Accounting for Managers (ACC00724) Assignment 2 Solution Analysis

VerifiedAdded on 2023/06/08

|11

|1212

|390

Homework Assignment

AI Summary

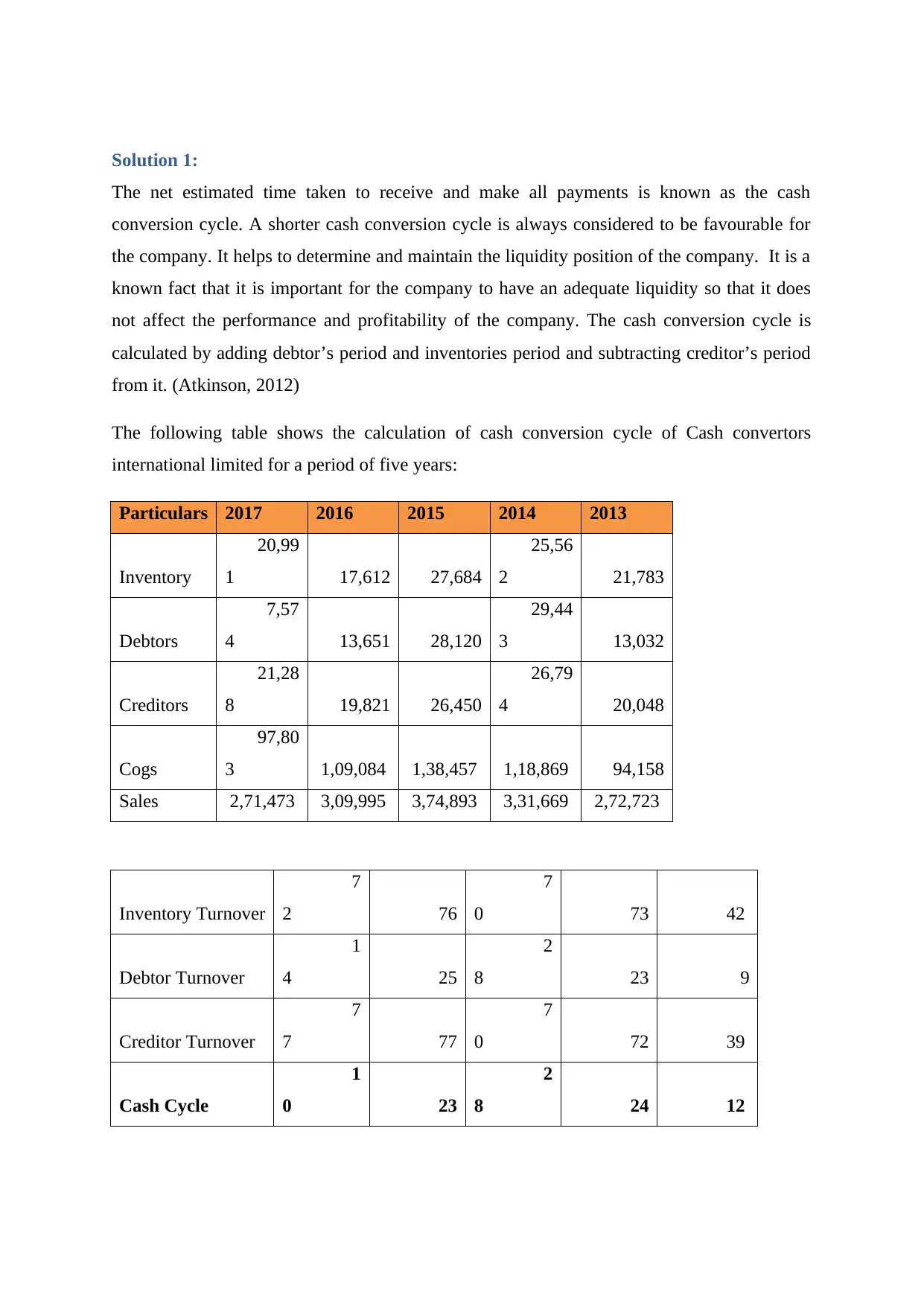

