HNC Business: Accounting Management Report on Financial Systems

VerifiedAdded on 2021/05/28

|45

|14945

|460

Report

AI Summary

This report, submitted by a student, provides a comprehensive overview of accounting management. It begins by defining managerial accounting and tracing its origins to the industrial revolution, highlighting its role in providing internal financial analyses and supporting management decisions. The report then explores the roles of management accounting in developing financial strategies, explaining financial implications, and monitoring spending. It delves into key principles such as designing and compiling accounting data, and employing management by exception. The report further examines different accounting systems including inventory control, cost accounting, job costing, and price management. It differentiates between financial and management accounting, detailing their objectives, users, and reporting formats. The importance of relevant, reliable, and accurate information is emphasized, along with the need for information to be interpreted in a comprehensible manner. Finally, the report discusses various types of managerial accounting reports, such as budget reports and accounts receivable aging reports, used by small businesses to monitor performance and manage cash flow.

ASSIGNMENT COVER SHEET

Name:

Haarsh Lallbeharry

Student Number:

3009HNCB

Address:

Branch road

Fond du sac

Mauritius

Post code / Zip:

20602

Email Address:

haarsh10@gmail.com

Date:

30/04/21

Course Name:

HNC BUSINESS

Tutor Name:

Jeremy Oughton

Assignment Name:

Accounting Management

PLEASE NOTE:

1

Name:

Haarsh Lallbeharry

Student Number:

3009HNCB

Address:

Branch road

Fond du sac

Mauritius

Post code / Zip:

20602

Email Address:

haarsh10@gmail.com

Date:

30/04/21

Course Name:

HNC BUSINESS

Tutor Name:

Jeremy Oughton

Assignment Name:

Accounting Management

PLEASE NOTE:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

YOU SHOULD INCLUDE THIS INFORMATION WITH EVERY ASSIGNMENT

Please ensure your name is printed in the footer of every page of your assignment

Learner statement of

authenticity:

I confirm that the attached completed assignment is all my own work, and

does not include any work completed by anyone other than myself. I have

completed the assignment in accordance with the Institute’s approved

instructions .

Tick here to opt

out

I consent for this assignment to be used for assessment standardisation and

where appropriate, for the dissemination of good practice, on the

understanding that the content is anonymised.

Signed: H.L Date: 30/04/21

Centre statement of

authenticity:

On behalf of Brighton School of Business and Management, I confirm that

the above mentioned learner is registered at the centre on a Pearson

Edexcel programme of study. The candidate is, to the best of my

knowledge, the sole author of the completed assignment.

Name: Job Title:

Signed: Date:

2

Please ensure your name is printed in the footer of every page of your assignment

Learner statement of

authenticity:

I confirm that the attached completed assignment is all my own work, and

does not include any work completed by anyone other than myself. I have

completed the assignment in accordance with the Institute’s approved

instructions .

Tick here to opt

out

I consent for this assignment to be used for assessment standardisation and

where appropriate, for the dissemination of good practice, on the

understanding that the content is anonymised.

Signed: H.L Date: 30/04/21

Centre statement of

authenticity:

On behalf of Brighton School of Business and Management, I confirm that

the above mentioned learner is registered at the centre on a Pearson

Edexcel programme of study. The candidate is, to the best of my

knowledge, the sole author of the completed assignment.

Name: Job Title:

Signed: Date:

2

LO1. Demonstrate an understanding of management accounting

systems.

Accounting for Management

Management accounting, the method of reviewing a company's expenses and activities in order

to compile internal financial analyses, databases, and books to help management in meeting

their goals is known as cost accounting or managerial accounting. In other words, it's the

method of deciphering financial and costing data and translating it into material that

management and officers may use.

Origin

Managerial accounting has its roots in the industrial revolution of the nineteenth century. During

this period, the majority of companies were closely managed by a small number of owner-

managers who borrowed money based on personal connections and personal properties. When

there were no international loans and no unsecured lending, there was no need for complicated

accounting records. Managerial accounting, on the other hand, was more advanced and

included the data needed to handle early large-scale clothing, steel, and other commodity

manufacturing. Due to new demands on companies from stock markets, creditors,

administrative authorities, and federal income taxes, financial accounting standards exploded at

the turn of the century. "Many companies wanted to collect funds from increasingly widespread

and remote sources of funding," Johnson and Kaplan write. To control these vast pools of

outside wealth, corporate executives required audited financial statements. When outside

funding outlets focused on audited financial statements, independent accountants were also

involved in designing well-defined protocols for corporate financial management. Public

accountants adopted an asset costing methodology at the turn of the century, which had a

major influence on management accounting. As a result, over the last few decades,

management accountants have focused mostly on ensuring that financial accounting

requirements are met and financial statements are released on time.

Roles

-Financial Strategies

Financial plans can be developed using sales projections, budgets, and job-costing approaches,

among other managerial accounting tools. They'll also use financial reporting data to develop

strategies for increasing total revenue, net profit, and earnings per share. If designing a budget

to purchase new properties or lowering operating expenses to ensure a company's long-term

viability, management accountants play a key role in developing good financial strategies..

-Explain Choices' Financial Implications

When senior executives change a company's financial strategy, management accountants may

explain the implications of adding additional debt or equity capital. Partnerships with other

companies, building new service centres, and laying off large numbers of employees all fit the

same trend. They'll see how decisions impact budgets and financial statements, as well as how

decisions affect the profit or loss of a business over time. Although certain policy choices will

3

systems.

Accounting for Management

Management accounting, the method of reviewing a company's expenses and activities in order

to compile internal financial analyses, databases, and books to help management in meeting

their goals is known as cost accounting or managerial accounting. In other words, it's the

method of deciphering financial and costing data and translating it into material that

management and officers may use.

Origin

Managerial accounting has its roots in the industrial revolution of the nineteenth century. During

this period, the majority of companies were closely managed by a small number of owner-

managers who borrowed money based on personal connections and personal properties. When

there were no international loans and no unsecured lending, there was no need for complicated

accounting records. Managerial accounting, on the other hand, was more advanced and

included the data needed to handle early large-scale clothing, steel, and other commodity

manufacturing. Due to new demands on companies from stock markets, creditors,

administrative authorities, and federal income taxes, financial accounting standards exploded at

the turn of the century. "Many companies wanted to collect funds from increasingly widespread

and remote sources of funding," Johnson and Kaplan write. To control these vast pools of

outside wealth, corporate executives required audited financial statements. When outside

funding outlets focused on audited financial statements, independent accountants were also

involved in designing well-defined protocols for corporate financial management. Public

accountants adopted an asset costing methodology at the turn of the century, which had a

major influence on management accounting. As a result, over the last few decades,

management accountants have focused mostly on ensuring that financial accounting

requirements are met and financial statements are released on time.

