Business Transactions & Accounting: Kool Kit Ltd Report, UWL

VerifiedAdded on 2023/04/06

|8

|1962

|98

Report

AI Summary

This report provides advice to Mr. Till, director of Kool Kit Ltd, a kilt manufacturing business, regarding accounting procedures. It covers the importance of accounting information, the differences between gross and net profit with numerical examples, and the distinction between current and non-current assets and liabilities. The report also explains the double-entry bookkeeping system, its origins with Luca Pacioli, and the concepts of debit and credit. The analysis uses examples such as Apple's financial data to illustrate key concepts. The report concludes that maintaining accurate books of accounts using the double-entry system is crucial for analyzing records and finalizing accounts.

Recording Business

Transaction

1

Transaction

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction......................................................................................................................................3

Main body........................................................................................................................................3

A. What is the importance of Accounting Information in a Business Organisation?..................3

B. Differences between Gross Profit vs Net Profit......................................................................4

C. Difference between non-current assets and current assets and non-current liabilities and

current liabilities..........................................................................................................................5

D. The meaning of the double entry bookkeeping system..........................................................6

E. Who invented this system originally?.....................................................................................6

F. What is meant by debit and credit?.........................................................................................7

Accounting entries...........................................................................................................................7

Conclusion.......................................................................................................................................7

References........................................................................................................................................8

2

Introduction......................................................................................................................................3

Main body........................................................................................................................................3

A. What is the importance of Accounting Information in a Business Organisation?..................3

B. Differences between Gross Profit vs Net Profit......................................................................4

C. Difference between non-current assets and current assets and non-current liabilities and

current liabilities..........................................................................................................................5

D. The meaning of the double entry bookkeeping system..........................................................6

E. Who invented this system originally?.....................................................................................6

F. What is meant by debit and credit?.........................................................................................7

Accounting entries...........................................................................................................................7

Conclusion.......................................................................................................................................7

References........................................................................................................................................8

2

Introduction

Business transactions are considered as the group activity or the events that ae measured

in form of monetary form and this helps in determining the financial position of the company.

This has been seen that all the business transaction in a company affects the accounting elements

which are considered as the Assets, Liabilities, capital, income and the expenses. Also all the

transactions may be classified into exchange transactions or non-exchange transactions (Buffum

and et. al., 2018). This report contains the advice that is given to Mr. Till who is director of small

business. They are engaged in the business of kilts and the company is named as Kool kit Ltd.

also the questions that would be answered in this report are importance of accounting

information in business organisation, difference between the gross profit and net profit. Also the

difference between non-current and current assets and liabilities would be discusses here in.

After this the report will move to meaning of double entry book keeping system. At last the

discussion would move to the meaning of what is meant by debit and credit.

Main body

A. What is the importance of Accounting Information in a Business Organisation?

This is important for the business organisation to record the accounting data which is

available to them so that it is easy for the stakeholders to know about the financial position of the

company (Collis, Holt and Hussey, 2017). The term accounting is considered as very common

term which helps the company to record the business information in the monetary form so that

the decisions can be made for increasing the profits of the company. To run the business

organisation it is important to record the data, analyse it and sustain it. Hence the accounting

information is very important for the company’s management so as to take decisions for the

better implementation of the strategies to expand the business and earn maximum revenue. This

is very important for the company as without the accounting information the company is not able

to form the strategies for the future business. There are various importance of accounting which

includes the following:

Helps to monitor the cash flows: The requirement of working capital and the liquid assets

can be predicted through the financial information of the company.

Income statement: this helps management in knowing the profits or loss the company is

gaining over its operating activities.

3

Business transactions are considered as the group activity or the events that ae measured

in form of monetary form and this helps in determining the financial position of the company.

