevant AASB standards. Besides, the company has made disclosures which are not

mandated by the AASB which is reflected in the explanation on “Samarco Dam Failure” and

the effect of the same for the company across various parameters which has been outlined in

the annual report (ICAEW, 2006).

7

Contingent Liabilities – (Relevant Standard - AASB 137)

This accounting standard required that it is essential on the part of the reporting entities to

disclose the potential future obligations which are likely to arise in the future but is not

controlled by the reporting entity due to which measurement of liability cannot be reliably

carried out leading to contingent liability (AASB, 2010c). The policy in this regard for BHP

Billiton is as indicated below (BHP Billiton, 2016).

It is evident that the policy in place complies with AASB 137 along with the conceptual

framework and hence ensuring that useful information is passed on to the relevant users in a

timely manner which allows these to be informed about the potential issues that could be

faced by the company going forwards. For a mining company, such a disclosure is critical as

on account of legal and environmental related issues, these liabilities could be quite

significant. BHP also tends to highlight the various likely events that can possibly lead to

liabilities which are earmarked as “Significance Events” in the notes to account (BHP

Billiton, 2016).

On the basis of the above evidence, it would be appropriate to conclude that the BHP Billiton

while preparing the financial statement has adhered to both the conceptual framework and

also the relevant AASB standards. Besides, the company has made disclosures which are not

mandated by the AASB which is reflected in the explanation on “Samarco Dam Failure” and

the effect of the same for the company across various parameters which has been outlined in

the annual report (ICAEW, 2006).