Roles

-Financial Strategies

Financial plans can be developed using sales projections, budgets, and job-costing approaches,

among other managerial accounting tools. They'll also use financial reporting data to develop

strategies for increasing total revenue, net profit, and earnings per share. If designing a budget

to purchase new properties or lowering operating expenses to ensure a company's long-term

viability, management accountants play a key role in developing good financial strategies..

-Explain Choices' Financial Implications

When senior executives change a company's financial strategy, management accountants may

explain the implications of adding additional debt or equity capital. Partnerships with other

companies, building new service centres, and laying off large numbers of employees all fit the

same trend. They'll see how decisions impact budgets and financial statements, as well as how

decisions affect the profit or loss of a business over time. Although certain policy choices will

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

seem to be fair, only a careful review of the facts can allow an organisation to decide whether

they add up.

- Keep an eye on your spending

Management accountants can build rigid, fluid, or rolling schedules, as well as other forms of

reports, to help senior executives and department heads keep track of their spending. Since

running costs have a significant effect on bottom-line profit, this is critical. Business accountants

may help an organization operate as cost-effectively as possible by choosing the right budgeting

strategy for their stakeholders' unique needs. They will also create ad-hoc reports to help their

clients identify the kinds of costs their agency or company incurs.

Principles

-Designing and compiling

Accounting data, notes, reports, declarations, and other evidence of past, present, and future

results should be designed and compiled to meet the specific needs of each organization and/or

concern.

It means that the management accounting system is set up in such a way that all necessary

paperwork is available. If this is the case, there is a serious problem that needs to be solved.

Accounting records may also be modified and applied to meet the needs of management.

- Exceptional Management

The definition of management by exception is used for presenting information to managers. It

says the management accounting system employs a financial control system as well as

conventional costing methods.

To detect deviations, the actual output is compared to a pre-determined one. The root of the

problem is defined as the unfavorable deviations alone. If this is the case, management has

spent more time acting on the data rather than reading and analyzing it.

Accounting System and Management

Financial accounting is concerned with compiling records for third parties such as stockholders,

financial regulators, and lenders in accordance with generally accepted accounting principles.

Managerial accounting, on the other hand, takes a company's financial data and organizes it

into databases for managers to use in making decisions and identifying ways to improve the

company's operations. These reports, which are based on management's informational needs,

include budgeting, breakeven maps, product cost analysis, trend charts, and forecasts.

-Inventory Control System

The key goal of inventory management is to define the shape and position of stocked objects. It

is likely to occur before the usual and planned course of production and inventory stocking at

different locations within a plant or across a supply network.

-Accounting Scheme for Expenses

4

they add up.

- Keep an eye on your spending

Management accountants can build rigid, fluid, or rolling schedules, as well as other forms of

reports, to help senior executives and department heads keep track of their spending. Since

running costs have a significant effect on bottom-line profit, this is critical. Business accountants

may help an organization operate as cost-effectively as possible by choosing the right budgeting

strategy for their stakeholders' unique needs. They will also create ad-hoc reports to help their

clients identify the kinds of costs their agency or company incurs.

Principles

-Designing and compiling

Accounting data, notes, reports, declarations, and other evidence of past, present, and future

results should be designed and compiled to meet the specific needs of each organization and/or

concern.

It means that the management accounting system is set up in such a way that all necessary

paperwork is available. If this is the case, there is a serious problem that needs to be solved.

Accounting records may also be modified and applied to meet the needs of management.

- Exceptional Management

The definition of management by exception is used for presenting information to managers. It

says the management accounting system employs a financial control system as well as

conventional costing methods.

To detect deviations, the actual output is compared to a pre-determined one. The root of the

problem is defined as the unfavorable deviations alone. If this is the case, management has

spent more time acting on the data rather than reading and analyzing it.

Accounting System and Management

Financial accounting is concerned with compiling records for third parties such as stockholders,

financial regulators, and lenders in accordance with generally accepted accounting principles.

Managerial accounting, on the other hand, takes a company's financial data and organizes it

into databases for managers to use in making decisions and identifying ways to improve the

company's operations. These reports, which are based on management's informational needs,

include budgeting, breakeven maps, product cost analysis, trend charts, and forecasts.

-Inventory Control System

The key goal of inventory management is to define the shape and position of stocked objects. It

is likely to occur before the usual and planned course of production and inventory stocking at

different locations within a plant or across a supply network.

-Accounting Scheme for Expenses

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Manufacturers report production processes using a cost accounting scheme and a permanent

inventory system. To put it another way, it's a manufacturing-specific accounting system for

tracking inventory as it goes through the various stages of processing.

-System of Job Costing

The practice of allocating costs to a certain job that you or the corporation is employed on is

known as employment cost accounting. This term is commonly used in the construction industry

to describe how a company allocates costs to individual construction projects.

-System for price management

Price management is the process of determining the sale sweet point, or optimizing price

against a customer's willingness to pay. Pricing optimization is a significant endeavor for

companies at all levels of the supply chain, including B2B and B2C, to ensure that their products

are delivered effectively at the right price while making a reasonable profit.