This has been seen that all the business transaction in a company affects the accounting elements

which are considered as the Assets, Liabilities, capital, income and the expenses. Also all the

transactions may be classified into exchange transactions or non-exchange transactions (Buffum

and et. al., 2018). This report contains the advice that is given to Mr. Till who is director of small

business. They are engaged in the business of kilts and the company is named as Kool kit Ltd.

also the questions that would be answered in this report are importance of accounting

information in business organisation, difference between the gross profit and net profit. Also the

difference between non-current and current assets and liabilities would be discusses here in.

After this the report will move to meaning of double entry book keeping system. At last the

discussion would move to the meaning of what is meant by debit and credit.

Main body

A. What is the importance of Accounting Information in a Business Organisation?

This is important for the business organisation to record the accounting data which is

available to them so that it is easy for the stakeholders to know about the financial position of the

company (Collis, Holt and Hussey, 2017). The term accounting is considered as very common

term which helps the company to record the business information in the monetary form so that

the decisions can be made for increasing the profits of the company. To run the business

organisation it is important to record the data, analyse it and sustain it. Hence the accounting

information is very important for the company’s management so as to take decisions for the

better implementation of the strategies to expand the business and earn maximum revenue. This

is very important for the company as without the accounting information the company is not able

to form the strategies for the future business. There are various importance of accounting which

includes the following:

Helps to monitor the cash flows: The requirement of working capital and the liquid assets

can be predicted through the financial information of the company.

Income statement: this helps management in knowing the profits or loss the company is

gaining over its operating activities.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