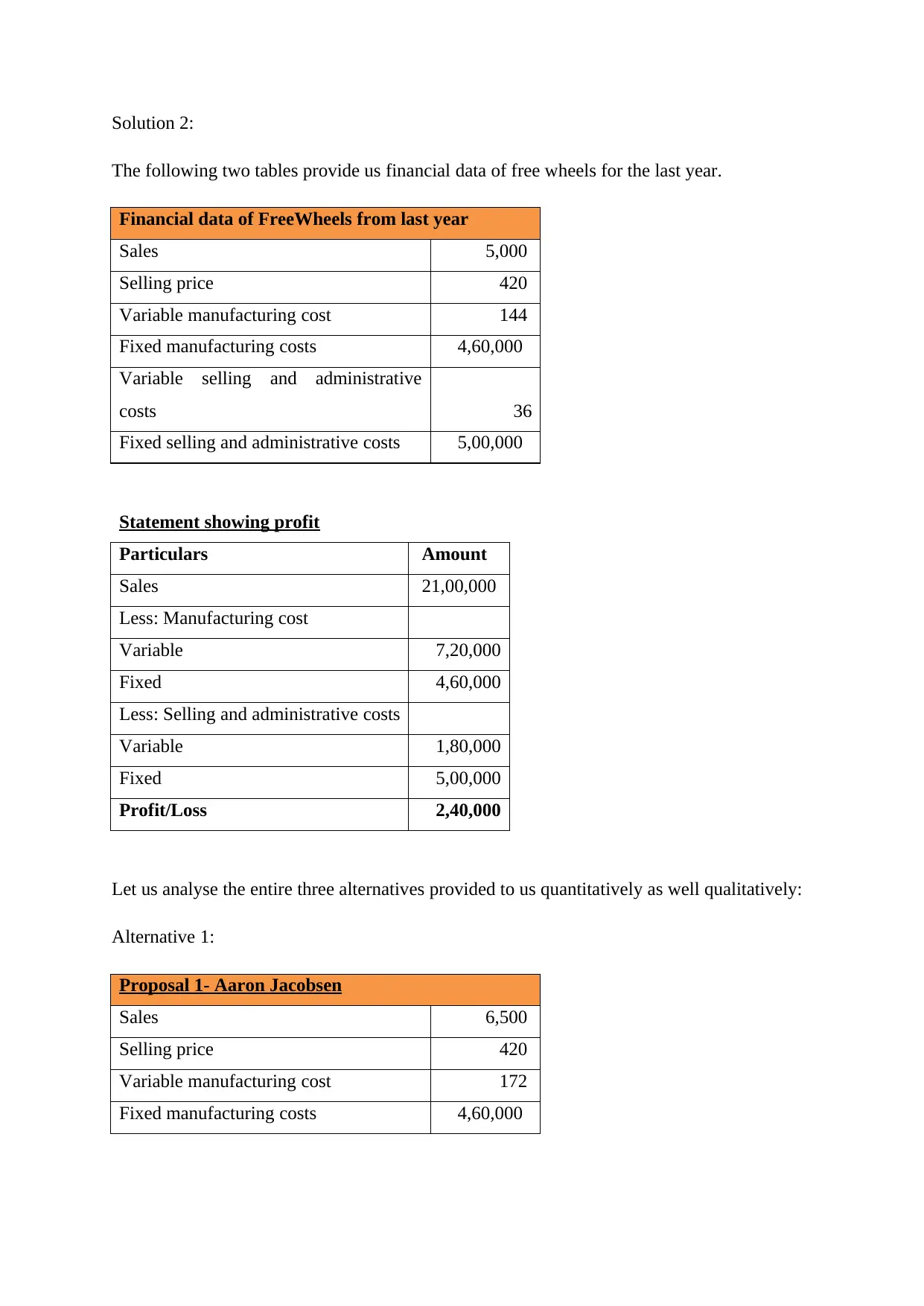

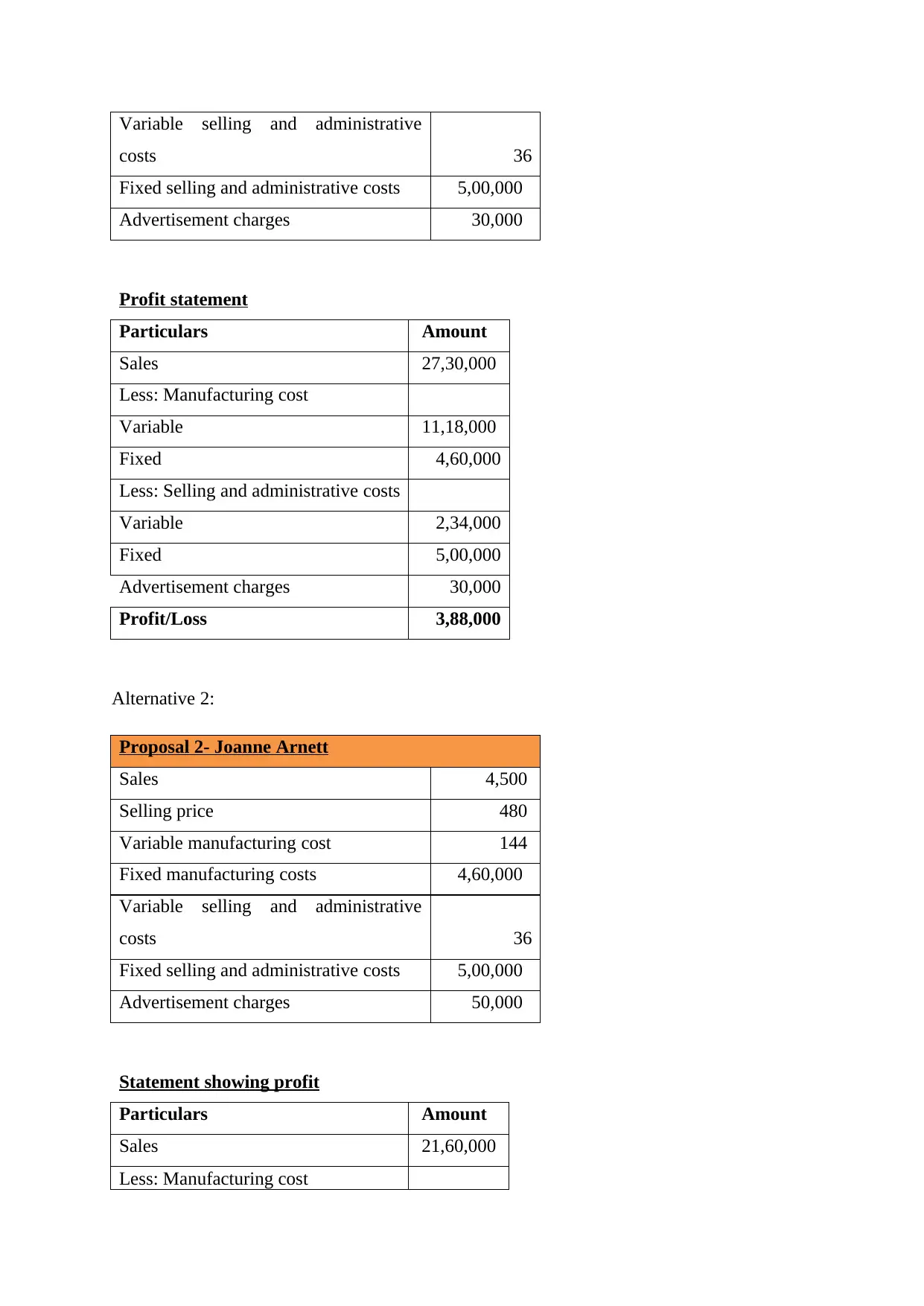

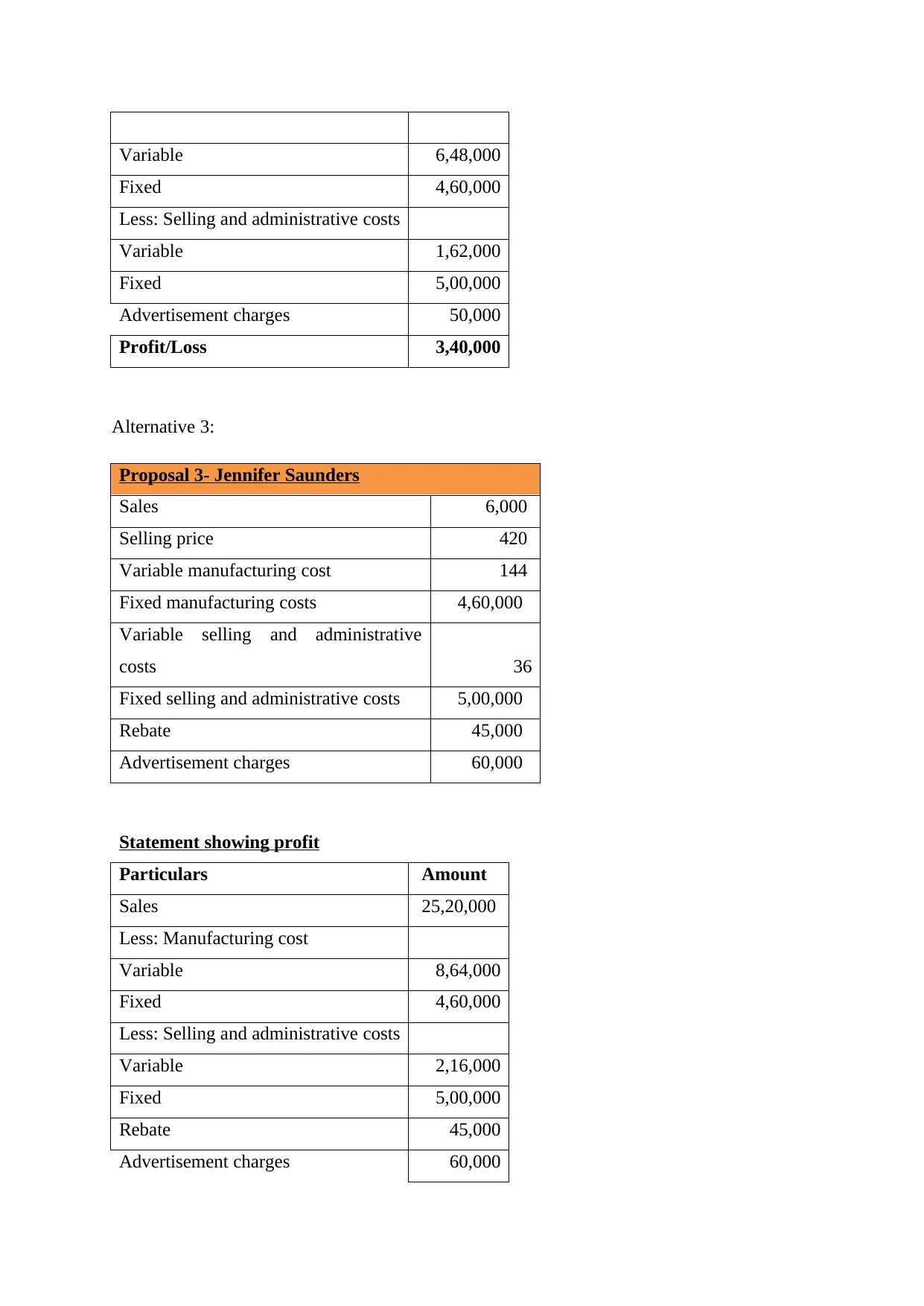

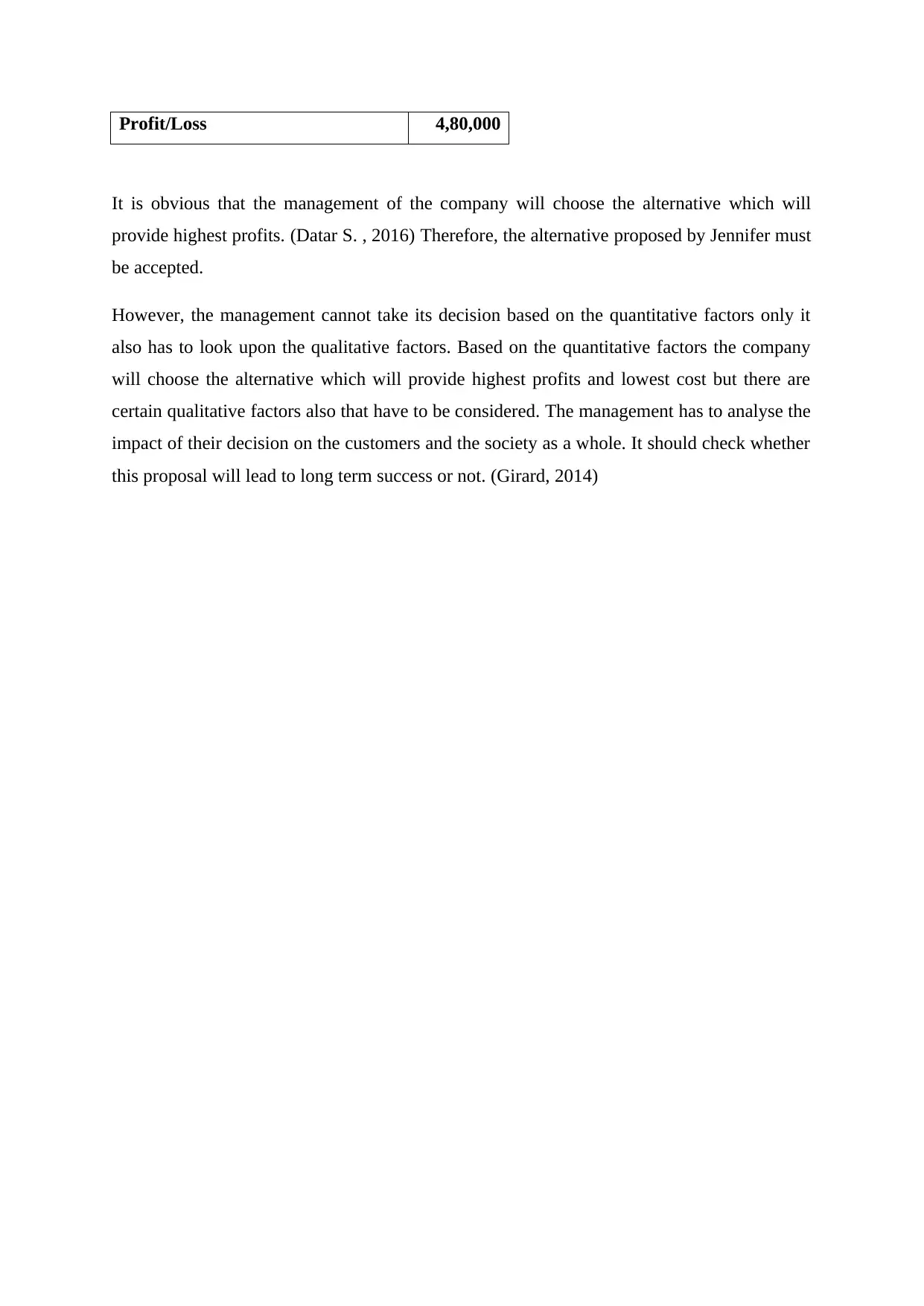