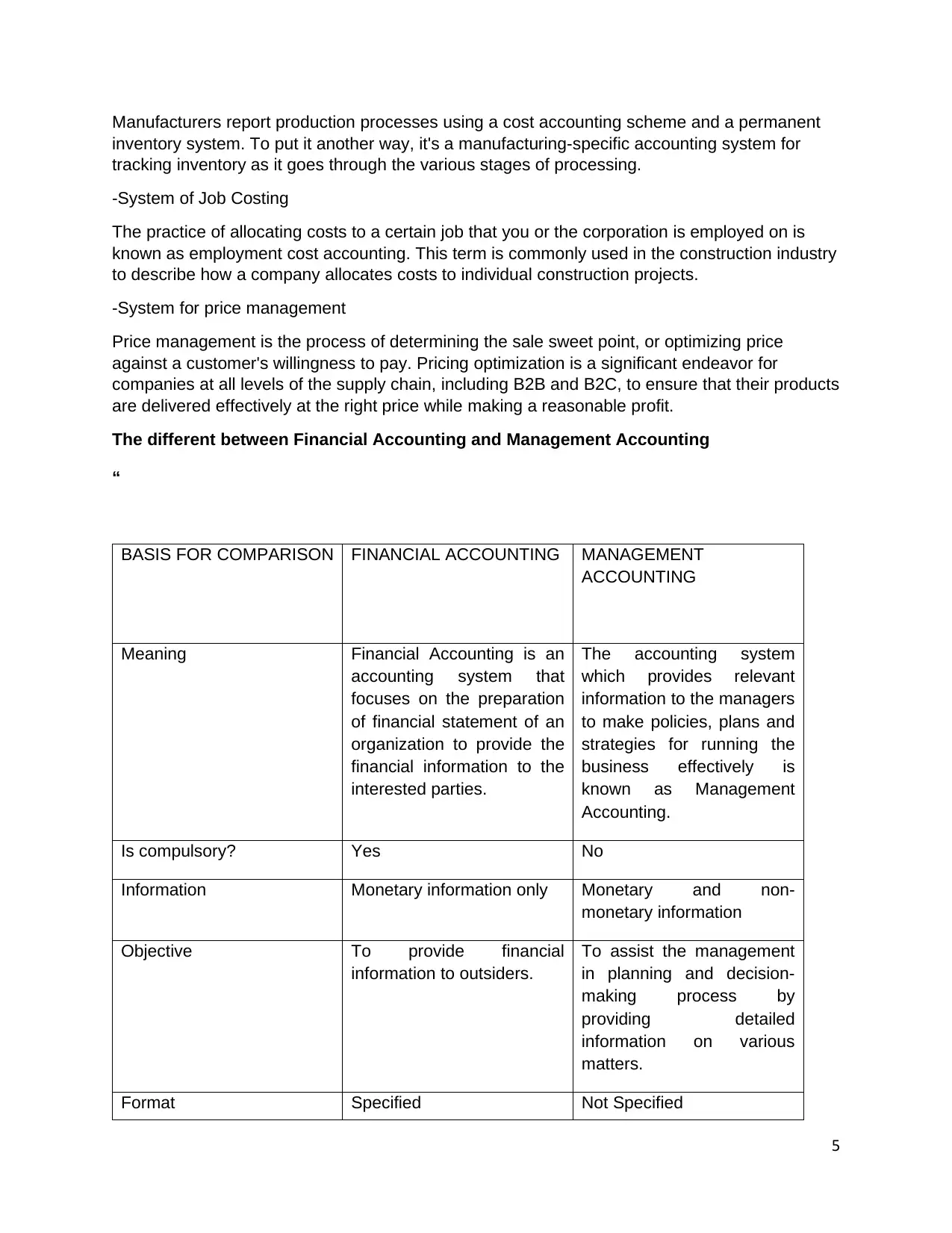

The different between Financial Accounting and Management Accounting

“

BASIS FOR COMPARISON FINANCIAL ACCOUNTING MANAGEMENT

ACCOUNTING

Meaning Financial Accounting is an

accounting system that

focuses on the preparation

of financial statement of an

organization to provide the

financial information to the

interested parties.

The accounting system

which provides relevant

information to the managers

to make policies, plans and

strategies for running the

business effectively is

known as Management

Accounting.

Is compulsory? Yes No

Information Monetary information only Monetary and non-

monetary information

Objective To provide financial

information to outsiders.

To assist the management

in planning and decision-

making process by

providing detailed

information on various

matters.

Format Specified Not Specified

5

inventory system. To put it another way, it's a manufacturing-specific accounting system for

tracking inventory as it goes through the various stages of processing.

-System of Job Costing

The practice of allocating costs to a certain job that you or the corporation is employed on is

known as employment cost accounting. This term is commonly used in the construction industry

to describe how a company allocates costs to individual construction projects.

-System for price management

Price management is the process of determining the sale sweet point, or optimizing price

against a customer's willingness to pay. Pricing optimization is a significant endeavor for

companies at all levels of the supply chain, including B2B and B2C, to ensure that their products

are delivered effectively at the right price while making a reasonable profit.

The different between Financial Accounting and Management Accounting

“

BASIS FOR COMPARISON FINANCIAL ACCOUNTING MANAGEMENT

ACCOUNTING

Meaning Financial Accounting is an

accounting system that

focuses on the preparation

of financial statement of an

organization to provide the

financial information to the

interested parties.

The accounting system

which provides relevant

information to the managers

to make policies, plans and

strategies for running the

business effectively is

known as Management

Accounting.

Is compulsory? Yes No

Information Monetary information only Monetary and non-

monetary information

Objective To provide financial

information to outsiders.

To assist the management

in planning and decision-

making process by

providing detailed

information on various

matters.

