BACC1AMD - Accounting for Management Decisions, La Trobe Melbourne

VerifiedAdded on 2023/06/13

|16

|2801

|147

Report

AI Summary

This assignment solution delves into accounting for management decisions, presenting financial transactions, charts of accounts, journal entries, and income statements for three players in a simulated business scenario. It covers real estate investment analysis, discussing benefits and drawbacks, and addresses the accounting implications of environmental costs, particularly natural disasters. The report includes detailed financial data and explores investment strategies, attracting developers, corporate occupiers, and consumers. It examines environmental cost accounting and responsibility towards all.

Running head: ACCOUNTING FOR MANAGEMENT DECISIONS

Accounting for management decisions

University Name

Student Name

Authors’ Note

Accounting for management decisions

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2ACCOUNTING FOR MANAGEMENT DECISIONS

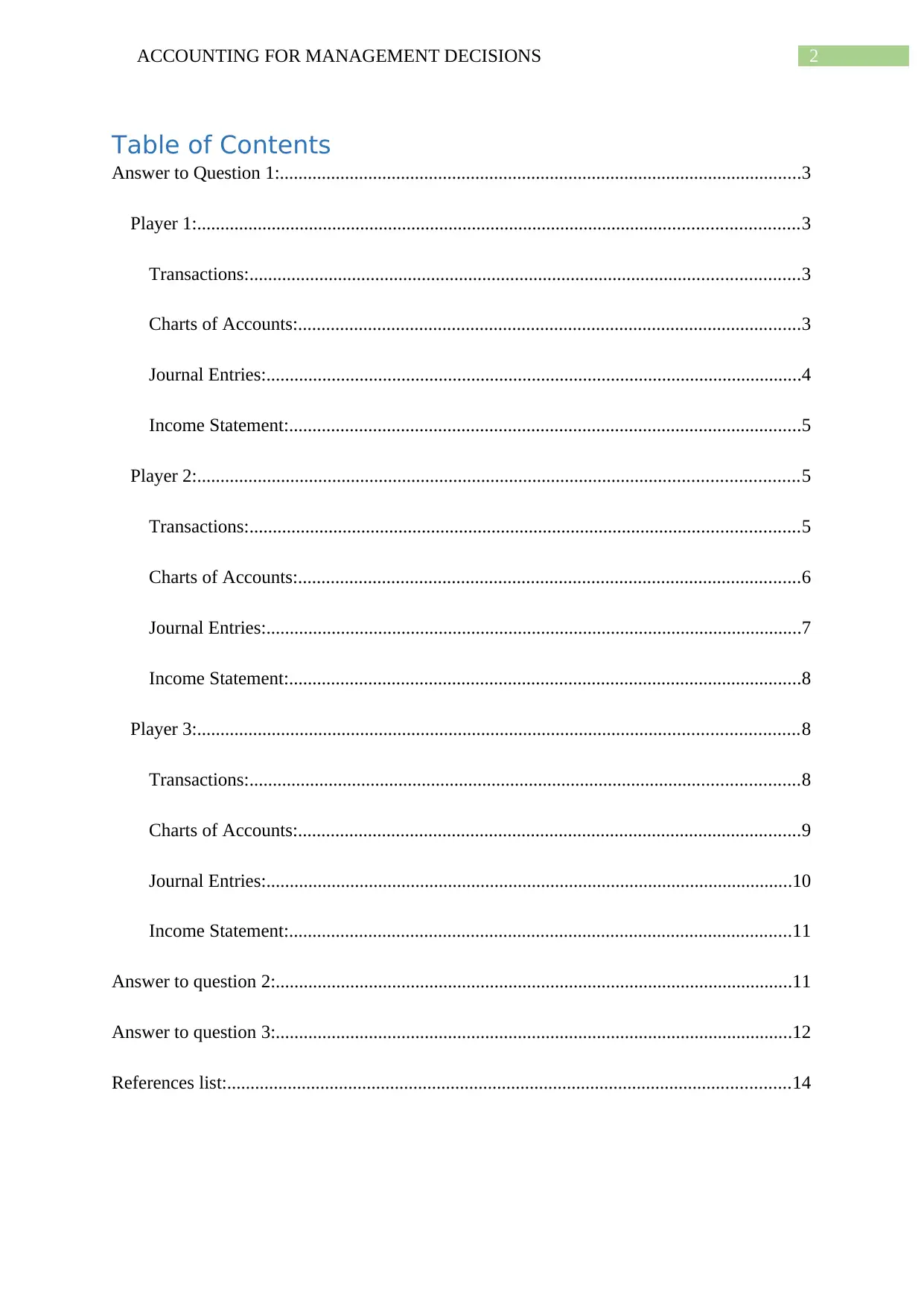

Table of Contents

Answer to Question 1:................................................................................................................3

Player 1:.................................................................................................................................3

Transactions:......................................................................................................................3

Charts of Accounts:............................................................................................................3

Journal Entries:...................................................................................................................4

Income Statement:..............................................................................................................5

Player 2:.................................................................................................................................5

Transactions:......................................................................................................................5

Charts of Accounts:............................................................................................................6

Journal Entries:...................................................................................................................7

Income Statement:..............................................................................................................8

Player 3:.................................................................................................................................8

Transactions:......................................................................................................................8

Charts of Accounts:............................................................................................................9

Journal Entries:.................................................................................................................10

Income Statement:............................................................................................................11

Answer to question 2:...............................................................................................................11

Answer to question 3:...............................................................................................................12

References list:.........................................................................................................................14

Table of Contents

Answer to Question 1:................................................................................................................3

Player 1:.................................................................................................................................3

Transactions:......................................................................................................................3

Charts of Accounts:............................................................................................................3

Journal Entries:...................................................................................................................4

Income Statement:..............................................................................................................5

Player 2:.................................................................................................................................5

Transactions:......................................................................................................................5

Charts of Accounts:............................................................................................................6

Journal Entries:...................................................................................................................7

Income Statement:..............................................................................................................8

Player 3:.................................................................................................................................8

Transactions:......................................................................................................................8

Charts of Accounts:............................................................................................................9

Journal Entries:.................................................................................................................10

Income Statement:............................................................................................................11

Answer to question 2:...............................................................................................................11

Answer to question 3:...............................................................................................................12

References list:.........................................................................................................................14

3ACCOUNTING FOR MANAGEMENT DECISIONS

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4ACCOUNTING FOR MANAGEMENT DECISIONS