7

CONTEMPORARY ISSUES IN ACCOUNTING

Woolworths

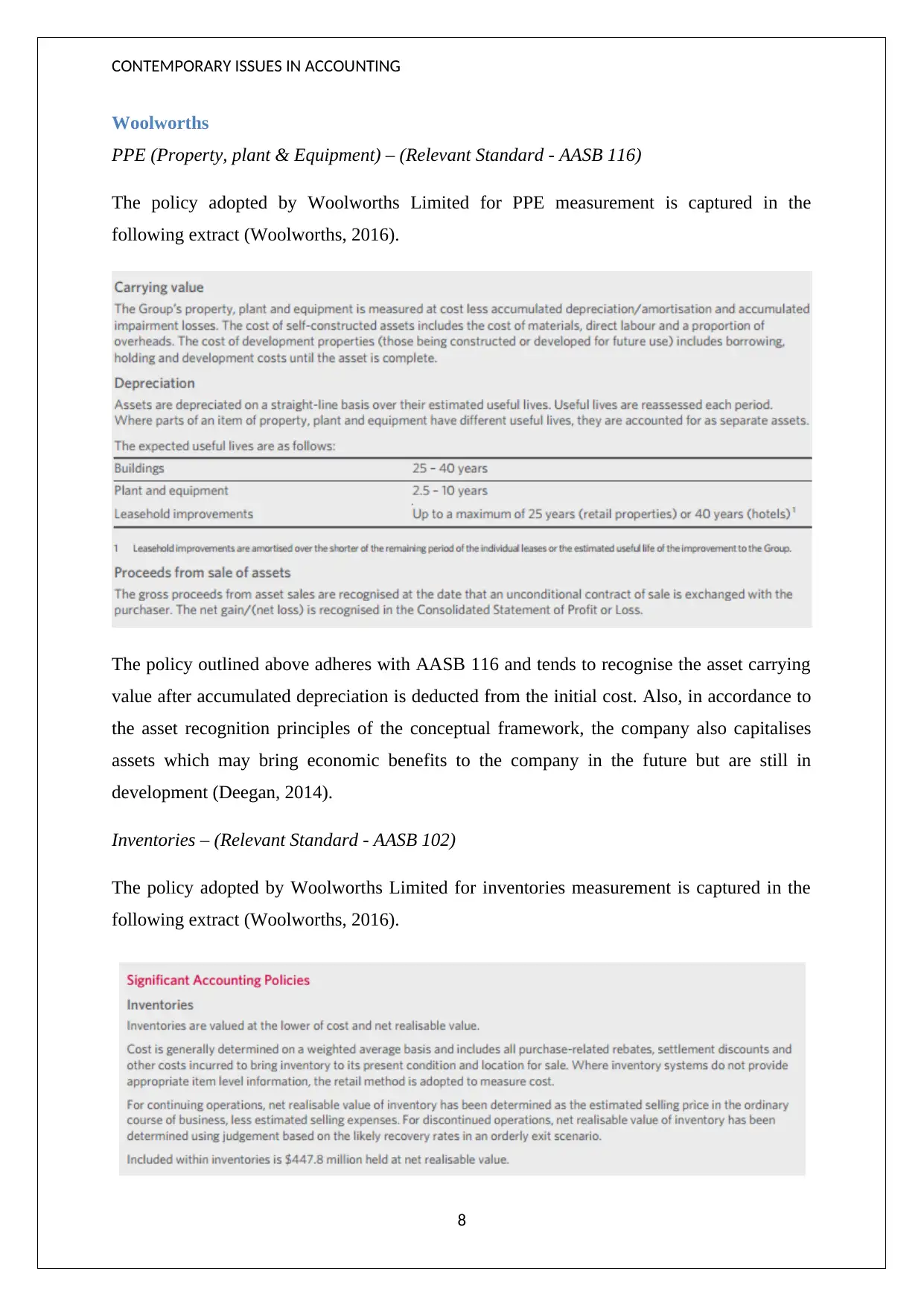

PPE (Property, plant & Equipment) – (Relevant Standard - AASB 116)

The policy adopted by Woolworths Limited for PPE measurement is captured in the

following extract (Woolworths, 2016).

The policy outlined above adheres with AASB 116 and tends to recognise the asset carrying

value after accumulated depreciation is deducted from the initial cost. Also, in accordance to

the asset recognition principles of the conceptual framework, the company also capitalises

assets which may bring economic benefits to the company in the future but are still in

development (Deegan, 2014).