Format Specified Not Specified

5

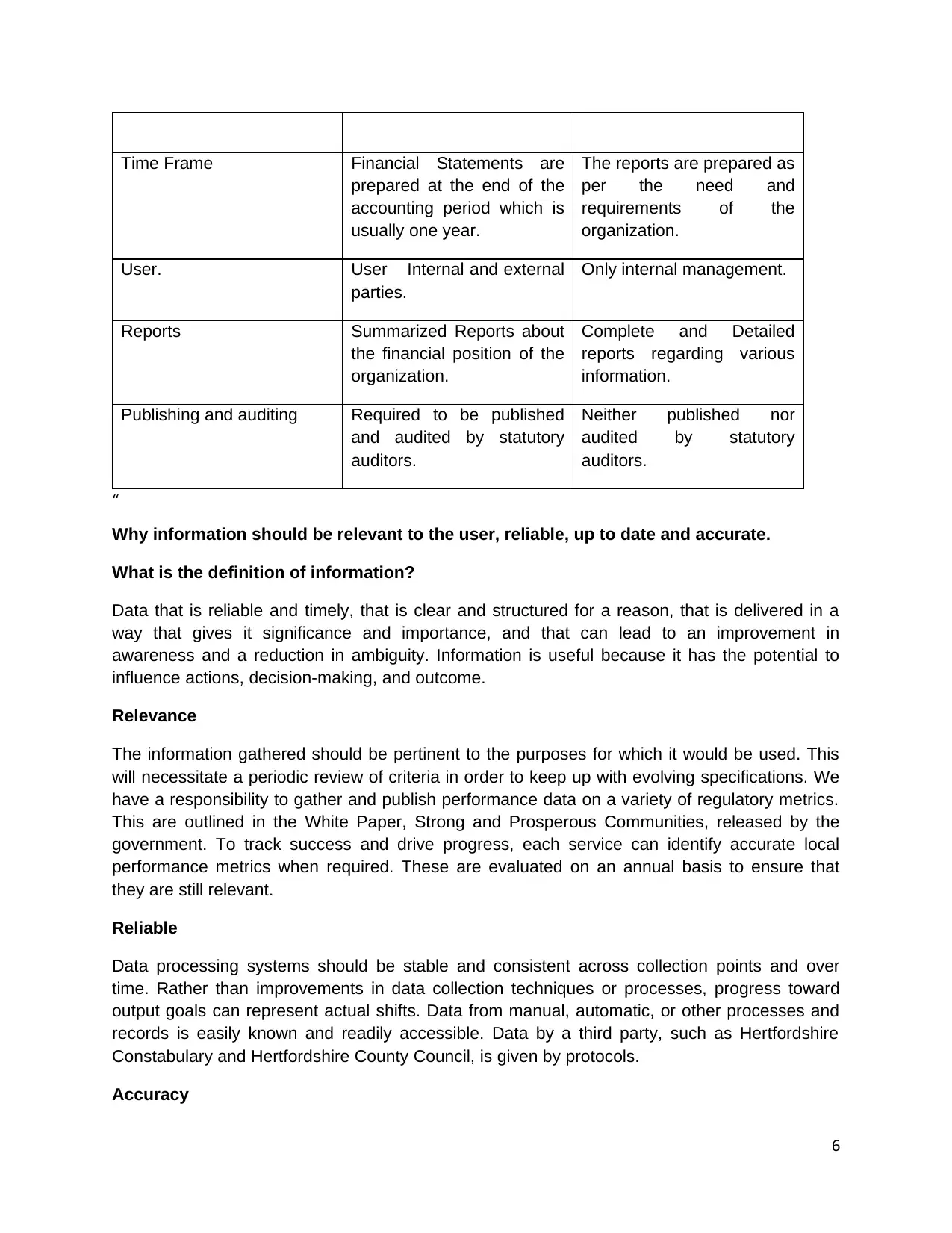

Time Frame Financial Statements are

prepared at the end of the

accounting period which is

usually one year.

The reports are prepared as

per the need and

requirements of the

organization.

User. User Internal and external

parties.

Only internal management.

Reports Summarized Reports about

the financial position of the

organization.

Complete and Detailed

reports regarding various

information.

Publishing and auditing Required to be published

and audited by statutory

auditors.

Neither published nor

audited by statutory

auditors.

“

Why information should be relevant to the user, reliable, up to date and accurate.

What is the definition of information?

Data that is reliable and timely, that is clear and structured for a reason, that is delivered in a

way that gives it significance and importance, and that can lead to an improvement in

awareness and a reduction in ambiguity. Information is useful because it has the potential to

influence actions, decision-making, and outcome.

Relevance

The information gathered should be pertinent to the purposes for which it would be used. This

will necessitate a periodic review of criteria in order to keep up with evolving specifications. We

have a responsibility to gather and publish performance data on a variety of regulatory metrics.

This are outlined in the White Paper, Strong and Prosperous Communities, released by the

government. To track success and drive progress, each service can identify accurate local

performance metrics when required. These are evaluated on an annual basis to ensure that

they are still relevant.

Reliable

Data processing systems should be stable and consistent across collection points and over

time. Rather than improvements in data collection techniques or processes, progress toward

output goals can represent actual shifts. Data from manual, automatic, or other processes and

records is easily known and readily accessible. Data by a third party, such as Hertfordshire

Constabulary and Hertfordshire County Council, is given by protocols.

Accuracy

6

prepared at the end of the

accounting period which is

usually one year.

The reports are prepared as

per the need and

requirements of the

organization.

User. User Internal and external

parties.

Only internal management.

Reports Summarized Reports about

the financial position of the

organization.

Complete and Detailed

reports regarding various

information.

Publishing and auditing Required to be published

and audited by statutory

auditors.

Neither published nor

audited by statutory

auditors.

“

Why information should be relevant to the user, reliable, up to date and accurate.

What is the definition of information?

Data that is reliable and timely, that is clear and structured for a reason, that is delivered in a

way that gives it significance and importance, and that can lead to an improvement in

awareness and a reduction in ambiguity. Information is useful because it has the potential to

influence actions, decision-making, and outcome.

Relevance

The information gathered should be pertinent to the purposes for which it would be used. This

will necessitate a periodic review of criteria in order to keep up with evolving specifications. We

have a responsibility to gather and publish performance data on a variety of regulatory metrics.

This are outlined in the White Paper, Strong and Prosperous Communities, released by the

government. To track success and drive progress, each service can identify accurate local

performance metrics when required. These are evaluated on an annual basis to ensure that

they are still relevant.

Reliable

Data processing systems should be stable and consistent across collection points and over

time. Rather than improvements in data collection techniques or processes, progress toward

output goals can represent actual shifts. Data from manual, automatic, or other processes and

records is easily known and readily accessible. Data by a third party, such as Hertfordshire

Constabulary and Hertfordshire County Council, is given by protocols.

Accuracy

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

And if it has multiple uses, data should be accurate enough for the intended use and should

only be obtained once. Data should be recorded at the point of service. Data is also captured at

the point of service. Output data is automatically entered into Performance Plus by the service

manager or designated data entry staff.

Reliability

Data can be obtained as quickly as possible after an event or procedure and made available for

the intended use within a reasonable time frame. Data must be readily accessible and reliable in

order to support information requirements and influence service or management decisions.

Timeliness

Data should be collected as soon as possible following an event or activity and made available

for the anticipated use in a reasonable period of time. To meet information demands and

influence service or management decisions, data must be available in a timely and accurate

manner.

Why is it necessary for the knowledge to be interpreted in a comprehensible manner?

When users can read, understandable material must be easy to obtain ideas. And this

knowledge shows you how to schedule, monitor, and coordinate the decision-making process. A

short, full, and consistent interpretation of the details contained in the study is called

understanding. Users require information about the arrangement in order to interpret financial

statements. The genuine history of company practices signifies an appreciation of evidence and

financial quality that can be deduced by experienced individuals.