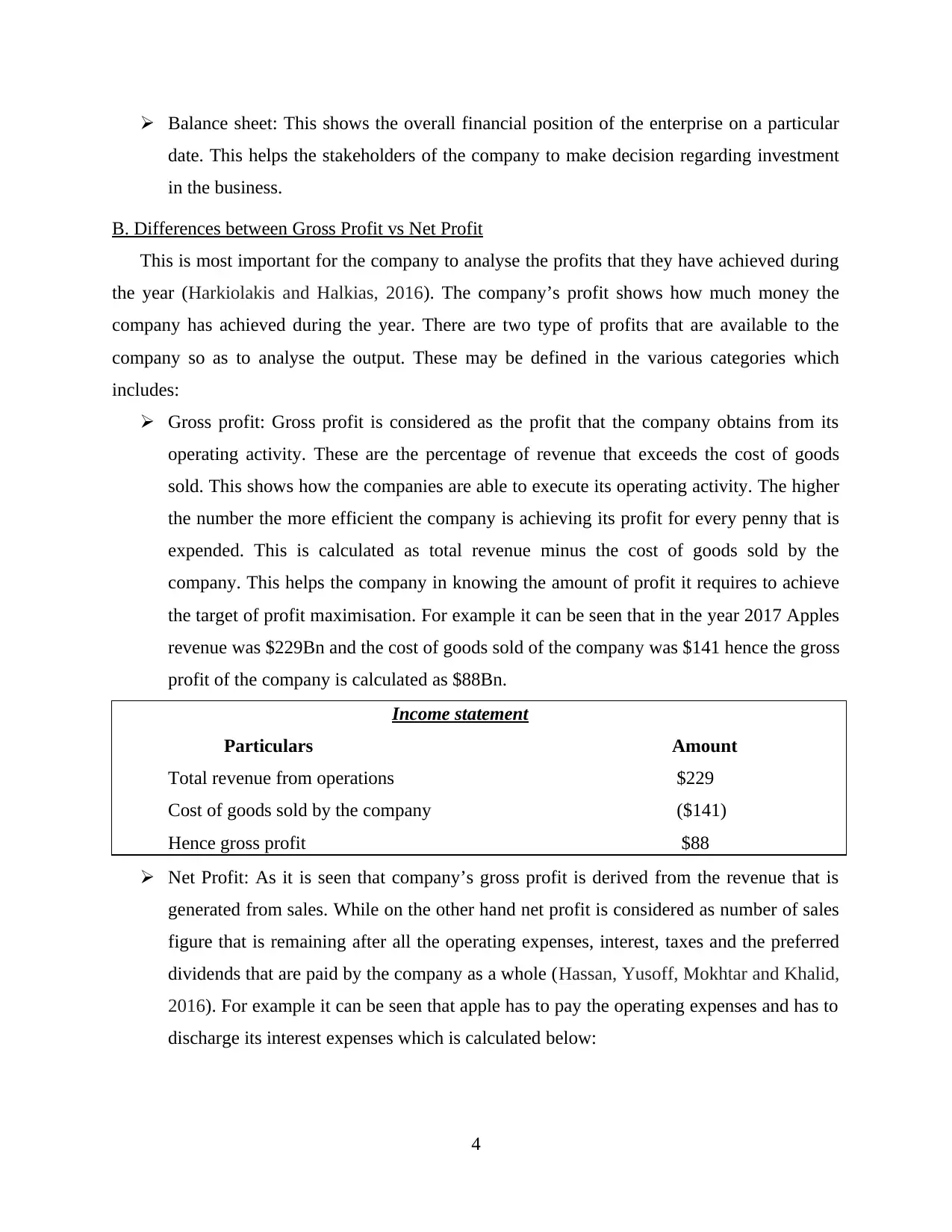

Balance sheet: This shows the overall financial position of the enterprise on a particular

date. This helps the stakeholders of the company to make decision regarding investment

in the business.

B. Differences between Gross Profit vs Net Profit

This is most important for the company to analyse the profits that they have achieved during

the year (Harkiolakis and Halkias, 2016). The company’s profit shows how much money the

company has achieved during the year. There are two type of profits that are available to the

company so as to analyse the output. These may be defined in the various categories which

includes:

Gross profit: Gross profit is considered as the profit that the company obtains from its

operating activity. These are the percentage of revenue that exceeds the cost of goods

sold. This shows how the companies are able to execute its operating activity. The higher

the number the more efficient the company is achieving its profit for every penny that is

expended. This is calculated as total revenue minus the cost of goods sold by the

company. This helps the company in knowing the amount of profit it requires to achieve

the target of profit maximisation. For example it can be seen that in the year 2017 Apples

revenue was $229Bn and the cost of goods sold of the company was $141 hence the gross

profit of the company is calculated as $88Bn.

Income statement

Particulars Amount

Total revenue from operations $229

Cost of goods sold by the company ($141)

Hence gross profit $88

Net Profit: As it is seen that company’s gross profit is derived from the revenue that is

generated from sales. While on the other hand net profit is considered as number of sales

figure that is remaining after all the operating expenses, interest, taxes and the preferred

dividends that are paid by the company as a whole (Hassan, Yusoff, Mokhtar and Khalid,

2016). For example it can be seen that apple has to pay the operating expenses and has to

discharge its interest expenses which is calculated below:

4

date. This helps the stakeholders of the company to make decision regarding investment

in the business.

B. Differences between Gross Profit vs Net Profit

This is most important for the company to analyse the profits that they have achieved during

the year (Harkiolakis and Halkias, 2016). The company’s profit shows how much money the

company has achieved during the year. There are two type of profits that are available to the

company so as to analyse the output. These may be defined in the various categories which

includes:

Gross profit: Gross profit is considered as the profit that the company obtains from its

operating activity. These are the percentage of revenue that exceeds the cost of goods

sold. This shows how the companies are able to execute its operating activity. The higher

the number the more efficient the company is achieving its profit for every penny that is

expended. This is calculated as total revenue minus the cost of goods sold by the

company. This helps the company in knowing the amount of profit it requires to achieve

the target of profit maximisation. For example it can be seen that in the year 2017 Apples

revenue was $229Bn and the cost of goods sold of the company was $141 hence the gross

profit of the company is calculated as $88Bn.