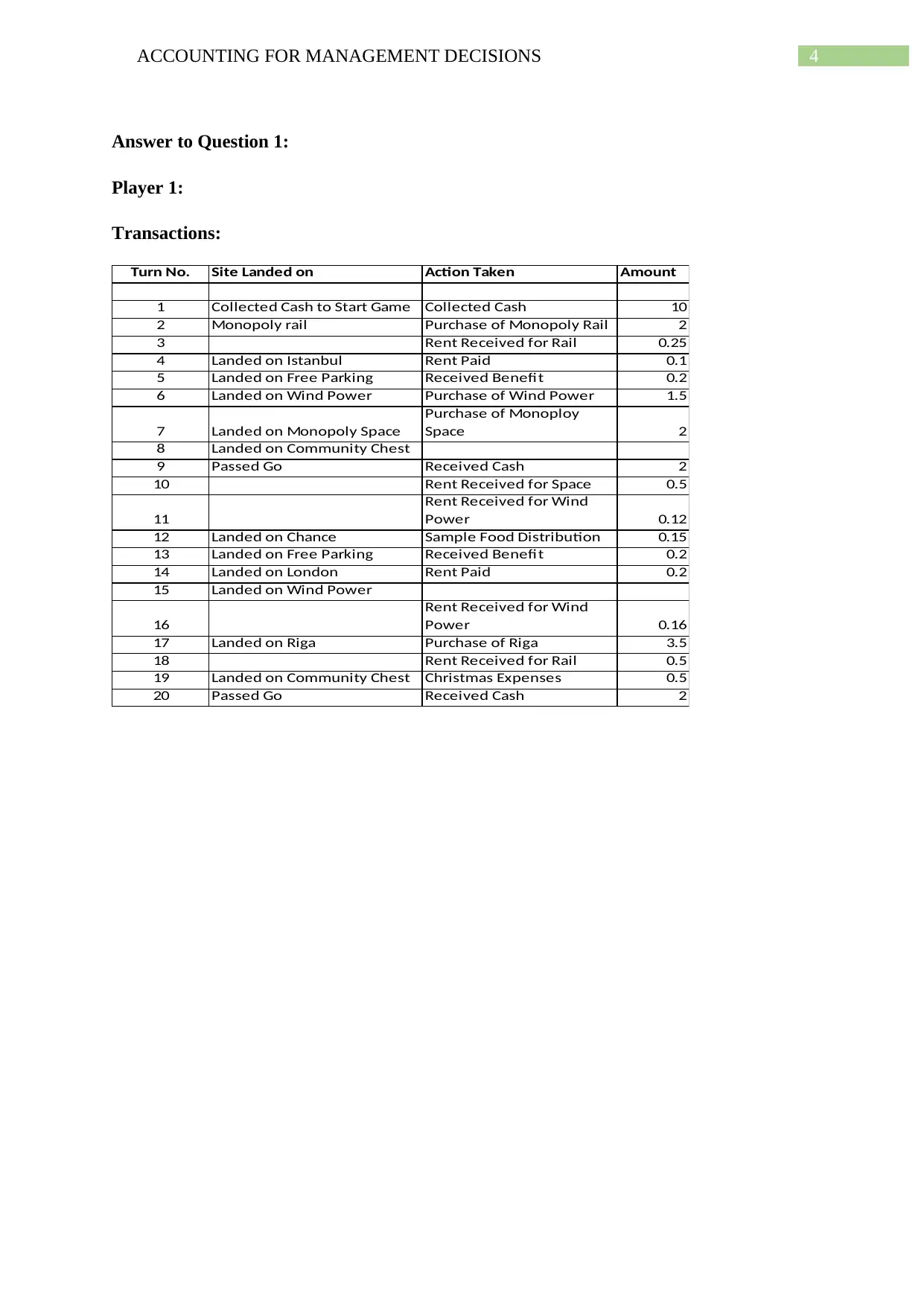

Answer to Question 1:

Player 1:

Transactions:

Turn No. Site Landed on Action Taken Amount

1 Collected Cash to Start Game Collected Cash 10

2 Monopoly rail Purchase of Monopoly Rail 2

3 Rent Received for Rail 0.25

4 Landed on Istanbul Rent Paid 0.1

5 Landed on Free Parking Received Benefit 0.2

6 Landed on Wind Power Purchase of Wind Power 1.5

7 Landed on Monopoly Space

Purchase of Monoploy

Space 2

8 Landed on Community Chest

9 Passed Go Received Cash 2

10 Rent Received for Space 0.5

11

Rent Received for Wind

Power 0.12

12 Landed on Chance Sample Food Distribution 0.15

13 Landed on Free Parking Received Benefit 0.2

14 Landed on London Rent Paid 0.2

15 Landed on Wind Power

16

Rent Received for Wind

Power 0.16

17 Landed on Riga Purchase of Riga 3.5

18 Rent Received for Rail 0.5

19 Landed on Community Chest Christmas Expenses 0.5

20 Passed Go Received Cash 2

Answer to Question 1:

Player 1:

Transactions:

Turn No. Site Landed on Action Taken Amount

1 Collected Cash to Start Game Collected Cash 10

2 Monopoly rail Purchase of Monopoly Rail 2

3 Rent Received for Rail 0.25

4 Landed on Istanbul Rent Paid 0.1

5 Landed on Free Parking Received Benefit 0.2

6 Landed on Wind Power Purchase of Wind Power 1.5

7 Landed on Monopoly Space

Purchase of Monoploy

Space 2

8 Landed on Community Chest

9 Passed Go Received Cash 2

10 Rent Received for Space 0.5

11

Rent Received for Wind

Power 0.12

12 Landed on Chance Sample Food Distribution 0.15

13 Landed on Free Parking Received Benefit 0.2

14 Landed on London Rent Paid 0.2

15 Landed on Wind Power

16

Rent Received for Wind

Power 0.16

17 Landed on Riga Purchase of Riga 3.5

18 Rent Received for Rail 0.5

19 Landed on Community Chest Christmas Expenses 0.5

20 Passed Go Received Cash 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5ACCOUNTING FOR MANAGEMENT DECISIONS

Charts of Accounts:

Account No. Account Name

1001 Cash A/c.

1002 Investment in Monopoly Rail A/c.

1003 Investment in Wind Power A/c.

1004 Investment in Monopoly Space A/c.

1005 Investment in Riga A/c.

3001 Capital A/c.

4001 Rent Revenue A/c.

4002 Revenue from Go A/c.

4003 Revenue from Free Parking A/c.

4004 Profit from Non-Current Assets A/c.

5001 Rent Expenses A/c.

5002 Legal Charges A/c.

5003 Sample Food Distribuition A/c.

5004 Christmas Expense A/c.

Charts of Accounts:

Account No. Account Name

1001 Cash A/c.

1002 Investment in Monopoly Rail A/c.

1003 Investment in Wind Power A/c.

1004 Investment in Monopoly Space A/c.

1005 Investment in Riga A/c.

3001 Capital A/c.

4001 Rent Revenue A/c.

4002 Revenue from Go A/c.

4003 Revenue from Free Parking A/c.

4004 Profit from Non-Current Assets A/c.

5001 Rent Expenses A/c.

5002 Legal Charges A/c.

5003 Sample Food Distribuition A/c.

5004 Christmas Expense A/c.

6ACCOUNTING FOR MANAGEMENT DECISIONS

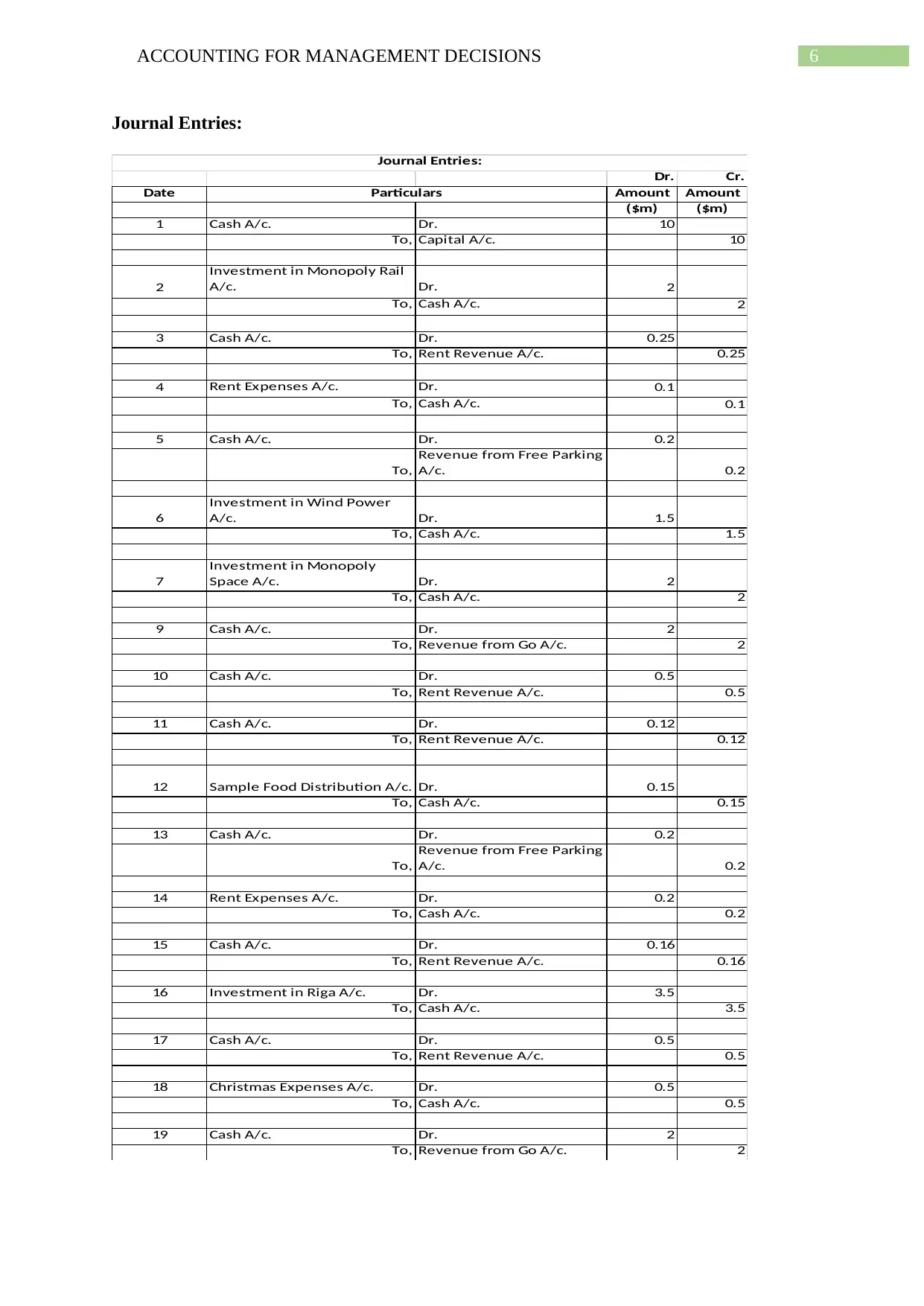

Journal Entries:

Dr. Cr.

Date Amount Amount

($m) ($m)

1 Cash A/c. Dr. 10

To, Capital A/c. 10

2

Investment in Monopoly Rail

A/c. Dr. 2

To, Cash A/c. 2

3 Cash A/c. Dr. 0.25

To, Rent Revenue A/c. 0.25

4 Rent Expenses A/c. Dr. 0.1

To, Cash A/c. 0.1

5 Cash A/c. Dr. 0.2

To,

Revenue from Free Parking

A/c. 0.2

6

Investment in Wind Power

A/c. Dr. 1.5

To, Cash A/c. 1.5

7

Investment in Monopoly

Space A/c. Dr. 2

To, Cash A/c. 2

9 Cash A/c. Dr. 2

To, Revenue from Go A/c. 2

10 Cash A/c. Dr. 0.5

To, Rent Revenue A/c. 0.5

11 Cash A/c. Dr. 0.12

To, Rent Revenue A/c. 0.12

12 Sample Food Distribution A/c. Dr. 0.15

To, Cash A/c. 0.15

13 Cash A/c. Dr. 0.2

To,

Revenue from Free Parking

A/c. 0.2

14 Rent Expenses A/c. Dr. 0.2

To, Cash A/c. 0.2

15 Cash A/c. Dr. 0.16

To, Rent Revenue A/c. 0.16

16 Investment in Riga A/c. Dr. 3.5

To, Cash A/c. 3.5

17 Cash A/c. Dr. 0.5

To, Rent Revenue A/c. 0.5

18 Christmas Expenses A/c. Dr. 0.5

To, Cash A/c. 0.5

19 Cash A/c. Dr. 2

To, Revenue from Go A/c. 2

Particulars

Journal Entries:

Journal Entries:

Dr. Cr.

Date Amount Amount

($m) ($m)

1 Cash A/c. Dr. 10

To, Capital A/c. 10

2

Investment in Monopoly Rail

A/c. Dr. 2

To, Cash A/c. 2

3 Cash A/c. Dr. 0.25

To, Rent Revenue A/c. 0.25

4 Rent Expenses A/c. Dr. 0.1

To, Cash A/c. 0.1

5 Cash A/c. Dr. 0.2

To,

Revenue from Free Parking

A/c. 0.2

6

Investment in Wind Power

A/c. Dr. 1.5

To, Cash A/c. 1.5

7

Investment in Monopoly

Space A/c. Dr. 2

To, Cash A/c. 2

9 Cash A/c. Dr. 2

To, Revenue from Go A/c. 2

10 Cash A/c. Dr. 0.5

To, Rent Revenue A/c. 0.5

11 Cash A/c. Dr. 0.12

To, Rent Revenue A/c. 0.12

12 Sample Food Distribution A/c. Dr. 0.15

To, Cash A/c. 0.15

13 Cash A/c. Dr. 0.2

To,

Revenue from Free Parking

A/c. 0.2

14 Rent Expenses A/c. Dr. 0.2

To, Cash A/c. 0.2

15 Cash A/c. Dr. 0.16

To, Rent Revenue A/c. 0.16

16 Investment in Riga A/c. Dr. 3.5

To, Cash A/c. 3.5

17 Cash A/c. Dr. 0.5

To, Rent Revenue A/c. 0.5

18 Christmas Expenses A/c. Dr. 0.5

To, Cash A/c. 0.5

19 Cash A/c. Dr. 2

To, Revenue from Go A/c. 2

Particulars

Journal Entries:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7ACCOUNTING FOR MANAGEMENT DECISIONS