Different types of managerial accounting reports

Small business owners and managers use managerial accounting reports to keep track of their

company's results, and they are prepared if needed during accounting periods. Depending on

the scope of the project and the time-sensitive nature of the content, an owner or manager can

request reports periodically, annually, weekly, or even daily.

Budget Report

Budget reviews help small business owners in reviewing their company's performance, and

executives in analyzing and managing spending within their divisions if the enterprise is big

enough. The estimated spending for the year is usually dependent on actual expenses from the

previous year. When a small business or a specific department was over budget the previous

year and couldn't find a way to cut costs, the budget for the next year would need to be

increased to a more accurate level. Owners and employers may use budget analysis to provide

incentives to their employees.

Accounts Receivable Aging Reports

The accounts receivable aged report is a useful tool for companies who lend credit to their

customers to manage cash flow. Consumer balances are classified in this report based on how

7

only be obtained once. Data should be recorded at the point of service. Data is also captured at

the point of service. Output data is automatically entered into Performance Plus by the service

manager or designated data entry staff.

Reliability

Data can be obtained as quickly as possible after an event or procedure and made available for

the intended use within a reasonable time frame. Data must be readily accessible and reliable in

order to support information requirements and influence service or management decisions.

Timeliness

Data should be collected as soon as possible following an event or activity and made available

for the anticipated use in a reasonable period of time. To meet information demands and

influence service or management decisions, data must be available in a timely and accurate

manner.

Why is it necessary for the knowledge to be interpreted in a comprehensible manner?

When users can read, understandable material must be easy to obtain ideas. And this

knowledge shows you how to schedule, monitor, and coordinate the decision-making process. A

short, full, and consistent interpretation of the details contained in the study is called

understanding. Users require information about the arrangement in order to interpret financial

statements. The genuine history of company practices signifies an appreciation of evidence and

financial quality that can be deduced by experienced individuals.

Different types of managerial accounting reports

Small business owners and managers use managerial accounting reports to keep track of their

company's results, and they are prepared if needed during accounting periods. Depending on

the scope of the project and the time-sensitive nature of the content, an owner or manager can

request reports periodically, annually, weekly, or even daily.

Budget Report

Budget reviews help small business owners in reviewing their company's performance, and

executives in analyzing and managing spending within their divisions if the enterprise is big

enough. The estimated spending for the year is usually dependent on actual expenses from the

previous year. When a small business or a specific department was over budget the previous

year and couldn't find a way to cut costs, the budget for the next year would need to be

increased to a more accurate level. Owners and employers may use budget analysis to provide

incentives to their employees.

Accounts Receivable Aging Reports

The accounts receivable aged report is a useful tool for companies who lend credit to their

customers to manage cash flow. Consumer balances are classified in this report based on how

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

long they have been unpaid. Many aging databases have separate tables for invoices that are

30 days late, 60 days late, or 90 days late or more. A contractor could use the old study to find

problems with the company's collection process. If a substantial number of customers are

unable to pay their bills, the credit policies of the firm may need to be tightened. Through

checking the accounts receivable aged on a daily basis, the collections department is also

prevented from overlooking old debts.

Job Cost Reports

The expenses associated with a project are detailed in job expense forecasts. They're normally

paired with a revenue estimate in order for the company to assess the job's viability. This

encourages the company to focus on higher-earning facets of the industry rather than wasting

time and money on employees with reduced profit margins. Job cost assessments are also

used to measure expenditures when a project is still in progress, enabling management to find

areas where costs are rising too quickly.

Inventory and Manufacturing

Managerial accounting documents may aid physical inventory companies in improving their

manufacturing processes. Material waste, hourly labor rates, and per-unit overhead costs are

often used in these analyses. The manager will also compare different production lines inside

the company and see how they can improve or reward the teams with the best performance.

Impact of effective management accounting system in Wiz’s different departments

Finance, IT, networking, human resources, logistics, and sales are all integrated into one

structure through an effective management accounting process, which will have a positive

effect. Administrative accounting will provide non-financial information such as cash on hand,

monthly sales figures, number of phone calls every day, order backlog, delivery due dates,

aging state of accounts receivables and payables, and current inventory percentages of raw

materials and finished products. All of this information is used to categorize the various parts of

a company's key performance indicators.

It is intended to assist management in their stewardship role, as well as support management in

their day-to-day activities and decision-making. Machines were developed in 1880 to aid in the

accounting procedure. Advancements of computer management changed accounting systems

and procedures as the years progressed. The Accounting Information System has had a lot of

changes (AIS). This is intended to aid in the administration and regulation of operations relating

to the commercial and financial aspects of the company. The bulk of corporate companies need

an accounting procedure. Technology advances have resulted in the creation of a computerized

accounting system that is still widely used for businesses. As a result, a dynamic market has

emerged. As a result, organizations must upgrade their processes to properly balance their

knowledge needs in order to make better decisions.

An information system is a set of interconnected subsystems that gather, process, store, turn,

and distribute data for planning, decision-making, and management. Data gathering, sorting,

storage, transformation, and dissemination can also be made more efficient by the use of

8

30 days late, 60 days late, or 90 days late or more. A contractor could use the old study to find

problems with the company's collection process. If a substantial number of customers are

unable to pay their bills, the credit policies of the firm may need to be tightened. Through

checking the accounts receivable aged on a daily basis, the collections department is also

prevented from overlooking old debts.

Job Cost Reports

The expenses associated with a project are detailed in job expense forecasts. They're normally

paired with a revenue estimate in order for the company to assess the job's viability. This

encourages the company to focus on higher-earning facets of the industry rather than wasting

time and money on employees with reduced profit margins. Job cost assessments are also

used to measure expenditures when a project is still in progress, enabling management to find

areas where costs are rising too quickly.

Inventory and Manufacturing

Managerial accounting documents may aid physical inventory companies in improving their

manufacturing processes. Material waste, hourly labor rates, and per-unit overhead costs are

often used in these analyses. The manager will also compare different production lines inside

the company and see how they can improve or reward the teams with the best performance.

Impact of effective management accounting system in Wiz’s different departments

Finance, IT, networking, human resources, logistics, and sales are all integrated into one

structure through an effective management accounting process, which will have a positive

effect. Administrative accounting will provide non-financial information such as cash on hand,

monthly sales figures, number of phone calls every day, order backlog, delivery due dates,

aging state of accounts receivables and payables, and current inventory percentages of raw

materials and finished products. All of this information is used to categorize the various parts of

a company's key performance indicators.