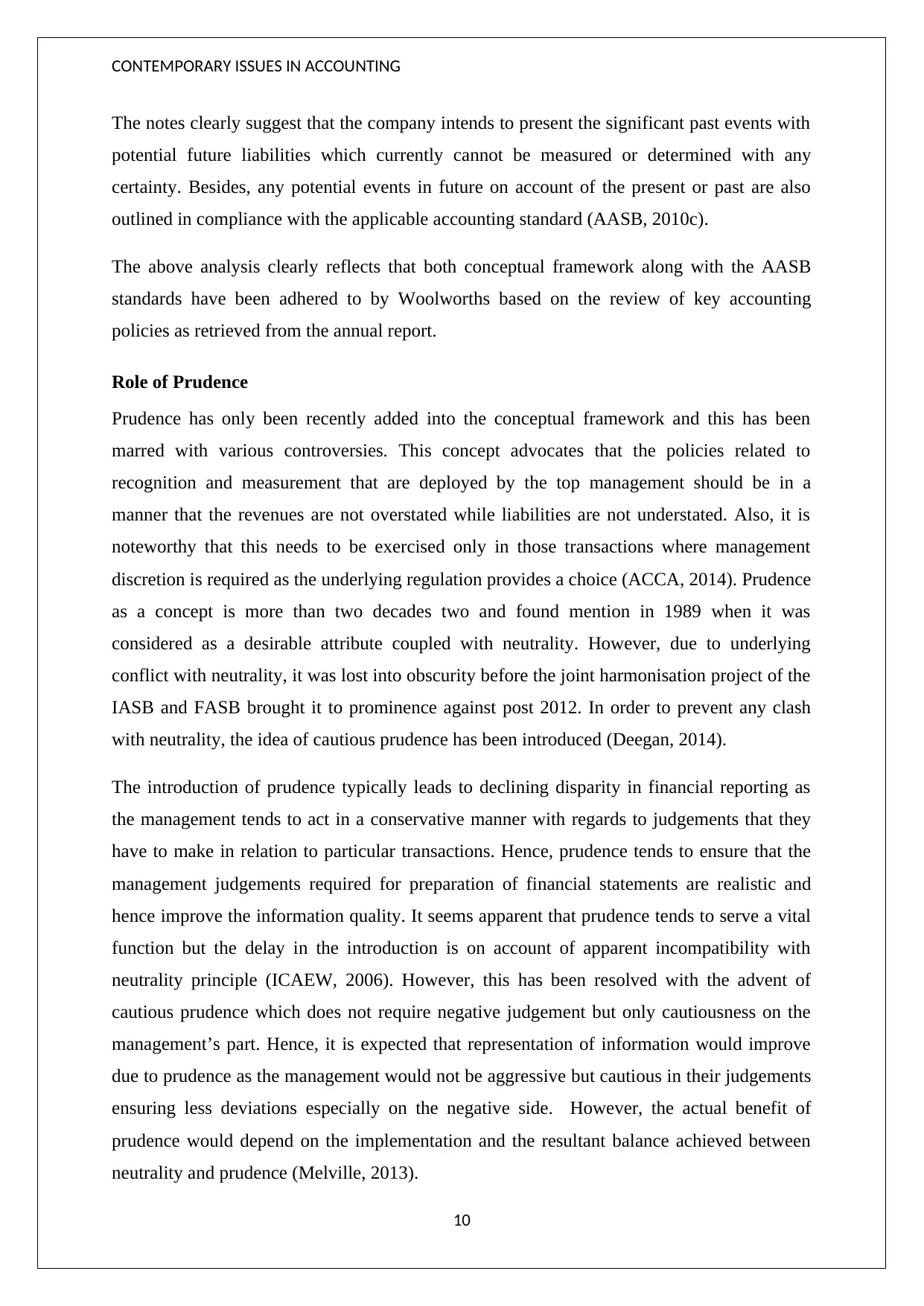

Inventories – (Relevant Standard - AASB 102)

The policy adopted by Woolworths Limited for inventories measurement is captured in the

following extract (Woolworths, 2016).

8

Woolworths

PPE (Property, plant & Equipment) – (Relevant Standard - AASB 116)

The policy adopted by Woolworths Limited for PPE measurement is captured in the

following extract (Woolworths, 2016).

The policy outlined above adheres with AASB 116 and tends to recognise the asset carrying

value after accumulated depreciation is deducted from the initial cost. Also, in accordance to

the asset recognition principles of the conceptual framework, the company also capitalises

assets which may bring economic benefits to the company in the future but are still in

development (Deegan, 2014).

Inventories – (Relevant Standard - AASB 102)

The policy adopted by Woolworths Limited for inventories measurement is captured in the

following extract (Woolworths, 2016).

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTEMPORARY ISSUES IN ACCOUNTING

It is apparent that the company has followed the applicable accounting standard that is

relevant for inventories which is AASB 102. In a bid to ensure that users have correct

information, the inventory is valued at the lower price of the cost and the net realisable value.

If this inventory would have been instead measured at cost, then the information expressed in

the books of account would not be correct (AASB, 2015).

Asset Impairment – (Relevant Standard -AASB 136)

The policy adopted by Woolworths Limited for asset impairment is captured in the following

extract (Woolworths, 2016).

AASB 136 norms have been complied with in relation to the asset impairment and clear

distinguishing between the impairment of intangible assets (infinite life) and goodwill has

been drawn with other assets. While the former is checked for impairment on a periodic

basis, the latter is checked for impairment as and when there is any development which

indicates towards the same (AASB, 2010b).

Contingent Liabilities – AASB 137

The note in place for Woolworths Limited for contingent liabilities is captured in the

following extract (Woolworths, 2016).

9

It is apparent that the company has followed the applicable accounting standard that is

relevant for inventories which is AASB 102. In a bid to ensure that users have correct

information, the inventory is valued at the lower price of the cost and the net realisable value.