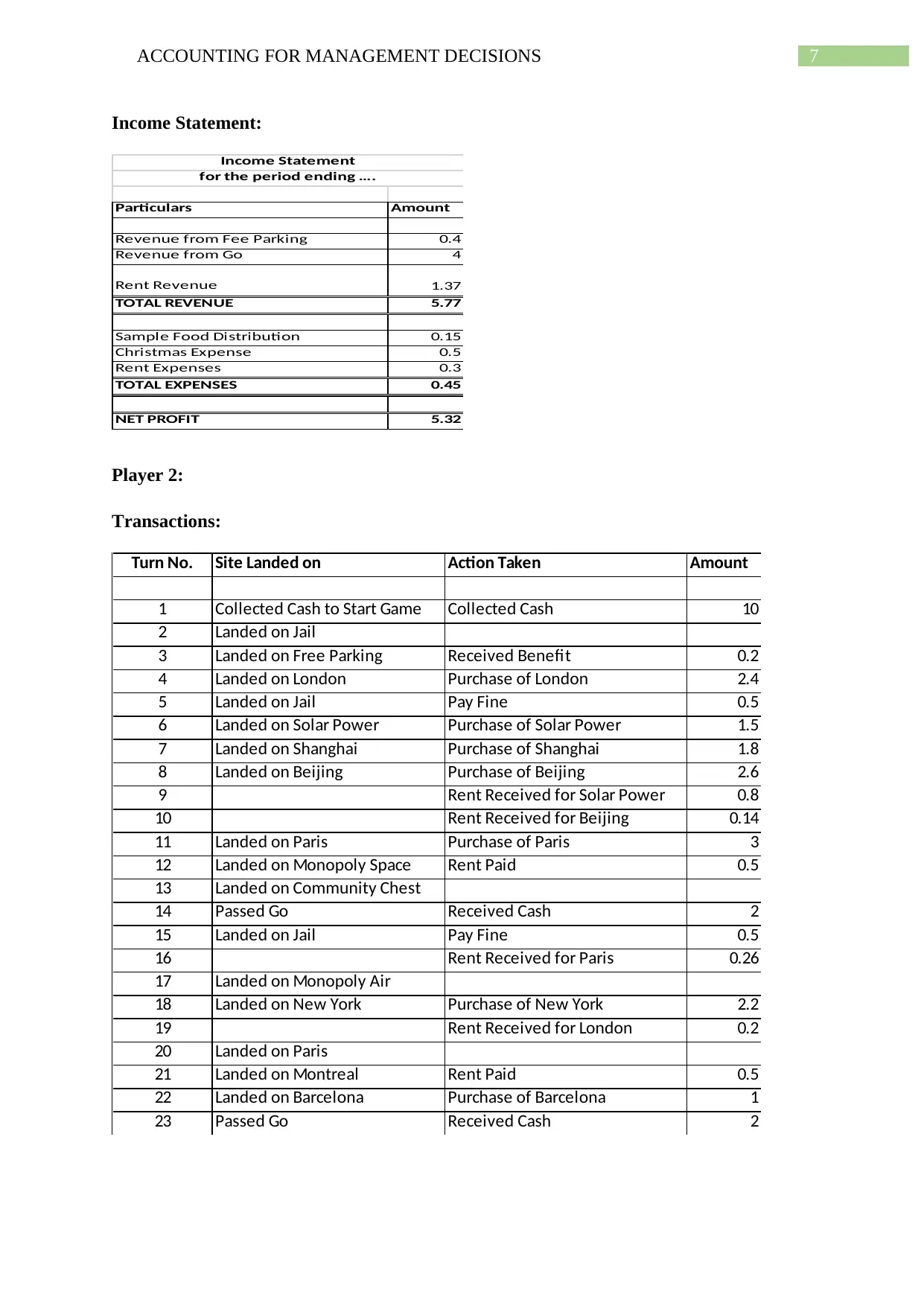

Income Statement:

Particulars Amount

Revenue from Fee Parking 0.4

Revenue from Go 4

Rent Revenue 1.37

TOTAL REVENUE 5.77

Sample Food Distribution 0.15

Christmas Expense 0.5

Rent Expenses 0.3

TOTAL EXPENSES 0.45

NET PROFIT 5.32

Income Statement

for the period ending ….

Player 2:

Transactions:

Turn No. Site Landed on Action Taken Amount

1 Collected Cash to Start Game Collected Cash 10

2 Landed on Jail

3 Landed on Free Parking Received Benefit 0.2

4 Landed on London Purchase of London 2.4

5 Landed on Jail Pay Fine 0.5

6 Landed on Solar Power Purchase of Solar Power 1.5

7 Landed on Shanghai Purchase of Shanghai 1.8

8 Landed on Beijing Purchase of Beijing 2.6

9 Rent Received for Solar Power 0.8

10 Rent Received for Beijing 0.14

11 Landed on Paris Purchase of Paris 3

12 Landed on Monopoly Space Rent Paid 0.5

13 Landed on Community Chest

14 Passed Go Received Cash 2

15 Landed on Jail Pay Fine 0.5

16 Rent Received for Paris 0.26

17 Landed on Monopoly Air

18 Landed on New York Purchase of New York 2.2

19 Rent Received for London 0.2

20 Landed on Paris

21 Landed on Montreal Rent Paid 0.5

22 Landed on Barcelona Purchase of Barcelona 1

23 Passed Go Received Cash 2

Income Statement:

Particulars Amount

Revenue from Fee Parking 0.4

Revenue from Go 4

Rent Revenue 1.37

TOTAL REVENUE 5.77

Sample Food Distribution 0.15

Christmas Expense 0.5

Rent Expenses 0.3

TOTAL EXPENSES 0.45

NET PROFIT 5.32

Income Statement

for the period ending ….