It is intended to assist management in their stewardship role, as well as support management in

their day-to-day activities and decision-making. Machines were developed in 1880 to aid in the

accounting procedure. Advancements of computer management changed accounting systems

and procedures as the years progressed. The Accounting Information System has had a lot of

changes (AIS). This is intended to aid in the administration and regulation of operations relating

to the commercial and financial aspects of the company. The bulk of corporate companies need

an accounting procedure. Technology advances have resulted in the creation of a computerized

accounting system that is still widely used for businesses. As a result, a dynamic market has

emerged. As a result, organizations must upgrade their processes to properly balance their

knowledge needs in order to make better decisions.

An information system is a set of interconnected subsystems that gather, process, store, turn,

and distribute data for planning, decision-making, and management. Data gathering, sorting,

storage, transformation, and dissemination can also be made more efficient by the use of

8

computers in information systems. Accounting management systems (AIS) are a type of

instrument used in the field of information and technology systems. It is important for

commercial companies. This is the person in charge of gathering accurate financial data for

decision-making. There are several different device implementations and they must take into

account aspects that affect how information is collected and reported. It would still be

determined by the information's intended consumers and the kinds of choices they are likely to

make. The size of the company, amount of transaction data, nature of operations, organizational

structure, and business model may all influence the system's architecture.

Accounting developed from a company's day-to-day operations in order to provide relevant data

for decision-making. Financial activity data is thus critical to an organization's life, viability, and

development. As a result, keeping a proper and reliable log of all events is a good way to get

the accounting data you need. Any corporation, whether private or governmental, is required to

keep financial records in order to evaluate its results. However, dramatic developments in

information technology and the advent of computers have had a significant impact on the

process of transmitting financial data. The first computer system was developed for accounting,

signaling a new era in the profession's history as companies rapidly welcome it to streamline

accounting records. Computers and advances in information and communication technology

(ICT) have altered the way accounting and accounting roles are carried out. The

computerization of financial accounting systems has presented challenges to the accounting

profession, as accountants now face a variety of issues, especially when performing accounting

and accounting for businesses in an electronic environment. However, it has expanded the

fraternity (scientific exposure) of accountants, allowing them to have more service levels and a

wider range of services to their customers. Auditors' schedules used to require separate stages

of preparation, but in today's constantly changing technologically-driven field of financial

statements, auditors may need to revise their conventional audit schedules and conduct checks

on a continual basis due to improvements in technology.

LO2. Apply a range of management accounting techniques

P3. Calculate costs using appropriates techniques of cost analysis to

prepare an income statement using marginal and absorption costs.

A. Price

In industry and accounting world , cost is the amount of money spent by a company to produce

something. Cost refers to the amount of money invested by a company on the production or

production of goods or services. The net margin is not used in this calculation. From the

standpoint of a vendor, cost is the quantity of money spent to manufacture a product or service.

A producer's expenses and profits would break even if he sold his goods at the production price,

ensuring he would not lose money on the sales. He will not, however, make a profit. The quality

of a good is also known as the price from the buyer's perspective. This is the price a vendor

costs for a good, and it covers both the manufacturing expense and the mark-up that the seller

adds to make a profit.

9

instrument used in the field of information and technology systems. It is important for

commercial companies. This is the person in charge of gathering accurate financial data for

decision-making. There are several different device implementations and they must take into

account aspects that affect how information is collected and reported. It would still be

determined by the information's intended consumers and the kinds of choices they are likely to

make. The size of the company, amount of transaction data, nature of operations, organizational

structure, and business model may all influence the system's architecture.

Accounting developed from a company's day-to-day operations in order to provide relevant data

for decision-making. Financial activity data is thus critical to an organization's life, viability, and

development. As a result, keeping a proper and reliable log of all events is a good way to get

the accounting data you need. Any corporation, whether private or governmental, is required to

keep financial records in order to evaluate its results. However, dramatic developments in

information technology and the advent of computers have had a significant impact on the

process of transmitting financial data. The first computer system was developed for accounting,

signaling a new era in the profession's history as companies rapidly welcome it to streamline

accounting records. Computers and advances in information and communication technology

(ICT) have altered the way accounting and accounting roles are carried out. The

computerization of financial accounting systems has presented challenges to the accounting

profession, as accountants now face a variety of issues, especially when performing accounting

and accounting for businesses in an electronic environment. However, it has expanded the

fraternity (scientific exposure) of accountants, allowing them to have more service levels and a

wider range of services to their customers. Auditors' schedules used to require separate stages

of preparation, but in today's constantly changing technologically-driven field of financial

statements, auditors may need to revise their conventional audit schedules and conduct checks

on a continual basis due to improvements in technology.

LO2. Apply a range of management accounting techniques

P3. Calculate costs using appropriates techniques of cost analysis to

prepare an income statement using marginal and absorption costs.

A. Price

In industry and accounting world , cost is the amount of money spent by a company to produce

something. Cost refers to the amount of money invested by a company on the production or

production of goods or services. The net margin is not used in this calculation. From the

standpoint of a vendor, cost is the quantity of money spent to manufacture a product or service.

A producer's expenses and profits would break even if he sold his goods at the production price,

ensuring he would not lose money on the sales. He will not, however, make a profit. The quality

of a good is also known as the price from the buyer's perspective. This is the price a vendor

costs for a good, and it covers both the manufacturing expense and the mark-up that the seller

adds to make a profit.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

B. Different Classification cost such as,

Fixed Cost

A quarterly cost that remains relatively stable independent of revenue or production.

While no costing is purely consistent over time of business, the concept of fixed costs is

expected in short-term cost accounting. The cost structures in organizations with a high

fixed cost system and those with a high variable cost structure are vastly different. This

distinction has an effect on the company's financial situation, as well as pricing and

profits. In comparison to high variable-cost companies, their breakeven point is typically

much higher, and their marginal gain (rate of contribution) is also much higher.

- EX- insurance, interest, rent, salaries

Variable Cost

“A variable cost is one that varies depending on the level of output or the services

rendered. There can be no variable costs where there is no manufacturing or no facilities

rendered.”

EX- Bonus, wage cost

Direct Cost

A direct cost is a price that can be traced back to a particular product or service's production.

Depreciation and maintenance costs, for example, are more difficult to assign to a particular

product and are often known as indirect costs.

