Financial Capital Analysis and Valuation of Alam.com Venture

VerifiedAdded on 2022/10/17

|8

|1324

|329

Report

AI Summary

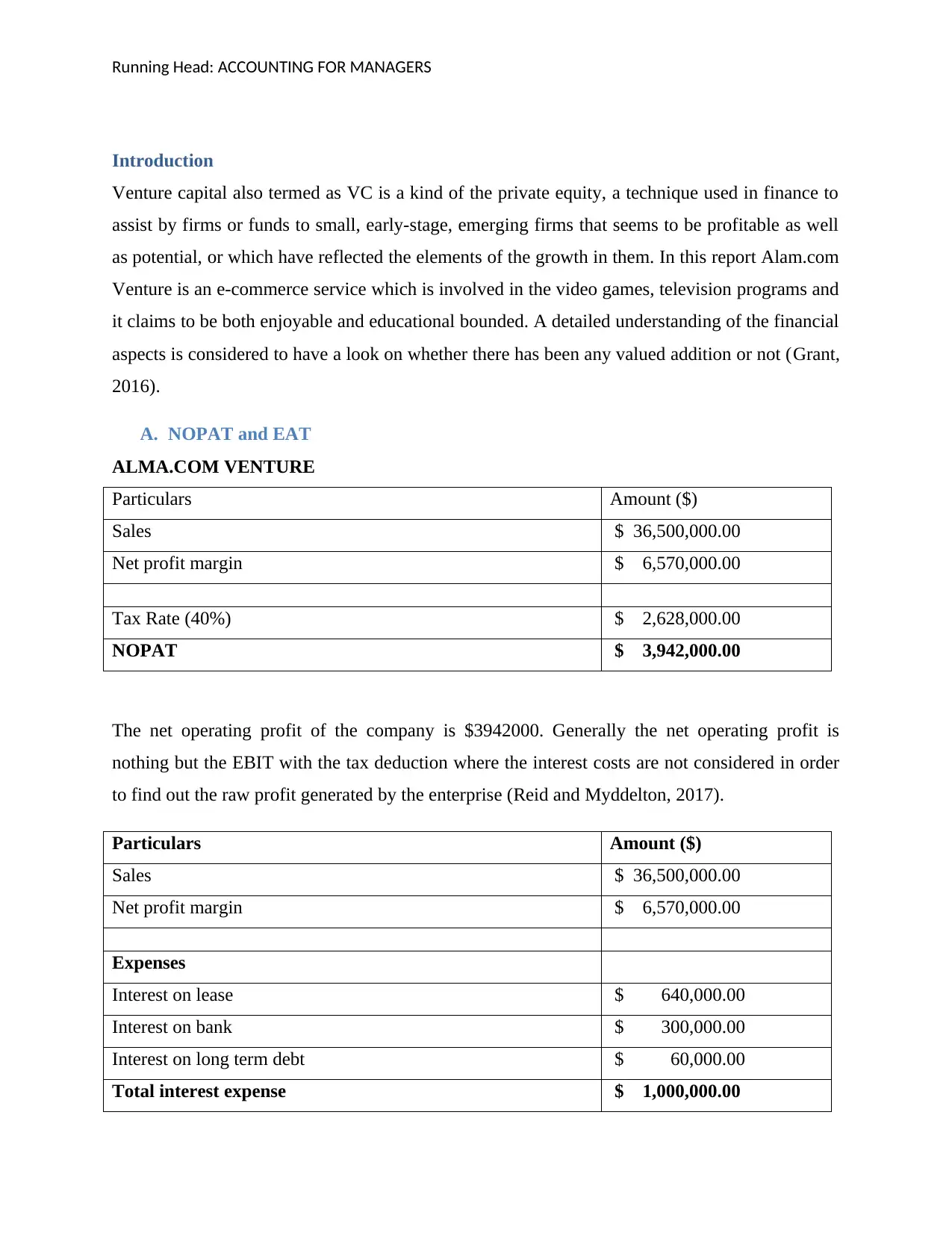

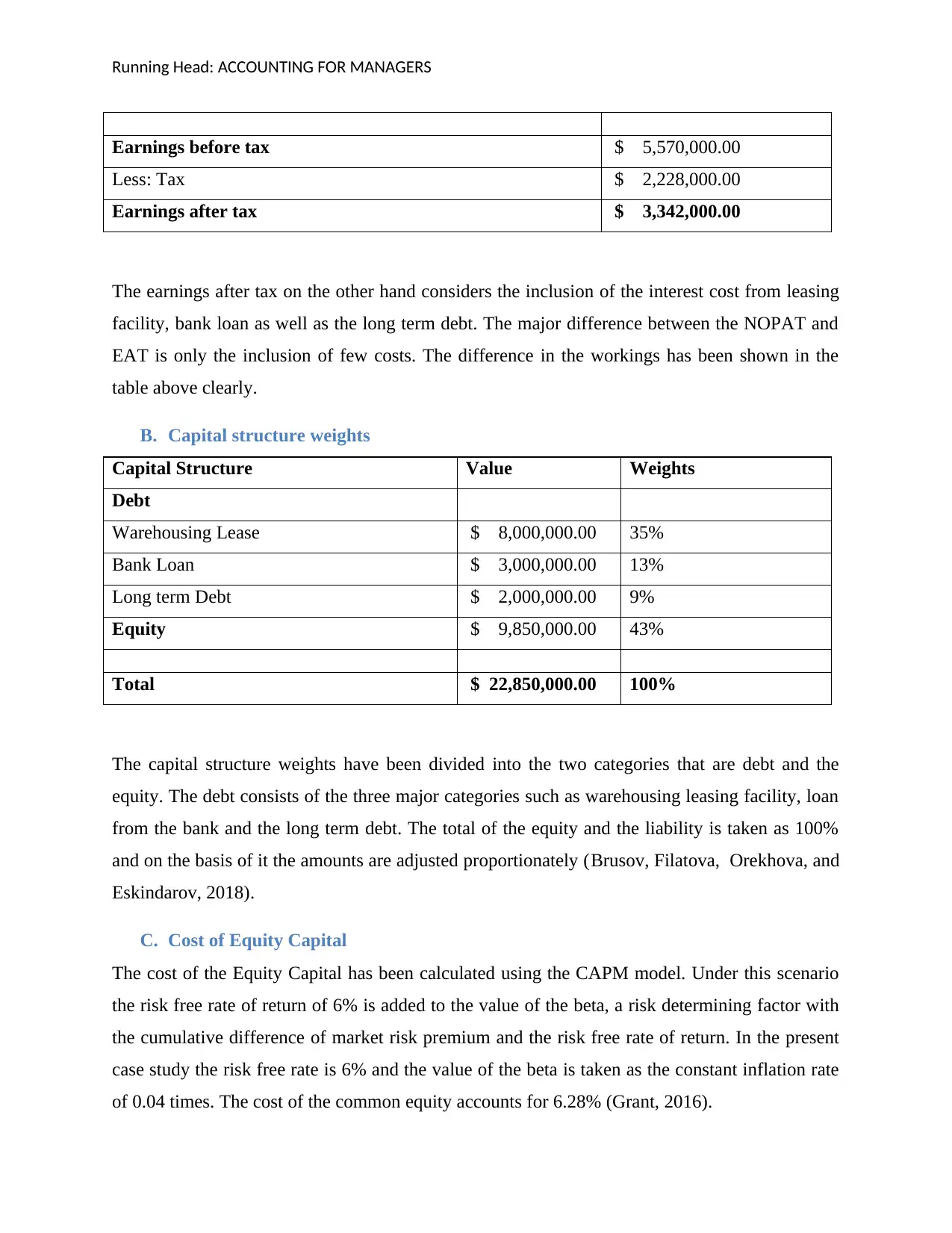

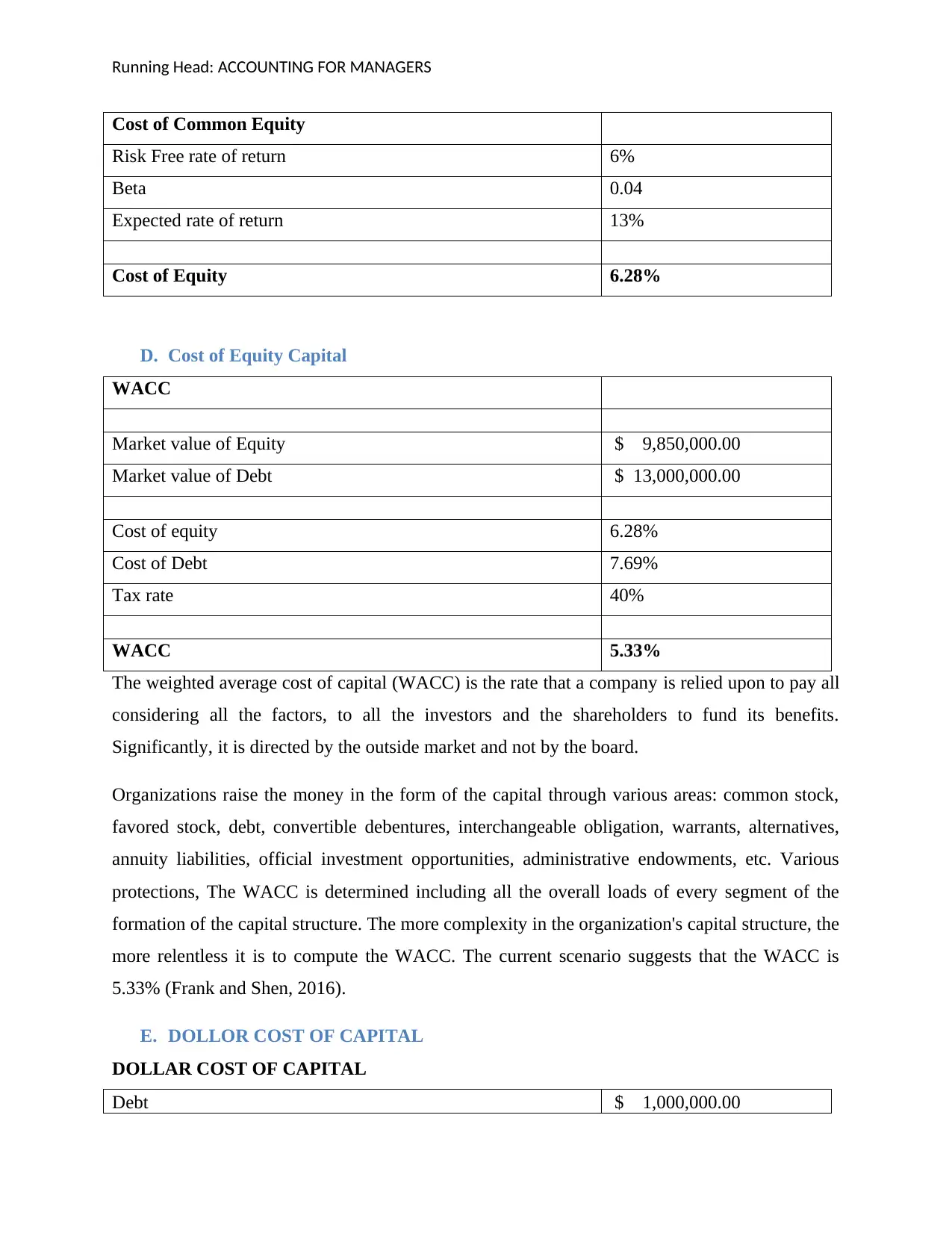