Income statement

Particulars Amount

Total revenue from operations $229

Cost of goods sold by the company ($141)

Hence gross profit $88

Net Profit: As it is seen that company’s gross profit is derived from the revenue that is

generated from sales. While on the other hand net profit is considered as number of sales

figure that is remaining after all the operating expenses, interest, taxes and the preferred

dividends that are paid by the company as a whole (Hassan, Yusoff, Mokhtar and Khalid,

2016). For example it can be seen that apple has to pay the operating expenses and has to

discharge its interest expenses which is calculated below:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

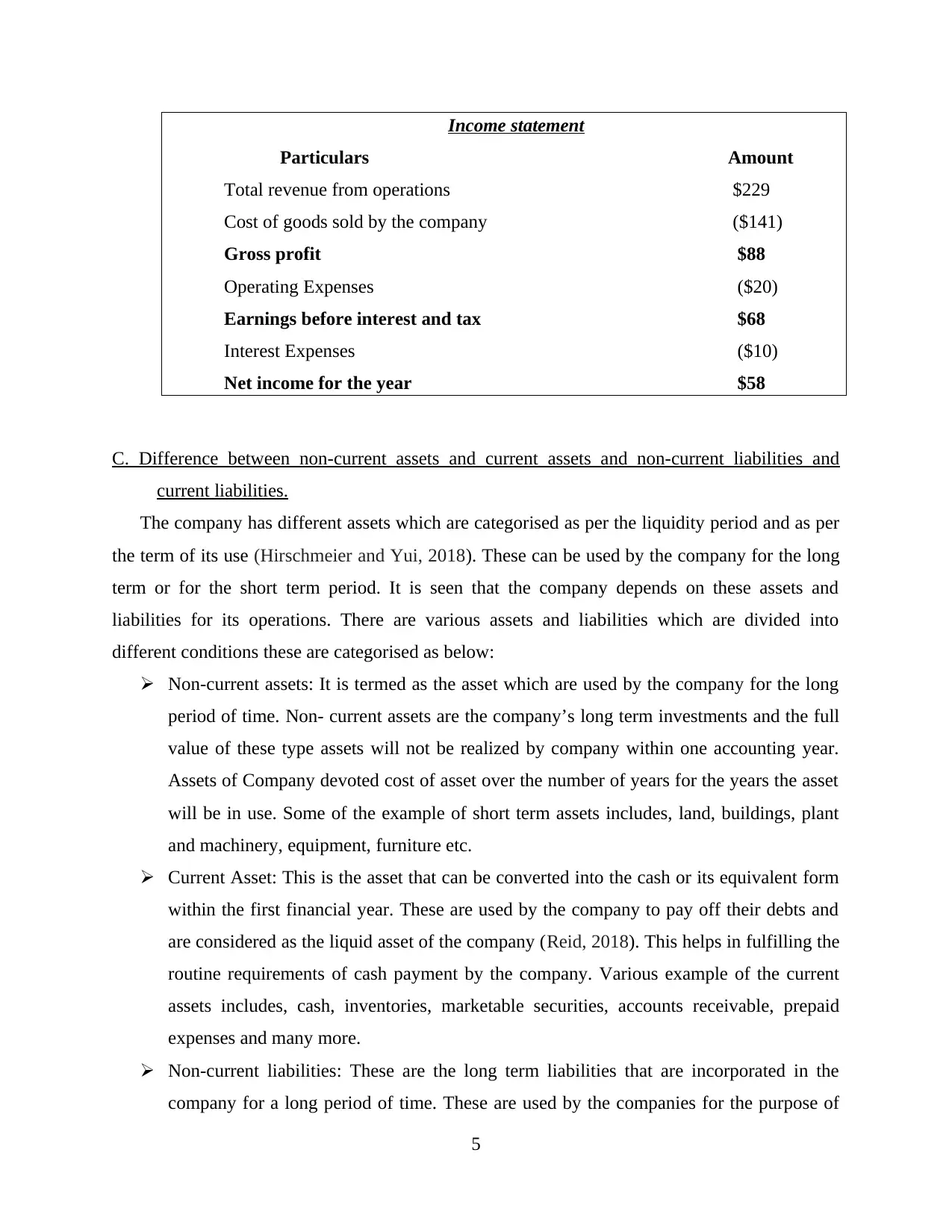

Income statement

Particulars Amount

Total revenue from operations $229

Cost of goods sold by the company ($141)

Gross profit $88

Operating Expenses ($20)

Earnings before interest and tax $68

Interest Expenses ($10)

Net income for the year $58

C. Difference between non-current assets and current assets and non-current liabilities and

current liabilities.