Player 2:

Transactions:

Turn No. Site Landed on Action Taken Amount

1 Collected Cash to Start Game Collected Cash 10

2 Landed on Jail

3 Landed on Free Parking Received Benefit 0.2

4 Landed on London Purchase of London 2.4

5 Landed on Jail Pay Fine 0.5

6 Landed on Solar Power Purchase of Solar Power 1.5

7 Landed on Shanghai Purchase of Shanghai 1.8

8 Landed on Beijing Purchase of Beijing 2.6

9 Rent Received for Solar Power 0.8

10 Rent Received for Beijing 0.14

11 Landed on Paris Purchase of Paris 3

12 Landed on Monopoly Space Rent Paid 0.5

13 Landed on Community Chest

14 Passed Go Received Cash 2

15 Landed on Jail Pay Fine 0.5

16 Rent Received for Paris 0.26

17 Landed on Monopoly Air

18 Landed on New York Purchase of New York 2.2

19 Rent Received for London 0.2

20 Landed on Paris

21 Landed on Montreal Rent Paid 0.5

22 Landed on Barcelona Purchase of Barcelona 1

23 Passed Go Received Cash 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8ACCOUNTING FOR MANAGEMENT DECISIONS

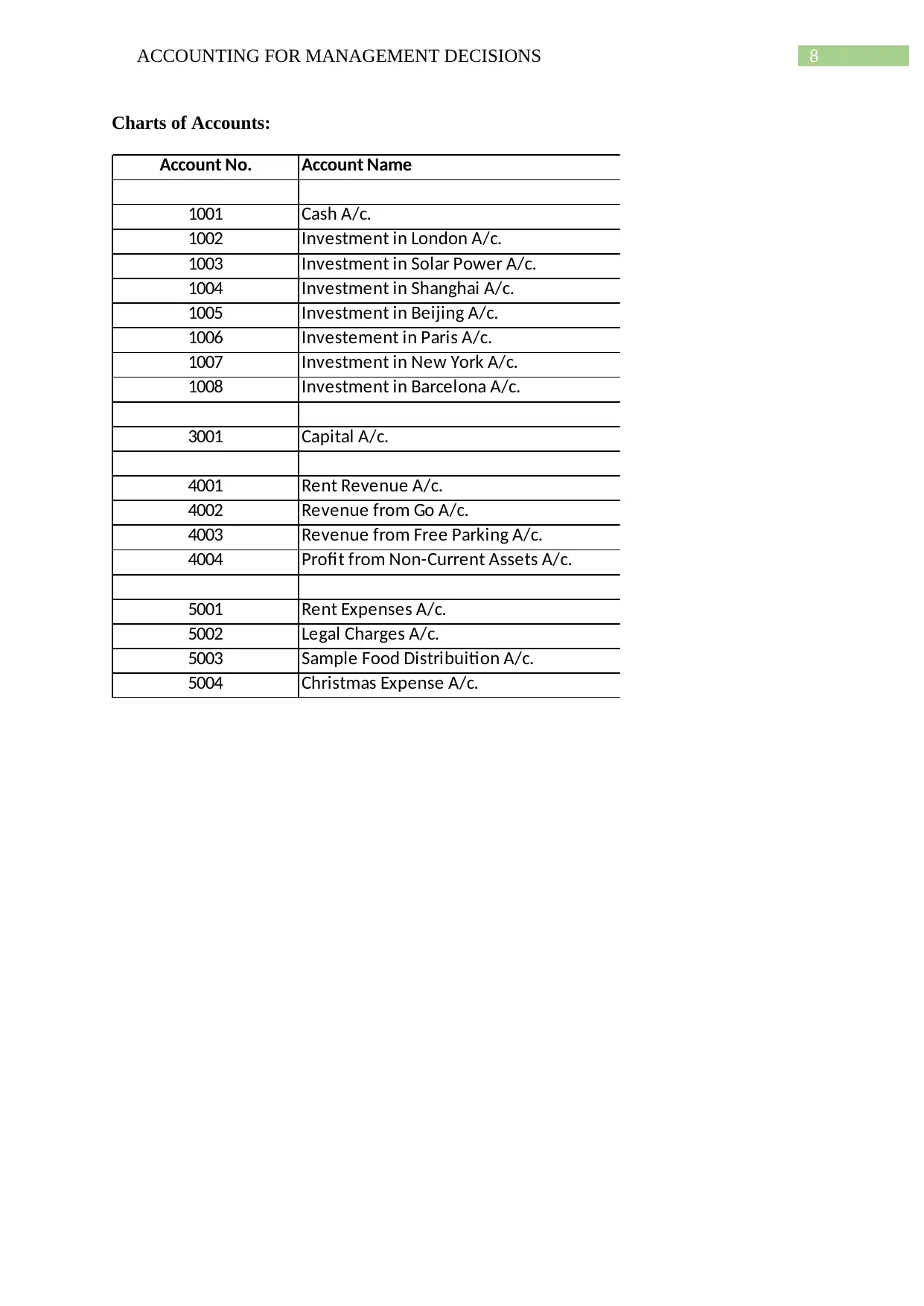

Charts of Accounts:

Account No. Account Name

1001 Cash A/c.

1002 Investment in London A/c.

1003 Investment in Solar Power A/c.

1004 Investment in Shanghai A/c.

1005 Investment in Beijing A/c.

1006 Investement in Paris A/c.

1007 Investment in New York A/c.

1008 Investment in Barcelona A/c.

3001 Capital A/c.

4001 Rent Revenue A/c.

4002 Revenue from Go A/c.

4003 Revenue from Free Parking A/c.

4004 Profit from Non-Current Assets A/c.

5001 Rent Expenses A/c.

5002 Legal Charges A/c.

5003 Sample Food Distribuition A/c.

5004 Christmas Expense A/c.

Charts of Accounts:

Account No. Account Name

1001 Cash A/c.

1002 Investment in London A/c.

1003 Investment in Solar Power A/c.

1004 Investment in Shanghai A/c.

1005 Investment in Beijing A/c.

1006 Investement in Paris A/c.

1007 Investment in New York A/c.

1008 Investment in Barcelona A/c.

3001 Capital A/c.

4001 Rent Revenue A/c.

4002 Revenue from Go A/c.

4003 Revenue from Free Parking A/c.

4004 Profit from Non-Current Assets A/c.

5001 Rent Expenses A/c.

5002 Legal Charges A/c.

5003 Sample Food Distribuition A/c.

5004 Christmas Expense A/c.

9ACCOUNTING FOR MANAGEMENT DECISIONS

Journal Entries:

Dr. Cr.

Date Amount Amount

($m) ($m)

1 Cash A/c. Dr. 10

To, Capital A/c. 10

3 Cash A/c. Dr. 0.2

To, Revenue from Free Parking A/c. 0.2

4 Investment in London A/c. Dr. 2.4

To, Cash A/c. 2.4

5 Legal Charges A/c. Dr. 0.5

To, Cash A/c. 0.5

6 Investment in Solar Power A/c. Dr. 1.5

To, Cash A/c. 1.5

7 Investment in Shanghai A/c. Dr. 1.8

To, Cash A/c. 1.8

8 Investment in Beijing A/c. Dr. 2.6

To, Cash A/c. 2.6

9 Cash A/c. Dr. 0.8

To, Rent Revenue A/c. 0.8

10 Cash A/c. Dr. 0.14

To, Rent Revenue A/c. 0.14

11 Investment in Paris A/c. Dr. 3

To, Cash A/c. 3

12 Rent Expenses A/c. Dr. 0.5

To, Cash A/c. 0.5

14 Cash A/c. Dr. 2

To, Revenue from Go A/c. 2

15 Legal Charges A/c. Dr. 0.5

To, Cash A/c. 0.5

16 Cash A/c. Dr. 0.26

To, Rent Revenue A/c. 0.26

18 Investment in New York A/c. Dr. 2.2

To, Cash A/c. 2.2

19 Cash A/c. Dr. 0.2

To, Rent Revenue A/c. 0.2

21 Rent Expenses A/c. Dr. 0.5

To, Cash A/c. 0.5

22 Investment in Barcelona A/c. Dr. 1

To, Cash A/c. 1

23 Cash A/c. Dr. 2

To, Revenue from Go A/c. 2

Journal Entries:

Particulars

Journal Entries:

Dr. Cr.

