Financial Analysis and Ratio Calculations: ACC00724 Assignment 2

VerifiedAdded on 2022/11/18

|7

|1252

|208

Homework Assignment

AI Summary

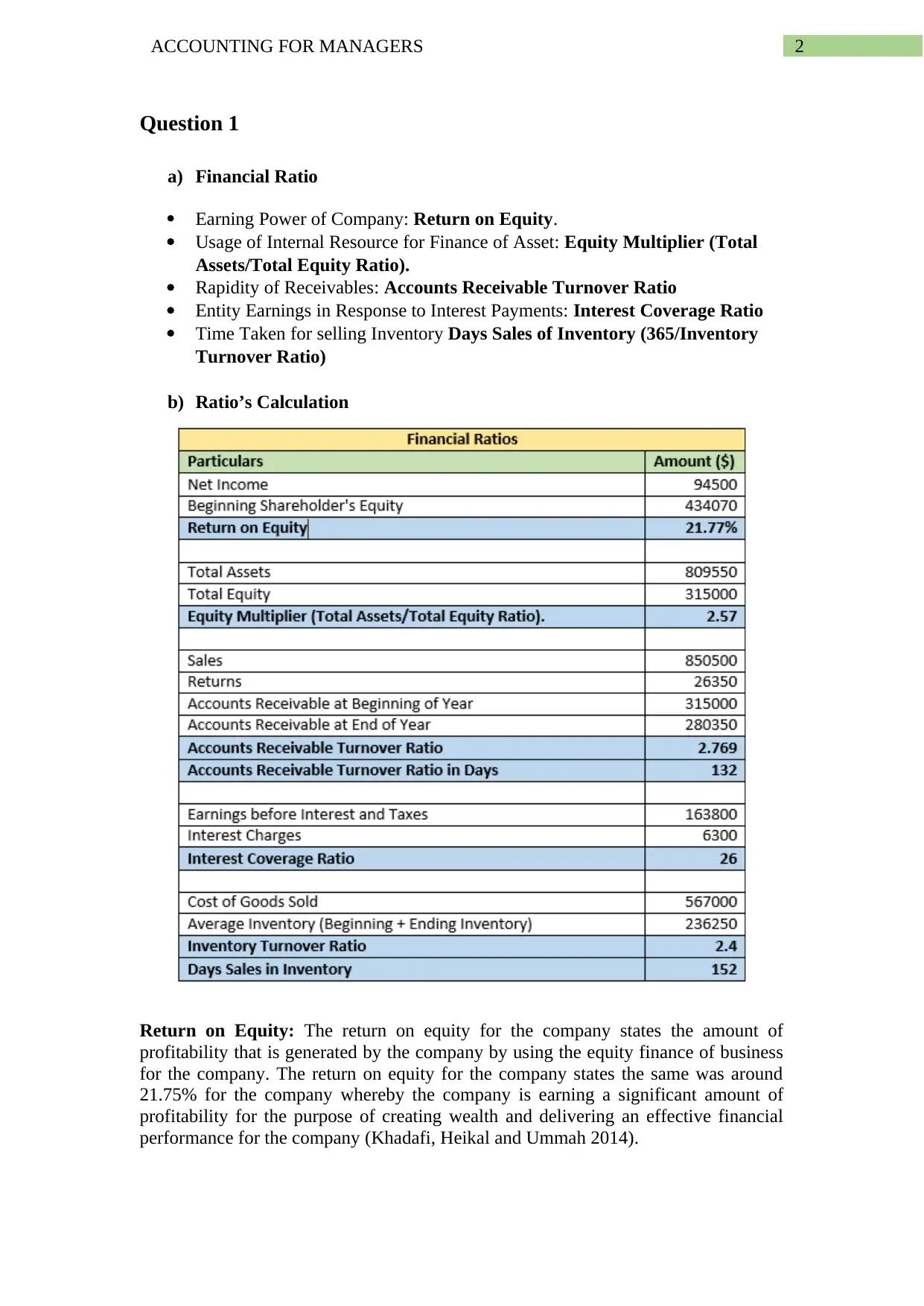

This document presents a comprehensive solution to Assignment 2 in Accounting for Managers (ACC00724), focusing on financial statement analysis. The assignment encompasses the calculation and interpretation of various financial ratios, including Return on Equity, Equity Multiplier, Accounts Receivable Turnover, Interest Coverage, and Inventory Turnover, to assess a company's earning power, resource utilization, and operational efficiency. It further delves into break-even analysis, calculating the break-even point, determining target profit enrollment, and exploring multi-product break-even scenarios. Additionally, the solution covers predetermined overhead rate calculations, overhead allocation to jobs, and the factors influencing the selection of an allocation base. The assignment provides detailed calculations, interpretations, and discussions, offering a robust understanding of key accounting concepts and their practical application in financial management.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.