If this inventory would have been instead measured at cost, then the information expressed in

the books of account would not be correct (AASB, 2015).

Asset Impairment – (Relevant Standard -AASB 136)

The policy adopted by Woolworths Limited for asset impairment is captured in the following

extract (Woolworths, 2016).

AASB 136 norms have been complied with in relation to the asset impairment and clear

distinguishing between the impairment of intangible assets (infinite life) and goodwill has

been drawn with other assets. While the former is checked for impairment on a periodic

basis, the latter is checked for impairment as and when there is any development which

indicates towards the same (AASB, 2010b).

Contingent Liabilities – AASB 137

The note in place for Woolworths Limited for contingent liabilities is captured in the

following extract (Woolworths, 2016).

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ISSUES IN ACCOUNTING

The notes clearly suggest that the company intends to present the significant past events with

potential future liabilities which currently cannot be measured or determined with any

certainty. Besides, any potential events in future on account of the present or past are also

outlined in compliance with the applicable accounting standard (AASB, 2010c).

The above analysis clearly reflects that both conceptual framework along with the AASB

standards have been adhered to by Woolworths based on the review of key accounting

policies as retrieved from the annual report.

Role of Prudence

Prudence has only been recently added into the conceptual framework and this has been

marred with various controversies. This concept advocates that the policies related to

recognition and measurement that are deployed by the top management should be in a

manner that the revenues are not overstated while liabilities are not understated. Also, it is

noteworthy that this needs to be exercised only in those transactions where management

discretion is required as the underlying regulation provides a choice (ACCA, 2014). Prudence

as a concept is more than two decades two and found mention in 1989 when it was

considered as a desirable attribute coupled with neutrality. However, due to underlying

conflict with neutrality, it was lost into obscurity before the joint harmonisation project of the

IASB and FASB brought it to prominence against post 2012. In order to prevent any clash

with neutrality, the idea of cautious prudence has been introduced (Deegan, 2014).

The introduction of prudence typically leads to declining disparity in financial reporting as

the management tends to act in a conservative manner with regards to judgements that they

have to make in relation to particular transactions. Hence, prudence tends to ensure that the

management judgements required for preparation of financial statements are realistic and

hence improve the information quality. It seems apparent that prudence tends to serve a vital

function but the delay in the introduction is on account of apparent incompatibility with

neutrality principle (ICAEW, 2006). However, this has been resolved with the advent of

cautious prudence which does not require negative judgement but only cautiousness on the

management’s part. Hence, it is expected that representation of information would improve

due to prudence as the management would not be aggressive but cautious in their judgements

ensuring less deviations especially on the negative side. However, the actual benefit of

prudence would depend on the implementation and the resultant balance achieved between

neutrality and prudence (Melville, 2013).

10

The notes clearly suggest that the company intends to present the significant past events with

potential future liabilities which currently cannot be measured or determined with any

certainty. Besides, any potential events in future on account of the present or past are also

outlined in compliance with the applicable accounting standard (AASB, 2010c).

The above analysis clearly reflects that both conceptual framework along with the AASB

standards have been adhered to by Woolworths based on the review of key accounting

policies as retrieved from the annual report.

Role of Prudence

Prudence has only been recently added into the conceptual framework and this has been

marred with various controversies. This concept advocates that the policies related to

recognition and measurement that are deployed by the top management should be in a

manner that the revenues are not overstated while liabilities are not understated. Also, it is

noteworthy that this needs to be exercised only in those transactions where management

discretion is required as the underlying regulation provides a choice (ACCA, 2014). Prudence

as a concept is more than two decades two and found mention in 1989 when it was

considered as a desirable attribute coupled with neutrality. However, due to underlying

conflict with neutrality, it was lost into obscurity before the joint harmonisation project of the

IASB and FASB brought it to prominence against post 2012. In order to prevent any clash

with neutrality, the idea of cautious prudence has been introduced (Deegan, 2014).

