Accounting for Management (MCC5212) Assignment Solution Analysis

VerifiedAdded on 2022/09/08

|11

|1342

|16

Homework Assignment

AI Summary

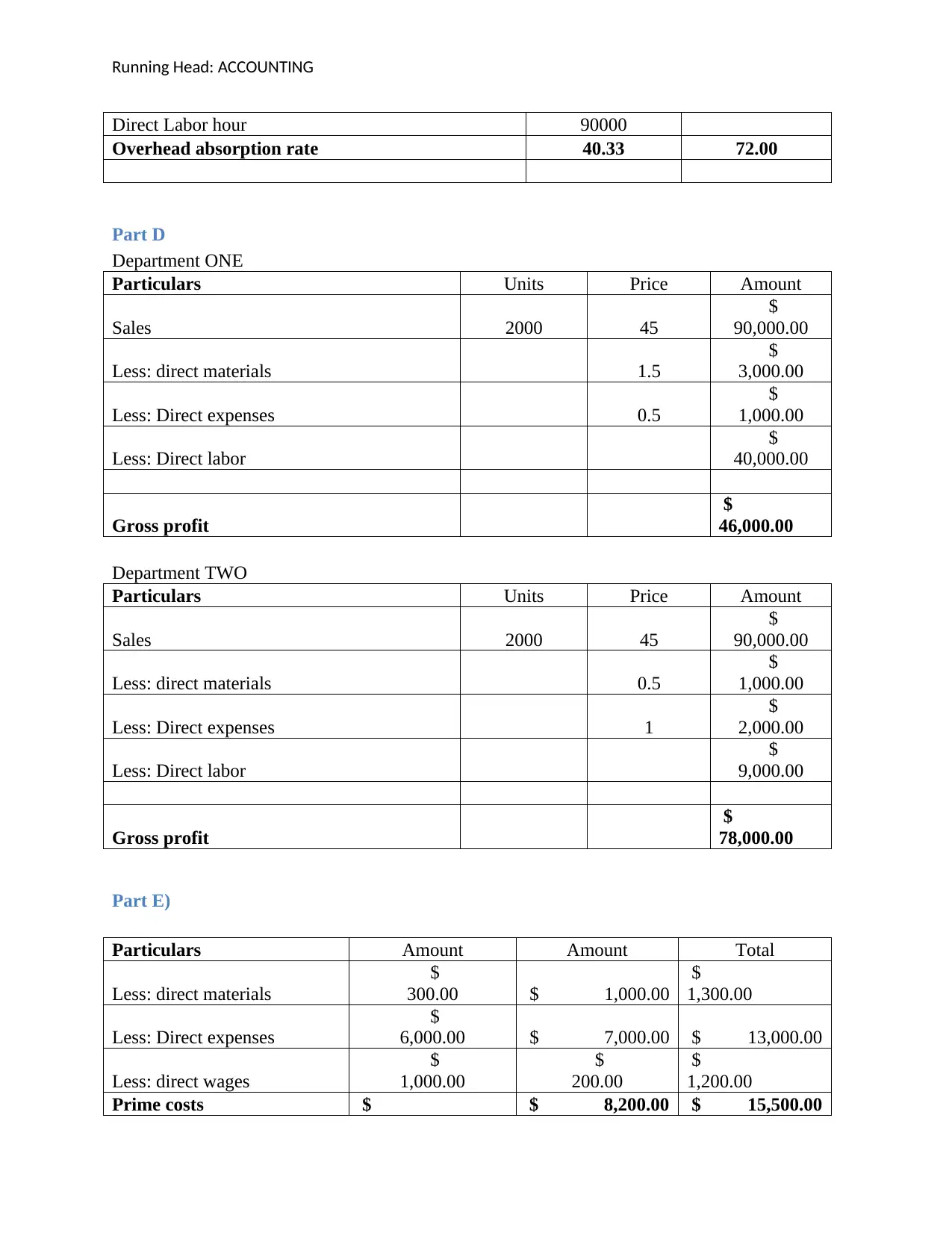