-EX-Direct labor, Direct materials

Indirect Cost

Costs that are not strictly related to a cost object are known as indirect costs (such as a

particular project, facility, function or product). Indirect costs can be constant or contingent, but

certain overhead costs are direct costs that can be directly traced to a project.

-EX—Indirect labor, indirect material

C. Different Costing system such as,

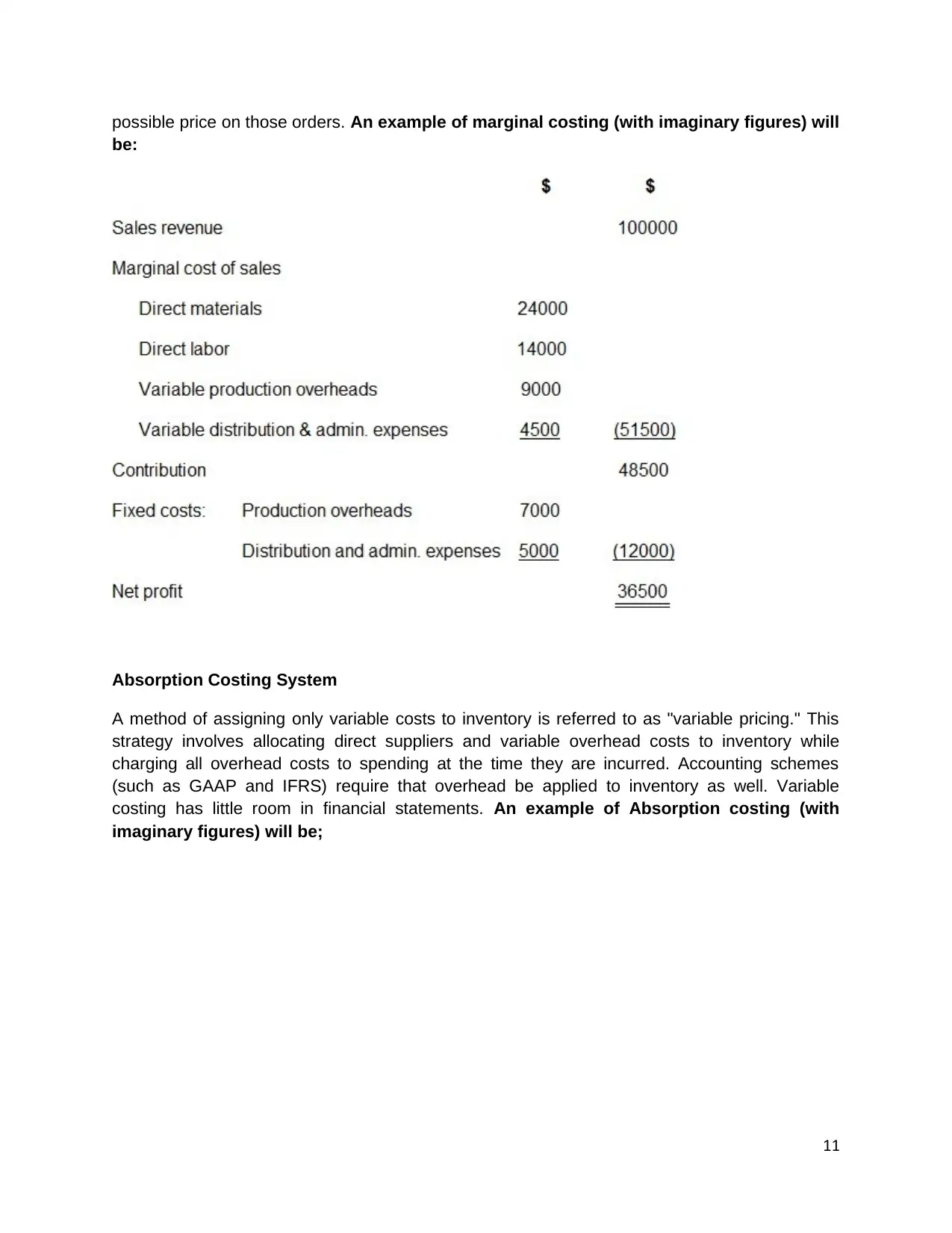

Marginal Costing System

The marginal cost of one additional unit of output is referred to as marginal cost. The concept is

used to determine an organization's optimum production quantity, which is the lowest cost of

generating additional units. If an organization succeeds in this "sweet spot," its profits will be

maximized. The theory is often used to determine product prices as buyers negotiate the lowest

10

Fixed Cost

A quarterly cost that remains relatively stable independent of revenue or production.

While no costing is purely consistent over time of business, the concept of fixed costs is

expected in short-term cost accounting. The cost structures in organizations with a high

fixed cost system and those with a high variable cost structure are vastly different. This

distinction has an effect on the company's financial situation, as well as pricing and

profits. In comparison to high variable-cost companies, their breakeven point is typically

much higher, and their marginal gain (rate of contribution) is also much higher.

- EX- insurance, interest, rent, salaries

Variable Cost

“A variable cost is one that varies depending on the level of output or the services

rendered. There can be no variable costs where there is no manufacturing or no facilities

rendered.”

EX- Bonus, wage cost

Direct Cost

A direct cost is a price that can be traced back to a particular product or service's production.

Depreciation and maintenance costs, for example, are more difficult to assign to a particular

product and are often known as indirect costs.

-EX-Direct labor, Direct materials

Indirect Cost

Costs that are not strictly related to a cost object are known as indirect costs (such as a

particular project, facility, function or product). Indirect costs can be constant or contingent, but

certain overhead costs are direct costs that can be directly traced to a project.