The introduction of prudence typically leads to declining disparity in financial reporting as

the management tends to act in a conservative manner with regards to judgements that they

have to make in relation to particular transactions. Hence, prudence tends to ensure that the

management judgements required for preparation of financial statements are realistic and

hence improve the information quality. It seems apparent that prudence tends to serve a vital

function but the delay in the introduction is on account of apparent incompatibility with

neutrality principle (ICAEW, 2006). However, this has been resolved with the advent of

cautious prudence which does not require negative judgement but only cautiousness on the

management’s part. Hence, it is expected that representation of information would improve

due to prudence as the management would not be aggressive but cautious in their judgements

ensuring less deviations especially on the negative side. However, the actual benefit of

prudence would depend on the implementation and the resultant balance achieved between

neutrality and prudence (Melville, 2013).

10

CONTEMPORARY ISSUES IN ACCOUNTING

Comparison of disclosures

In relation to the disclosures that have been made by the concerned companies, the

noteworthy points are highlighted below (BHP Billiton, 2016; Woolworths, 2016).

In context of segmental reporting, segment performance in accordance with product

and geography has been provided by both companies wherever the same is relevant

and sizable.

In context of the remuneration report, the top management’s remuneration has been

highlighted coupled with the key principles in accordance with which this has been

determined. This is true for both the companies.

In context of the director report, the management insight is particularly significant

which provides information about the current financial performance along with the

potential expectations from the future. This is true for both the companies.

However, on the whole it has been observed that for BHP Billiton, the financial

disclosures are more exhaustive in comparison with Woolworths. This is particularly

apparent in the detailed explanation with regards to why a particular accounting

policy has been deployed. Further, the significant events have been covered in great

detail by BHP Billiton which is apparent from the Samarco dam failure description.

This allows the users to be well informed and aids the objectives of corporate

reporting.

Conclusion

The discussion carried out above leads to the conclusion that both the given companies have

managed to comply with conceptual framework principles along with the applicable AASB

standards as has been demonstrated using certain key items accounting policies. The

introduction of cautious prudence in the folds of the conceptual framework is a positive

development which would ensure that more prudence is observed by the management while

using their discretion and judgement this leading to improvement in the standard of corporate

reporting which can be measures using the rate of discrepancies. Besides, the disclosures for

the two companies tend to be highly overlapping but overall, more exhaustive disclosures

have been found for BHP Billiton in comparison with Woolworths.

11

Comparison of disclosures

In relation to the disclosures that have been made by the concerned companies, the

noteworthy points are highlighted below (BHP Billiton, 2016; Woolworths, 2016).

In context of segmental reporting, segment performance in accordance with product

and geography has been provided by both companies wherever the same is relevant

and sizable.

In context of the remuneration report, the top management’s remuneration has been

highlighted coupled with the key principles in accordance with which this has been

determined. This is true for both the companies.

In context of the director report, the management insight is particularly significant

which provides information about the current financial performance along with the

potential expectations from the future. This is true for both the companies.

However, on the whole it has been observed that for BHP Billiton, the financial

disclosures are more exhaustive in comparison with Woolworths. This is particularly

apparent in the detailed explanation with regards to why a particular accounting

policy has been deployed. Further, the significant events have been covered in great

detail by BHP Billiton which is apparent from the Samarco dam failure description.

This allows the users to be well informed and aids the objectives of corporate

reporting.

Conclusion

The discussion carried out above leads to the conclusion that both the given companies have

managed to comply with conceptual framework principles along with the applicable AASB

standards as has been demonstrated using certain key items accounting policies. The

introduction of cautious prudence in the folds of the conceptual framework is a positive

development which would ensure that more prudence is observed by the management while

using their discretion and judgement this leading to improvement in the standard of corporate

reporting which can be measures using the rate of discrepancies. Besides, the disclosures for

the two companies tend to be highly overlapping but overall, more exhaustive disclosures

have been found for BHP Billiton in comparison with Woolworths.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

![Report: Contemporary Issues in Accounting - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fzz%2F9509ff46c136422d929242036a52e1cb.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.