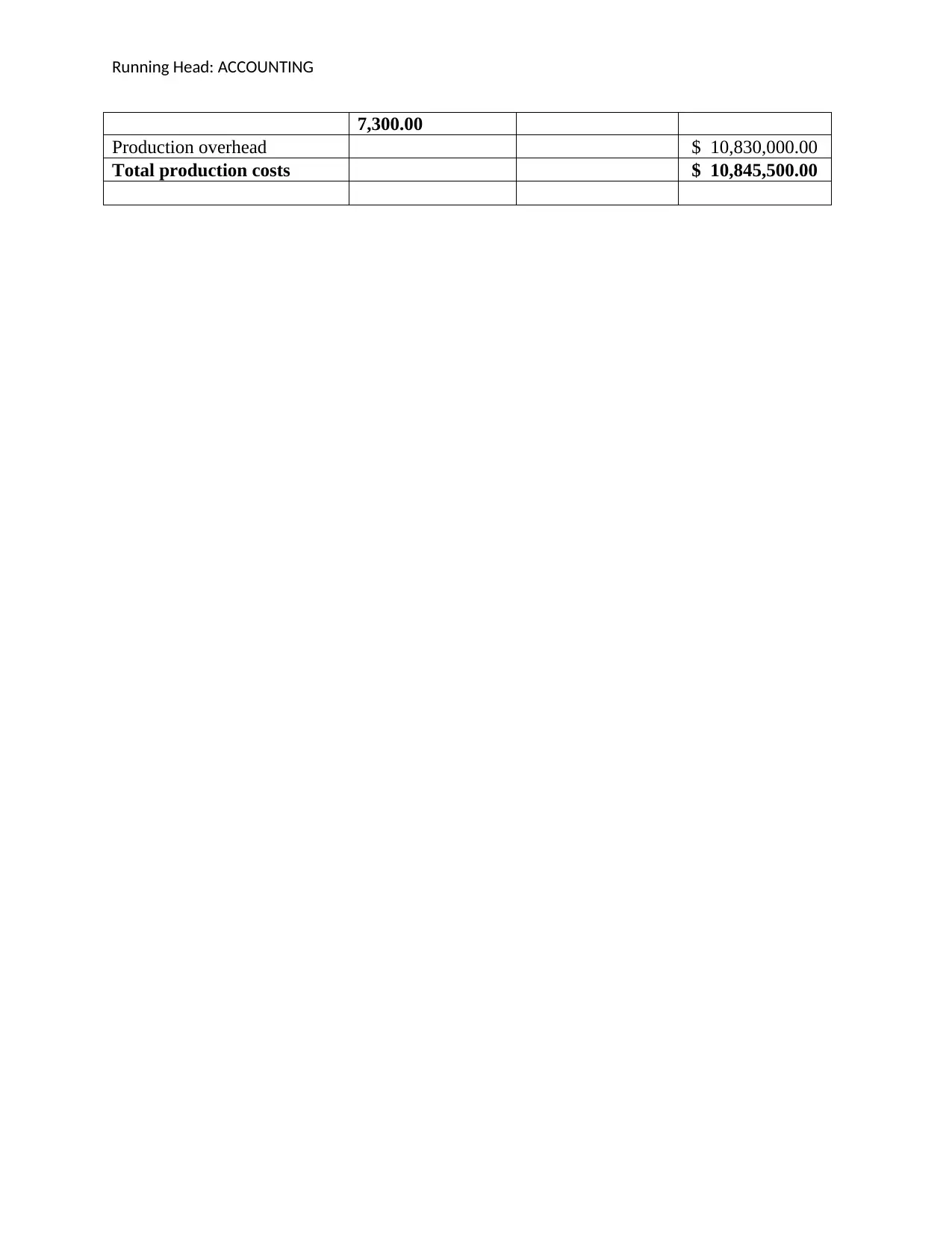

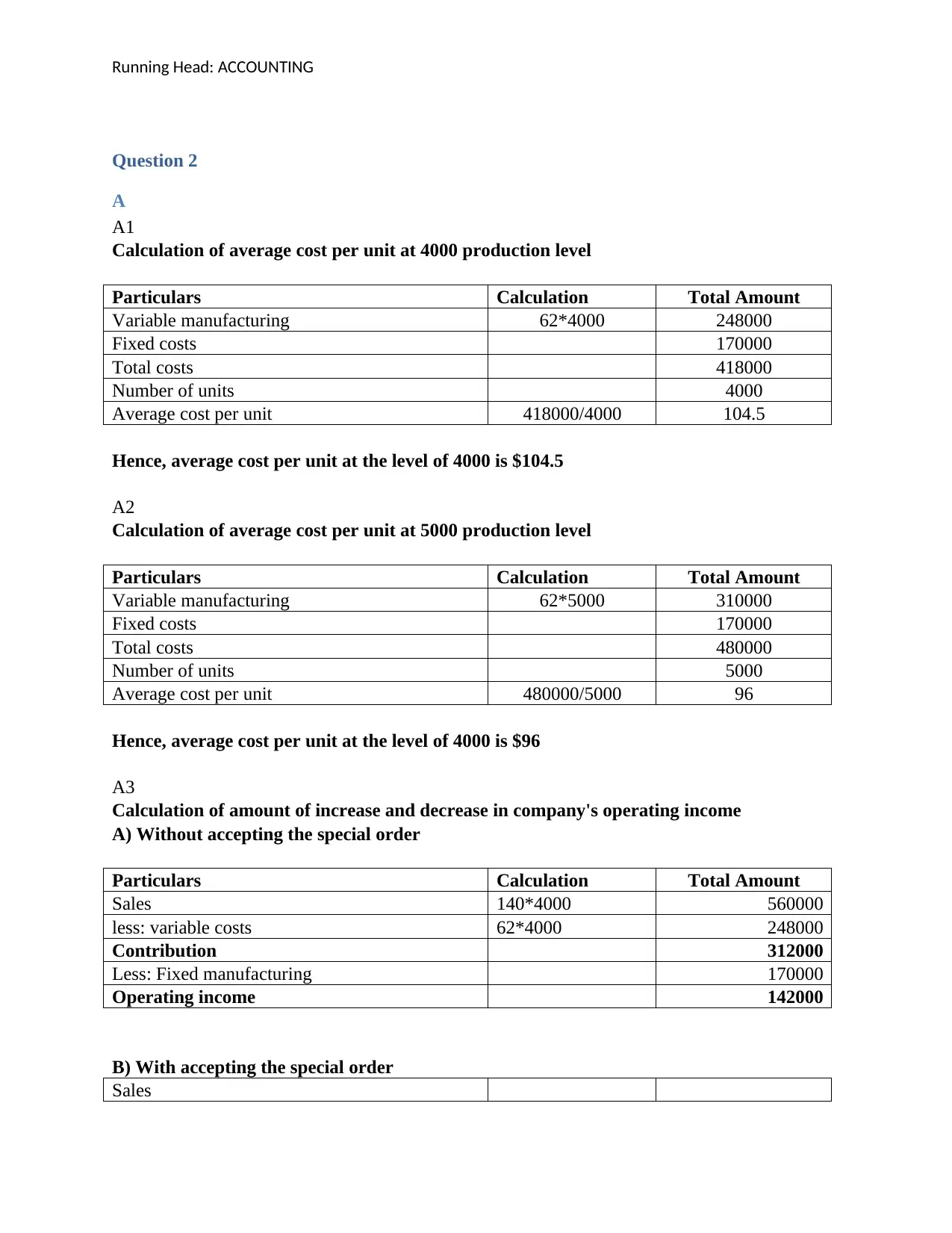

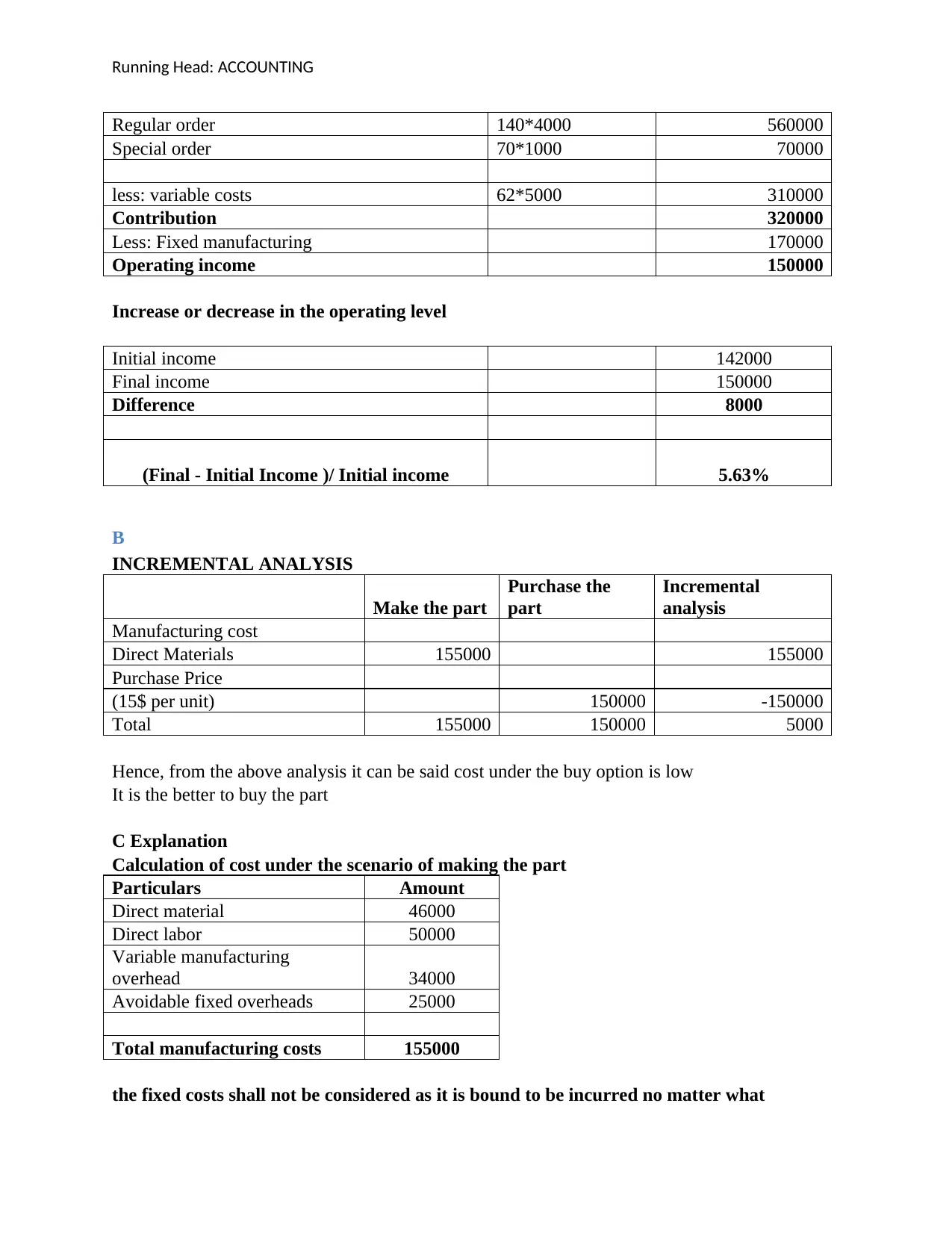

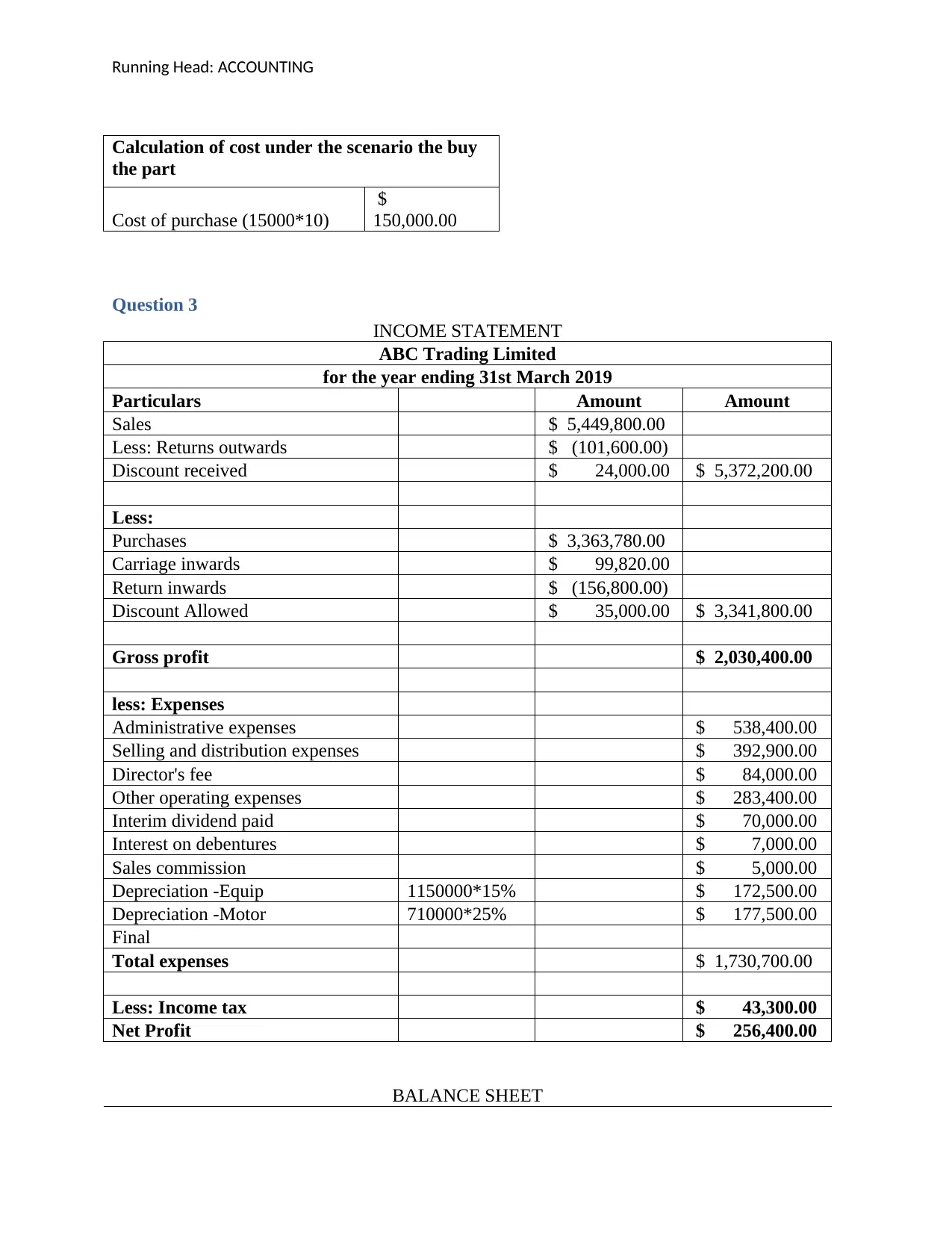

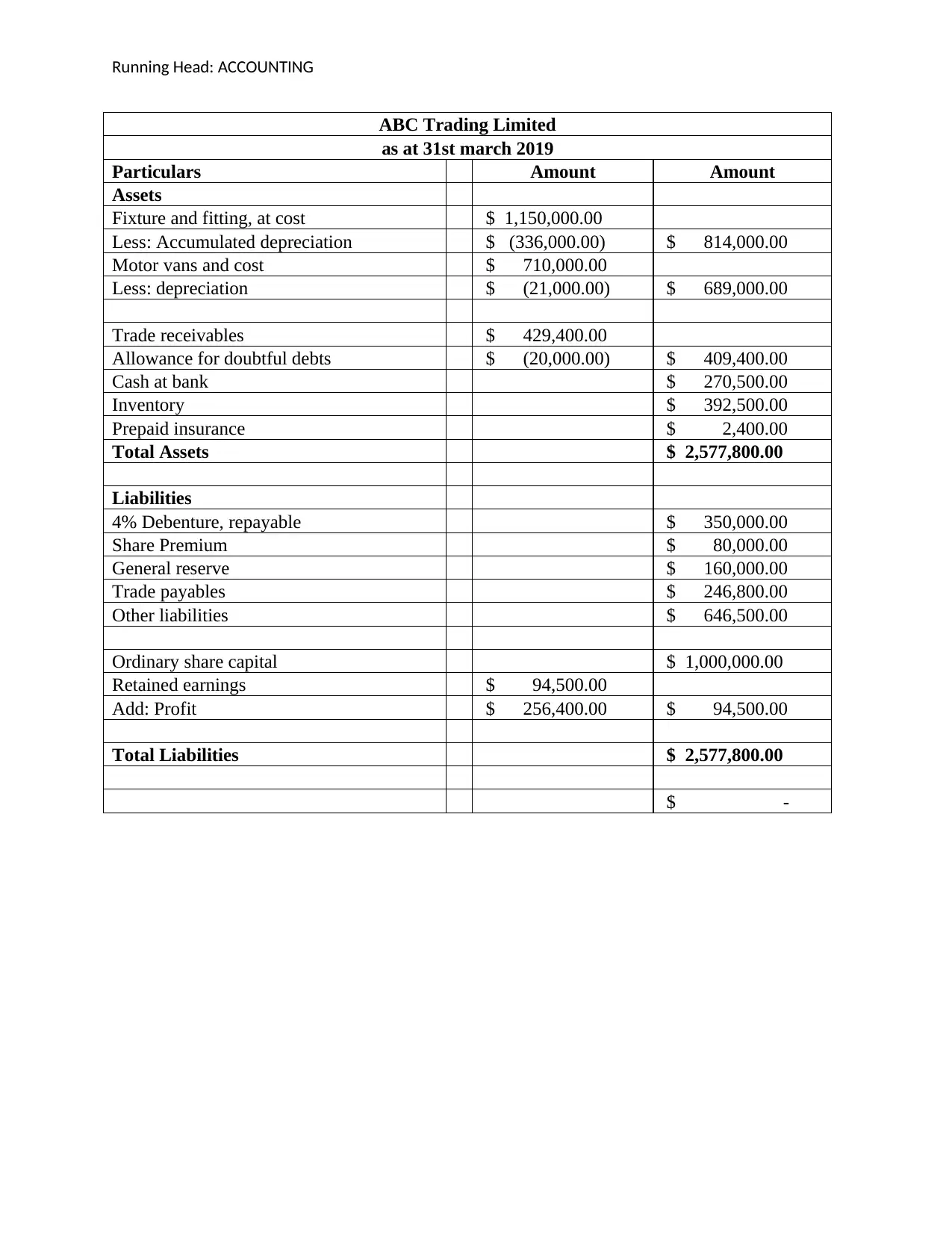