-EX—Indirect labor, indirect material

C. Different Costing system such as,

Marginal Costing System

The marginal cost of one additional unit of output is referred to as marginal cost. The concept is

used to determine an organization's optimum production quantity, which is the lowest cost of

generating additional units. If an organization succeeds in this "sweet spot," its profits will be

maximized. The theory is often used to determine product prices as buyers negotiate the lowest

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

possible price on those orders. An example of marginal costing (with imaginary figures) will

be:

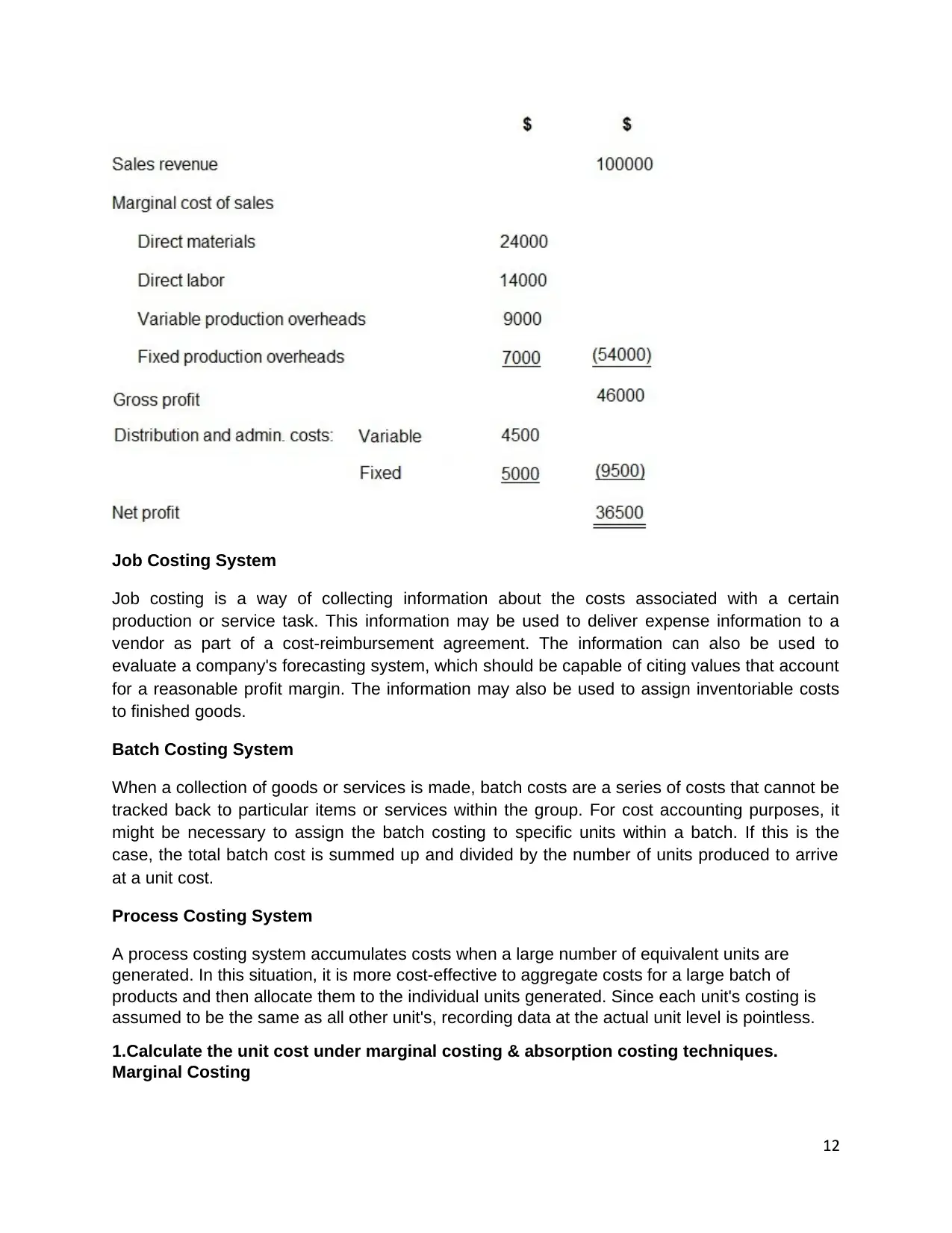

Absorption Costing System

A method of assigning only variable costs to inventory is referred to as "variable pricing." This

strategy involves allocating direct suppliers and variable overhead costs to inventory while

charging all overhead costs to spending at the time they are incurred. Accounting schemes

(such as GAAP and IFRS) require that overhead be applied to inventory as well. Variable

costing has little room in financial statements. An example of Absorption costing (with

imaginary figures) will be;

11

be:

Absorption Costing System

A method of assigning only variable costs to inventory is referred to as "variable pricing." This

strategy involves allocating direct suppliers and variable overhead costs to inventory while

charging all overhead costs to spending at the time they are incurred. Accounting schemes

(such as GAAP and IFRS) require that overhead be applied to inventory as well. Variable

costing has little room in financial statements. An example of Absorption costing (with

imaginary figures) will be;

11

Job Costing System

Job costing is a way of collecting information about the costs associated with a certain

production or service task. This information may be used to deliver expense information to a

vendor as part of a cost-reimbursement agreement. The information can also be used to

evaluate a company's forecasting system, which should be capable of citing values that account

for a reasonable profit margin. The information may also be used to assign inventoriable costs

to finished goods.

Batch Costing System

When a collection of goods or services is made, batch costs are a series of costs that cannot be

tracked back to particular items or services within the group. For cost accounting purposes, it

might be necessary to assign the batch costing to specific units within a batch. If this is the

case, the total batch cost is summed up and divided by the number of units produced to arrive

at a unit cost.

Process Costing System

A process costing system accumulates costs when a large number of equivalent units are

generated. In this situation, it is more cost-effective to aggregate costs for a large batch of

products and then allocate them to the individual units generated. Since each unit's costing is

assumed to be the same as all other unit's, recording data at the actual unit level is pointless.

1.Calculate the unit cost under marginal costing & absorption costing techniques.

Marginal Costing

12

Job costing is a way of collecting information about the costs associated with a certain

production or service task. This information may be used to deliver expense information to a

vendor as part of a cost-reimbursement agreement. The information can also be used to

evaluate a company's forecasting system, which should be capable of citing values that account

for a reasonable profit margin. The information may also be used to assign inventoriable costs

to finished goods.

Batch Costing System

When a collection of goods or services is made, batch costs are a series of costs that cannot be

tracked back to particular items or services within the group. For cost accounting purposes, it

might be necessary to assign the batch costing to specific units within a batch. If this is the

case, the total batch cost is summed up and divided by the number of units produced to arrive

at a unit cost.

Process Costing System

A process costing system accumulates costs when a large number of equivalent units are

generated. In this situation, it is more cost-effective to aggregate costs for a large batch of

products and then allocate them to the individual units generated. Since each unit's costing is

assumed to be the same as all other unit's, recording data at the actual unit level is pointless.

1.Calculate the unit cost under marginal costing & absorption costing techniques.

Marginal Costing

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 45

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.