Accounting for Managers Assignment 2: Financial Analysis Report

VerifiedAdded on 2021/06/17

|7

|1354

|25

Report

AI Summary

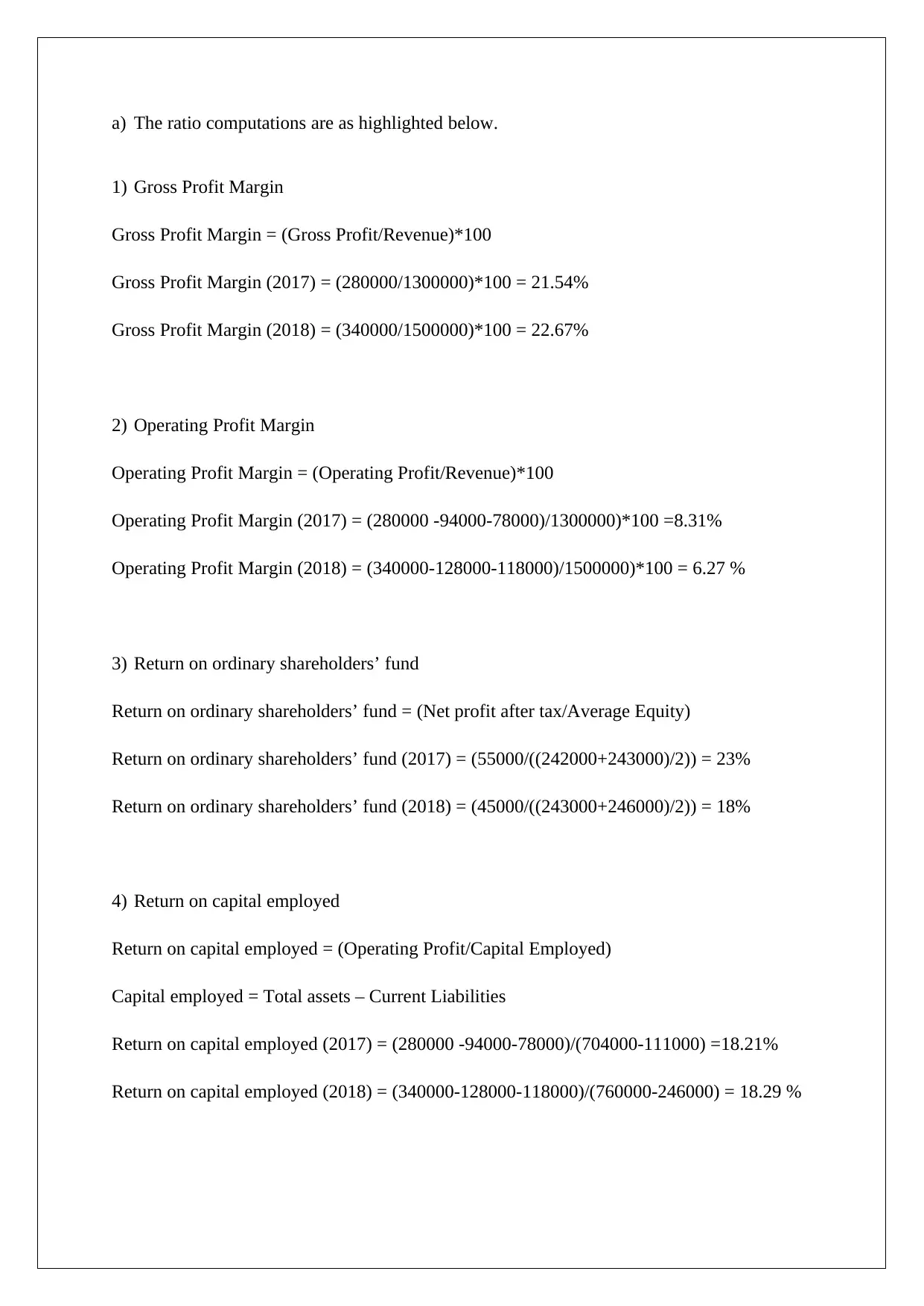

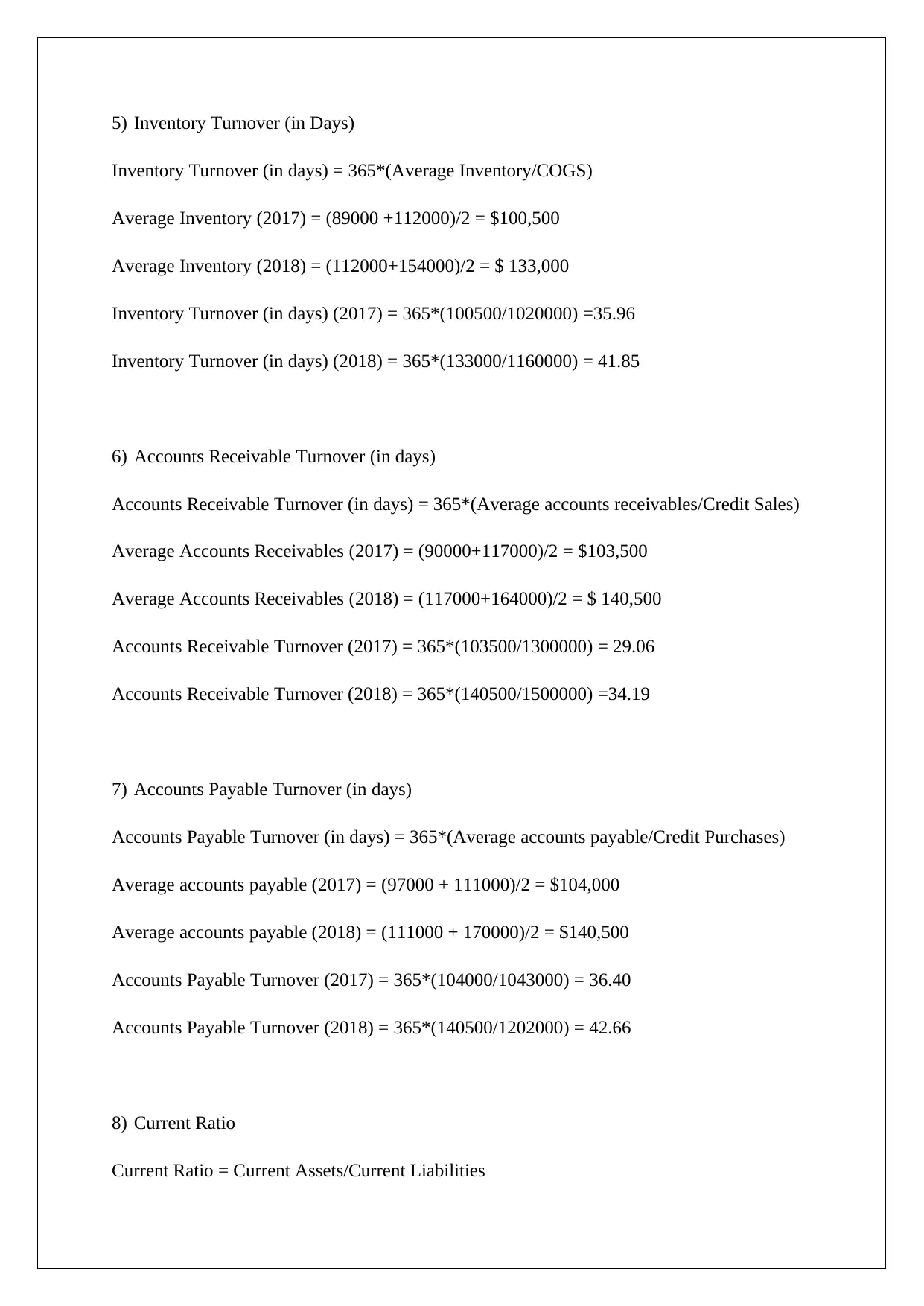

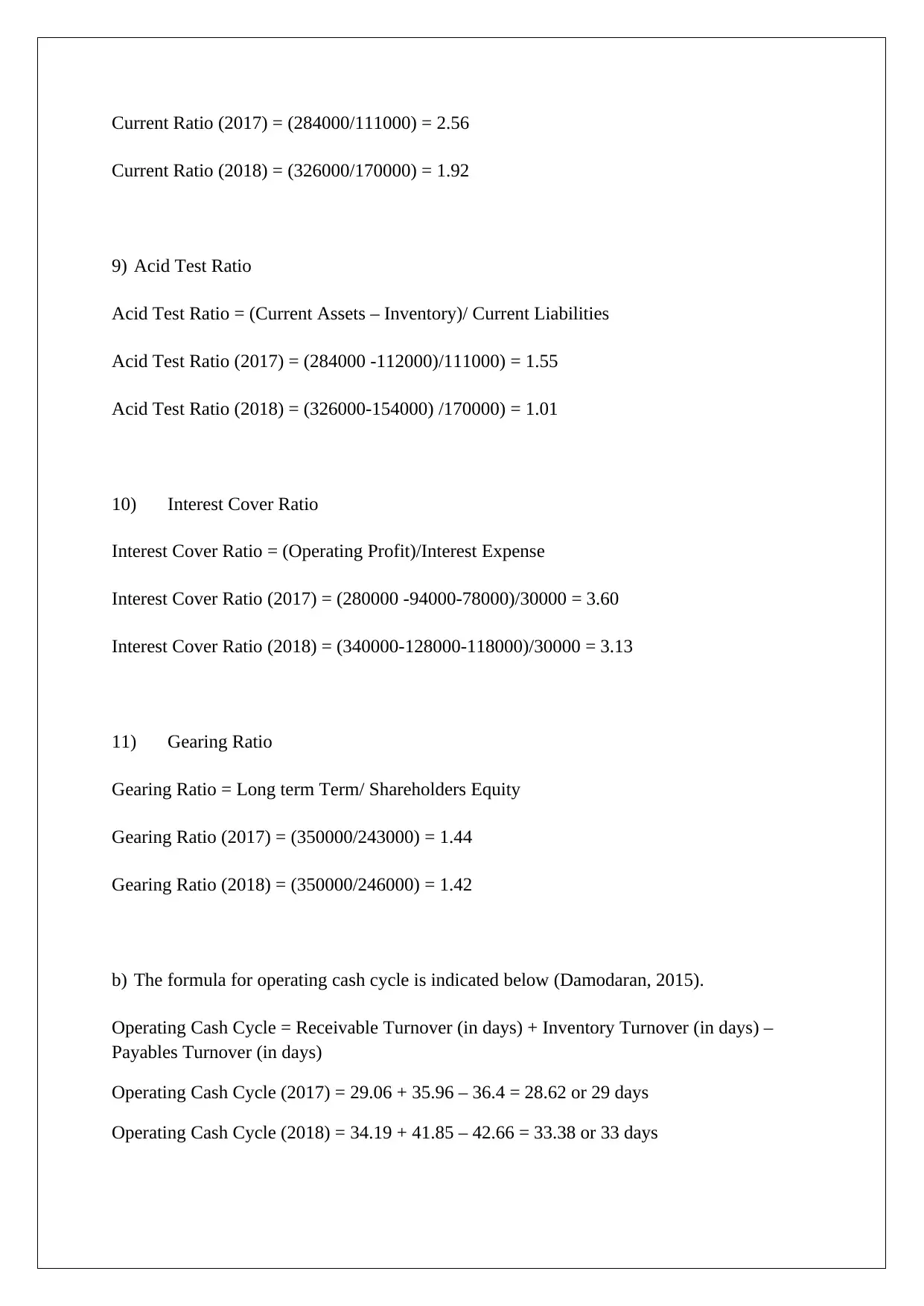

This report presents a comprehensive financial ratio analysis of Macca Pty Ltd, examining its performance over the years 2017 and 2018. The analysis includes the calculation and interpretation of various ratios, such as gross profit margin, operating profit margin, return on equity, return on capital employed, inventory turnover, accounts receivable turnover, accounts payable turnover, current ratio, acid test ratio, interest cover ratio, and gearing ratio. The report assesses the company's profitability, efficiency, liquidity, and gearing, highlighting trends and potential areas of concern. The findings reveal insights into the company's financial health, including improvements in gross profit margin, but declines in operating margins, and shifts in efficiency and liquidity metrics. The report concludes with a discussion of the operating cash cycle and provides references to relevant financial literature. This assignment is available on Desklib, a platform offering AI-powered study tools for students.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.