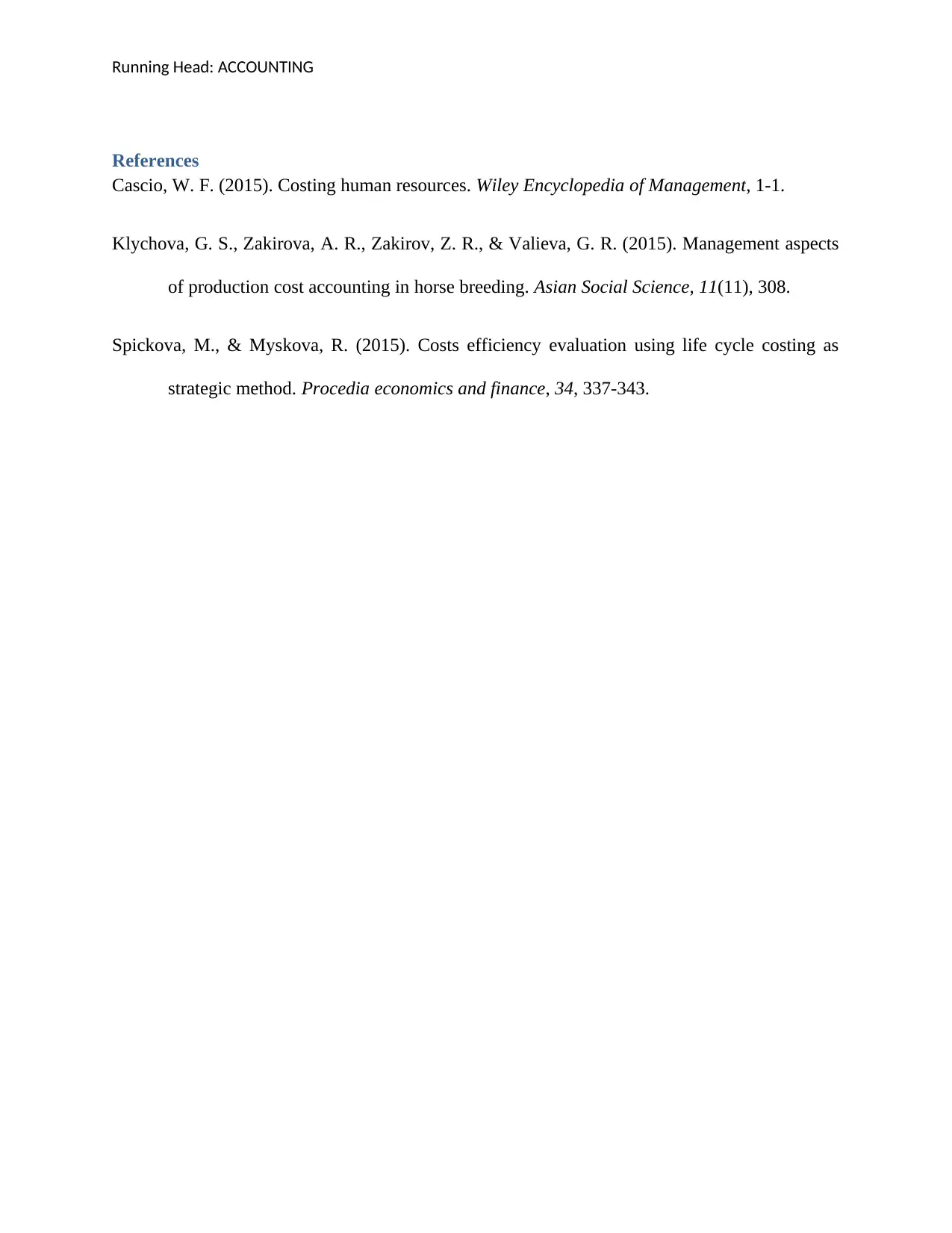

This document presents a comprehensive solution to an accounting assignment focused on Kwong Tin Company. The solution encompasses various aspects of cost accounting, including the differentiation between product and period costs, variable, fixed, and semi-variable costs. It provides detailed calculations for budgeted prime costs, production overhead absorption rates, and the preparation of income statements and balance sheets. The analysis includes calculations for average costs at different production levels, incremental analysis for make-or-buy decisions, and a complete income statement and balance sheet for ABC Trading Limited. The assignment covers topics such as cost classification, overhead allocation, and financial statement preparation, providing a thorough understanding of accounting principles and their practical application in management accounting.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.