Date Amount Amount

($m) ($m)

1 Cash A/c. Dr. 10

To, Capital A/c. 10

3 Cash A/c. Dr. 0.2

To, Revenue from Free Parking A/c. 0.2

4 Investment in London A/c. Dr. 2.4

To, Cash A/c. 2.4

5 Legal Charges A/c. Dr. 0.5

To, Cash A/c. 0.5

6 Investment in Solar Power A/c. Dr. 1.5

To, Cash A/c. 1.5

7 Investment in Shanghai A/c. Dr. 1.8

To, Cash A/c. 1.8

8 Investment in Beijing A/c. Dr. 2.6

To, Cash A/c. 2.6

9 Cash A/c. Dr. 0.8

To, Rent Revenue A/c. 0.8

10 Cash A/c. Dr. 0.14

To, Rent Revenue A/c. 0.14

11 Investment in Paris A/c. Dr. 3

To, Cash A/c. 3

12 Rent Expenses A/c. Dr. 0.5

To, Cash A/c. 0.5

14 Cash A/c. Dr. 2

To, Revenue from Go A/c. 2

15 Legal Charges A/c. Dr. 0.5

To, Cash A/c. 0.5

16 Cash A/c. Dr. 0.26

To, Rent Revenue A/c. 0.26

18 Investment in New York A/c. Dr. 2.2

To, Cash A/c. 2.2

19 Cash A/c. Dr. 0.2

To, Rent Revenue A/c. 0.2

21 Rent Expenses A/c. Dr. 0.5

To, Cash A/c. 0.5

22 Investment in Barcelona A/c. Dr. 1

To, Cash A/c. 1

23 Cash A/c. Dr. 2

To, Revenue from Go A/c. 2

Journal Entries:

Particulars

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10ACCOUNTING FOR MANAGEMENT DECISIONS

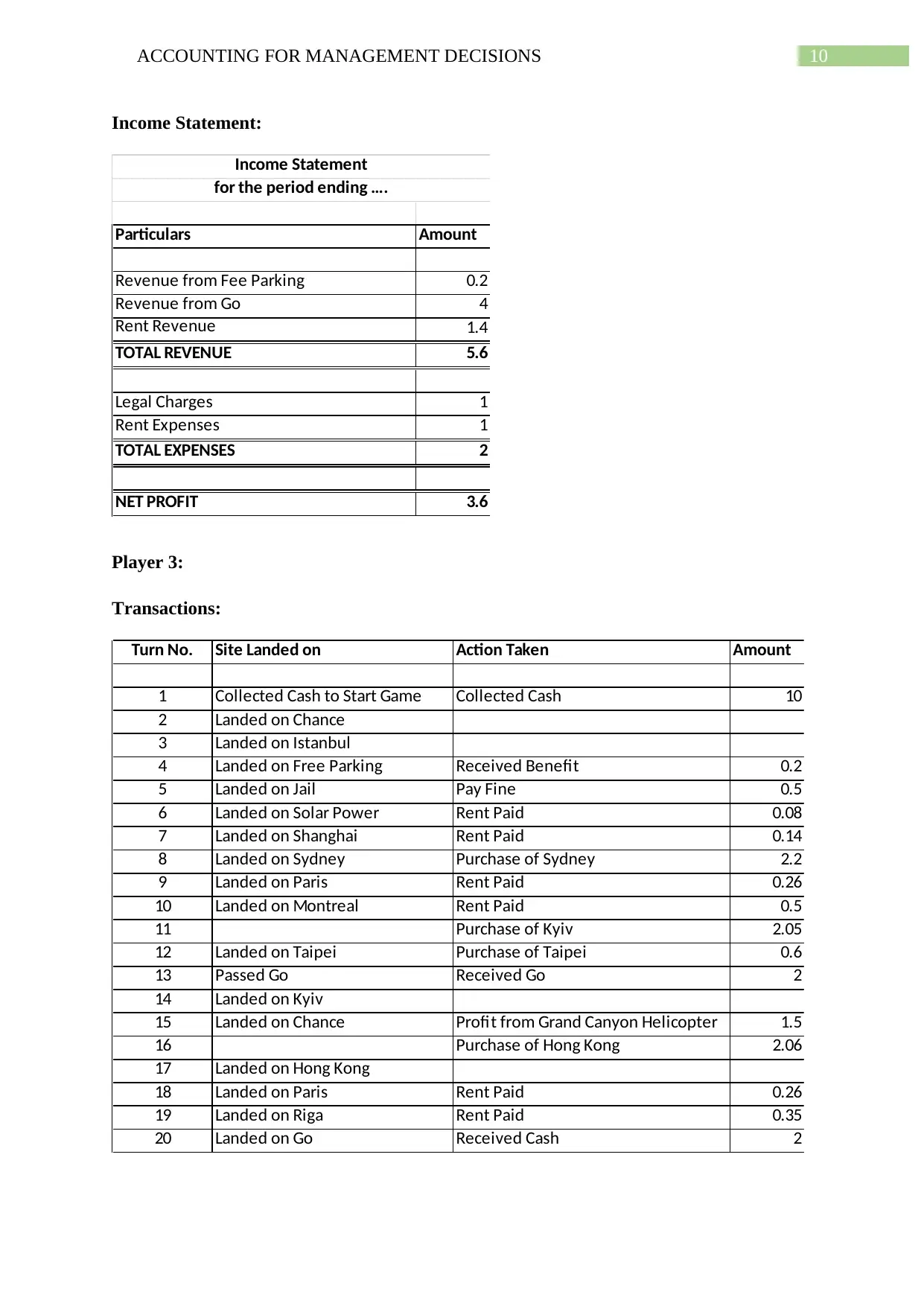

Income Statement:

Particulars Amount

Revenue from Fee Parking 0.2

Revenue from Go 4

Rent Revenue 1.4

TOTAL REVENUE 5.6

Legal Charges 1

Rent Expenses 1

TOTAL EXPENSES 2

NET PROFIT 3.6

Income Statement

for the period ending ….