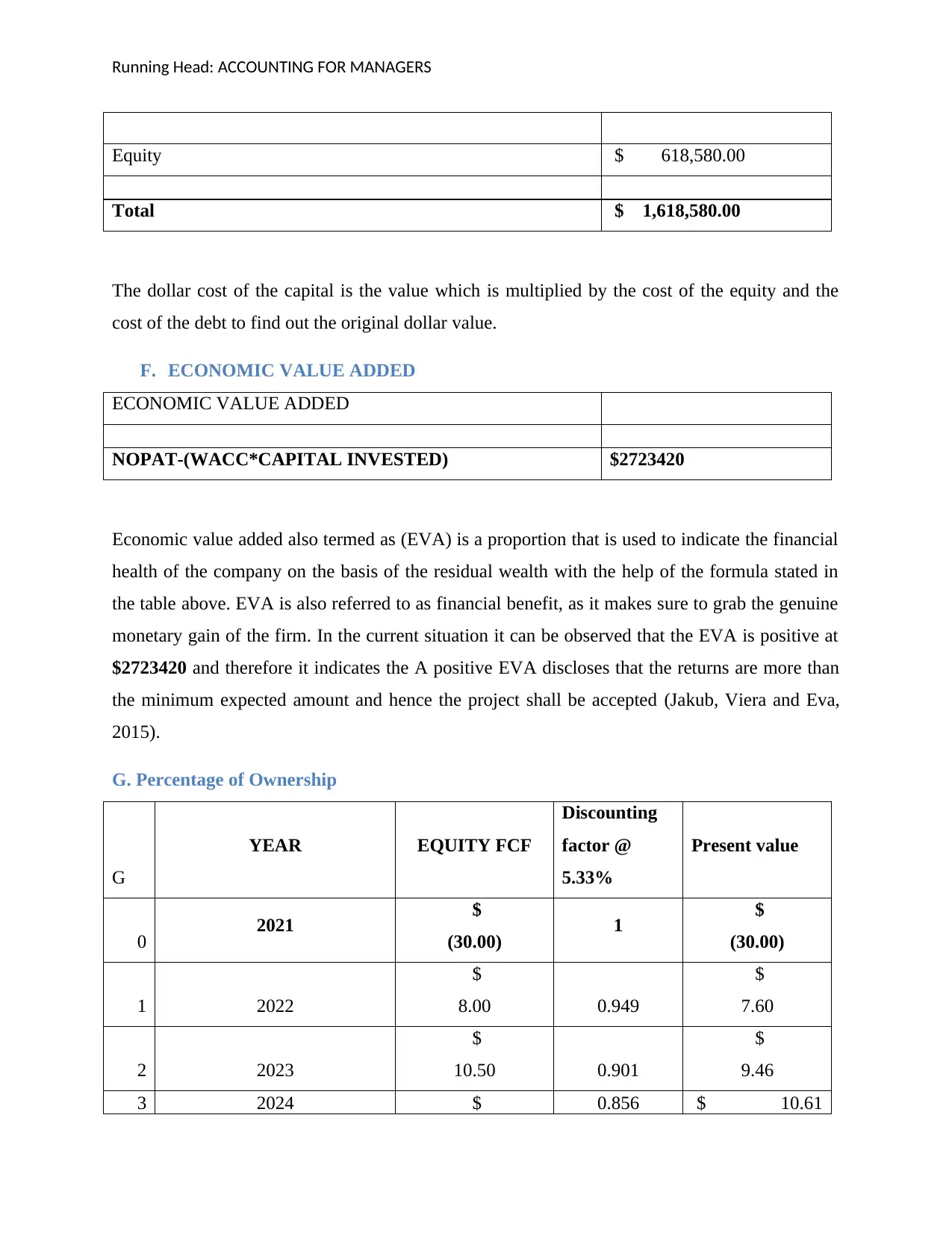

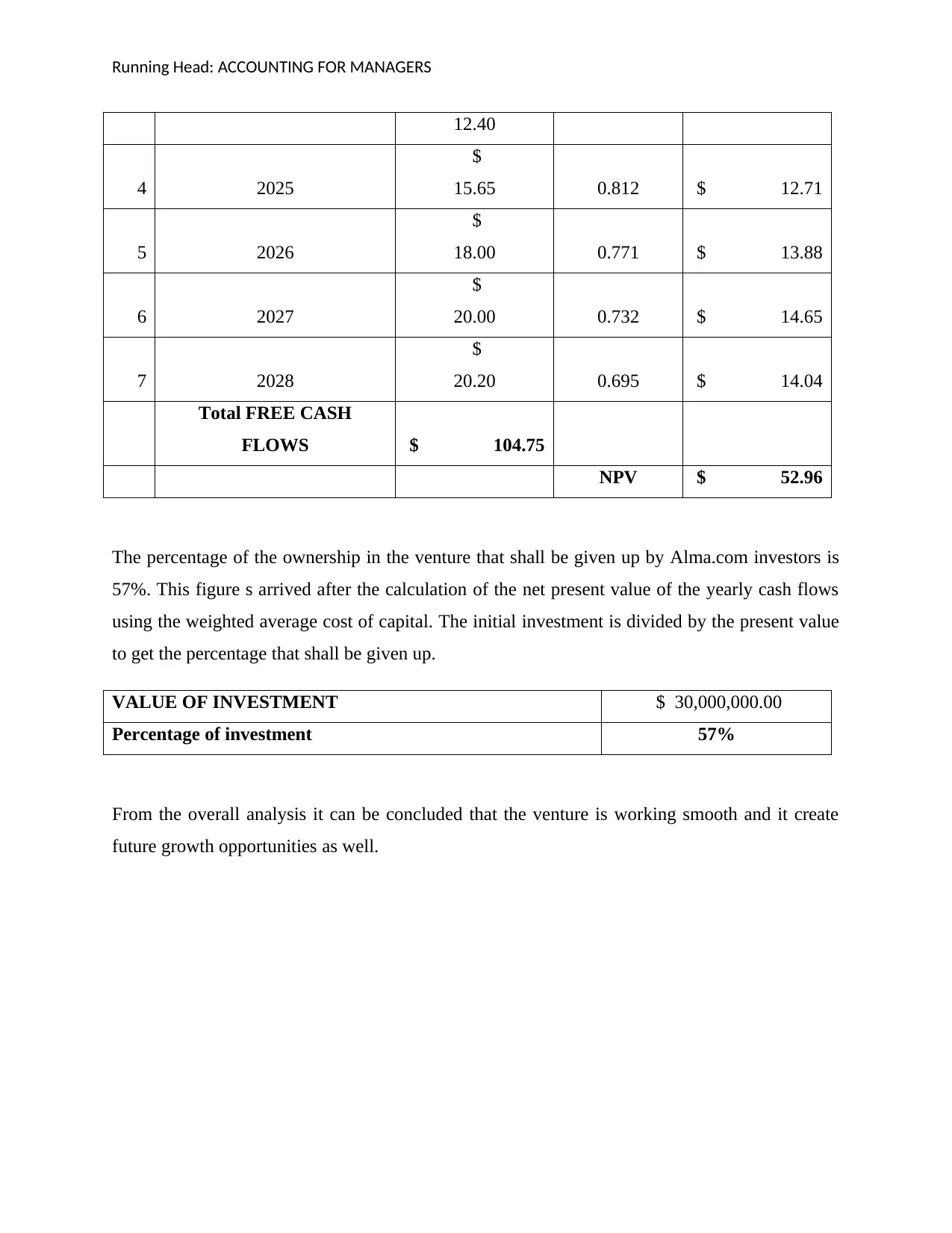

This report analyzes the financial aspects of Alam.com Venture, an e-commerce service involved in video games and television programs. It begins by calculating NOPAT and EAT to assess profitability, considering sales, expenses, and tax rates. The report then delves into capital structure, determining the weights of debt and equity components. The cost of equity capital is calculated using the CAPM model, and the weighted average cost of capital (WACC) is determined to evaluate the overall cost of financing. Furthermore, the report calculates the dollar cost of capital and the economic value added (EVA) to gauge the company's financial health. Finally, it determines the percentage of ownership in the venture that should be given up by investors, based on a net present value analysis of future cash flows. The analysis concludes that the venture is performing well and presents future growth opportunities.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.