The company has different assets which are categorised as per the liquidity period and as per

the term of its use (Hirschmeier and Yui, 2018). These can be used by the company for the long

term or for the short term period. It is seen that the company depends on these assets and

liabilities for its operations. There are various assets and liabilities which are divided into

different conditions these are categorised as below:

Non-current assets: It is termed as the asset which are used by the company for the long

period of time. Non- current assets are the company’s long term investments and the full

value of these type assets will not be realized by company within one accounting year.

Assets of Company devoted cost of asset over the number of years for the years the asset

will be in use. Some of the example of short term assets includes, land, buildings, plant

and machinery, equipment, furniture etc.

Current Asset: This is the asset that can be converted into the cash or its equivalent form

within the first financial year. These are used by the company to pay off their debts and

are considered as the liquid asset of the company (Reid, 2018). This helps in fulfilling the

routine requirements of cash payment by the company. Various example of the current

assets includes, cash, inventories, marketable securities, accounts receivable, prepaid

expenses and many more.

Non-current liabilities: These are the long term liabilities that are incorporated in the

company for a long period of time. These are used by the companies for the purpose of

5

Particulars Amount

Total revenue from operations $229

Cost of goods sold by the company ($141)

Gross profit $88

Operating Expenses ($20)

Earnings before interest and tax $68

Interest Expenses ($10)

Net income for the year $58

C. Difference between non-current assets and current assets and non-current liabilities and

current liabilities.

The company has different assets which are categorised as per the liquidity period and as per

the term of its use (Hirschmeier and Yui, 2018). These can be used by the company for the long

term or for the short term period. It is seen that the company depends on these assets and

liabilities for its operations. There are various assets and liabilities which are divided into

different conditions these are categorised as below:

Non-current assets: It is termed as the asset which are used by the company for the long

period of time. Non- current assets are the company’s long term investments and the full

value of these type assets will not be realized by company within one accounting year.

Assets of Company devoted cost of asset over the number of years for the years the asset

will be in use. Some of the example of short term assets includes, land, buildings, plant

and machinery, equipment, furniture etc.

Current Asset: This is the asset that can be converted into the cash or its equivalent form

within the first financial year. These are used by the company to pay off their debts and

are considered as the liquid asset of the company (Reid, 2018). This helps in fulfilling the

routine requirements of cash payment by the company. Various example of the current

assets includes, cash, inventories, marketable securities, accounts receivable, prepaid

expenses and many more.

Non-current liabilities: These are the long term liabilities that are incorporated in the

company for a long period of time. These are used by the companies for the purpose of

5

expanding their business obligations. It includes various accounts such as long terms

loans, bonds payables, differed revenues, etc.

Current liabilities: These are considered as the liabilities that are to be paid within a

period of time. These are considered as the companies short term debt obligations which

are required to be paid within one fiscal year. Some of the examples of short term

liabilities includes trade payables, cash credit of the company, etc.

D. The meaning of the double entry bookkeeping system

The term double entry book keeping system is considered as the main system which helps

in providing a standard system of recording the accounting transaction in the books of accounts.

This system implies that each transaction in the accounting world must be recorded in a

minimum of two accounts (Robison and Ritchie, 2016). This implies that all the transactions

entered which are debited must have an equal credit in the books and vice versa. The equation

that is made through this system of accounting includes, (Assets= Liabilities+ Owners capital).