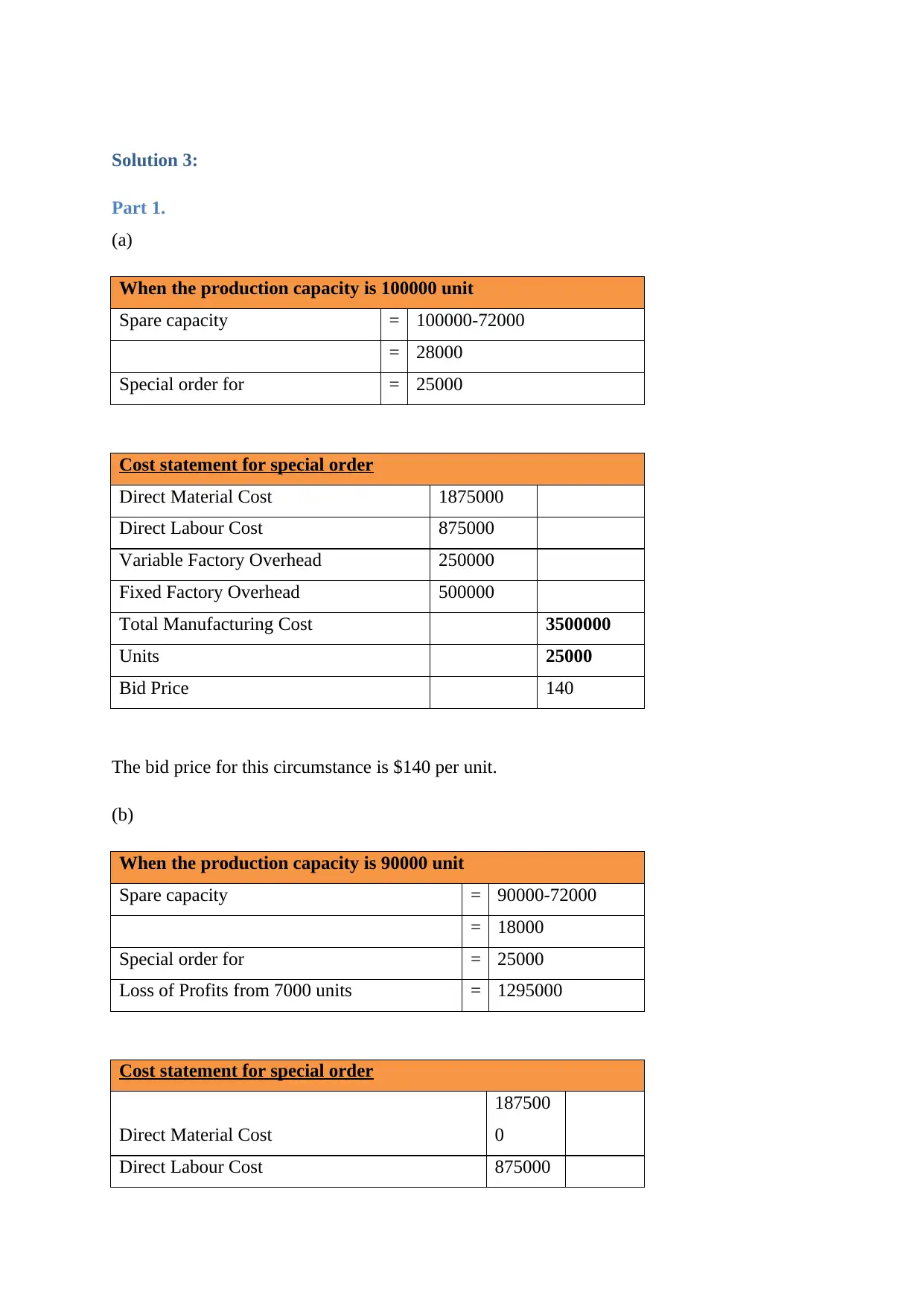

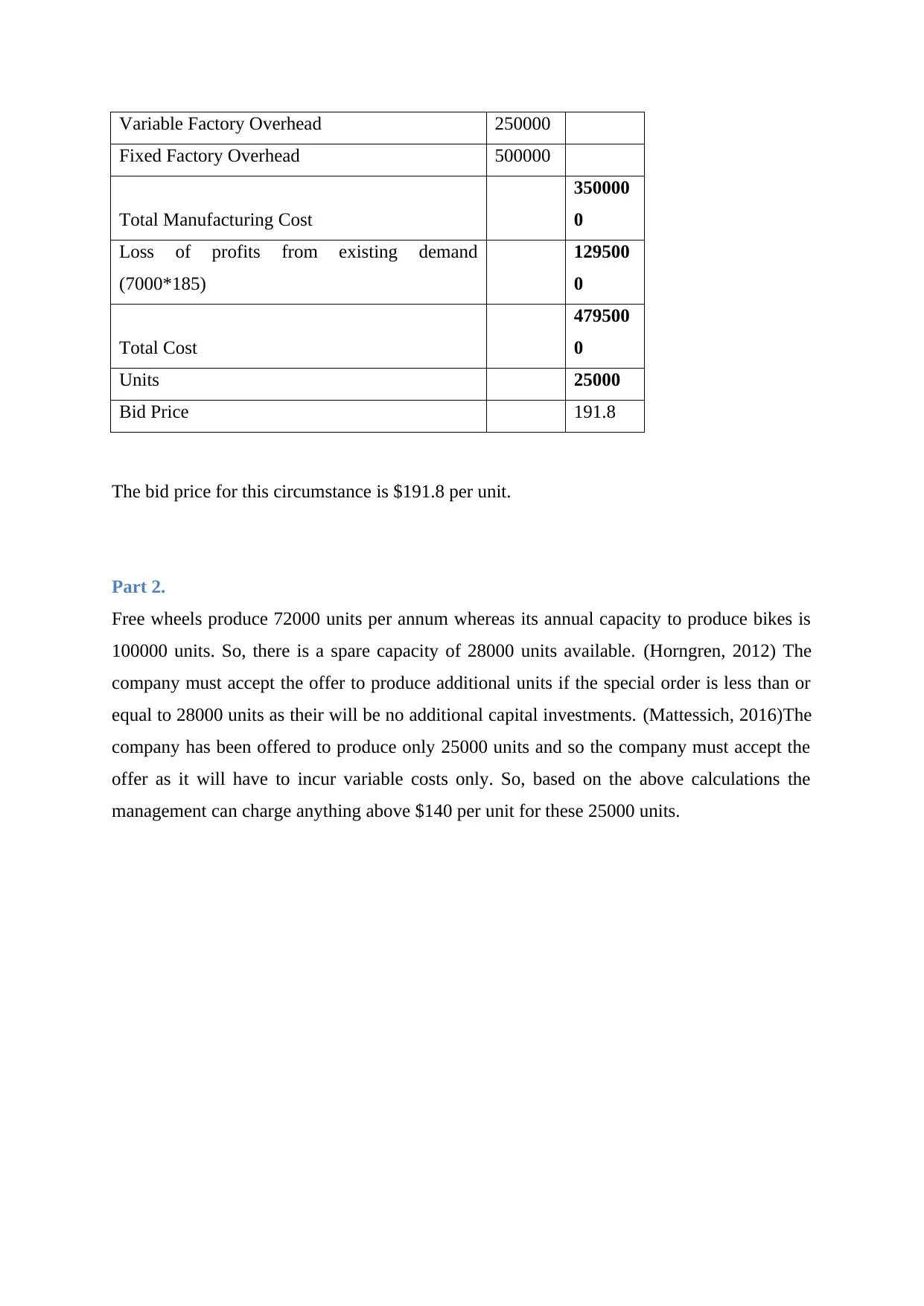

This document presents a detailed solution to an Accounting for Managers assignment, addressing key concepts such as cash conversion cycles, financial data analysis, and special order pricing. The solution begins by calculating the cash conversion cycle for a company over a five-year period, analyzing trends and liquidity positions. It then delves into a profitability analysis based on financial data from FreeWheels, evaluating three alternative proposals and recommending the best option based on both quantitative and qualitative factors. Finally, the solution explores special order pricing, calculating bid prices under different production capacity scenarios and determining the optimal pricing strategy for the company. The document also includes a bibliography of relevant sources.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.