Player 3:

Transactions:

Turn No. Site Landed on Action Taken Amount

1 Collected Cash to Start Game Collected Cash 10

2 Landed on Chance

3 Landed on Istanbul

4 Landed on Free Parking Received Benefit 0.2

5 Landed on Jail Pay Fine 0.5

6 Landed on Solar Power Rent Paid 0.08

7 Landed on Shanghai Rent Paid 0.14

8 Landed on Sydney Purchase of Sydney 2.2

9 Landed on Paris Rent Paid 0.26

10 Landed on Montreal Rent Paid 0.5

11 Purchase of Kyiv 2.05

12 Landed on Taipei Purchase of Taipei 0.6

13 Passed Go Received Go 2

14 Landed on Kyiv

15 Landed on Chance Profit from Grand Canyon Helicopter 1.5

16 Purchase of Hong Kong 2.06

17 Landed on Hong Kong

18 Landed on Paris Rent Paid 0.26

19 Landed on Riga Rent Paid 0.35

20 Landed on Go Received Cash 2

Income Statement:

Particulars Amount

Revenue from Fee Parking 0.2

Revenue from Go 4

Rent Revenue 1.4

TOTAL REVENUE 5.6

Legal Charges 1

Rent Expenses 1

TOTAL EXPENSES 2

NET PROFIT 3.6

Income Statement

for the period ending ….

Player 3:

Transactions:

Turn No. Site Landed on Action Taken Amount

1 Collected Cash to Start Game Collected Cash 10

2 Landed on Chance

3 Landed on Istanbul

4 Landed on Free Parking Received Benefit 0.2

5 Landed on Jail Pay Fine 0.5

6 Landed on Solar Power Rent Paid 0.08

7 Landed on Shanghai Rent Paid 0.14

8 Landed on Sydney Purchase of Sydney 2.2

9 Landed on Paris Rent Paid 0.26

10 Landed on Montreal Rent Paid 0.5

11 Purchase of Kyiv 2.05

12 Landed on Taipei Purchase of Taipei 0.6

13 Passed Go Received Go 2

14 Landed on Kyiv

15 Landed on Chance Profit from Grand Canyon Helicopter 1.5

16 Purchase of Hong Kong 2.06

17 Landed on Hong Kong

18 Landed on Paris Rent Paid 0.26

19 Landed on Riga Rent Paid 0.35

20 Landed on Go Received Cash 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11ACCOUNTING FOR MANAGEMENT DECISIONS

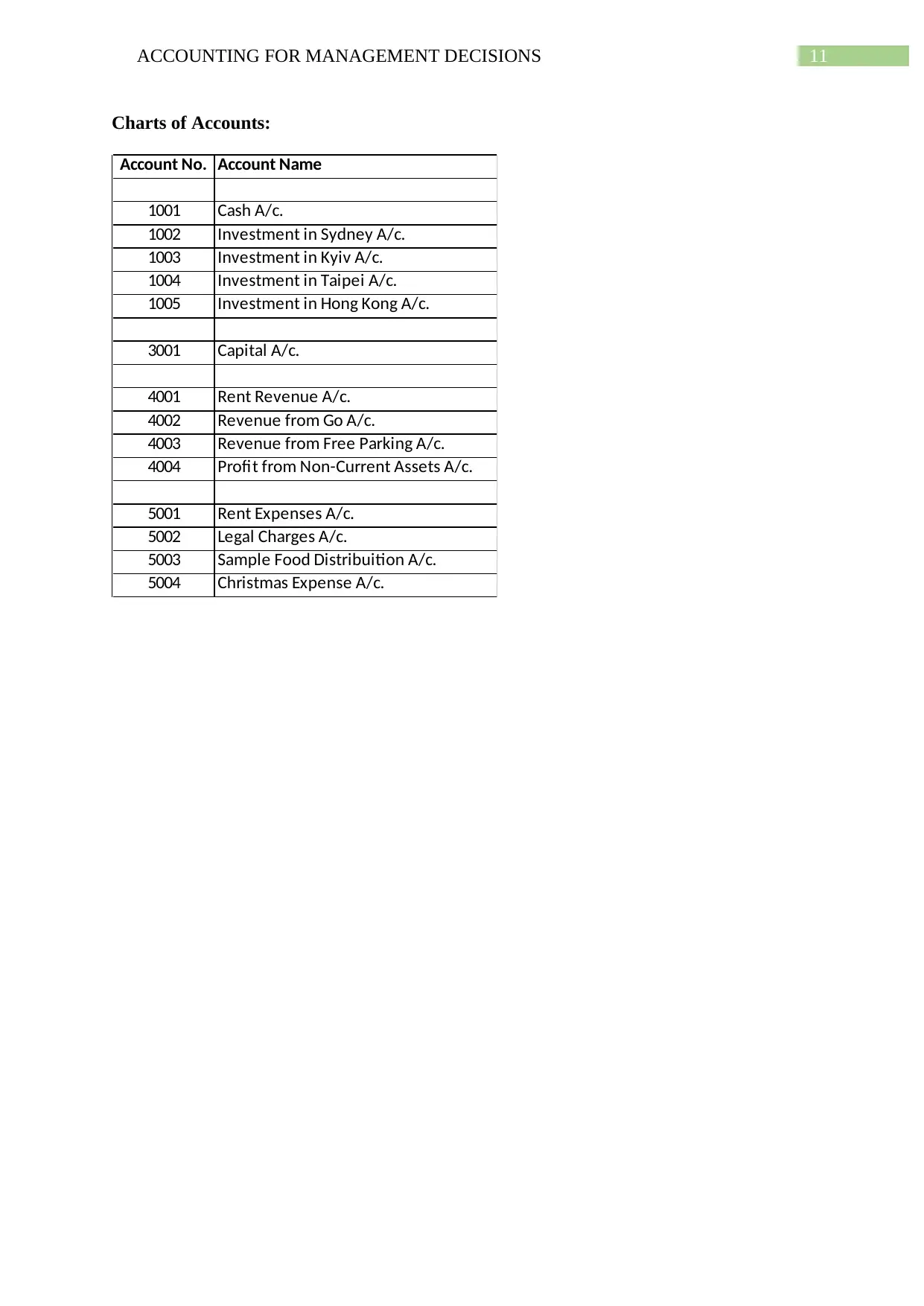

Charts of Accounts:

Account No. Account Name

1001 Cash A/c.

1002 Investment in Sydney A/c.

1003 Investment in Kyiv A/c.

1004 Investment in Taipei A/c.

1005 Investment in Hong Kong A/c.

3001 Capital A/c.

4001 Rent Revenue A/c.

4002 Revenue from Go A/c.

4003 Revenue from Free Parking A/c.

4004 Profit from Non-Current Assets A/c.

5001 Rent Expenses A/c.

5002 Legal Charges A/c.

5003 Sample Food Distribuition A/c.

5004 Christmas Expense A/c.

Charts of Accounts:

Account No. Account Name

1001 Cash A/c.

1002 Investment in Sydney A/c.

1003 Investment in Kyiv A/c.

1004 Investment in Taipei A/c.

1005 Investment in Hong Kong A/c.

3001 Capital A/c.

4001 Rent Revenue A/c.

4002 Revenue from Go A/c.

4003 Revenue from Free Parking A/c.

4004 Profit from Non-Current Assets A/c.

5001 Rent Expenses A/c.

5002 Legal Charges A/c.

5003 Sample Food Distribuition A/c.

5004 Christmas Expense A/c.

12ACCOUNTING FOR MANAGEMENT DECISIONS

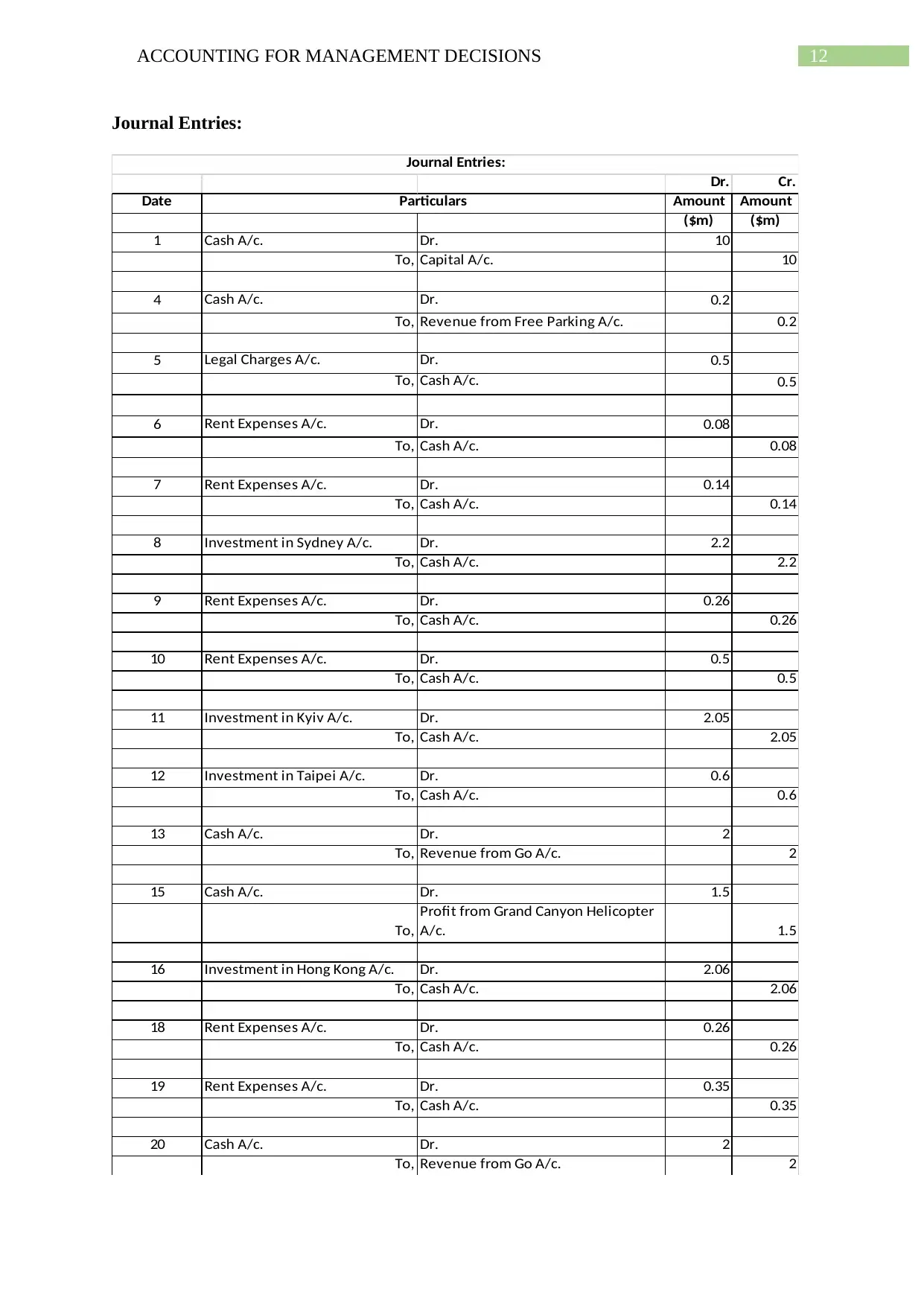

Journal Entries:

Dr. Cr.

Date Amount Amount

($m) ($m)

1 Cash A/c. Dr. 10

To, Capital A/c. 10

4 Cash A/c. Dr. 0.2

To, Revenue from Free Parking A/c. 0.2

5 Legal Charges A/c. Dr. 0.5

To, Cash A/c. 0.5

6 Rent Expenses A/c. Dr. 0.08

To, Cash A/c. 0.08

7 Rent Expenses A/c. Dr. 0.14

To, Cash A/c. 0.14

8 Investment in Sydney A/c. Dr. 2.2

To, Cash A/c. 2.2

9 Rent Expenses A/c. Dr. 0.26

To, Cash A/c. 0.26

10 Rent Expenses A/c. Dr. 0.5

To, Cash A/c. 0.5

11 Investment in Kyiv A/c. Dr. 2.05

To, Cash A/c. 2.05

12 Investment in Taipei A/c. Dr. 0.6

To, Cash A/c. 0.6

13 Cash A/c. Dr. 2

To, Revenue from Go A/c. 2

15 Cash A/c. Dr. 1.5

To,

Profit from Grand Canyon Helicopter

A/c. 1.5

16 Investment in Hong Kong A/c. Dr. 2.06

To, Cash A/c. 2.06

18 Rent Expenses A/c. Dr. 0.26

To, Cash A/c. 0.26

19 Rent Expenses A/c. Dr. 0.35

To, Cash A/c. 0.35

20 Cash A/c. Dr. 2

To, Revenue from Go A/c. 2

Journal Entries:

Particulars

Journal Entries:

Dr. Cr.

Date Amount Amount

($m) ($m)

1 Cash A/c. Dr. 10

To, Capital A/c. 10

4 Cash A/c. Dr. 0.2

To, Revenue from Free Parking A/c. 0.2

5 Legal Charges A/c. Dr. 0.5

To, Cash A/c. 0.5

6 Rent Expenses A/c. Dr. 0.08

To, Cash A/c. 0.08

7 Rent Expenses A/c. Dr. 0.14

To, Cash A/c. 0.14

8 Investment in Sydney A/c. Dr. 2.2

To, Cash A/c. 2.2

9 Rent Expenses A/c. Dr. 0.26

To, Cash A/c. 0.26

10 Rent Expenses A/c. Dr. 0.5

To, Cash A/c. 0.5

11 Investment in Kyiv A/c. Dr. 2.05

To, Cash A/c. 2.05

12 Investment in Taipei A/c. Dr. 0.6

To, Cash A/c. 0.6

13 Cash A/c. Dr. 2

To, Revenue from Go A/c. 2

15 Cash A/c. Dr. 1.5

To,

Profit from Grand Canyon Helicopter

A/c. 1.5

16 Investment in Hong Kong A/c. Dr. 2.06

To, Cash A/c. 2.06

18 Rent Expenses A/c. Dr. 0.26

To, Cash A/c. 0.26

19 Rent Expenses A/c. Dr. 0.35

To, Cash A/c. 0.35

20 Cash A/c. Dr. 2

To, Revenue from Go A/c. 2

Journal Entries:

Particulars

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.