This equation suggest that company’s assets and liabilities should show always be balanced. In

this system entries are recorded first recorded in debit and then it is recorded in credit terms.

E. Who invented this system originally?

Double entry book keeping system was established in the Jewish community of the

medieval east. This has been seen that Luca Pacioli was one of the mathematician who started to

write about the double entry book keeping system with the collaboration of Leonardo da Vinci

(Trigo, Belfo and Estébanez, 2016). This book was published in Venice in the year 1494. As the

Luca Pacioli is known as the father of accounting and was considered as the one who published a

detailed description on the double entry system of accounting. As it is seen that Pacioli wrote the

book but Leonardo drew the practical illustration on double entry book system. The book was

bifurcated into various sections and the one who talked for this was about double entry book

system so as to achieve its advantage of describing the double entry book keeping system was

entitled as “Particularis de computis et scripturis”.

F. What is meant by debit and credit?

This is seen that the business transactions are considered as one of the events that are recorded in

the books of accounts (Stubkjær, 2017). When accounting for these transactions are done these

are recorded in debit or the credit side of the accounting. This can be bifurcated as,

6

loans, bonds payables, differed revenues, etc.

Current liabilities: These are considered as the liabilities that are to be paid within a

period of time. These are considered as the companies short term debt obligations which

are required to be paid within one fiscal year. Some of the examples of short term

liabilities includes trade payables, cash credit of the company, etc.

D. The meaning of the double entry bookkeeping system

The term double entry book keeping system is considered as the main system which helps

in providing a standard system of recording the accounting transaction in the books of accounts.

This system implies that each transaction in the accounting world must be recorded in a

minimum of two accounts (Robison and Ritchie, 2016). This implies that all the transactions

entered which are debited must have an equal credit in the books and vice versa. The equation

that is made through this system of accounting includes, (Assets= Liabilities+ Owners capital).

This equation suggest that company’s assets and liabilities should show always be balanced. In

this system entries are recorded first recorded in debit and then it is recorded in credit terms.

E. Who invented this system originally?

Double entry book keeping system was established in the Jewish community of the

medieval east. This has been seen that Luca Pacioli was one of the mathematician who started to

write about the double entry book keeping system with the collaboration of Leonardo da Vinci

(Trigo, Belfo and Estébanez, 2016). This book was published in Venice in the year 1494. As the

Luca Pacioli is known as the father of accounting and was considered as the one who published a

detailed description on the double entry system of accounting. As it is seen that Pacioli wrote the

book but Leonardo drew the practical illustration on double entry book system. The book was

bifurcated into various sections and the one who talked for this was about double entry book

system so as to achieve its advantage of describing the double entry book keeping system was

entitled as “Particularis de computis et scripturis”.

F. What is meant by debit and credit?

This is seen that the business transactions are considered as one of the events that are recorded in

the books of accounts (Stubkjær, 2017). When accounting for these transactions are done these

are recorded in debit or the credit side of the accounting. This can be bifurcated as,

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Debit entries: These are the entries which occurs when there is either the increase in the

asset or the expense of the company in an account, or these happens when there is an

decrease in an liability or equity account. These are entries are positioned in the left side

if the accounts.

Credit entries: These are the entries that occurs when there is increase in the liability or in

the equity account, also it increases the asset or the expense of the account (Wolff and

Chan, 2016). These are mainly positioned in the right side of the accounting entry.

Example of these are,

1. Cash A/C…………………………… Dr. $1000

To Sales A/C…………………Cr. $100

Accounting entries

Refer Excel sheet.

Conclusion

From the above report it is concluded that recording accounting transactions are

considered as one of the important part of the accounting. It is important for the company to

maintain the books of accounts so as to compute the transactions in best and suitable manner.

Also this has been seen that the double entry book keeping system is considered as one of main

feature of recording the accounts in the books. This makes it easier to analyse the records and

finalize the accounts.

7

asset or the expense of the company in an account, or these happens when there is an

decrease in an liability or equity account. These are entries are positioned in the left side

if the accounts.

Credit entries: These are the entries that occurs when there is increase in the liability or in

the equity account, also it increases the asset or the expense of the account (Wolff and

Chan, 2016). These are mainly positioned in the right side of the accounting entry.

Example of these are,

1. Cash A/C…………………………… Dr. $1000

To Sales A/C…………………Cr. $100

Accounting entries

Refer Excel sheet.

Conclusion

From the above report it is concluded that recording accounting transactions are

considered as one of the important part of the accounting. It is important for the company to

maintain the books of accounts so as to compute the transactions in best and suitable manner.

Also this has been seen that the double entry book keeping system is considered as one of main

feature of recording the accounts in the books. This makes it easier to analyse the records and

finalize the accounts.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Books and journals

Buffum, C., Levy, J., Calvin, N., Gould, C., King, J. and Lipin, D., EMC IP Holding Co LLC,

2018. Dialog-based voiceprint security for business transactions. U.S. Patent Application

10/083,695.

Collis, J., Holt, A. and Hussey, R., 2017. Business accounting. Palgrave.

Harkiolakis, N. and Halkias, D., 2016. E-negotiations: networking and cross-cultural business

transactions. Routledge.

Hassan, K.H., Yusoff, S.S.A., Mokhtar, M.F. and Khalid, K.A.T., 2016. The use of technology in

the transformation of business dispute resolution. European journal of law and economics. 42(2).

Pp.369-381.

Hirschmeier, J. and Yui, T., 2018. The development of Japanese business, 1600-1980.

Routledge.

Reid, W., 2018. The meaning of company accounts. Routledge.

Robison, L.J. and Ritchie, B.K., 2016. Relationship economics: The social capital paradigm and

its application to business, politics and other transactions. Routledge.

Stubkjær, E., 2017. Modelling real property transactions. In The Ontology and Modelling of Real

Estate Transactions (pp. 1-21). Routledge.

Trigo, A., Belfo, F. and Estébanez, R.P., 2016. Accounting Information Systems: evolving

towards a business process oriented accounting. Procedia Computer Science. 100. pp.987-994.

Wolff, L.C. and Chan, J., 2016. Case Study: Flipped Classrooms for ‘The Law of International

Business Transactions II’. In Flipped Classrooms for Legal Education (pp. 81-107). Springer,

Singapore.

8

Books and journals

Buffum, C., Levy, J., Calvin, N., Gould, C., King, J. and Lipin, D., EMC IP Holding Co LLC,

2018. Dialog-based voiceprint security for business transactions. U.S. Patent Application

10/083,695.

Collis, J., Holt, A. and Hussey, R., 2017. Business accounting. Palgrave.

Harkiolakis, N. and Halkias, D., 2016. E-negotiations: networking and cross-cultural business

transactions. Routledge.

Hassan, K.H., Yusoff, S.S.A., Mokhtar, M.F. and Khalid, K.A.T., 2016. The use of technology in

the transformation of business dispute resolution. European journal of law and economics. 42(2).

Pp.369-381.

Hirschmeier, J. and Yui, T., 2018. The development of Japanese business, 1600-1980.

Routledge.

Reid, W., 2018. The meaning of company accounts. Routledge.

Robison, L.J. and Ritchie, B.K., 2016. Relationship economics: The social capital paradigm and

its application to business, politics and other transactions. Routledge.

Stubkjær, E., 2017. Modelling real property transactions. In The Ontology and Modelling of Real

Estate Transactions (pp. 1-21). Routledge.

Trigo, A., Belfo, F. and Estébanez, R.P., 2016. Accounting Information Systems: evolving

towards a business process oriented accounting. Procedia Computer Science. 100. pp.987-994.

Wolff, L.C. and Chan, J., 2016. Case Study: Flipped Classrooms for ‘The Law of International

Business Transactions II’. In Flipped Classrooms for Legal Education (pp. 81-107). Springer,

Singapore.

8

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.